MNI EUROPEAN MARKETS ANALYSIS: Equity Losses In Asia Pac

- Risk off has continued, with US equity futures not too far from the 50-day EMA support this afternoon. This follows Thursday cash losses in US markets, with credit concerns cited. Regional Asia Pac equities have seen larger losses, with Hong Kong stocks falling sharply (led by the tech side).

- US Tsy yields have extended lower, which has aided USD/JPY downside, breaking under 150.00. AUD has underperformed. Gold has been volatile but is tracking close to fresh record highs.

- Looking ahead it is fairly quiet data wise, but we do have BOE, ECB and Fed (before the blackout period) speak to round out the week. The BoJ Deputy Governor is also due to speak.

MARKETS

US TSYS: Yields Lower, 10-Yr Resetting Recent Ranges

- UST's strength overnight followed through into the Asia trading day with TYZ5 up +06 at 113-30+ after touching near term highs overnight. The NIKKEI is down as other regional bourses start their trading day, watching to see if the lead in from the US follows through.

- US 2-Yr is down further at 3.40% (-2bps today)

- US 5-Yr is at 3.52% (-2.5bps)

- US 10-yr is consolidating below 4.00% with a further rally to 3.94%. The key will be whether it can hold below 4% overnight and reset recent trading ranges.

- US 30-yr is down -1bps at 4.55% and is back to levels of April due the peak of the trade war volatility.

- Data out tonight include housing starts and Import and Export price index.

- The rally in bonds overnight is being attributed to regional bank fears with two banks reported exposure to the sub prime lender Tricolor Holdings which has collapsed. Looking at the current discussions on exposures to the balance sheets of these banks it appears manageable and the market will watch closely tonight for further details.

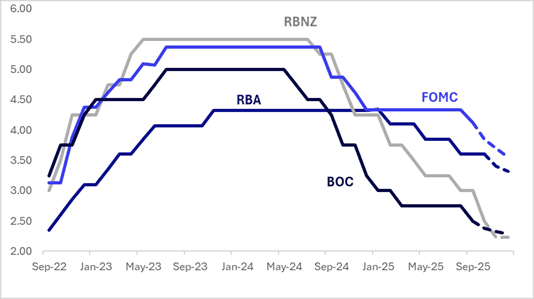

STIR: $-Bloc Pricing Softer Over Past Week, Led By AUS & US

Interest rate expectations across the $-bloc have softened over the past week, led by Australia (-15bps) and the US (-9bps), with New Zealand (-3bps) and Canada (-2bps) lagging.

- In Australia, Thursday’s data showed that labour market conditions eased in September. Most notable was the spike in the unemployment rate to 4.5%, versus 4.3% (4.3% was the Aug outcome). The participation rate rose to 67.0%, versus 66.8% forecast, so that played a role. Job growth of +14.9k was close to the +20k forecast.

- The generally softer Q3 is likely to drive RBA revisions in the near-term, but it may want to see further developments before changing its medium-term view. There are now signs that job growth can’t keep up with increases in the labour force, resulting in higher unemployment and that any additional demand is being met by increasing hours. This makes a November rate cut more likely, but given the RBA’s inflation concerns, Q3 CPI on 29 October remains the key input.

- The next key regional events are the FOMC and BOC policy decisions on October 29. Market pricing currently implies an 108% probability of a 25bps cut by the Fed and a 58% chance of easing by the BOC.

- Looking ahead to December 2025, current market-implied policy rates cumulative expected easing is as follows: US (FOMC): 3.55%, -58bps; Canada (BOC): 2.28%, -22bps; Australia (RBA): 3.32%, -28bps; and New Zealand (RBNZ): 2.23%, -27bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Holding Richer Despite BOJ Words, BoJ Uchida Speech Due

JGB futures are sharply stronger, +43 compared to settlement levels.

- (MNI Policy) Bank of Japan officials are watching for signs that some businesses are struggling to pass on cost pressures to selling prices as consumer spending lacks momentum amid persistent high prices and negative real wages, a development that could further complicate the central bank’s efforts to normalise policy smoothly, MNI understands.

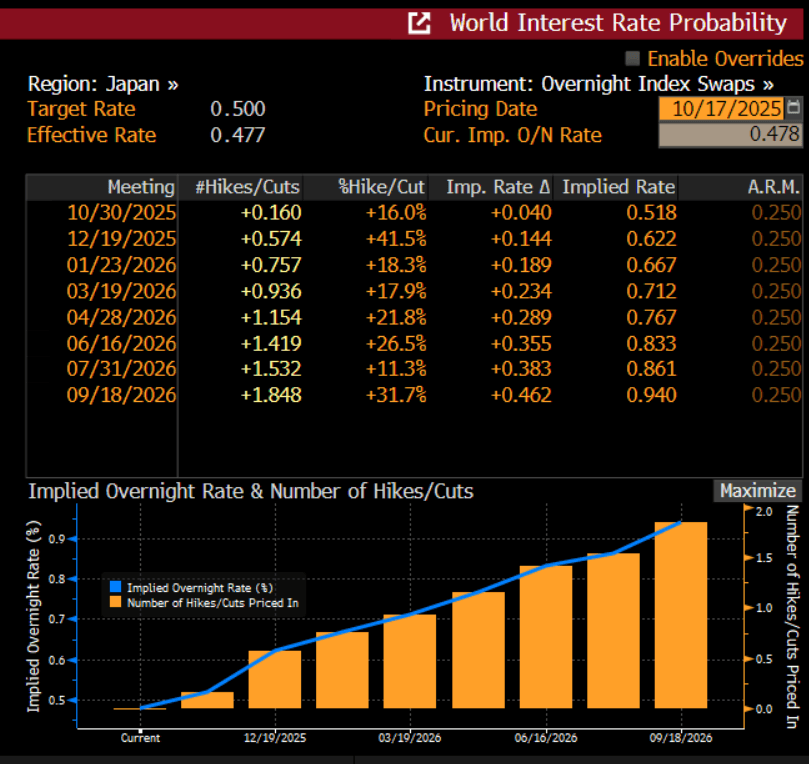

- (Bloomberg) “Bank of Japan Governor Kazuo Ueda indicated that the bank will continue tightening if confidence in achieving its economic outlook strengthens — keeping the door open for a near-term interest-rate hike.

- Markets doubt the BOJ will raise its 0.5% policy rate at the Oct. 30 meeting, pricing in a 42% chance of a hike at the Dec. 19 session, with a 0.75% rate not fully expected until at least April. (see chart)

- Cash US tsys are 3-4bps richer in today’s Asia-Pac session after yesterday’s solid gains.

- Cash JGBs are 1-4bps richer across benchmarks, with the futures linked 7-year leading.

- 2/30 yield curve is closing in on near support around 220bps.

- Swap rates are 1-3bps lower.

- On Monday, the local calendar will be empty apart from a speech from BOJ Board Takata. Speech by BOJ Deputy Governor Uchida is due later today.

Bloomberg Finance LP

JAPAN DATA: Offshore Investors Continue To Return To Local Stocks

Japan weekly investment flows saw continued net buying of local stocks by offshore investors. In the past two weeks, this investor has bought over ¥4.3trln of local stocks, partially reversing the recent outflows seen since mid August. This follows the break higher in local stock indices in recent weeks, led by tech optimism/and yen weakness. These trends have faltered somewhat though in recent sessions. Stocks bourses in Japan remain close to recent record highs, with offshore investors still likely to be overweigh given aggregate inflows in the past 6 months.

- Offshore investors continued to buy local bonds, after strong inflows in the prior week. Still, aggregate inflows are only marginally positive for recent months.

- In terms of outbound Japan flows, we saw local investors buying bonds, although only partially reversed the previous week's net selling. Global bond returns have firmed this week, given downside in US Tsy yields (break 4.00% on the 10yr).

- We also saw buying of offshore stocks, but local investors remain cautious on global stocks, with cumulative outflows seen in recent weeks.

Table: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Oct 10 | Prior Week |

| Foreign Buying Japan Stocks | 1885.0 | 2476.1 |

| Foreign Buying Japan Bonds | 199.4 | 1258.6 |

| Japan Buying Foreign Bonds | 596.4 | -923.0 |

| Japan Buying Foreign Stocks | 59.3 | -1450.2 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Sharply Stronger As Post-Jobs Rally Extends

ACGBs (YM +8.5 & XM +6.5) are richer and at session highs. Today's move currently leaves futures 11-16bps stronger than yesterday's pre-jobs data levels, with the YMXM curve 5bps steeper. However, the curve remains near its flattest point since April, having broken out of a well-defined range earlier in the year.

- Cash US tsys are 3-4bps richer in today's Asia-Pac session after yesterday’s solid gains.

- Cash ACGBs are 6-8bps richer with the AU-US 10-year yield differential at +15bps.

- The bills strip has bull-flattened, with pricing +4 to +9.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in November is given an 80% probability, with a cumulative 28bps of easing priced by year-end.

- Interest rate expectations across the $-bloc have softened over the past week, led by Australia (-15bps) and the US (-9bps), with New Zealand (-3bps) and Canada (-2bps) lagging.

- The local data calendar is fairly quiet through the course of the next week, with Oct preliminary PMIs out next Friday, with the RBA's Bullock also speaking that day.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Rally Extends But Lags $-Bloc, Q3 CPI On Monday

NZGBs closed showing a bull-flattener, with benchmark yields 3-5bps lower, on a data-light session.

- On a relative basis, NZGBs lagged the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials 4bps and 2bps wider, respectively.

- Nevertheless, the NZ-US differential is holding around levels last seen in February.

- Swap rates closed 4-6bps richer with the 5-year leading.

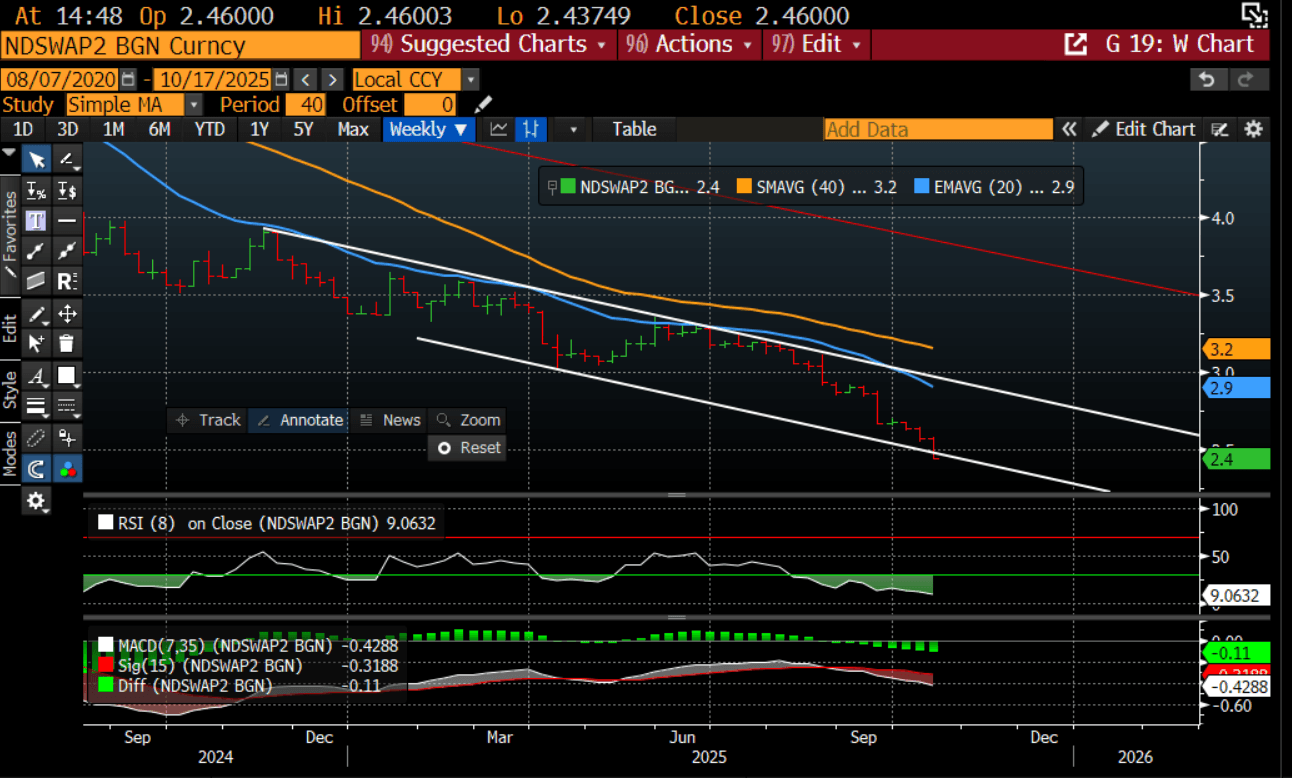

- For context, the 2-year swap rate is around 40bps lower than levels seen before the release of Q2 GDP data in late September, which dramatically undershot expectations. (see chart)

- RBNZ-dated OIS pricing is little changed across meetings. 26bps of easing is priced for November, with a cumulative 36bps by February 2026.

- On Monday, the local calendar will see Q3 CPI, with BNZ expecting the CPI to fall from its Q3 peak at 3%, as the current bout of inflation gradually unwinds. Monthly prices, released yesterday, edged slightly lower compared to prior months, indicating a softer trend and a lower base heading into the fourth quarter. - MTN

Bloomberg Finance LP

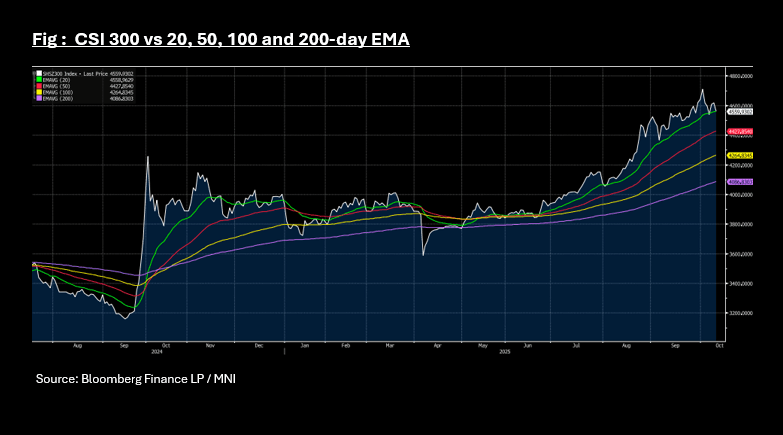

ASIA STOCKS: Equities Down from Overnight Leads, CSI 300 Testing Key Levels

- The overnight lead from the US followed over into major bourses in Asia today, with China and Hong Kong down. Earlier in the week the HSI tested the 50-day EMA support but with the overnight headwinds traded through it has stabilized at the mid-point between the 50 and 100-day EMA. The CSI 300 is down -1.2% and is near the 20-day EMA which it has struggled to hold below since April. An article on BBG suggests that data shows China's households may be stepping back from equities, with cash holdings spiking in September - challenging the last few weeks of positive momentum.

- The NIKKEI is down -1.20% unable to gain further momentum back towards last week's new all time high and could be set to finish down for the week.

- The KOSPI has also reached new highs again and hovering around unchanged on the day, as it outperforms regional peers.

- In Taiwan, the strength of the TSMC results overnight and the accompanying outlook was not enough to see the TAIEX rally, falling by -0.6% today in a subdued day of trading.

- In India, there is renewed hope for trade discussions with the US with the NIFTY 50 holding onto modest gains this morning, looking at a second successive weeks of gains.

ASIA STOCKS: Tech Sensitive Inflows Up, Indian Inflows Recovering

Yesterday saw decent offshore inflows into both South Korean and Taiwan equity markets. The Kospi remains in a strong uptrend, getting close to fresh highs of 3800 in the first part of trade today, although we sit off best levels now. AI/chip sentiment remains strong, underscored by Taiwan's TSMC Q3 results yesterday. Indeed, in Thursday US trade the SOX index still finished higher despite broader credit concerns (which weighed on bank/financial stocks). The US-South Korean trade negotiations continue, with still uncertainty as to how investment/FX concerns on the South Korean side will be met, (particularly given US demand around when the $350bn investment inflows should take place). This, along with broader equity trends, will be watch points.

- In Taiwan, even with yesterday's net inflow, we have still lagged the positive trends seen in local equities (last 5 trading days has seen cumulative outflows near -$2bn). TSMC results bode well for the tech sector, although shares in the tech bellwether are down so far today.

- Indian inflow momentum is better and there is scope for a further recovery (given YTD outflows are still over -$16.5bn). Th break higher in local stocks, the NIFTY through 25500 may induce more inflow momentum. A more stable to stronger FX backdrop may aid with inflows, but broader trends are likely to be dictated by US-India trade discussions and RBI easing expectations.

- In South East Asia, outflows have been evident, with Malaysia now seeing 10 consecutive sessions of outflows. Most markets in this part of the region sit off recent highs or are tracking sideways.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 403 | 1135 | 3224 |

| Taiwan (USDmn) | 426 | -1932 | 7669 |

| India (USDmn)* | 79 | 995 | -16512 |

| Indonesia (USDmn) | -37 | -22 | -3297 |

| Thailand (USDmn) | -62 | -146 | -3035 |

| Malaysia (USDmn) | -3 | -260 | -4130 |

| Philippines (USDmn) | -3 | -28 | -710 |

| Total (USDmn) | 803 | -258 | -16790 |

| * Data Up To Oct 15 |

Source: Bloomberg Finance L.P./MNI

FOREX: USD Falters On Further Yields Losses, USD/JPY Tests Under 150, A$ Lower

USD indices continue to tick lower, the BBDXY off a further 0.10% to 1206.5/6 (fresh lows since Oct 7). US Tsy yields have dropped further, amid a continuation of the risk off mood. JPY (testing under 150.00) and CHF (near 0.7900) are the outperformers, particularly against the higher beta AUD. A$ losses have been compounded by China/HK equity market weakness.

- USD/JPY got to lows of 149.90 a short while ago, so sub the 20-day EMA, before stabilizing. The 50-day is further south at near 148.75/80. Risk tones are dictating yen shifts. US equity futures are down a further 0.40% so far today, with eyes on whether the 50-day EMA support zone will be tested. Credit jitters related financial/bank equity sentiment on Thursday. Risk tones are also driving demand for Tsys, with yields down a further 3bps (10yr to 3.94%).

- USD/JPY already looked too elevated relative to US-JP rate differentials, with today's moves reinforcing these trends.

- The Japan PM vote is scheduled to go ahead on Oct 21. It remains to be seen if there will be a Ishin/LDP coalition (with agreement potentially not coming until early next week). An Ishin co-leader stated earlier coalition chances were 50/50.

- AUD/USD remains in a downtrend, although is still above recent lows of 0.6440 (last 0.6470). This week's jobs data has bought RBA cuts back into focus, which is likely driving some fresh A$ and cross selling, particularly given broader risk off. AUD/JPY got to 96.89 earlier, around earlier Oct lows and we are under the 50-day EMA support (97.46).

- NZD/USD has been relatively steady, last near 0.5730, lagging yen and CHF gains. AUD/NZD is back under 1.1300 with focus on next Monday's Q3 CPI print in NZ.

- Looking ahead it is fairly quiet data wise, but we do have BOE, ECB and Fed (before the blackout period) speak to round out the week.

Oil Falls for Third Week on US China Standoff

- Oil prices continued to fall today and is set for a third successive weekly fall.

- WTI is approaching being oversold after US China trade tensions challenge global growth assumptions, and news of the potential Trump / Putin meeting challenge assumptions on Russian supply.

- This comes as OPEC+ has ramped up production, agreeing to successive increases.

- WTI is down -2.7% at US$57.31 bbl week to date and on the 14-day Relative Strength Index, nears being oversold.

- Similarly Brent is down -2.9% this week and down 13% over the last three weeks.

- EU Commission has published updated guidelines on the documentation, due diligence required for complying with the import ban on refined products that have been processed from Russian crude oil, according to its website. The guidelines set out how importers should exercise due diligence when importing fuels to ensure it has not come from Russian crude (as per BBG).

- This comes as India's refiners have stated that they intend to reduce (but not stop) the purchase of Russian oil, as per comments from India's biggest refiners.

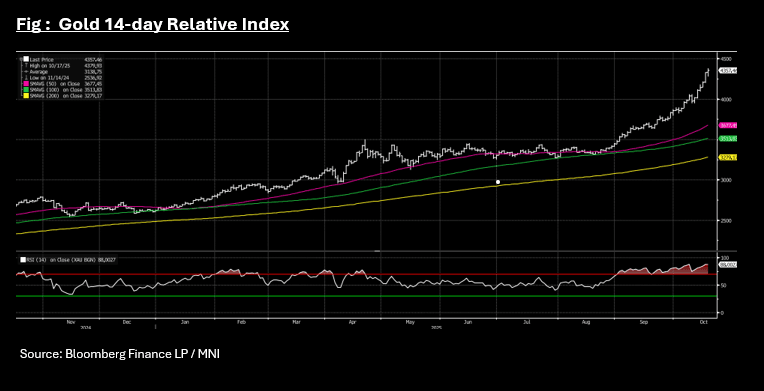

Gold Set for Biggest Weekly Gain of Year

- The relentless rally for gold continued today as new all time highs were reached yet again.

- A rally +0.70% today to US$4,356 sees the precious metal up over 8% for the week.

- Markets turned weaker overnight as credit fears reared over two regional banks in the US. This came following the collapse of a sub-prime lender with two regional banks share prices falling heavily given fears of exposure to the lender.

- That environment is ideal for gold and prices were strong in regional trade today.

- Gold is up over 12% in October alone and over 60% this year and remaining overbought on the relative strength index for a second month.

ASIA FX: USD Losses Curbed By Equity Weakness, China GDP, BoK & BI Next Week

The past week has mostly delivered Asia FX gains, with lwoer US Tsy levels and a firmer yen, aiding such trends. There have been some laggards though with TWD, IDR and MYR not participating. Focus is likely to shift to broader risk trends we have seen some sharp regional equity losses today following the Wall St dip on Thursday (amid credit concerns). Continued risk off could lend USD/Asia pairs more support. Next Monday we have Q3 GDP growth which is expected to slow. The BoK and BI decisions are due next week, with BI seen cutting, BoK on hold.

- USD/CNH couldn't sustain sub 7.1200 levels. From lows of 7.1168, we are back to 7.1240, little changed. This comes despite another lwoer USD/CNY fix, while some offset is coming from weaker equities. China stocks are threatening to break down through 20-day EMA support. Seemingly little in the way of forward US-China progress may be weighing on the yuan. Next Monday also delivers house prices for Sep, and Sep activity figures.

- USD/KRW has edged a little higher, last near 1420, with support evident around the 1414 region. Local equities are outperforming, but broader equity trends are less supportive, while US-South Korea trade deal doubts linger.

- USD/TWD is holding near 32.65, off 0.35% so far this week in TWD terms. Local equities are off 1% despite strong TSMC results yesterday. We have also seen nearly $2bn in net equity outflows the past 5 trading days.

- USD/IDR has also struggled for downside this week. We remain around 16585 currently, near the 20-day EMA. Next week the BI may cut again to support growth, which could weigh on IDR all else equal. Local equities are off over 2% so far today, as recent gains are given back.

- SGD, MYR, THB and PHP have all ticked up against the USD so far today.

China Data Preview: GDP to Moderate, LPRs Unchanged

- Next week could be a pivotal week for policy for the remainder of the year with the loan prime rate decision and GDP third quarter released. The current forecast for GDP 3Q is for it to moderate to 4.7% from 5.2%.

- The decline from Q2 is likely as much about the upside surprise in Q2, then a dramatic slowdown with 4.7% a somewhat fairer reflection. Exports have rebounded with September expanding by +8.3%, from 4.4% the month prior though retail sales and industrial production out next week also is forecast at the weakest pace of expansion this year.

- The outlook for retail sales and service related data releases could be revised up following the October Golden week holiday numbers showing a surge in spending on travel and retail, despite long standing property woes.

- The Chinese party officials meet next week with the fourth plenum in Beijing. The output will provide guidance for the next 5-years and may be the catalyst for further policy intervention, specifically targeting domestic consumption (which has declined as a percentage of GDP) whilst mindful of the impact of the trade war on manufacturing and exports.

- We don't expect any change in the LPR given the pressure on bank margins and look for signals from the party meeting as guide for potential moves in monetary or fiscal policy.

SOUTH KOREA: BOK on Hold Given Housing Concerns

- The BOK meets next week on the 23rd at a time when the government is focused on slowing the housing sector.

- Given the government's focus on cooling the housing market, particularly in Seoul, yesterday's release of the September Loans to households was relevant to next week's BOK. However with mortgage loans increasing 2.5t won MoM to KRW932.7 tn at end of September, there seems to be no immediate impact from policy and this limits the ability of the BOK to cut.

- South Korea has announced further measures at cooling the sector including tighter loan limits specifically in Seoul, higher risk weights on banks' home loan portfolios and reducing loan to value ratios for purchases. "The recent instability in housing markets is spreading on global rate-cut expectations and persistent supply-demand imbalances that are driving concerns over excess capital inflows into real estate," said the Minister of Land, Infrastructure and Transport Kim Yun-duk said in a briefing Wednesday. "In response, we're going to take pre-emptive measures to curb instability in the housing market early and to ensure that capital is directed toward more productive sectors of the economy," he added. (as per BBG).

- Since October the Bank of Korea has cut rates four times going on hold in April, following the release of the initial policy changes by the then new government. The BOK then cut rates in May and as the meeting next week approaches, markets remain uncertain with no rate cuts priced in over a one month time horizon and just -6bps over the next three months.

- Market consensus on BBG is for no change and we see limited possibility of any change from the BOK.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/10/2025 | 0600/0800 | ** | Unemployment | |

| 17/10/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/10/2025 | 0935/1035 | BOE Pill Speech at Institute of Chartered Accountants Conference | ||

| 17/10/2025 | 1100/1200 | BOE Greene Roundtable at Atlantic Council | ||

| 17/10/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1315/0915 | *** | Industrial Production | |

| 17/10/2025 | 1615/1215 | St. Louis Fed's Alberto Musalem | ||

| 17/10/2025 | 1630/1730 | BOE Breeden in Panel at IMF/World Bank Meetings | ||

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 2000/1600 | ** | TICS | |

| 18/10/2025 | 1130/1330 | ECB Cipollone Speech at Euro50Group Meeting | ||

| 18/10/2025 | 1300/1500 | ECB Lagarde in Economic Outlook Panel at G30 | ||

| 18/10/2025 | 1300/1400 | BOE Bailey at G30 International Banking Seminar |