MNI EUROPEAN MARKETS ANALYSIS: Central Bank Speak In Focus

- JGB futures are slightly weaker, -2 compared to settlement levels, after giving up substantial gains following today’s poor 10-year auction. USD/JPY probed under 147.00 but had no follow through. US Tsy futures are little changed.

- Australian consumer spending and trade data was below forecast. AUD/USD is little changed but AUD/NZD has continued to move off recent highs.

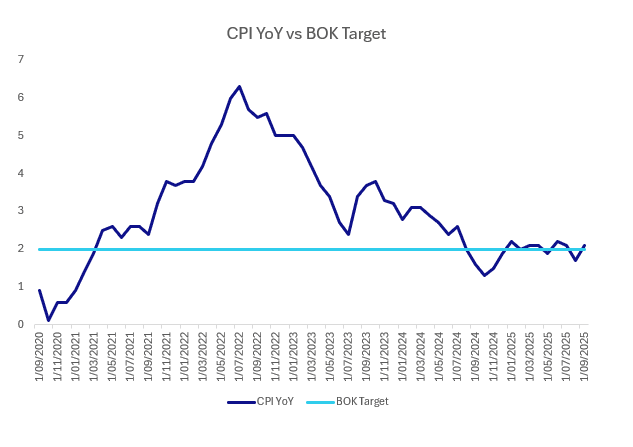

- In South Korea, after briefly dipping in August in what was primarily technically driven, CPI YoY moved back above the BOK 2% target in the September release.

- Later the Fed’s Logan & Goolsbee and ECBs’s de Guindos & Montagner speak. US government-produced data will now be delayed, including payrolls, and so private sector data, such as today’s Challenger job cuts, are being monitored closely. Swiss September CPI, French August budget balance and euro area August unemployment rate also print.

MARKETS

US TSY: Futures Little Changed After Giving Up Early Gains

TYZ5 is dealing at 112-27+, +0-00+ from closing levels in today's Asia-Pac session.

- Cash bonds are slightly cheaper across benchmarks, with a flattening bias, after reversing earlier modest gains.

- Yesterday, US tsys finished 2-7bps richer, with a steeper curve.

- The ADP release for September was weak, showing the biggest private payrolls drop (-32k) since March 2023 and before that, June 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. This was a significant miss for private payrolls versus +51k expected.

- Thursday's scheduled economic data has been largely delayed/suspended due to the shutdown - weekly jobless/continuing claims, as well as Factory New Orders, will not be released.

JGBS: Early Gains Given Up After Poor 10Y Auction

JGB futures are slightly weaker, -2 compared to settlement levels, after giving up substantial gains following today’s poor 10-year auction.

- The 10-year JGB auction delivered weak results, with the low price failing to meet expectations at 100.49, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.3356x from 3.9156x, and the tail lengthened to 0.19 from 0.06.

- Earlier, data showed that offshore investors were meaningful sellers of Japanese bonds last week. Net selling of local bonds by offshore investors was at nearly -2trln. This was the largest weekly outflow since September last year. That said, trend flows for this segment in recent months are fairly indifferent from a cumulative standpoint.

- Cash US tsys are slightly cheaper across benchmarks, with a flattening bias, after reversing earlier modest gains.

- Cash JGBs are slightly richer across benchmarks out to the 7-year, but flat to 2bps cheaper beyond. The benchmark 10-year yield is 0.8bp higher at 1.660%, hovering just below its cyclical high.

- The swap curve has twist-steepened, with rates 1bp lower to 2bps higher.

- Tomorrow, the local calendar will see Labour Market and S&P Global Composite & Services PMI data alongside a speech by BOJ Governor Ueda. BOJ Deputy Governor Uchida’s speech is due later today (1535 JT).

JAPAN DATA: Offshore Investors Sell Both Local Stocks & Bonds, Japan Flows Muted

Offshore investors were meaningful sellers of both Japan equities and bonds last week. In the equity space we continue to see a paring back of the net long position built up earlier in the year. In the last 6 weeks we have seen net selling of near ¥6trln for this segment by offshore investors. This curbs cumulative inflows since the start of April to sub ¥6trln. Japan stocks have faltered in recent weeks, with early Oct trends taking us away from recent record highs. Offshore outflows, at the margin, has likely aided such trends.

- Net selling of local bonds by offshore investors was even larger last week, at nearly -¥2trln. This was the largest weekly outflow since Sep last year. Trend flows for this segment in recent months are fairly indifferent from a cumulative standpoint. JGB yields remain at risk of breaking higher, although recent auction outcomes have steadied sentiment from a demand standpoint.

- In terms of outbound Japan flows, we saw net selling of both overseas bonds and equities, although these shifts were modest. On the bond side, the dip in global bond returns (as US Tsy yields rose) may be a factor.

- IN the equity space, aggregate flows for local investors remains light.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Sep 26 | Prior Week |

| Foreign Buying Japan Stocks | -963.3 | -1747.1 |

| Foreign Buying Japan Bonds | -1997.0 | 53.4 |

| Japan Buying Foreign Bonds | -162.0 | 816.7 |

| Japan Buying Foreign Stocks | -11.6 | -151.5 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Modestly Stronger, Consumption Weaker Than Expected

ACGBs (YM +3.5 & XM +3.0) are stronger, hovering just below session bests.

- August household consumption was weaker than expected rising 0.1% m/m with the annual rate slowing to 5.0% from 5.3% but still above the series average. The RBA noted in September that private consumption was stronger than it expected as financial conditions have eased and real incomes are higher.

- Australia’s non-rural goods exports fell 2.5% m/m and 7.4% y/y in August with coal and metal values falling in the month but ores posting a small increase. In addition, overall shipments to Asia were soft with key commodities contracting to Japan and South Korea.

- Cash US tsys are slightly mixed in today's Asia-Pac session.

- Cash ACGBs are 3-4bps richer with the AU-US 10-year yield differential at +23bps.

- The bills strip is +1 to +4 across contracts, with a flattening bias.

- RBA-dated OIS pricing is showing a 25bp rate cut in October as a 42% probability, with a cumulative 14bps of easing priced by year-end.

- Tomorrow, the local calendar will see S&P Global Composite & Services PMIs.

- The AOFM plans to sell A$1000mn of the 1.25% 21 May 2032 bond on Friday.

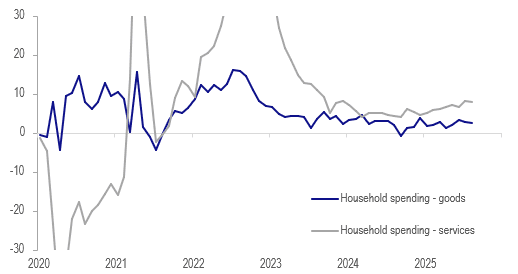

AUSTRALIA DATA: Services Keep Consumption Positive, Next Month Q3 Volumes Print

August household consumption was weaker than expected rising 0.1% m/m with the annual rate slowing to 5.0% from 5.3% but still above the series average. The RBA noted in September that private consumption was stronger than it expected as financial conditions have eased and real incomes are higher. While the monthly data are nominal, it will be monitoring the quarterly volumes included in the September release on 3 November before the 4 November RBA decision.

- Discretionary spending rose 0.2% m/m in August to be up 4.7% y/y after 0.3% & 4.9%, while non-discretionary fell 0.1% m/m but still rose 5.6% y/y following July’s +0.7% & 6.0%. The gradual recovery in discretionary spending is good news and reflects some improvement in confidence driven by lower inflation and rates.

- Services expenditure increased 0.5% m/m after July’s strong 1.6% and is up 8.1% y/y, well above August 2024’s 4.5% y/y. The monthly rise was due to increased travel spending.

- Goods spending has slowed posting its second straight monthly decline after mid-year discounting boosted May and June. Drops in recreation and alcohol & tobacco drove August down 0.2% m/m to be up 2.5% y/y down from 2.9% but still higher than August 2024’s 2.0%.

Australia household consumption goods vs services y/y%

Source: MNI - Market News/ABS

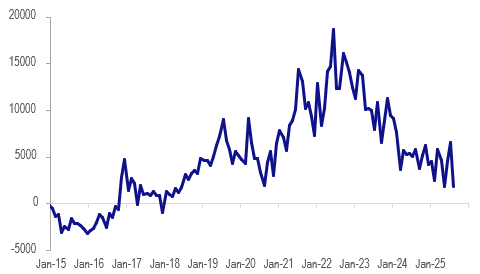

AUSTRALIA DATA: Trade Surplus Lowest In Over 7 Years

Australia’s merchandise trade surplus narrowed to $1825mn in August from a downwardly-revised $6612mn, which was significantly more than expected. The weakness was driven by a sharp 7.8% m/m drop in exports while imports rose 3.2%, but it is worth noting that the former has been gradually recovering over the last two years. This was the lowest surplus in over seven years.

Australia merchandise trade surplus A$mn

Source: MNI - Market News/ABS

- The monthly drop in exports was driven by non-monetary gold sinking 47.2% m/m but non-rural goods were down 2.5% m/m & 7.4% y/y with coal and metals weak. Export growth fell 2.5% y/y after 6.1%, the slowest since February. Rural goods remain strong rising 3.1% m/m & 22.1% y/y.

- Global gold prices rose almost 12% over September and so a rise in export volumes should provide support to a recovery in export growth in the month.

- The strength in imports was broad based across key components with consumer goods up 5.8% m/m & 10% y/y with all categories higher in August, in line with a recovery in household spending. Capex goods rose 1.8% m/m to be up 5% y/y but most items fell on the month with the increase due to aircraft and ADP equipment.

Australia goods exports vs imports y/y%

Source: MNI - Market News/ABS

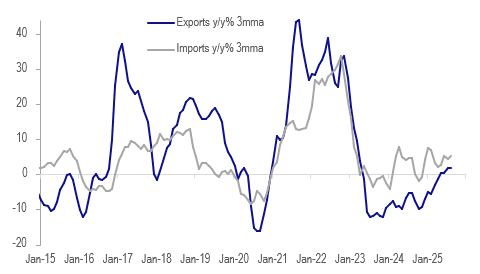

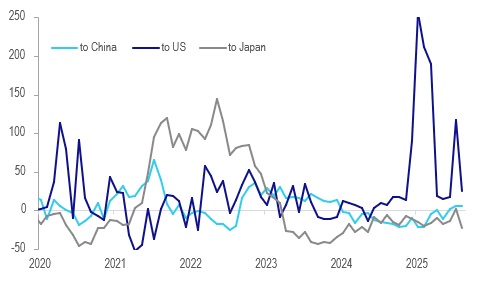

AUSTRALIA DATA: Australia’s Exports To Asia Underperforming To Non-Asia

Australia’s non-rural goods exports fell 2.5% m/m and 7.4% y/y in August with coal and metal values falling in the month but ores posting a small increase. In addition, overall shipments to Asia were soft with key commodities contracting to Japan and South Korea.

- Exports to China grew 5.7% y/y after contracting through 2024 but lower than the rates seen in 2023. Iron ore volumes increased in August but thermal coal was down sharply. China has said that it will no longer import iron ore from Western Australia but BHP has told the Australian government that this is just a price negotiation tactic, according to The Australian. Given its importance, it will be worth monitoring developments.

- Shipments to Japan fell 22.5% y/y, -44.4% y/y to India and -36% y/y to Indonesia, while they remained strong to the US, UK and Germany. Exports to South Korea have been recovering over 2025.

- Volumes of iron ore (lump) fell 2.3% m/m driven by Taiwan and Korea while fines rose due to China but were lower to Korea and Japan. Prices were higher for both types.

- Hard-coking coal export volumes rose sharply driven by the Netherlands, India and Sweden, while thermal fell on the month due to China and Japan. Coal unit values were higher after falling in July.

- Both LNG export volumes and prices fell in August.

Australia merchandise exports y/y%

Source: MNI - Market News/ABS

BONDS: NZGBS: Closed With A Modest Bull-Flattener

NNZGBs closed showing a modest bull-flattener, with benchmark yields flat to 2bps lower.

- Today’s weekly supply saw solid demand metrics, with cover ratios ranging from 3.67x (May-30) to 3.85x (May-35).

- NZGB 10-year’s relative performance in the $-bloc was mixed on the day, with the NZ-US yield differential 2bps wider but the NZ-AU 1bp tighter.

- Cash US tsys are slightly cheaper across benchmarks, with a flattening bias, after reversing earlier modest gains.

- Thursday's scheduled economic data largely delayed/suspended due to the shutdown - weekly jobless/continuing claims as well as Factory New Orders will not be released.

- Swap rates closed flat to 2bps lower.

- RBNZ dated OIS pricing closed little changed across meetings. 33bps of easing is priced for October, with a cumulative 62bps by November 2025.

- Tomorrow, the local calendar will be empty. The next release will be ANZ Commodity Prices on Monday.

FOREX: Majors Steady, AUD/NZD Off Recent Highs

The major USD indices are little changed in the first part of Thursday dealing. We were last near 1200.25 for the BBDXY index. Outside of NZD, which has continued to track a little stronger, G10 FX moves are less than 0.10% at this stage. Cross asset sentiment is relatively steady, with US Tsy yields last a little higher, but gains are less than 1bps. The equity tone has been positive, particularly for tech sensitive plays.

- We did have some Australian data, which was below expectations. The trade surplus fell sharply in August, as exports faltered. Household spending was also below forecast, albeit modestly. AUD/USD is little changed though holding above 0.6615 at this stage (session lows were at 0.6602).

- Some further profit taking in AUD/NZD longs may have been in play, with the cross back to 1.1344 before stabilizing (last 1.1350/55). Still, we are above the 20-day EMA support point still (1.1260), while AU-NZ 2yr swap spreads have barely budged off recent highs and have correlated strongly with the recent move higher in the cross. Hence, we may need to see weakness in such spreads for further AUD/NZD downside.

- For NZD/USD we got to 0.5836, continuing the recent recovery, but sit back at 0.5825/30 in latest dealings.

- USD/JPY probed under 147.00 but had no follow through. Wednesday lows were 146.59. Later on we here from BoJ Deputy Governor Uchida. Focus is likely to rest on hiking hints (if any are given) in light of this week's resilient Tankan survey result (which has been a key BoJ watch point for gauging tariff fallout).

- BoJ hike odds for the Oct meeting are little changed over the week, with the market pricing in around 14bps of tightening.

- EUR/USD was last unchanged at 1.1730.

- Looking ahead, the Fed’s Logan & Goolsbee and ECBs’s de Guindos & Montagner speak. Private sector US data will still be released which today includes September Challenger job cuts. Swiss September CPI, French August budget balance and euro area August unemployment rate also print.

ASIA STOCKS: Chip Deal Gives Tech Stocks a Boost

News of OPENAI's agreement with Korea's Samsung Electronics and SK Hynix Inc to supply chips to the companies Stargate project has seen shares in both surge today. Samsung is up 4.6% and SK Hynix up 10.5% driving the KOSPI higher. This dragged the sector higher throughout the region with Japanese chip related stocks benefiting, helping it snap a four day losing streak.

- A four days of falls, the NIKKEI is up today by +0.77%.

- The KOSPI is up +2.95%, reaching a new all time high of 3,557.

- The TAIEX joined in the tech led rally, rising +1.6%

- The FTSE Malay KLCI is up +0.72% for its biggest 1-day gain in three weeks.

- The Jakarta Composite is up +0.25% after two days of losses, yet remains down for the week.

- The NIFTY 50 finished yesterday marginally down yet has rebounded today to be up +0.92% for it's biggest one day gain since the middle of August.

OIL: : Crude Stabilises Ahead Of OPEC As Geopolitical Developments Return

Oil prices fell sharply this week ahead of the 5 October OPEC meeting to decide November’s production target. They appear to have stabilised during today’s APAC session with WTI up 0.5% to $62.12/bbl after a high of $62.54 which followed a WSJ report that the US would give Ukraine intelligence to support its strikes on Russian energy infrastructure and also encouraged NATO to do the same. Brent reached $66.15/bbl but is now around $65.70/bbl also to be 0.5% higher. The US dollar is flat.

- Bloomberg reported that following the G7 finance ministers meeting an agreement on substantial additional sanctions on Russia’s means to finance its war in Ukraine is close. The group has also decided on more assistance for Ukraine.

- OPEC is expected to continue to unwind previous output reductions when it meets this weekend. It increased the October target by 137kbd and at least that amount is likely in November. This comes in addition to the resumption of flows from Iraqi Kurdistan to Turkey which had been halted since March 2023.

- Later the Fed’s Logan & Goolsbee and ECBs’s de Guindos & Montagner speak. Private sector US data will still be released which today includes September Challenger job cuts. Swiss September CPI, French August budget balance and euro area August unemployment rate also print.

Gold Range Trading As Monitoring The Data Available, US Job Cuts Later

Today gold continued to range trade which it began during Wednesday’s US session. Earlier it fell to $3853.03/oz before approaching $3870. It is currently little changed at $3865.7 with the US dollar and yields also steady. Another vote to try and resolve the US debt ceiling issue failed yesterday and developments continue to be watched closely. Related safe-haven flows drove bullion to a series of record highs.

- US September payrolls won’t be released on Friday due to the government shutdown but with ADP employment falling 32k and August revised down to -3k, it appears that the labour market remained soft last month. The market now has a full 25bp rate cut priced in for the October FOMC meeting with almost another one in December, which is supportive of gold.

- Silver has also moved in a narrow range initially falling to $46.974 before reaching $47.527. It is currently down 0.2% to $47.24, just below initial resistance at $47.251.

- Equities are stronger with the S&P e-mini up 0.1%, Nikkei +0.7% and KOSPI +3.0%. Oil prices are up with WTI +0.5% to $62.10/bbl. Copper is 0.6% higher.

- Later the Fed’s Logan & Goolsbee and ECBs’s de Guindos & Montagner speak. Private sector US data will still be released which today includes September Challenger job cuts. Swiss September CPI, French August budget balance and euro area August unemployment rate also print.

SOUTH KOREA: CPI Moves Back Above BOK Target

- After briefly dipping in August in what was primarily technically driven, CPI YoY moved back above the BOK 2% target in the September release.

- CPI in September came in at +2.1% YoY as the MoM figure was flat on August at +0.5%

- Food prices +3.3%YoY and transport +1.2% YoY

- Sept. core CPI rises 2.0% YoY, Prior +1.3% YoY

INDONESIA: Country Wrap: BI Independence Challenged

Market Summary: The Jakarta Composite is up +0.25% after two days of losses, yet remains down for the week whilst the Rupiah had modest gains again today, to reach 16,609 it has gained -0.16% as it continues to edge lower from last week's wides of 16,750. Front end bonds have rallied strongly on the news story challenging independence with the 5-Yr the best performer, down 4bps to 5.47% and the 10-Yr is at 6.32% (from yesterday's close of 6.33%)

- Indonesia’s finance minister once wanted to run the country’s central bank. Now, he just wants to tell it what to do. Purbaya Yudhi Sadewa, who rose from relative obscurity to become one of Indonesia’s most powerful officials, has told friends and colleagues over the years that he doesn’t believe the central bank should be independent, according to people familiar with the matter. The nation’s populist leader Prabowo Subianto agrees with him, the people said. (source The Edge)

- Finance Minister Purbaya will redo some portions of the state budget (APBN) to allocate for the year-end stimulus program. He confirmed that the budget reallocation will be imposed on the least urgent spending, and he is still monitoring and gauging the budget lines that will be affected by the initiative. (source Antara)

MALAYSIA: Country Wrap: China Discussing Rare Earth Projects with Malaysia

Market Summary: The FTSE Malay KLCI is up +0.72% for its biggest 1-day gain in three weeks whilst the Ringgit at 4.2045 traded below a key trend line that it has struggled to hold and bonds have had a decent rally with 3-7yr yields 4-5bps tighter. MSG 10-Yr is down 3bps today at 3.45%

- China and Malaysia are in early talks for a project to process rare earths, with sovereign wealth fund Khazanah Nasional Bhd likely to partner with a Chinese state-owned firm to build a refinery in the Southeast Asian nation. (source The Edge)

- The Malaysia Pavilion at the 22nd China-ASEAN Expo (CAEXPO) has recorded total sales of RM376.14 million, according to the Malaysia External Trade Development Corporation (MATRADE). The Malaysia Pavilion, which comprised 70 exhibitors including eight ministries and agencies across various sectors, concluded successfully, underscoring the strong demand and growing opportunities for Malaysian products and services in the China-ASEAN market. (source The Star)

ASIA FX: KRW & TWD Up, But Lag Equity Rally, THB & PHP Softer

Asian currencies are mixed in the first part of Thursday trade. In North East Asia, China markets remain out (until next Thursday), while Hong Kong returned today. USD/CNH remains within recent ranges, with dips under 7.1300 supported so far today. Other currencies have seen modest gains against the USD.

- For KRW and TWD, we have seen strong onshore equity gains, with tech/AI optimism continuing to drive positive sentiment. For South Korea, this is bringing in fresh offshore inflows today, but the won is only modestly higher. Spot USD/KRW is still above 1400 at this stage. One factor for the won may be trade deal uncertainty. Headlines crossed earlier that South Korean officials haven't got a positive response from US officials around a swap line with South Korea (which is eyed as important given South Korea's $350bn investment pledge).

- Spot USD/TWD is back at 30.40, also up only a touch in TWD terms. Both TWD and KRW have lagged the better tech inspired equity market backdrop.

- In South East Asia, USD/THB continues to trade with a positive bias, last at 32.45, which is just short of recent highs. Dovish BoT rhetoric and a considered focus on baht volatility is aiding the pair. The Citi THB NEER is now 2% off Sep highs (but still up YTD).

- USD/PHP is also being supported on dips, last near 58.25. There appears to be some resistance above the 58.30, while early August highs were just above 58.50.

- The Rupiah has had modest gains again today, similar to yesterday. At 16600/05 it continues to edge lower from last week's wides of 16750. Some stability in bond flows towards the end of Sep appears to be helping, while seasonality for IDR is less negative in Oct compared to Sep.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/10/2025 | 0630/0830 | *** | CPI | |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University | ||

| 03/10/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/10/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/10/2025 | 0645/0845 | * | Industrial Production | |

| 03/10/2025 | 0700/0300 | * | Turkey CPI | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0800/1000 | * | Retail Sales | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/10/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/10/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/10/2025 | 0900/1100 | ** | EZ PPI | |

| 03/10/2025 | 0940/1140 | ECB Lagarde Speech At Knot Farewell Symposium | ||

| 03/10/2025 | 1000/0600 | NY Fed's John Williams | ||

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium |