GOLD: Gold Range Trading As Monitoring The Data Available, US Job Cuts Later

Today gold continued to range trade which it began during Wednesday’s US session. Earlier it fell to $3853.03/oz before approaching $3870. It is currently little changed at $3865.7 with the US dollar and yields also steady. Another vote to try and resolve the US debt ceiling issue failed yesterday and developments continue to be watched closely. Related safe-haven flows drove bullion to a series of record highs.

- US September payrolls won’t be released on Friday due to the government shutdown but with ADP employment falling 32k and August revised down to -3k, it appears that the labour market remained soft last month. The market now has a full 25bp rate cut priced in for the October FOMC meeting with almost another one in December, which is supportive of gold.

- Silver has also moved in a narrow range initially falling to $46.974 before reaching $47.527. It is currently down 0.2% to $47.24, just below initial resistance at $47.251.

- Equities are stronger with the S&P e-mini up 0.1%, Nikkei +0.7% and KOSPI +3.0%. Oil prices are up with WTI +0.5% to $62.10/bbl. Copper is 0.6% higher.

- Later the Fed’s Logan & Goolsbee and ECBs’s de Guindos & Montagner speak. Private sector US data will still be released which today includes September Challenger job cuts. Swiss September CPI, French August budget balance and euro area August unemployment rate also print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

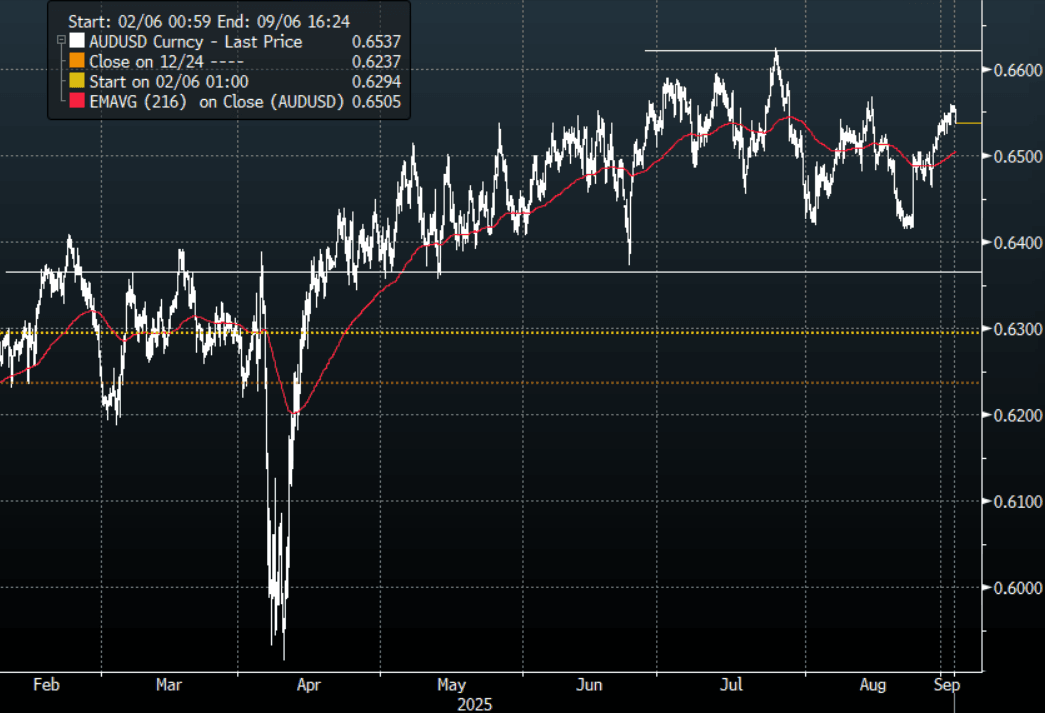

AUD: Asia Wrap - AUD/USD Drifts Lower, Within Range

The AUD/USD has had a range of 0.6537 - 0.6559 in the Asia- Pac session, it is currently trading around 0.6540, -0.20%. The AUD has drifted lower for most of our day. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- Current Account Deficits Continue, Net Exports Added 0.1pp. While Q2 recorded its ninth consecutive quarterly current account deficit, it narrowed from Q1 driven by the primary income deficit. Q2 printed at -$13.7bn after $14.1bn with primary income at -$16.8bn down from Q1’s -$18bn but the goods and services surplus was down $1.2bn at $3.1bn, the lowest in 7 years. Net exports contributed 0.1pp to Q2 growth, as expected.

- MNI: RBA November Cut Eyed, Lower Productivity To Pull Down R*. The Reserve Bank of Australia is likely to hold at its September meeting before delivering another 25-basis-point cut to the 3.6% cash rate in November, former staffers and leading economists told MNI, with the Bank’s downgraded productivity outlook expected to weigh on neutral rate estimates over the longer term.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD770m). Upcoming Close Strikes : 0.6400(AUD1.12b Sept 5), 0.6500(AUD974m Sept 5), 0.6600(AUD1b Sept 5) - BBG

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

- AUD/JPY - Asia-Pac range 96.37 - 96.65, Asia is trading around 96.60. The pair is probing above the 96.50 area this morning. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

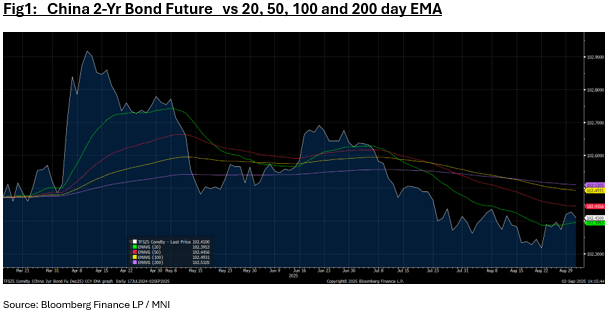

CHINA: Bond Futures Lower Tuesday

- China's bond futures are all trending lower in Tuesday morning trading.

- The 10-Yr bond future is down -0.05 at 107.935 after finishing Monday up +0.16.

- The 10-Yr remains below all major moving averages, with the nearest the 20-day EMA above at 108.05.

- The 2-Yr bond future is down -0.02 at 102.41. The 2-Yr sits around the mid-point of the 50-day EMA of 102.44 and the 20-day EMA of 102.39.

- China's 10-Yr Government bond is down -1bp in yield at 1.77%

US TSYS: Yields Drift Higher After US Holiday

The TYZ5 range has been 112-09+ to 112-13 during the Asia-Pacific session. It last changed hands at 112-12, down 0-04 from the previous close.

- The US 2-year yield has edged higher trading around 3.63%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.246%, up 0.02 from its close.

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. A break of the recent lows around 4.18% would bring the bottom of the range towards 4.10% back into focus.

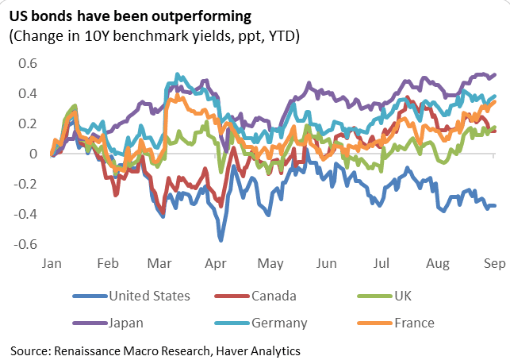

- Bloomberg - “World’s Long-Dated Bonds Face a Traditionally Terrible Month. Longer-maturity bonds may be in for a treacherous September, if history is any guide, with government bonds globally with maturities of over 10 years posting a median loss of 2% in September. The trend may worsen due to sticky inflation in Japan, political turmoil in France, and speculation that President Donald Trump may push the Federal Reserve to cut interest rates.”

- RenMac on X: “Notable that US 10Y yields are still down year-to-date despite rising rates across G-10, concerns about US fiscal deficits, and the rising risk premium associated with Trump's alleged threatening of the Fed’s policy independence.” See Fig.1 Below.

- Data/Events: S&P Manf. PMI, ISM Manf., Construction Spending

Fig 1: US Bonds Outperforming

Source: MNI - Market News/@RenMacLLC