FOREX: Majors Steady, AUD/NZD Off Recent Highs

The major USD indices are little changed in the first part of Thursday dealing. We were last near 1200.25 for the BBDXY index. Outside of NZD, which has continued to track a little stronger, G10 FX moves are less than 0.10% at this stage. Cross asset sentiment is relatively steady, with US Tsy yields last a little higher, but gains are less than 1bps. The equity tone has been positive, particularly for tech sensitive plays.

- We did have some Australian data, which was below expectations. The trade surplus fell sharply in August, as exports faltered. Household spending was also below forecast, albeit modestly. AUD/USD is little changed though holding above 0.6615 at this stage (session lows were at 0.6602).

- Some further profit taking in AUD/NZD longs may have been in play, with the cross back to 1.1344 before stabilizing (last 1.1350/55). Still, we are above the 20-day EMA support point still (1.1260), while AU-NZ 2yr swap spreads have barely budged off recent highs and have correlated strongly with the recent move higher in the cross. Hence, we may need to see weakness in such spreads for further AUD/NZD downside.

- For NZD/USD we got to 0.5836, continuing the recent recovery, but sit back at 0.5825/30 in latest dealings.

- USD/JPY probed under 147.00 but had no follow through. Wednesday lows were 146.59. Later on we here from BoJ Deputy Governor Uchida. Focus is likely to rest on hiking hints (if any are given) in light of this week's resilient Tankan survey result (which has been a key BoJ watch point for gauging tariff fallout).

- BoJ hike odds for the Oct meeting are little changed over the week, with the market pricing in around 14bps of tightening.

- EUR/USD was last unchanged at 1.1730.

- Looking ahead, the Fed’s Logan & Goolsbee and ECBs’s de Guindos & Montagner speak. Private sector US data will still be released which today includes September Challenger job cuts. Swiss September CPI, French August budget balance and euro area August unemployment rate also print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Back Below $3500 After Reaches New Record High

Gold prices spiked to a new record high of $3508.73/oz earlier in today’s APAC session on increased expectations of a September Fed easing. It is also benefiting from concerns regarding Fed independence. It rose above the bull trigger at $3500.1, 22 April record, but has been unable to hold the break. Bullion is now up 0.6% to $3497.0 despite a stronger US dollar (BBDXY +0.2%) and slightly higher yields.

- UBS believes that gold will continue trending higher driven by softening growth, rate cuts and geopolitical/economic uncertainty, according to Bloomberg.

- After rising 2.5% on Monday, silver is up another 0.3% to $40.82 today, holding just above initial resistance at $40.798. It reached a high of $40.850 after a low of $40.558. Bloomberg reported that in August ETF buying of silver rose for the 7th straight month.

- Silver has also been added to the US list of critical minerals. It is a key component of solar panels. The Silver Institute is expecting 2025 to be the fifth year the metal is in deficit, Bloomberg reported.

- Equities are mixed with the S&P e-mini slightly lower, Hang Seng down 0.6% but KOSPI up 0.8%. Oil prices are stronger again with WTI +1.4% to $64.92/bbl. Copper is little changed.

- Later the ECB’s Elderson and Machado appear. US August manufacturing PMI/ISM, July construction, euro area August CPI and July French budget data print.

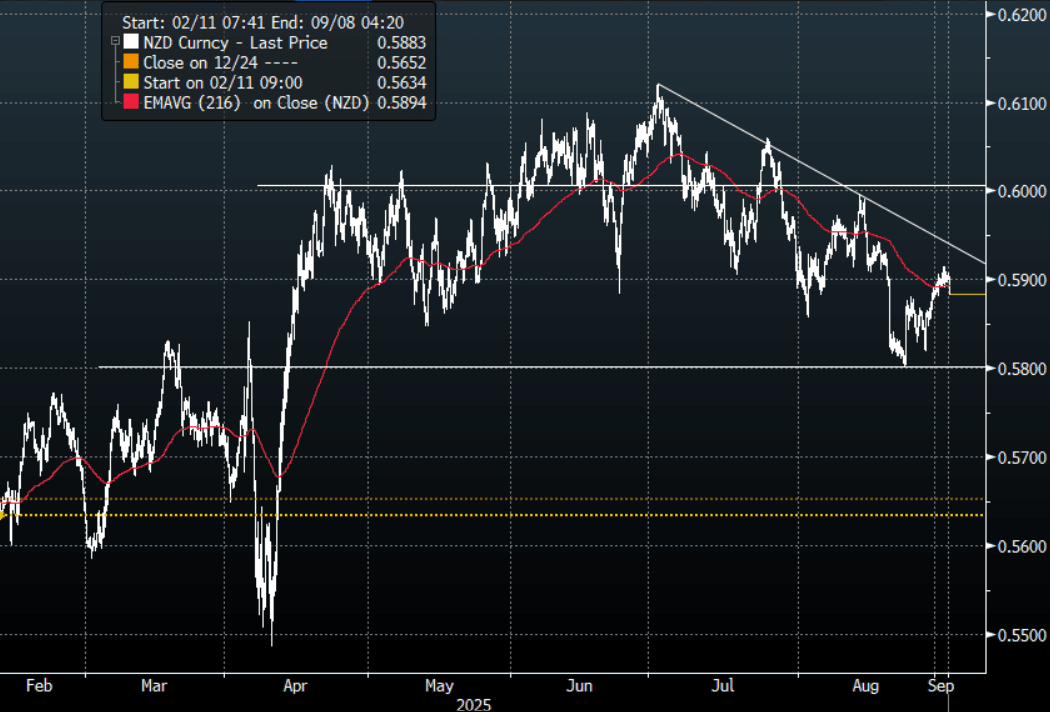

NZD: Asia Wrap - NZD/USD Sellers Return Above 0.5900

The NZD/USD had a range of 0.5883 - 0.5908 in the Asia-Pac session, going into the London open trading around 0.5885, -0.30%. The NZD has topped out above 0.5900 for now as the USD finally sees some demand return. The NZD has bounced off its support toward 0.5800, sellers should continue to be around looking to fade the move back towards the 0.5950/0.6000 area initially. Should the USD break lower and gain momentum this would complicate this trade and then it would be prudent to rotate the NZD shorts into the crosses.

- Goods Terms Of Trade Continues Moving Higher: NZ saw the largest improvement in the merchandise terms of trade in Q2 since Q1 2024. It rose 4.1% q/q, the sixth consecutive quarterly increase, to be up 12.2% y/y after 10.3% y/y in Q1. While domestic demand remains soft, this rise in the terms of trade will be providing some welcome support to growth. The services terms of trade fell 0.4% q/q but rose 1.0% y/y after falling 7.3% y/y.

- "New Zealand Treasury Says Domestic Economic Conditions Are Soft. The data inflow has improved at the margin over the past fortnight signaling better times ahead, but current economic activity is soft, the Treasury Dept. says in its Fortnightly Economic Update published Tuesday in Wellington." - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD500m). Upcoming Close Strikes : 0.5700(NZD384m Sept 3) - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- AUD/NZD range for the session has been 1.1095 - 1.1112, currently trading 1.1110. Momentum higher looks to have stalled above 1.1100 for now, look for demand to return on a dip back towards the 1.1000 area.

Fig 1: NZD/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

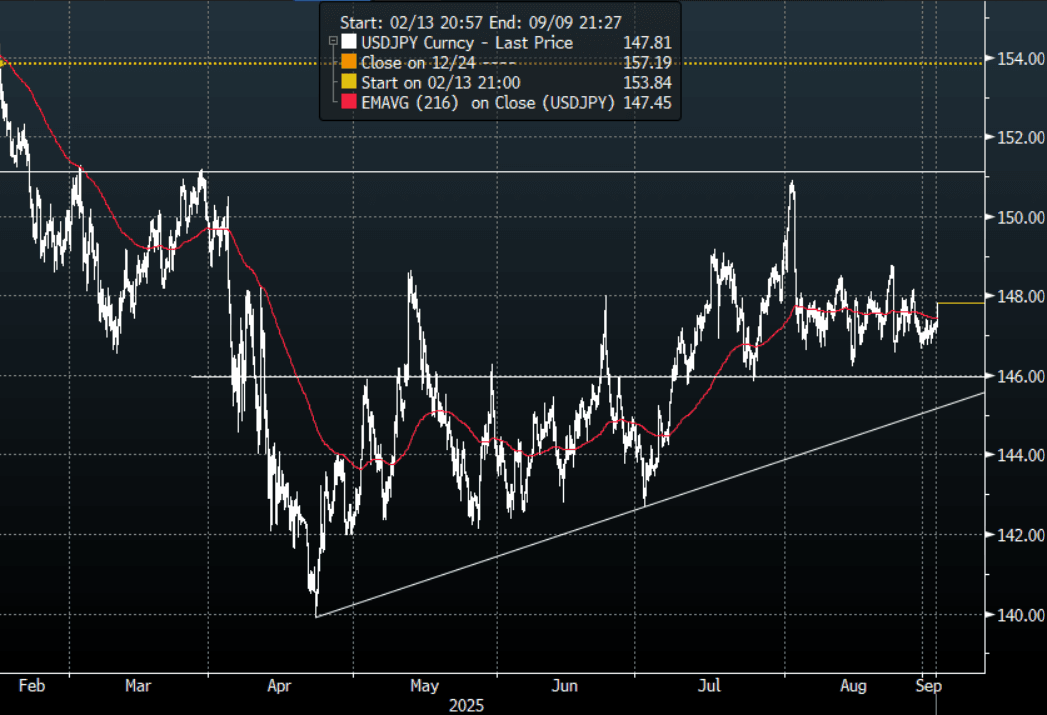

JPY: Asia Wrap - USD/JPY Demand Sees It Bounce Off 147.00 Again

The Asia-Pac USD/JPY range has been 147.05-147.82, Asia is currently trading around 147.80, +0.40%. USD/JPY saw some decent buying into the Japanese Fix, this demand then continued into the afternoon session helping the pair bounce back off its support. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range.

- MNI: BOJ's Himino Sees Gradual Hikes; Upside, Downside Risks. Bank of Japan Deputy Governor Ryozo Himino said Tuesday the Bank would raise its policy rate to adjust the degree of monetary accommodation if its baseline scenario for economic activity and prices materialises, though he gave no guidance on timing or pace.

- "BOJ DEPUTY GOV HIMINO: THERE IS BOTH CHANCE TRADE POLICY IMPACT COULD BE SMALLER OR BIGGER THAN EXPECTED, MUST FOCUS ON POSSIBILITY IT COULD BE BIGGER THAN EXPECTED - [RTRS]"

- On the balance sheet: "BOJ DEPUTY GOV HIMINO: BOJ'S PLAN TO REDUCE JGB BUYING SHOULD BE BASED ON PRINCIPLE THAT LONG-TERM RATES ARE TO BE FORMED IN MARKETS, BOJ SHOULD PROVIDE PREDICTABILITY WHILE ALLOWING ENOUGH FLEXIBILITY TO SUPPORT MARKET STABILITY" RTRS

- “JGB Futures Jumping With Relief After Solid 10-year Auction. JGBs are enjoying a leap higher after the bid-to-cover ratio printed at 3.92 for today’s auction, the best since 2023; there’s also a tighter tail than the previous sale. The list of buyers was led by MUFJ-MS, which typically signals long-term buyers participated.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.30($334m).Upcoming Close Strikes : 146.50($1.39b Sept 3), 146.00($2.16b Sept 5) - BBG.

- CFTC data for last week shows leveraged accounts have maintained their recent JPY shorts and will be hoping this support continues to be solid. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P