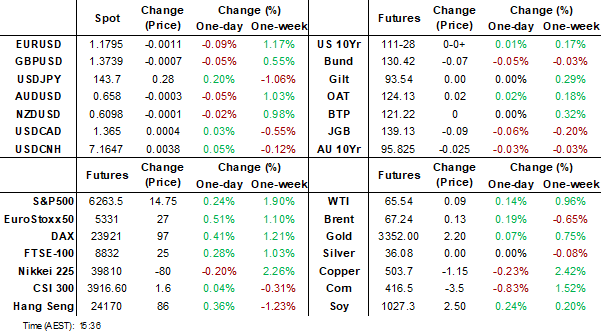

MNI EUROPEAN MARKETS ANALYSIS: Aust Retail Sales Sub Forecasts

- After making fresh lows yesterday, USD indices have consolidated today, ahead of key US NFP data on Thursday. Tsy yields have drifted a touch higher in Asia Pac trade. Equity sentiment is mixed throughout the region as Trump stated there wouldn't be a change to the July 9 tariff deadline.

- Australian retail sales were slightly below forecast and continued to lose momentum in y/y terms, reinforcing a likely RBA cut next week. FX impact on the AUD has been modest though. USD/TWD bucked the broader USD trend, falling amid surging equity inflows.

- Looking ahead, we have on the data front, Eurozone unemployment releases and US ADP. More central bank speak from Sintra is also due.

MARKETS

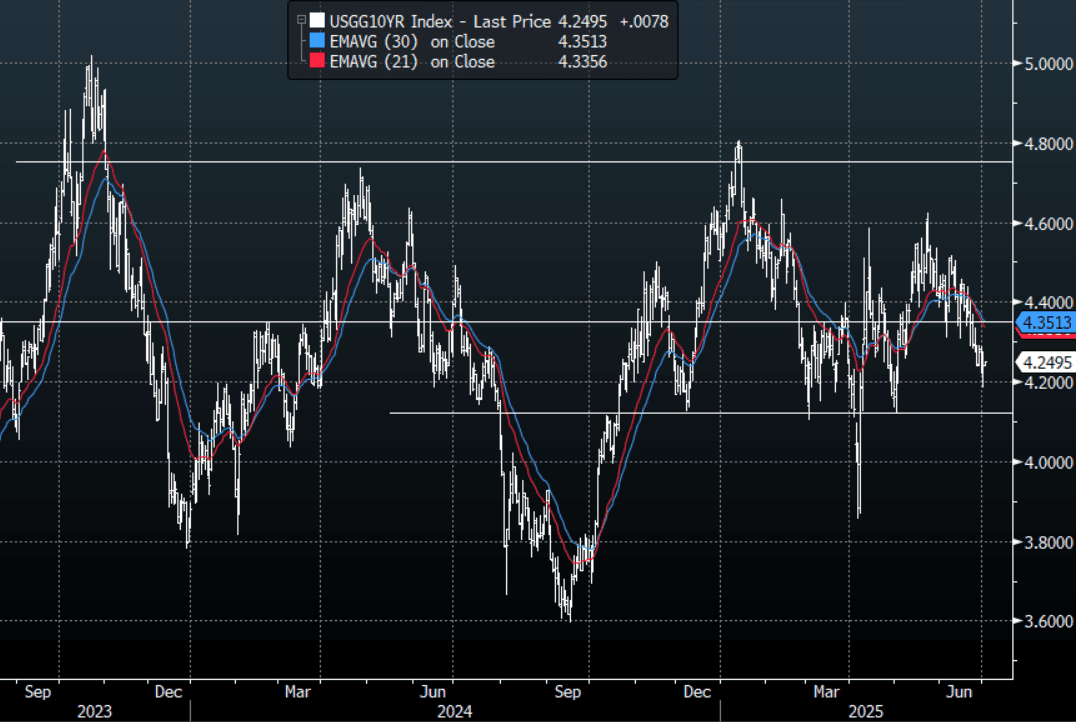

US TSYS: Asia Wrap - Yields Drift Higher

The TYU5 range has been 111-27 to 111-30+ during the Asia-Pacific session. It last changed hands at 111-27, down 0-00+ from the previous close.

- The US 2-year yield has drifted higher trading around 3.776%.

- The US 10-year yield has edged higher trading around 4.25%, up 0.01 from its close.

- The 10-year yield has seen a bounce after a very strong move lower with some paring back of longs ahead of NFP. Any bounce back to the 4.35% area would offer buyers a decent level to add again.

- (Bloomberg) - “Jerome Powell repeated that the Fed probably would have cut rates further this year absent Trump’s expanded use of tariffs, although he didn’t rule out easing at July’s meeting.”

- “The $3.3 trillion US tax and spending bill passed the Senate after JD Vance cast the tie-breaking vote. The House is expected to vote on the package Wednesday, but passage isn’t guaranteed.”(BBG)

- Data/Events: MBA Mortgage Applications, ADP, Challenger Job Cuts

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cash Bond Twist-Flattener, 30Y Supply Tomorrow

JGB futures are weaker and at Tokyo session lows, -13 compared to settlement levels.

- (Bloomberg) -- "Japan will continue actively negotiating tariffs in good faith with the US for both countries' mutual benefit, Deputy Chief Cabinet Secretary Kazuhiko Aoki says at a regular press conference on Wednesday."

- (Bloomberg) Japan’s 30-year bond auction on Thursday will likely see “modest to safe” results, according to Barclays Securities’ strategists Ayao Ehara and Shinichiro Kadota.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No scheduled Fed speakers. Thursday is a heavy data day with NFP added due to the Independence Day holiday closure on Friday.

- Cash JGBs have twist-flattened across benchmarks with yields 1bp higher to 1bp lower, pivoting at the 20-year. The benchmark 10-year yield is 1.4bps higher at 1.408% versus the cycle high of 1.596%.

- Swaps are slightly mixed across maturities.

- Tomorrow, the local calendar will see Weekly International Investment Flow and S&P Global Composite & Services PMI data alongside 30-year supply.

AUSSIE BONDS: Cheaper, Narrow Ranges Ahead Of Key US Data

ACGBs (YM -4.0 & XM -2.5) are modestly weaker after trading in narrow ranges.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's twist-flattener. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at -11bps.

- Today’s Jun-35 auction showed solid pricing for ACGBs, with the weighted average yield coming in 0.45bps below prevailing mid-yields. However, the cover ratio nudged lower to 3.3625x. The AOFM plans to sell A$1000mn of the 2.25% 21 May 2028 bond on Friday.

- The bills strip has bear-flattened, with pricing -1 to -4.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 95% probability, with a cumulative 82bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Tomorrow, the local calendar will see Trade Balance and S&P Global Composite & Services PMIs.

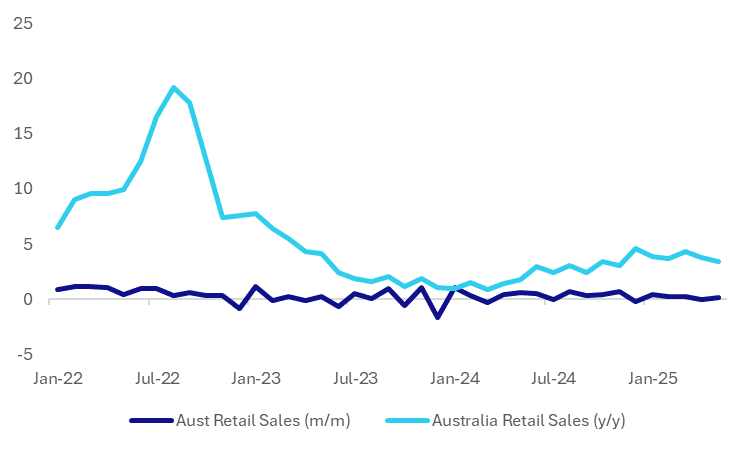

AUSTRALIA DATA: Retail Momentum Softens Further In May, Despite Clothing Bounce

Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- By sub category we had strong rebounds in both apparel retail sales and department store spending. Both categories were up close to 3%m/m, but this follows similar falls in April.

- The ABS noted: "‘Clothing retailers and department stores were boosted by people buying winter clothes, having held off on those purchases with the warmer-than-usual weather last month,’ Mr Ewing said."

- Otherwise, spending trends were either flat or down a touch. Notably food retailing fell by 0.4%m/m, after declining 0.2% in April.

- The y/y pace eased to 3.4% from 3.8% in April, see the chart below. The general trend in spending momentum is too moderate after last year's fiscal impulse for households helped drive a brief strengthening.

- The RBA meets next week, and the market has a 25bps cut priced in. Today's data is likely to reinforce easing expectations at the margin.

- Note this is the second last retail sales release, with the release to be replaced by the household spending series (the next update for this print is on Friday).

Fig 1: Australia Retail Sales Momentum Eases Further

Source: Bloomberg Finance L.P./MNI

BONDS: NZGBS: Closed Subdued Session Modestly Cheaper

NZGBs closed 1-2bps cheaper after a subdued session. There were 2bp ranges across the benchmarks.

- Cash US tsys are little changed in today's Asia-Pac session. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- The NZ-US yield differential closed 2bps tighter on the day. At +25bps, the NZ-US 10-year differential is in the top half of the -20bp to +40bps range seen this year.

- Swap rates closed 1-2bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed across meetings. 4bps of easing is priced for July, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will see Cotality Home Values, ANZ Commodity Prices and NZ Government 11-Month Financial Statements.

- The NZ Treasury launched a syndicated tap of the May 2031 nominal bond. Treasury expects to issue at least NZ$4bn and will cap it at NZ$6bn. Issue will be priced July 3 with initial price guidance +21-24 bps over the May 2030 nominal bond. The Treasury has cancelled the July 3 bond auction.

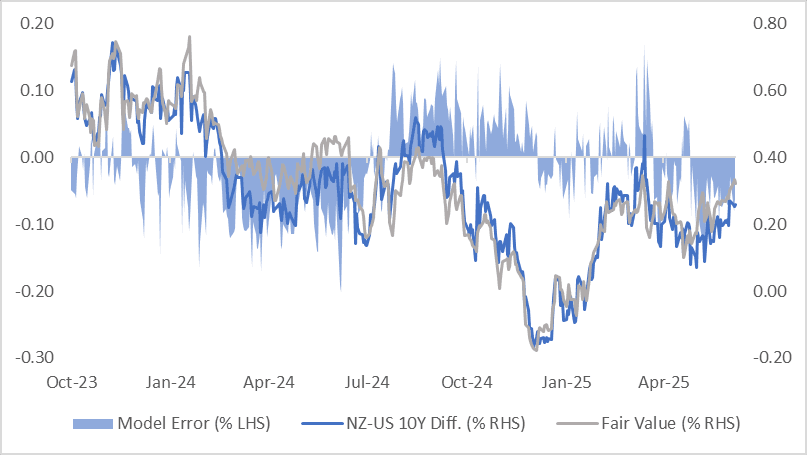

BONDS: NZ-US 10Y Differential In the Top Half Of This Year’s Range

NZGBs are richer today, with benchmark yields 2bps lower. The NZGB 10-year has slightly outperformed US 10-year since yesterday’s close, with the NZ-US yield differentials 2bps tighter on the day.

- At +25bps, the NZ-US 10-year differential is in the top half of the -20bp to +40bps range seen this year.

- A simple regression analysis of the 3-month forward swap rate spread (1Y3M) over the past 18 months indicates the 10-year yield differential is around 7bps below its estimated fair value of +32bps.

- Notably, the regression error has fluctuated within a range of ±15bps over the past year, highlighting some variability in the relationship.

- The 1Y3M differential continues to be a key driver of market expectations for long-term yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

FOREX: Asia FX Wrap - USD Consolidates As The Market Eyes NFP

The BBDXY has had a range of 1188.23 - 1190.00 in the Asia-Pac session, it is currently trading around 1189. The USD has traded sideways today after initially trying lower. The larger picture remains one of USD weakness, short-term though price is beginning to look a little stretched and we could see more profit-taking heading into NFP. In the current environment rallies should continue to be met with supply, first resistance is back towards the 1205/1215 area.

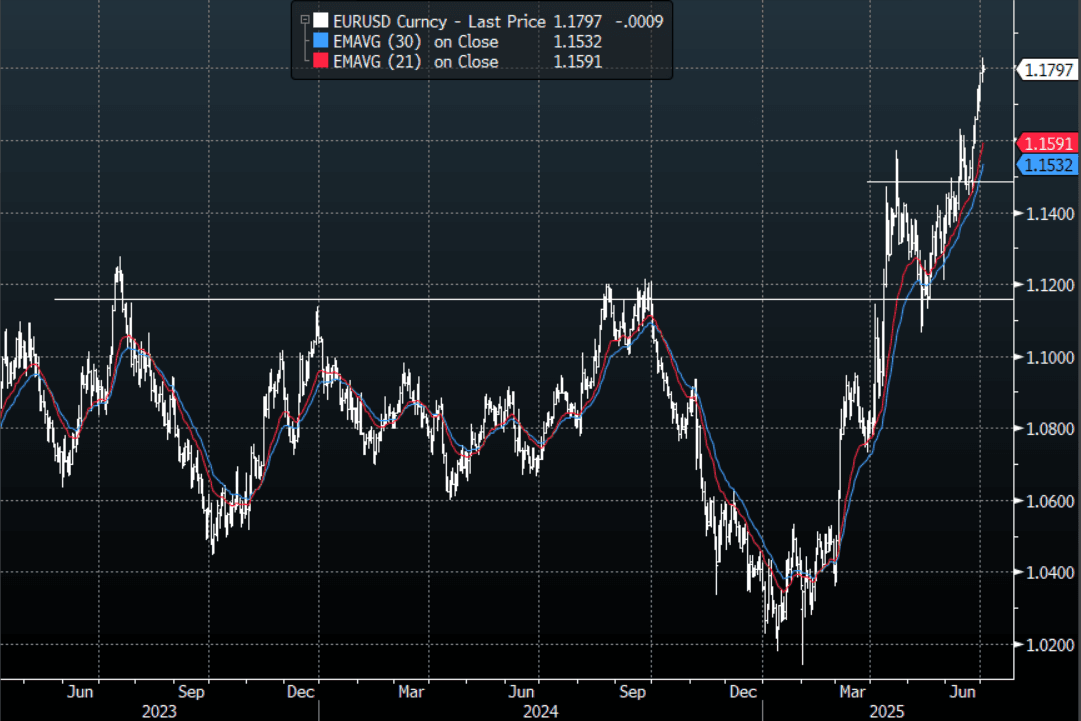

- EUR/USD - Asian range 1.1788 - 1.1810, Asia is currently trading 1.1800. While the USD remains on the back foot the EUR will continue to be supported, short-term it is starting to look stretched the first support is back towards 1.1500/1.1600. The medium term targets will now be towards 1.2000 and beyond.

- GBP/USD - Asian range 1.3732 - 1.3753, Asia is currently dealing around 1.3745.This move higher now looks to have broken convincingly higher and with the USD looking like it is set for another leg lower Cable could potentially now target levels back towards 1.4200. Short-term momentum seems to be stalling first support is back towards 1.3500/1.3600.

- USD/CNH - Asian range 7.1598 - 7.1662, the USD/CNY fix printed 7.1546 Asia is currently dealing around 7.1650. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX +0.27%, Gold $3340, US 10-Year 4.25%, BBDXY 1189, Crude oil $65.50

- Data/Events : Italy Unemployment, France Budget Balance, EZ Unemployment, Spain Unemployment

Fig 1: EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

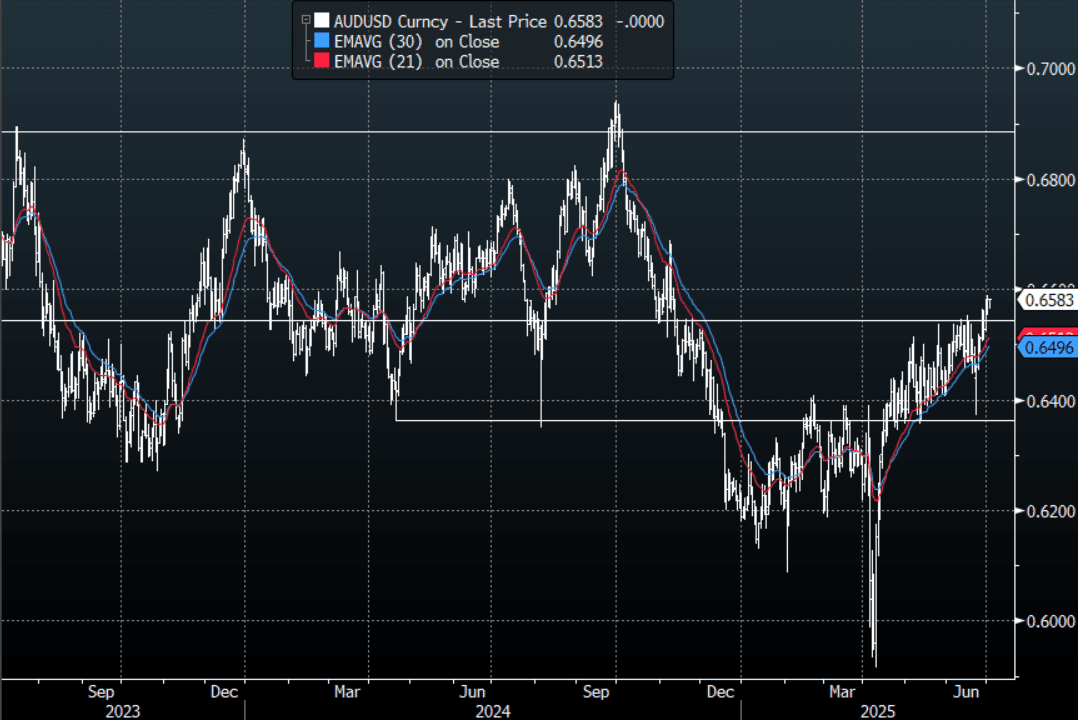

AUD: Asia Wrap - Disappointing Retail Data Finds Bids Around 0.6560

The AUD/USD has had a range of 0.6565 - 0.6583 in the Asia- Pac session, it is currently trading around 0.6583. The pair tested lower on the back of a lower than expected retail sale sprint, bids emerged back around 0.6560 and the pair has erased all of its losses going into London. US Equity futures have drifted higher in Asia, ESU5 +0.30%, NQU5 +0.35%. The market will be watching for signs of this move building upward momentum for a more significant move higher, could the catalyst be NFP on Thursday ?

- Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- (Bloomberg) -- Weak retail sales confirm our concerns about Australia’s consumers, who are keeping their wallets shut despite the Reserve Bank starting rate cuts in February and May. So far, there’s little sign the moves are reviving spending, and a stronger rebound likely hinges on additional easing.

- The AUD/USD is breaking through the top of its recent range as the pressure on the USD increases. First support is seen back towards 0.6500.

- The AUD needs a sustained break above 0.6550/0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn back to 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD654m). Upcoming Close Strikes : 0.6600(AUD2.55bm July4).

- AUD/JPY - Today's range 94.30 - 94.53, it is trading currently around 94.50, +0.1%. Choppy price action as the pair establishes a range between 92.00 - 96.00. Momentum higher seems to be stalling, a break sub 0.9350 would be needed to see the focus turn lower once more.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

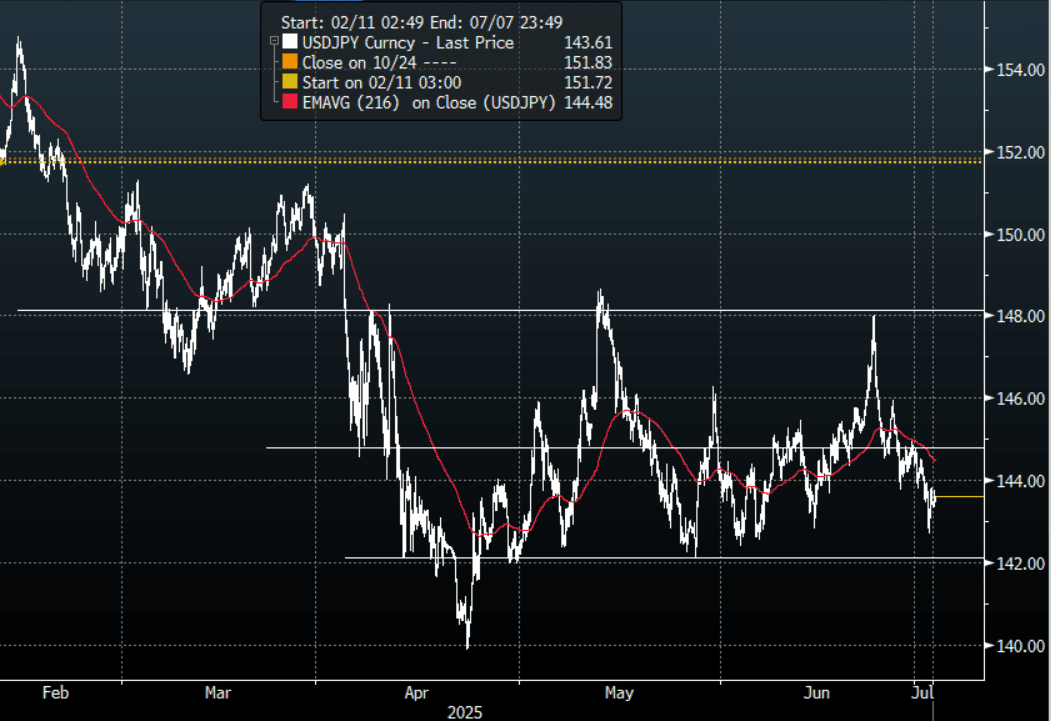

JPY: Asia Wrap - Quiet Session, Trades Sideways

The Asia-Pac USD/JPY range has been 143.32 - 143.75, Asia is currently trading around 143.60, +0.15%. USD/JPY has traded sideways in our session. This pair continues to trade with an offered bias, first resistance is back towards 144.50/145.00 and there should be sellers again eager to participate towards that level. The market will be waiting for NFP on Thursday to provide a potential catalyst to test the 142.00/140.00 area once more.

- (Bloomberg) -- “Japan will continue actively negotiating tariffs in good faith with the US for both countries' mutual benefit, Deputy Chief Cabinet Secretary Kazuhiko Aoki says at a regular press conference on Wednesday.”

- “Japan's super-long bonds are set to remain under pressure in the medium term as local life insurers may offload holdings to sidestep impairment losses on deeply discounted debt.” (per BBG)

- "ISHIBA: TALKS WITH US SEEM MORE ABOUT INVESTMENT THAN TARIFFS” - BBG

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY is looking for a fresh catalyst to probe the lower end of its range again, can the NFP on Thursday provide that ?

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($598m), 144.75(698m).Upcoming Close Strikes : 140.00($1.04b July3).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

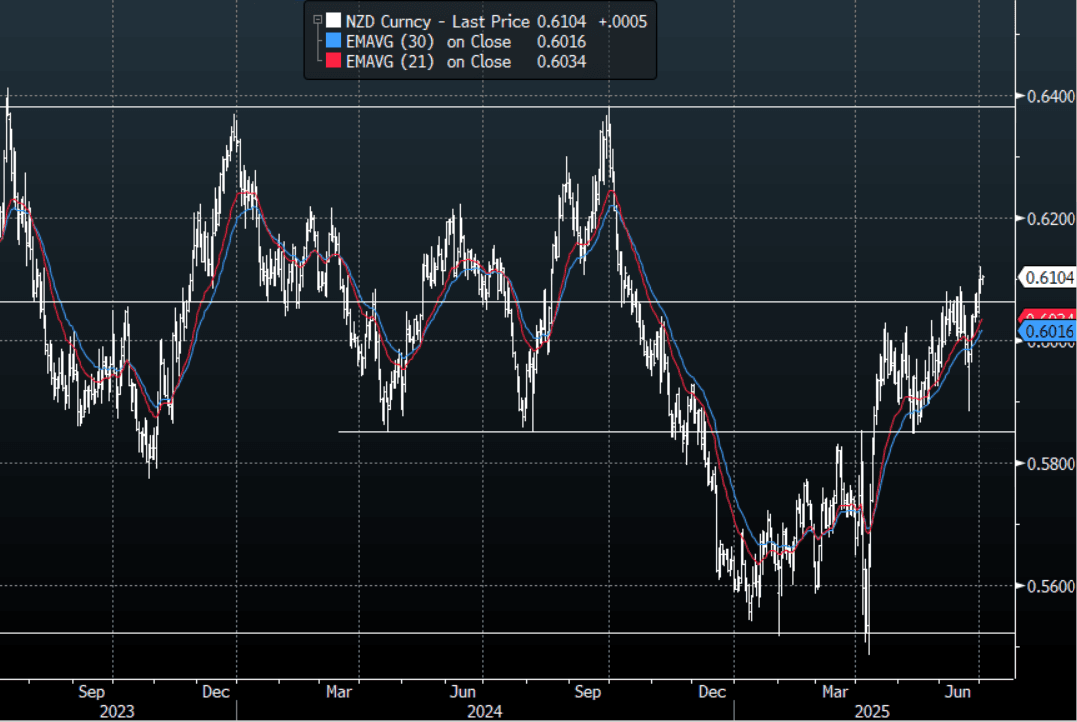

NZD: Asia Wrap - NZD/USD Continues To Be Well-Supported

The NZD/USD had a range of 0.6090 - 0.6106 in the Asia-Pac session, going into the London open trading around 0.6100, +0.05%. A tight range in a relatively quiet Asian session, US Equity futures have also drifted higher in Asia, ESU5 +0.30%, NQU5 +0.38%. The pair is breaking through its recent highs and attempting to build momentum for a potential look back towards the 0.6400/0.6500 area. The relentless pressure on the USD is providing a tailwind and dips towards 0.6000 should continue to see demand. The market will be eyeing NFP on Thursday so there is a good chance we will consolidate until we see if that gives the USD a further nudge lower.

- (Bloomberg) -- “Donald Trump said he’s not considering delaying his July 9 deadline for higher tariffs to resume. He sees a Japan deal as unlikely, saying it should be forced to pay a rate of “whatever the number is that we determine.”

- Whole Milk Prices Nearly 12% Off May Highs : Overnight the whole milk price auction saw a sharp fall. We fell to $3859 from $4084 prior, which was a 5.1% drop between the two auctions. The whole milk price is off close to 12% from its highs at the start of May.

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400/0.6500 area.

- CFTC Data shows Asset Managers have cut their shorts and are now beginning to build a long in NZD +12195, the Leveraged community maintained their short that had just been added to -11981.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5800(649m). Upcoming Close Strikes : none.

- AUD/NZD range for the session has been 1.0777 - 1.0796, currently trading 1.0780. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: A Mixed Day as Tariff Threats Echo Around the Region

Asia stocks were mixed today as the markets await the next raft of US data. As President Trumps latest headlines focus on tariff threats for Japan the tariff deadline looms for most countries. The threat towards Japan was a reminder for Korean investors who drove the KOSPI lower today as Nvidia's supplier SK Hynix slumped. Hong Kong got a bump from Casino stocks as June numbers came in ahead expectations.

- The Hang Seng stood out with gains today of +0.62% whilst CSI 300 rose just +0.07%. The Shanghai Comp did very little, down -0.04% whilst Shenzhen was the worst performer, down -0.45%

- The TAIEX in Taiwan was down modestly by -0.12%

- The KOSPI had two strong days of gains, only to fall on tariff fears today by -0.82%

- The FTSE Malay KLCI gained +0.44% capping off five successive days of gains.

- The Jakarta Composite is down -0.91% for a second successive day of falls.

- The FTSE Straits Times rose by +0.48% whilst the PSEi in the Philippines is down -0.39%.

- The NIFT 50 is down modestly by -0.10% offsetting yesterday's gains.

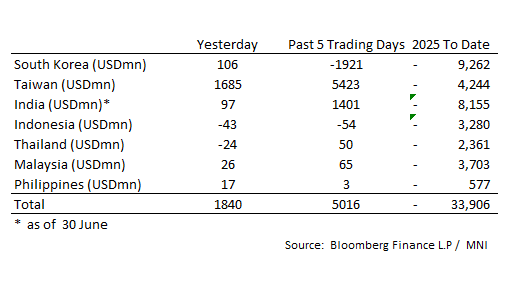

ASIA STOCKS: Taiwan Inflows Continue as Others Moderate

Taiwan enjoys $6.6bn of inflows over last six trading days.

- South Korea: Recorded inflows of +$106m yesterday, bringing the 5-day total to -$1,921m. 2025 to date flows are -$9,262. The 5-day average is -$384m, the 20-day average is +$106m and the 100-day average of -$76m.

- Taiwan: Had inflows of +$1,685m yesterday, with total inflows of +$5,423 m over the past 5 days. YTD flows are negative at -$4,244. The 5-day average is +$1,085m, the 20-day average of +$444m and the 100-day average of -$4m.

- India: Had inflows of +$97m as of the 30th, with total inflows of +$1,401m over the past 5 days. YTD flows are negative -$8,155m. The 5-day average is +$280m, the 20-day average of +$131m and the 100-day average of -$5m.

- Indonesia: Had outflows of -$43 yesterday, with total outflows of -$54m over the prior five days. YTD flows are negative -$3,280m. The 5-day average is -$11m, the 20-day average -$24m and the 100-day average -$31m.

- Thailand: Recorded outflows of -$24m yesterday, with inflows totaling +$50m over the past 5 days. YTD flows are negative at -$2,361m. The 5-day average is +$10m, the 20-day average of -$13m and the 100-day average of -$21m.

- Malaysia: Recorded inflows as of +$26m yesterday, totaling +$65m over the past 5 days. YTD flows are negative at -$3,703m. The 5-day average is +$16m, the 20-day average of -$13m and the 100-day average of -$20m.

- Philippines: Recorded inflows of +$17m yesterday, with net inflows of +$3m over the past 5 days. YTD flows are negative at -$577m. The 5-day average is +$1m, the 20-day average of -$3m the 100-day average of -$5m.

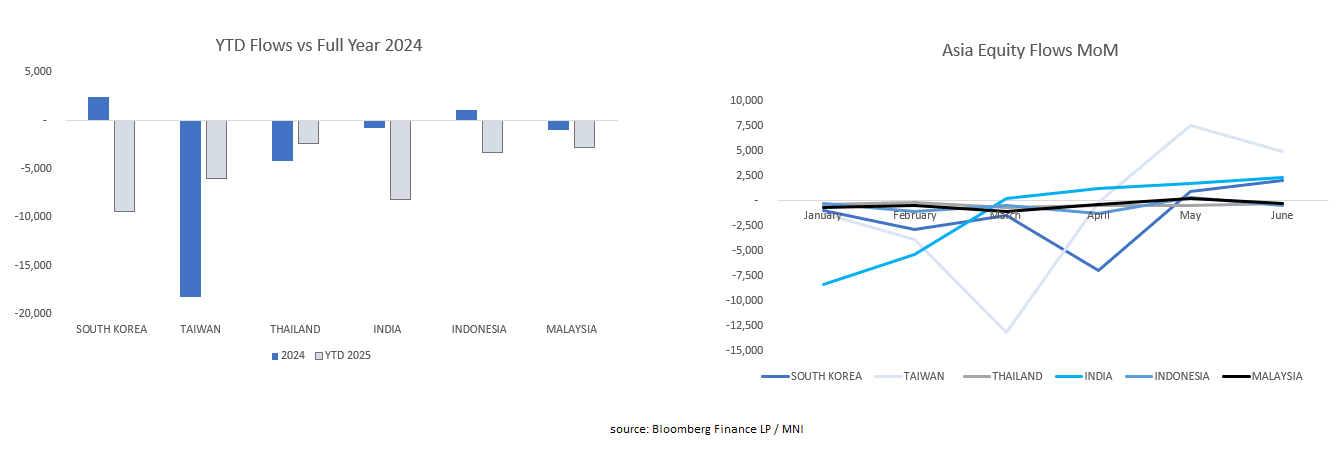

ASIA STOCKS: Is the tide Coming Back in for Asia Stock Flows

- We report each day the flow data for major regional bourses which suffered heavily under the threat of tariffs.

- However in recent months we have seen strong inflows into Taiwan, India and South Korea, and whilst year to date flows remain negative there appears sufficient evidence to ask whether the worst is over for outflows for major regional bourses.

- The flows began to turn positive when tariffs were paused in April with Taiwan the biggest beneficiary thanks to its semi-conductor manufacturers.

- USD weakness is a potential positive catalyst for the second half of 2025 for Asia flows, particularly if trade agreements are reached.

OIL: Price Action Limited Today for Oil

- Both Brent and WTI had limited price movement today, consolidating overnight moves.

- Having finished the US session with gains of +0.52%, WTI opened at US$65.56 bbl and slipped marginally to $65.46 and sits just below the 50-day EMA of $65.54.

- Brent had gone the other way overnight, closing down -0.74% at US$67.25 bbl and is at $67.15 in the Asia trading day, remaining below all major moving averages. The nearest being the 50-day EMA of $68.36

- The IEA forecasts that global oil demand will rise by up to 2.5m barrels a day from 2024-2030 despite EV's forecasting to displace up to 5m barrels per day over the next decade which comes at a time when the OPEC+ group intend to increase production by a further 400k barrels from August.

- President Donald Trump vowed to fill up the nation’s emergency oil stockpile, signaling he would take advantage of low crude prices to replenish the reserve that was drawn down under former President Joe Biden.

- The two-week average for global stockpiles of crude oil rose by a substantial 1.4m b/d over the last three months as large builds of floating storage in the Middle East added to spare inventories, according to Goldman Sachs

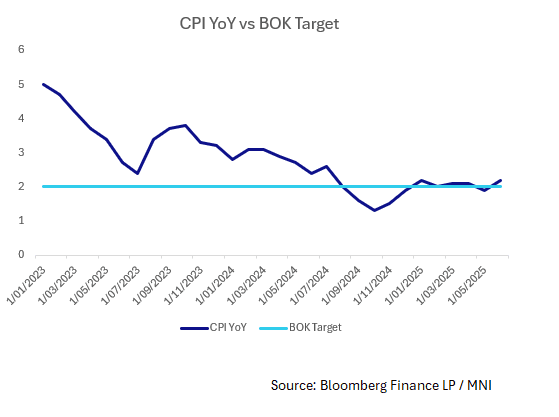

SOUTH KOREA: June CPI Showing Limited Signs of Revival

- South Korea has just released its June CPI and it remains on the BOK 2% target.

- CPI YoY for June rose 2.2% from 1.9% with the small rise likely sufficient to see the BOK on hold at their meeting in July as focus remains on house prices in Seoul which continue to rise rapidly.

- The result was ahead of market expectations of a +2.1% rise with food prices up +3.4% whilst the prices for services moderated.

- The month on month figure was flat and Core was unchanged at 2.0%

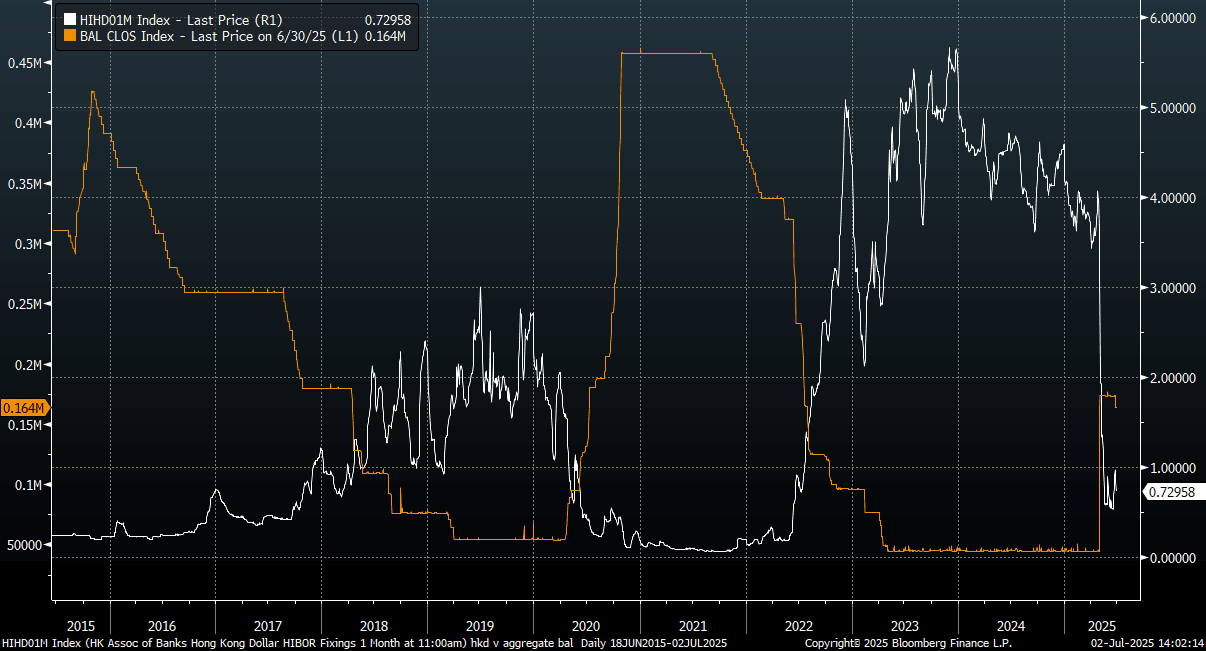

HKD: Spot USD/HKD Back Close To Upper Limit, Hibor Rates Little Changed

Spot USD/HKD has been supported on modest dips so far today. We were last back close to 7.8500, after coming down a touch at the early Asia Pac/NY cross over post HKMA intervention (as USD/HKD tested the upper end of the peg band).

- The Hibor fix hasn't seen a sharp fix in interest rates. The week edged up to 0.19% from 0.156% on Monday (there was no fix yesterday). The 1 month was unchanged around 0.73%, while the 3 month rose a touch, but the 12 month fell to 2.91%.

- USD/HKD spot versus US-HK rate differentials is not providing a compelling case for USD/HKD to retrace lower at this stage.

- The chart below plots the HKMA aggregate balance versus the Hibor 1 month rate. We would expect the aggregate balance to fall as the HKMA intervenes to protect the upside of the peg band at 7.8500. Still, as history shows, the translation into higher Hibor rates (via tighter liquidity) is often varied.

- Some sell-side analysts have noted it will take a while for Hong Kong liquidity to tighten and the authorities may be comfortable with this as it helps keep local rates low, which supports the economy (a point Nomura made back in early June).

Fig 1: Hibor 1 mth & HKMA Aggregate Balance

Source: Bloomberg FInance L.P/MNI

ASIA FX: USD Finds Support, Limited FX Fallout For THB From Political Turmoil

In South East Asia FX markets, there has been a modestly positive USD bias in the first part of Wednesday trade. Broader USD sentiment has stabilized following fresh cycle lows in dollar indices on Tuesday. Some consolidation may be taking place following the recent sharp sell-off and ahead of tomorrow's key US NFP release. MYR has lost close to 0.50% so far today, with losses elsewhere more modest.

- Spot USD/MYR has risen back above 4.2150. Lows yesterday were close to 4.1800, which was levels last seen in Oct 2024. The 20-day EMA resistance points sits closer to 4.2400 in terms of upside resistance levels.

- USD/THB was last up slightly on end Tuesday levels, holding in the 32.45/50 region. FX fallout from fresh political turmoil (with PM Paetongtarn Shinawatra now suspended) has been limited so far. The recent rebound in gold has likely helped at the margins. Still, the turmoil may weigh on domestic confidence and growth, pushing the BoT to ease further.

- USD/IDR is a touch higher, last around 16230, up 0.20% versus end Tuesday levels. Recent lows rest close to 16170. Broader risk sentiment is showing less upside from an equity market standpoint, while local stocks are down around 0.90% so far today. Onshore fiscal deficit concerns are another potential headwind, although arguably a wider deficit will not come as a huge surprise to the market (see this BBG link).

- USD/PHP is close to unchanged last around the 56.32 level.

ASIA FX: TWD Gains, USD/HKD Supported As Hibor Rates Steady

In North East Asian FX markets, outside of TWD gains, trends have been fairly steady, consistent with the majors. The BBDXY index is little changed after making fresh cycle lows yesterday, with some consolidation possible as markets await the US NFP print tomorrow.

- USD/CNH was last near 7.1650, slightly up on end NY levels for the pair, but very much within recent ranges. The USD/CNY fixing edged higher but the error term returned to a negative bias. Onshore equities are little changed.

- Spot USD/KRW got to highs of 1363.85, not too far from the 20-day EMA resistance point. We now sit back though at 1359, little changed for the session. Earlier headwinds were from weaker equities (Kospi losses now under 1%), while broader USD trends were also a likely driver. Inflation figures for June showed core and headline CPI still close to the 2% target.

- Spot USD/TWD has bucked the USD consolidation trend seen elsewhere. This pair was last down close to 0.40% and threatening a re-test of 29.00. The equity inflow backdrop has been very strong in recent sessions. We would expect the central bank to remain vigilant though around a sharp break sub 29.00 in the pair, as this could impact life insurers in terms of their offshore holdings/hedging. The pace of TWD appreciation is still likely to managed.

- Spot USD/HKD is back close to 7.8500, after a brief dip in the first part of trade as the HKMA intervened to protect the top end of the peg band. The intervention hasn't seen a spike in Hibor rates though, hence the limited USD/HKD downside.

INDONESIA: Country Wrap: Budget Deficit Up

- Indonesia expects to post a much bigger budget deficit this year due to weak revenue collections and the acceleration of President Prabowo Subianto’s priority programs. The shortfall is estimated at 2.78% of gross domestic product, higher than the 2.5% initially targeted in the 2025 budget, the Finance Minister said in a mid-year fiscal update to parliament on Tuesday. (source BBG)

- Bank Indonesia sees local currency strengthening to a range of 16,000-16,500 against the greenback in 2026, Governor Perry Warjiyo says in parliament briefing. BI will keep taking measures to stabilize rupiah amid global volatility and look for room to cut policy rate further, Warjiyo reiterates (source BBG)

- The Jakarta Composite is down -0.91% for a second successive day of falls.

- The Rupiah is down today by -0.23% to 16,238

- Bonds were mixed across the curve with the 10YR +1bp higher at 6.61%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/07/2025 | 0800/1000 | ECB de Guindos Chairs Sintra Panel | ||

| 02/07/2025 | 0900/1100 | ** | Unemployment | |

| 02/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/07/2025 | 0900/1100 | ECB Cipollone Chairs Sintra Panel | ||

| 02/07/2025 | 1030/1230 | ECB Lane Chairs Sintra Panel | ||

| 02/07/2025 | 1030/1130 | BOE Taylor On Panel At Sintra Conference | ||

| 02/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 02/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 02/07/2025 | 1415/1615 | ECB Lagarde Gives Closing Sintra Remarks | ||

| 02/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/07/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/07/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/07/2025 | 0130/1130 | ** | Trade Balance | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/07/2025 | 0630/0830 | *** | CPI | |

| 03/07/2025 | 0700/0300 | * | Turkey CPI | |

| 03/07/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0830/0930 | Decision Maker Panel data | ||

| 03/07/2025 | 0830/0930 | BOE Credit Conditions Survey | ||

| 03/07/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/07/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 03/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 03/07/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/07/2025 | 1230/0830 | *** | Employment Report | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/07/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI |