US TSYS: Asia Wrap - Yields Drift Higher

The TYU5 range has been 111-27 to 111-30+ during the Asia-Pacific session. It last changed hands at 111-27, down 0-00+ from the previous close.

- The US 2-year yield has drifted higher trading around 3.776%.

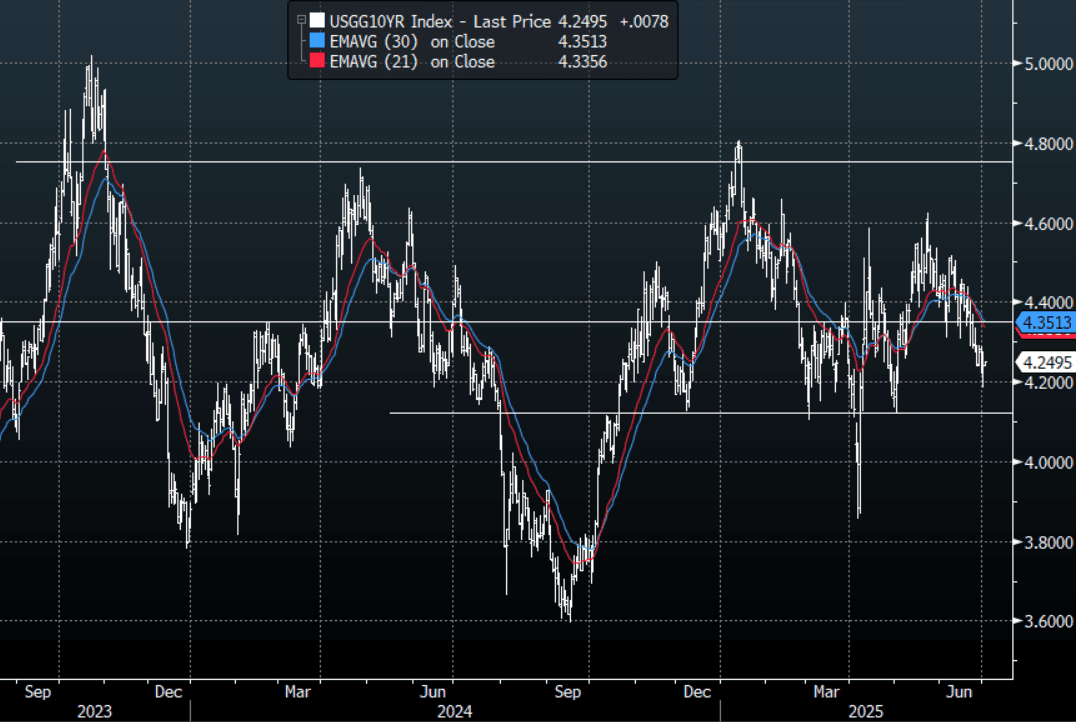

- The US 10-year yield has edged higher trading around 4.25%, up 0.01 from its close.

- The 10-year yield has seen a bounce after a very strong move lower with some paring back of longs ahead of NFP. Any bounce back to the 4.35% area would offer buyers a decent level to add again.

- (Bloomberg) - “Jerome Powell repeated that the Fed probably would have cut rates further this year absent Trump’s expanded use of tariffs, although he didn’t rule out easing at July’s meeting.”

- “The $3.3 trillion US tax and spending bill passed the Senate after JD Vance cast the tie-breaking vote. The House is expected to vote on the package Wednesday, but passage isn’t guaranteed.”(BBG)

- Data/Events: MBA Mortgage Applications, ADP, Challenger Job Cuts

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Long-End A Little Higher

The TYM5 range has been 110-22 to 110-30 during the Asia-Pacific session. It last changed hands at 110-25, up 0-01 from the previous close.

- The US 2-year yield is unchanged, trading around 3.9%, unchanged from its close.

- The US 10-year yield is a little higher, trading around 4.414%, up 0.01 from its close.

- This has seen the yield curve steepen in Asia - 2s10s +1.17 at 50.843, 5s30s +1.71 at 98.14.

- (Bloomberg) - “Federal Reserve Governor Christopher Waller said he continues to see a path to interest-rate cuts later this year amid his expectations that tariffs will boost unemployment and temporarily increase inflation.”

- “Asset managers heavily unwound net long positioning in Treasury futures, with positioning in ultra-long bond futures heavily cut in the week ending May 27, CFTC data show. Hedge funds covered short positions across the curve, taking the other side, with a big short unwind seen in ultra-long bonds.”(BBG)

- AFR via BBG - “JPMorgan chief executive Jamie Dimon on Friday night predicted that a crack in the bond market is “going to happen” - and it will scare the pants off everyone.”

- The 10-year has come back down to test its support around 4.35/40%, likely aided by month-end rebalancing. Yields need to hold above this area to continue to build for a move higher.

- Data/Events : S&P Global US Man PMI, ISM Man, Powell to talk.

JGBS: Belly Leads Yields Modestly Higher At Lunch

At the Tokyo lunch break, JGB futures are weaker, -15 compared to the settlement levels.

- Japan's Prime Minister Shigeru Ishiba announced a minister-level meeting to address the supply of rice and stabilise its price ahead of a summer election.

- “Asset managers’ decision to add to their long yen position through the week ended May 27 is looking a wise one, with the currency back in rally mode and poised to gain more.” (per BBG)

- Cash US tsys have twist-steepened, with yields -1bp lower to 2bps higher, in today's Asia-Pac session. Monday's US calendar sees ISM Manufacturing data and an appearance by Fed Chair Powell, with the June employment report looming at the end of next week.

- Cash JGBs are flat to 2bps cheaper across benchmarks, with the 5-7-year zone underperforming. The benchmark 10-year yield is 1.5bp higher at 1.516% versus the cycle high of 1.596%.

- Swap rates are flat to 1bp higher. Swap spreads are little changed.

CHINA: VIEW: JP Morgan Sees Some Easing In External Pressures

There was a slight improvement in China’s May NBS PMIs with the composite rising 0.2 points to 50.4, holding above the breakeven 50-mark. JP Morgan believes that there should be some “easing” in “near-term external pressure”. It’s “baseline scenario assumes China’s growth to moderate to an average 3%q/q saar pace through the rest of the year, with full-year 2025 GDP growth at 4.8%yoy.”

- JP Morgan sees “the main challenges to the Chinese economy coming from structural imbalance between production, consumption and investment, and deflation pressure, calling for ongoing growth-support measures.”

- “The manufacturing PMI recovered 0.5-pt to 49.5 upon US-China tariff de-escalation, though non-manufacturing PMI fell modestly by 0.1-pt to a 50.3 (four-month low). In all, the composite PMI rose 0.2-pt to 50.4.”

- “The export orders component of the manufacturing PMI recovered by 2.8-pt to 47.5 upon tariff de-escalation, as surveyed corporates reported a notable rebound in export demand from the US market. The new orders and output components also ticked up in May.”

- “The future output component recovered moderately in May, suggesting moderate improvement in manufacturers’ sentiment amid tariff de-escalation and easing of near-term external pressure.”

- “While there have been growing concerns that escalating tariff risks could hit employment notably, it is encouraging to note that labor market conditions seem to have stabilized somewhat amid a near-term improvement in export sector sentiment.”

- “The pricing components of the manufacturing PMI eased further in May, suggesting lingering deflation pressure.”

- “The service activity index edged up 0.1-pt to a still subdued level of 50.2, with major drags from the real estate service sector and financial services.”