MNI EUROPEAN MARKETS ANALYSIS: AUD Higher On RBA Hauser Chat

EXECUTIVE SUMMARY

- ACGBs and NZGBs strengthened ahead of today's release of US Non-Farm Payrolls.

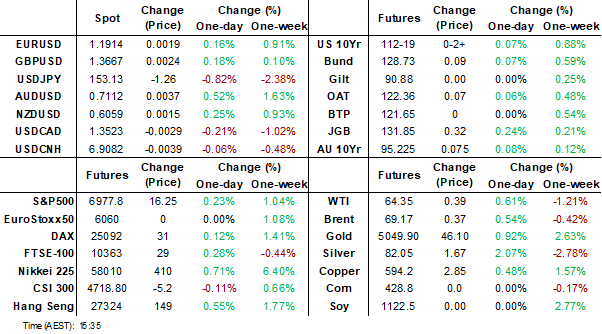

- The USD has fallen below most short-term supports and is looking to the lows seen in January. The AUD took another leg up across the board as the market reacted to Hauser saying they “will do what's necessary to return inflation to target”. USD/JPY has slumped further, now approaching 153.00.

- Weaker than expected overnight data in the US sees gold holding above $5,000 today.

- Coming up the main focus will be the US NFP print.

MARKETS

US TSYS: Cash Closed, Risks of Better NFP Not Priced

With Japan closed, it was only futures that traded today with volumes low. The 10-Yr traded in a range of 112-15+ to 112-19, finishing at the top end of the range for a gain of +02 today.

Its a big day Wednesday for data given the delayed Non Farm Payrolls and various Fed Speakers.

US Data/Speaker Calendar (prior, estimate). All times ET

02/11 0700 MBA Mortgage Applications (-8.9%, --)

02/11 0830 Change in Nonfarm Payrolls (50k, 67k)

02/11 1000 KC Fed Schmid moderated discussion on economy, mon-pol

02/11 1015 Fed VC Bowman moderated discussion

02/11 1130 US Tsy $69B 17W bill auction

02/11 1300 US Tsy $42B 10Y Note auction (91282CPZ8)

02/11 1400 Federal Budget Balance (-$144.7B, -$94.4B)

02/11 1600 Cleveland Fed Hammack on leadership (no text, Q&A)

Source: Bloomberg Finance L.P. / MNI

- There is a US$69bn 17-week and a US$42bn 10-Yr auction tonight

Yields have fallen more than expected in recent days, taking them back below the mid point of the 1 m range. The data suggests the economy is slowing (as evidenced by the recent peak in GDPNow) and yields should be lower. However the risks are now (given recent moves) that NFP in line or marginally stronger could see a modest unwind of the recent rally.

AUSSIE BONDS: Richer Ahead Of US NFP, Stronger Demand Drove Hike - RBA Hauser

ACGBs (YM +3.0 & XM +6.5) are stronger.

- MNI: The Reserve Bank of Australia’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply, Deputy Governor Andrew Hauser said.

- There has no cash US tsys dealings in today's Asia-Pac session, with Japan out on holiday.

- All focus turns to today's US employment data. Monthly payroll growth is currently expected at 70k in January for a slight acceleration from the 50k in December and 56k in November.

- Cash ACGBs are 2-5bps richer, with the 3/10 curve flatter.

- The latest ACGB April 2037 auction attracted solid demand, with the weighted average yield printing 0.68bps through prevailing mid-yields.

- Moreover, the cover ratio jumped sharply to 4.1429x from 3.4933x at the previous auction. The AOFM also plans to sell A$1000mn of the 2.50% 21 May 2030 bond on Friday.

- The bills strip has bull-flattened, with pricing flat to +3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 93% by June and 146% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data alongside the RBA’s Senate Testimony and RBA Hunter’s Speech.

Bloomberg Finance LP

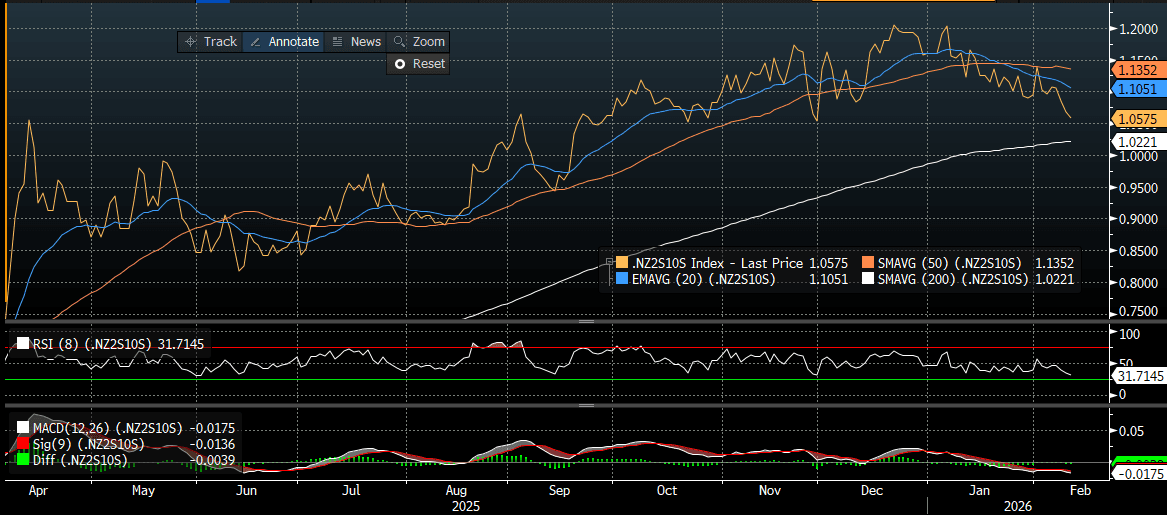

BONDS: NZGBS: Bull-Flattener Leaves Curve At Its Flattest Since Nov

NZGBs closed showing a bull-flattener, with benchmark yields 2-4bps lower.

- Nevertheless, NZGBs underperformed ACGBs with the NZ-AU 10-year yield differential 2bp wider on the day.

- There has no cash US tsys dealings in today’s Asia-Pac session, with Japan out on holiday.

- (Bloomberg) “New Zealand’s government has started an independent review of New Zealand’s monetary policy response to the Covid-19 pandemic. Purpose of the review is to identify lessons New Zealand could learn to improve the monetary policy response to future major events.”

- Swap rates closed 2-5bps lower, with the 2s10s curve flatter. At 1.06, the curve is at its flattest since late November (see chart).

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 43bps.

- The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP

FOREX: USD - BBDXY Testing 1175-1180 Into Employment Data

The BBDXY has had a range today of 1179.42 - 1183.25 in the Asia-Pac session; it is currently trading around 1179, -0.25%. The USD has fallen below most short-term supports and is looking to the lows seen in January now. It does not take a lot for the sellers to come back to market as nobody wants to miss out on this trade. The break lower in US yields is just adding to the USD headwinds and the market will be bracing for more bad news from the employment data tonight. On the day, the first resistance is toward the 1185-1187 area and then 1195 where I suspect we could see sellers return. A sustained break below 1175-1180 could potentially signal the start of another leg lower targeting 1150 first and then potentially 1115.

- EUR/USD - Asian range 1.1886-1.1915, Asia is currently trading 1.1915. The pair is consolidating around 1.1900 as the USD comes back under pressure and we await US employment data tonight. Price action has been pretty constructive after the initial sell-off and the support just below 1.1800 proved to be solid, can it now build some momentum from that base ? On the day, the first support is back toward the 1.1860-1.1890 area and then 1.1770-1.1800.

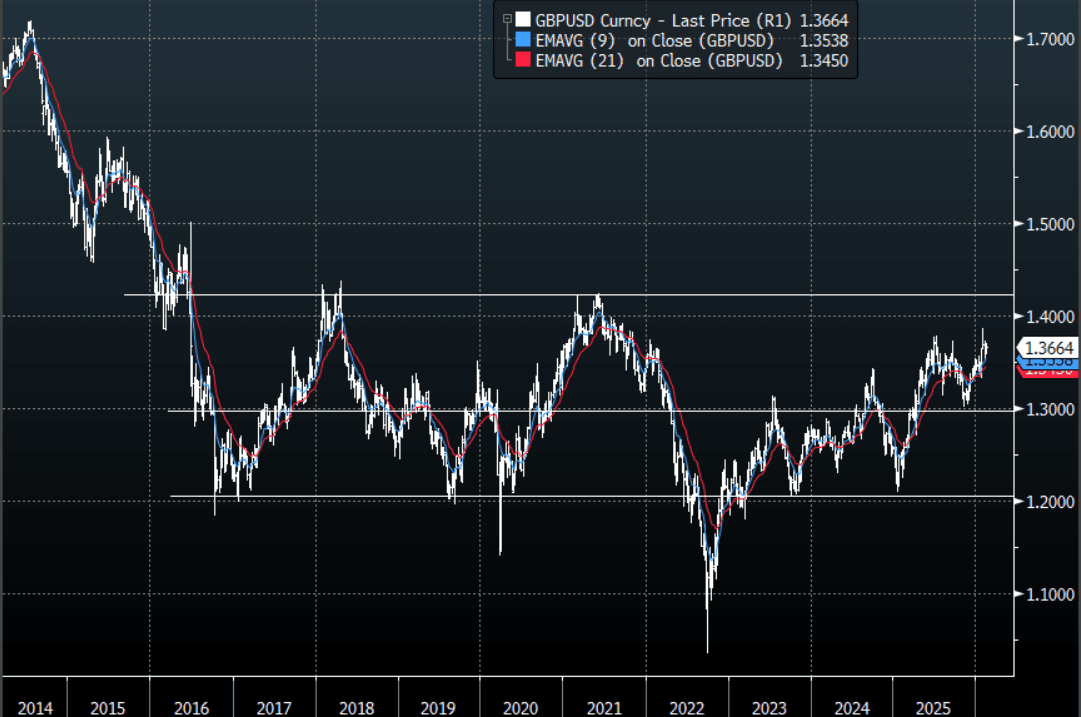

- GBP/USD - Asian range 1.3632-1.3670, Asia is currently dealing around 1.3665. The pair like everything is trying to bounce as the USD struggles. GBP looks like 1.3580-1.3730 to me for now as we wait to see if the big USD could potentially break lower. Should this play out then a move back above 1.4000 is back on the cards.

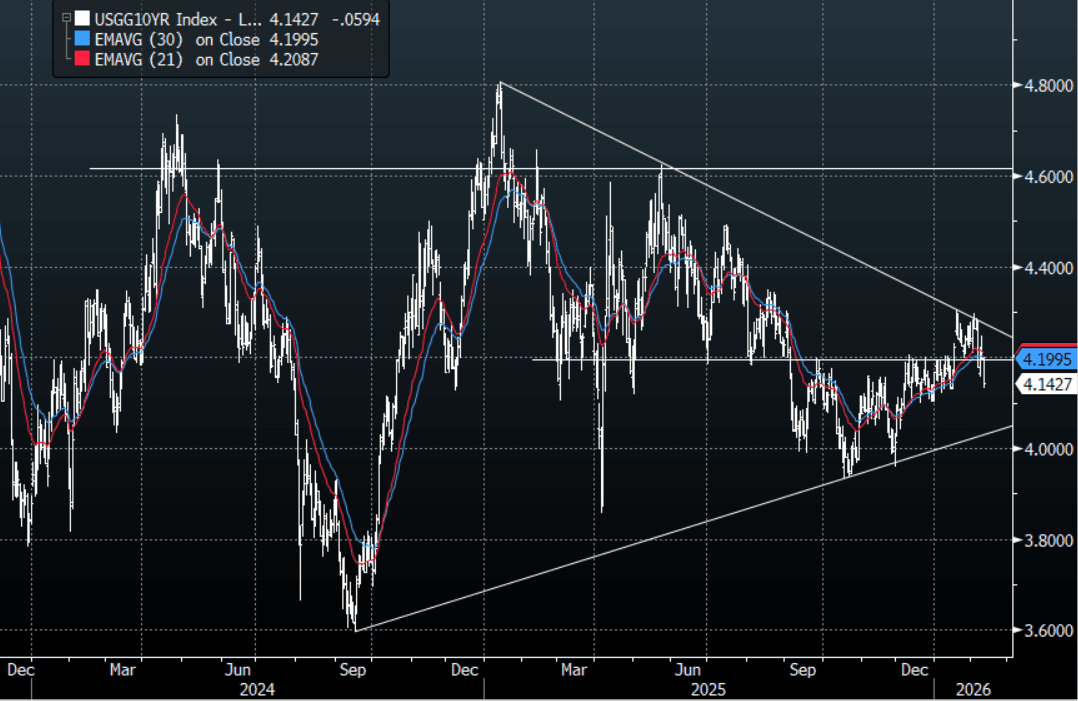

- Cross asset : SPX +0.30%, Gold $5057, US 10-Year 4.14%, BBDXY 1179, Crude Oil $64.48

- Data/Events : Italy Industrial Production

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Continues To Drift Lower As The USD Trades Poorly Into NFP

The USD/JPY range today has been 153.51 - 154.52 in the Asia-Pac session, it is currently trading around 153.55, -0.55%. USD/JPY could not bounce at all and was back under pressure from the open and has remained so all through our session. The price action on Monday in response to the election outcome showed it was mostly priced in, and we have seen some “buy the rumour, sell the fact” play out. I thought we would see better demand back toward the 155.00 area initially but this move in US yields is causing the Yen shorts some angst. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone as we await tonight's US labour data which will directly impact that move in US yields. On the day, the first resistance is back towards 154.75-155.15 and then the 155.80-156.20 area as the market pares back its USD longs and looks for another base to from from which to move higher again.

- “Deutsche Bank strategists said they’re no longer bearish on the yen after PM Sanae Takaichi’s election victory.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.50($1.16b), 156.60($550mm). Upcoming Close Strikes : 158.50($1.57b Feb 13), 159.00($1.91b Feb 13),160.00($3.06b Feb 13) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 154 Points

Fig 1 : US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

OPTIONS: +$3bn In USD/JPY Options So Far Today, O/N Vol Elevated Ahead Of NFP

In the FX option space, JPY volumes have dominated so far in Wednesday trade, with around $3.1bn in total volumes so far. This is 46.6% of total volumes, per DTCC via BBG and comes despite onshore markets in Japan being out today. Next on the volumes list is USD/TWD with 10.8% of total volumes. AUD/USD, which has broken above 0.7100 for the first time since 2023 just under $600mn in FX options volumes so far today (around 9.5% of total).

- For USD/JPY, the larger volume transactions ($100mn or more), are mostly for puts, with a variety of strike levels. A 143 strike, expiry end April this year was executed for +200mn per DTCC. This comes as USD/JPY continues to unwinds its pre-election bounce, amid signs that government wants to earn the markets trust around fiscal policy etc. Softer US yields are also weighing on USD/JPY.

- USD/JPY risk reversals are rolling back over, but are above late Jan lows. The 1 month is around -1.64.

- In the vol space, overnight vol is elevated near 16.45%, which reflects the upcoming US payrolls print later. Other implied vol measures are sub 10%.

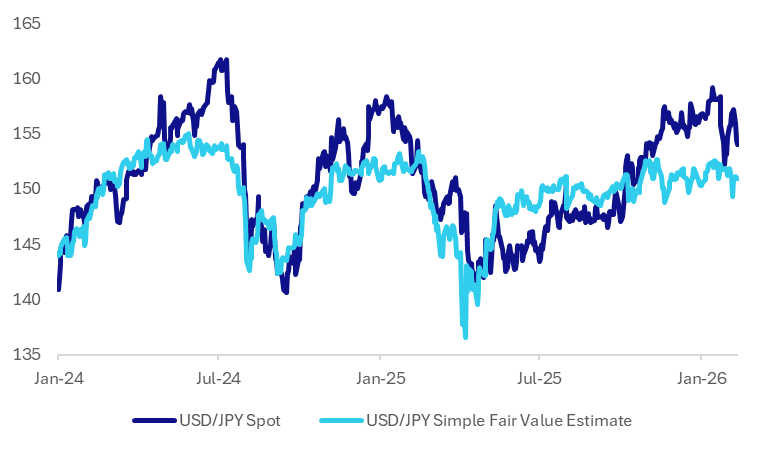

JPY: USD/JPY Correction Lower Continues, But Still Above Simple Fair Value

USD/JPY continues to correct lower, last near 153.90/95, earlier we had fresh lows in the pair (153.84) back to the end of Jan. The run higher in USD/JPY in lead up to the weekend election continues to be unwound. Plotted below is USD/JPY versus our simply fair value estimate, which is written off US-JP 2yr swap rate differentials and global equities. The fair value estimate is lower, last under 151.00. We have see the 2yr spread continue to narrow, last under +200bps, which is lows back to the first part of 2022. Global equities are up from recent lows, but aren't showing a strong upward trend at this stage. The recent low in the fair value estimate was 149.3, which reflected a combination of softer global equities and lower swap rate differentials.

- The wedge between current spot levels and the fair value estimate is back to around 1.95%, the narrowest since Jan 27. We have seen a fairly persistent wedge between spot and fair value since Nov last year.

- Some premium appears to be coming out of the so called Takaichi trade (the tendency for a weaker yen, JGBs, stronger equities, although local Japan equities are performing strongly), with comments from the PM around responsible fiscal management (lowering debt to GDP etc) and wanting to build trust with the market has no doubt helped both JPY and JGB sentiment.

- Our policy team also noted - Takaichi, whose coalition secured a two-thirds supermajority in Sunday’s general election, maintains that decisions on raising borrowing costs rest with the BOJ, despite her strong mandate to tackle the cost-of-living crisis.

- Softer US data outcomes, ahead of tonight's US NFP print, have also helped US-JP downside yield momentum. US yields have fallen sharply in recent sessions, so is a poor NFP print already priced in to some extent? Perhaps, but the longer term trends around US-JP yield differentials look skewed lower.

- Our FX technical team notes important support on the downside: 152.10 Low Jan 27 and the bear trigger.

Fig 1: Spot USD/JPY Versus Simple Fair Value Estimate

Source: Bloomberg Finance L.P./MNI

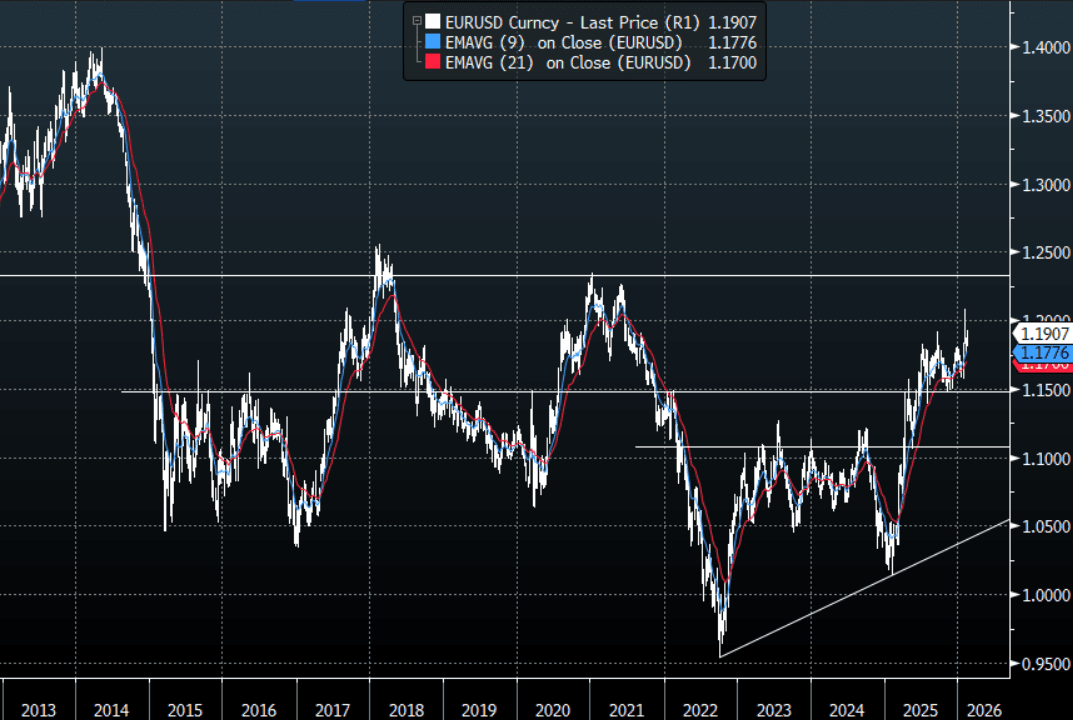

EUR/USD - Consolidating Gains Above 1.1900 Heading Into US Employment

The EUR/USD range overnight was 1.1887 - 1.1929, Asia is currently trading around 1.1905. The pair is consolidating around 1.1900 as the USD comes back under pressure and we await US employment data tonight. Price action has been pretty constructive after the initial sell-off and the support just below 1.1800 proved to be solid, can it now build some momentum from that base ? On the day, the first support is back toward the 1.1860-1.1890 area and then 1.1770-1.1800.

- MNI BRIEF: ECB Villeroy: Downside Risks A Little Stronger. In an interview with Les Echos published Tuesday, Villeroy said that ECB monetary policy was in a "good place" but that did not mean the current policy stance was either comfortable or fixed, noting that "risks to the downside for price developments nevertheless seem to me to be a little stronger than the risks to the upside".

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.1825(EU1.22b), 1.2000(EU2.17b). Upcoming Close Strikes : 1.1800(EU2.68b Feb 13), 1.1850(EU3.89b Feb 13), 1.1950(EU2.36b Feb 13) - BBG

- The EUR/USD Average True Range for the last 10 Trading days: 67 Points

Fig 1 : EUR/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

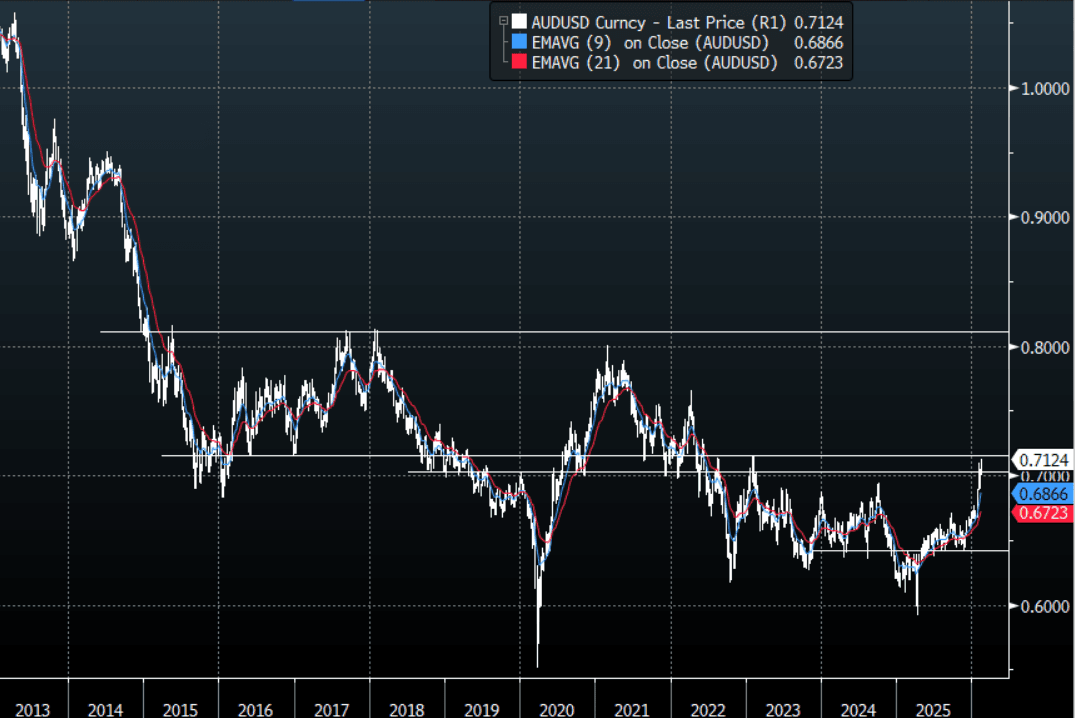

AUD/USD-Extends Above 0.7100 As Hauser Says: "Will Do What's Necessary"

The AUD/USD has had a range today of 0.7067 - 0.7128 in the Asia- Pac session, it is currently trading around 0.7125. The AUD took another leg up across the board as the market reacted to Hauser saying they “will do what's necessary to return inflation to target”. The USD is again back under pressure and the move lower in yields overnight is just adding to its headwinds, the AUD remains a favourite vehicle to express a long against it. The AUD has been outperforming across the board as leveraged funds continue to add to their longs as further hikes are potentially priced in. On the day, the first support is back toward the 0.7040–0.7070 area, and then the 0.6950 area. The bulls will be looking for dips to remain supported in order to break above the pivotal 0.7100-0.7200 area. A sustained break above here targets 0.7600-0.7800 first and then 0.8000-0.8200.

- "HAUSER: WILL DO WHAT'S NECESSARY TO RETURN INFLATION TO TARGET" - BBG

- MNI BRIEF: Stronger Demand Drove Hike - RBA's Hauser. The RBA’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply. The reason policy turned around in February is because the facts changed,” he said, referring to last week’s decision.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7010(AUD560m). Upcoming Close Strikes : 0.6800(AUD1.55b Feb 13), 0.6850(AUD933m Feb 12) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 80 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

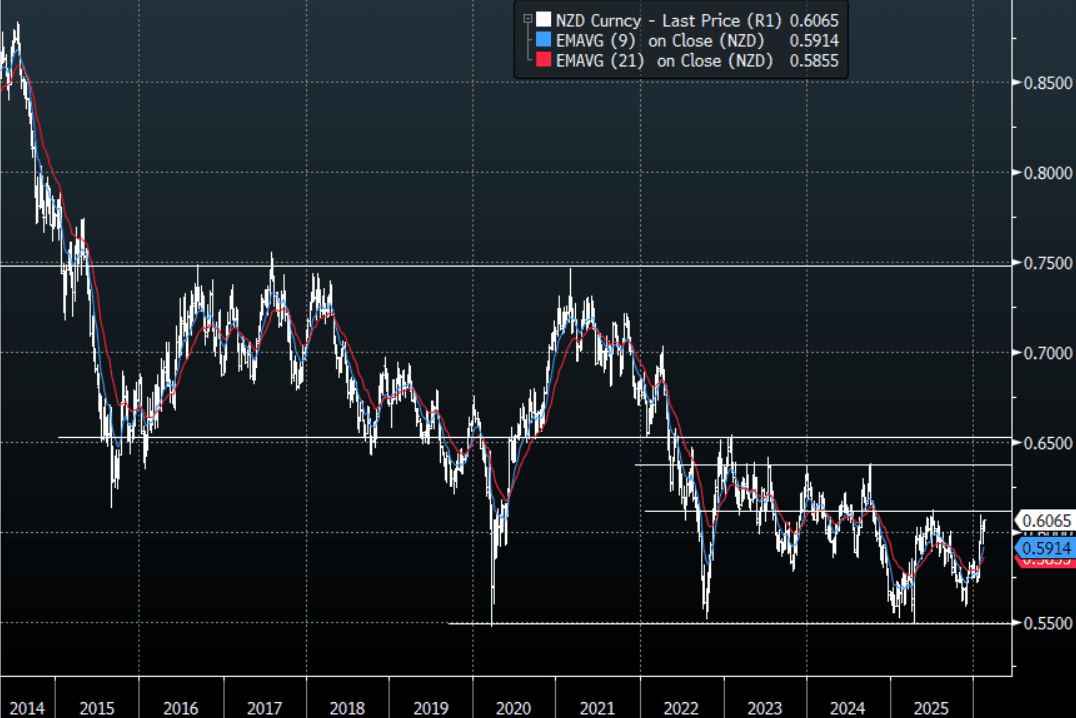

NZD/USD - Dragged Back Toward 0.6100 As The USD Gets Hit

The NZD/USD had a range today of 0.6037-0.6066 in the Asia-Pac session, it is currently trading around 0.6065, +0.33%. The NZD is pushing above its overnight highs that saw its momentum stall as the USD trades poorly into NFP. On the day, the NZD bulls will be hoping the pair can maintain its upward momentum to test the pivotal 0.6100 area. The first support is back toward 0.6025-0.6045 and then the 0.5900-0.5950 area. A sustained break back above 0.6100 could potentially open up a move back toward the 0.6400-0.6600 area and then beyond.

- MNI - Westpac Expects RBNZ To Raise Rates More Quickly In 2027: Westpac now expects the RBNZ to raise rates more quickly in 2027 (as spare capacity is exhausted). It maintains the start of the hiking cycle is expected in Dec of this year. The next RBNZ meeting is on Feb 18, next Wednesday. Market pricing, per OIS markets, is very flat for the first few meetings this year (around 2.25%, the current target rate). A full 25bps hike is priced by around the Oct meeting this year.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5900(NZD301m Feb16), 0.6200(NZD430m Feb 16) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 61 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Positive Bias Continues on JN / AI Optimism; Eyes on NFP

- Despite Japanese markets closed today, optimism from the PM's recent landslide victory continued to provide a supportive regional backdrop. The day’s primary driver was cooling U.S. retail sales. This raised expectations for Federal Reserve rate cuts later this year, boosting risk appetite across the region. Markets look ahead tonight to non farm payrolls for further indications for rates with Trump talking up NFP prospects, whilst FED officials suggest rates are on hold for some time.

- China's CPI for January missed expectations whilst the PPI remained in contraction, though base effects were strong. While this underscored weak domestic demand, it also increased expectations for further stimulus from Beijing to hit its 2026 growth target. Moves in China's major bourses were muted today with HSI up +0.4% whilst CSI 300 was down -0.15%

- The KOSPI and TAIEX - both considered tech heavy - were higher today with the TAIEX up +1.6% on TSMC gains of +2.4% and the KOSPI up +1.2% despite a mixed day for AI stocks. Despite recent global volatility in tech valuations, Asian tech hubs like South Korea and Taiwan remain well supported by global investors with recent days seeing in a surge of inflows into Taiwan stocks.

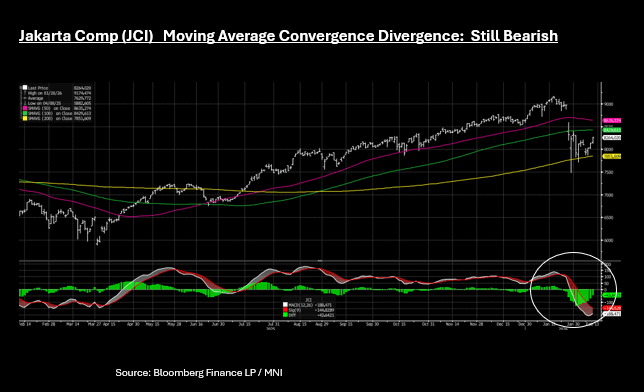

- The JCI has delivered three consecutive days of strong gains, up +1.6% today at 8,270; near to the upside resistance via the 100-day EMA at 8,359. Momentum indicators remain bearish for the JCI with the MACD line below the signal. A negative MACD value means the 12-day Exponential Moving Average (EMA) is significantly below the 26-day EMA.

OIL: Bias for Higher Prices on US Iran Threats

- The Trump administration has discussed whether to seize Iranian oil tankers involved to pressure Tehran but have held off, concerned about the regime's near-certain retaliation and the impact on global oil markets, U.S. officials said. (per BBG)

- President Trump has said that the leadership in Tehran “want to make a deal. I think they’d be foolish if they didn’t,” according to remarks to Fox Business. Wednesday in the US he is due to meet with Israeli Prime Minister Benjamin Netanyahu at the White House to discuss the situation with oil investors looking for indications as to the next steps.

- The American Petroleum Industry reported inventories swelled by 13.4 million barrels last week, which would be the largest jump in barrel terms since November 2023 if confirmed. (per BBG)

- WTI edged up +0.8% today to US$64.49 bbl, having traded in a tight range of $64.15 - $64.63.

- Brent has edged up +0.7% today to US$69.30 bbl, having traded in a tight range of $69 - $69.46.

- Longer term trends driven by over supply are likely to be ignored in the short term. With momentum indicators broadly neutral, oil prices are biased to rise on US Iran headlines and Wednesday in the US could bring further indications on the next steps in negotiations.

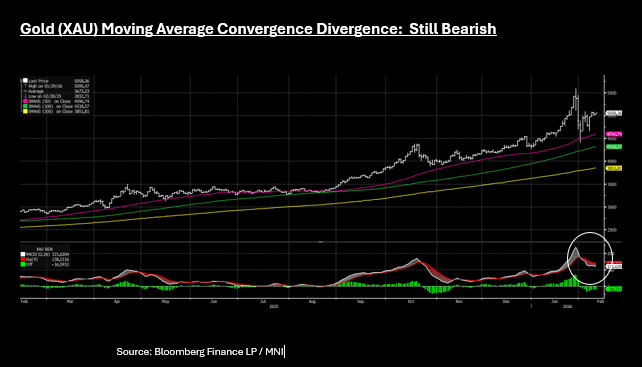

GOLD: Bearish Momentum Remains, Steadies Above $5,000

- Weaker than expected overnight data in the US sees gold holding above $5,000 today as investors position for rate cuts in the US.

- Gold has generally trended higher today in Asia, up +0.80% at US$5,058 - trading in a $5,026 - $5,060 range.

- Gold may climb to $6,000 an ounce by the end of the year as macroeconomic and geopolitical risks persist, according to BNP research (per BBG). This is one of the highest forecasts for gold with ranges of around $5,000 to $6,000 most prevalent.

- Gold short term momentum still remains bearish according to the MACD with the MACD (white) line below the Signal (red) line, a bearish sign.

- The volatility this month for gold seems far from over as we look ahead to non farm payrolls for a steer on US interest rates and the Trump and Netanyahu meeting on Iran.

CHINA: CPI Misses With LNY Distortions

- CPI YoY in January rose just 0.2%, missing the consensus forecast of 0.4% and down from 0.8% in December. The MoM edged up 0.2%, matching the December pace but falling short of the 0.3% forecasts. Core CPI slowed to 0.8% YoY, down from 1.2% driven by base effects and food prices.

- PPI remained negative, reflecting continued pressure on industrial profitability. Down 1.4% YoY, it was an improvement over December's 1.9% decline. However this is the 40th consecutive month of declines, reflecting weak domestic demand and overcapacity in manufacturing.

- Calls for monetary policy intervention remain with the PBOC pledging in its latest quarterly report to employ “flexible and efficient” cuts to interest rates and RRR to maintain an accommodative financial environment emphasizing a deepening coordination with fiscal policy to lower financing costs and boost domestic demand, according to Shanghai Securities News. Undoubtedly expectations will grow ahead of the National People's Congress in March.

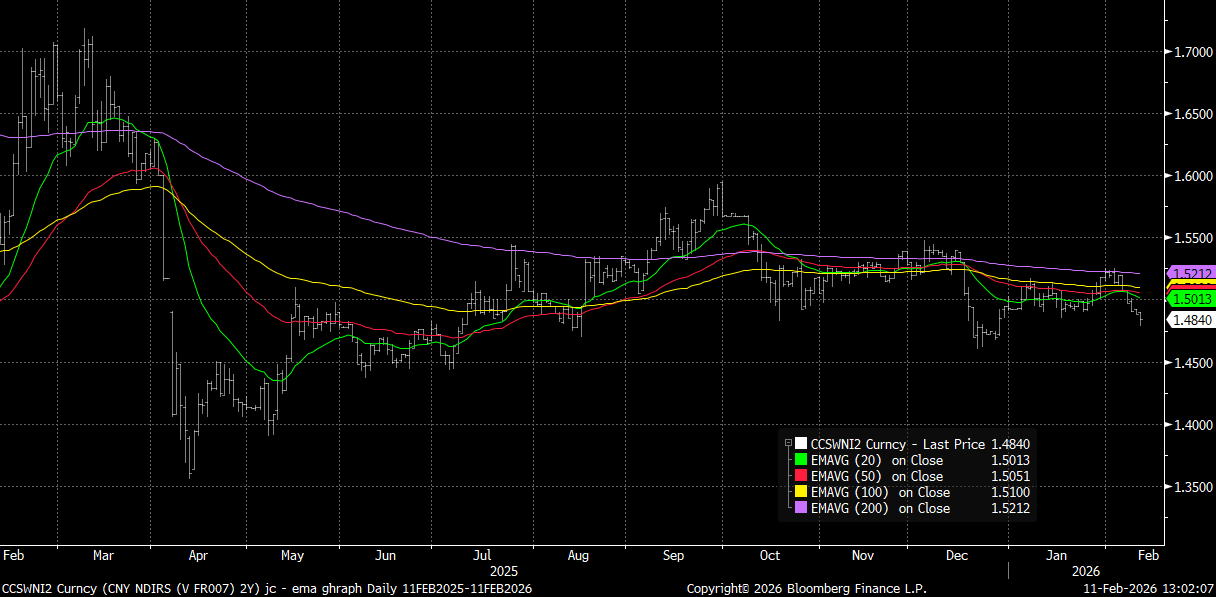

- China bond futures are up modestly, the 10-Yr up +.06 at 108.53 and the 2-Yr flat at 102.47. The 2-Yr NDIRS has broken below major moving averages and could test the December lows.

- CGB 10-Yr is modestly lower in yield at 1.80% following liquidity injections this morning during the OMO.

- Look for further liquidity support ahead of the LNY and the 10-Yr to test below 1.80% .

CNY 2-Yr NDIRS vs 20, 50, 100 and 200-day EMA

source: Bloomberg Finance LP / MNI

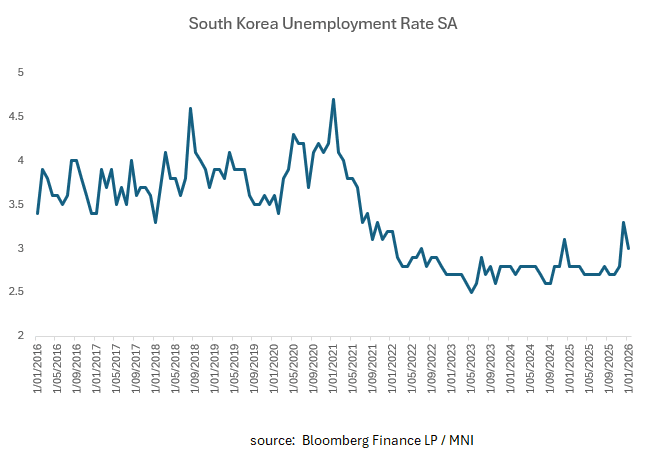

SOUTH KOREA: Unemployment Drops, Details Show Mixed Picture

- South Korea's unemployment rate fell to 3.0% in January , down from 3.3% in December. While the rate itself improved, the overall labor market showed signs of slowing, posting its weakest job growth in 13 months.

- The number of unemployed persons stood at 1.21 million, an 11.8% increase compared to the previous year with the youth unemployment rate rising to 6.8%.

- New applicants for job-seeking benefits rose by 8.0% year-on-year to 201,000 in January, primarily driven by the health, welfare, and business service sectors.

- The economy added only 108,000 jobs year-on-year, the smallest gain since December 2024, led by health and social welfare services (+185,000) and transportation/storage (+71,000). whilst manufacturing sector shed 23,000 jobs, its 19th consecutive month of decline, whilst construction fell for the 21st straight month, losing 20,000 jobs.

- The headline result is enough to support a further hold from the BOK but look for a policy response from the government to boost employment in the first half of the year.

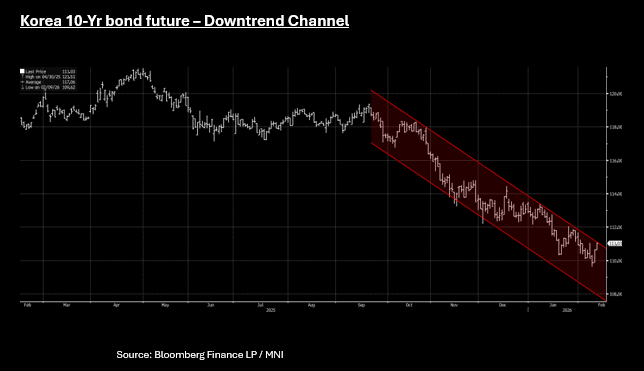

SOUTH KOREA: Bond Futures Post Strong Gains; Remain in Downtrend Channel

- Korean bond futures are up strongly in the morning session following the dual leads from the UST moves overnight and strength in JGBs. The 10-Yr is currently up +.343 at 111.05, near to the topside resistance from the 20-day EMA of 111.05. Earlier the 10-Yr reached a high of 111.11 but as the impact from the orders at open dissipate, has settled back below the 20-day EMA.

- The gains this morning see the 10-Yr remain within the downtrend channel that began in October as markets started to price rate cuts previously priced. Currently there is very limited priced in over the course of the next 6 months as the BOK and government focus on the Won and cooling the housing market respectively.

- The 3-Yr future is up strongly also Wednesday. The 3-Yr reached a high of 105.02 earlier before moderating to 105.00 for gains of +.13 today.

- Cash is strong with yields up to -4.5bps lower on the curve, with longer bonds outperforming. The 10-Yr has consolidated back below 3.70%, and is currently at 3.64% today (down -4.5bps) yet the 10-Yr remains above the mid point of the 1 month range

- The KOSPI has posted modest gains of +0.55% this morning and the Won modest gains.

- Later we get bank lending to households. This is eagerly watched by bond investors for signs that policy is slowing mortgage growth.

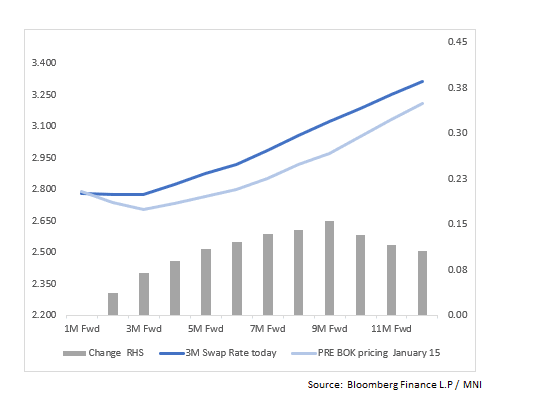

SOUTH KOREA: KRW Swaps: Rate Expectations Diminished; Hikes Priced by Year End

- The January 15 Bank of Korea meeting saw it hold its benchmark interest rate steady at 2.50% for the fifth consecutive meeting, a decision that saw some short term upward pressure on KTB yields. The 10-Yr KTB rose around 25bps in the weeks after, but has retraced some of those moves in recent days.

- The BOK hold was seen as hawkish and an end to the easing cycle, pushing the 10-year yield to its highest in more than a year.

- At year end, the remnants of rate cuts remained priced in for early 2026 but they are now gone. Over the next 1, 2 and 3 months there is no change priced into our swaps model and over the next 12 months +54bps (from +66bps last week) of increases all of focused in Q3/Q4

- The MIPR function on BBG has +39bps of increases over a 12 month period, from +42 last week .

- Later in the week Korea releases export / import prices which are a good indicator for future inflation pressures.

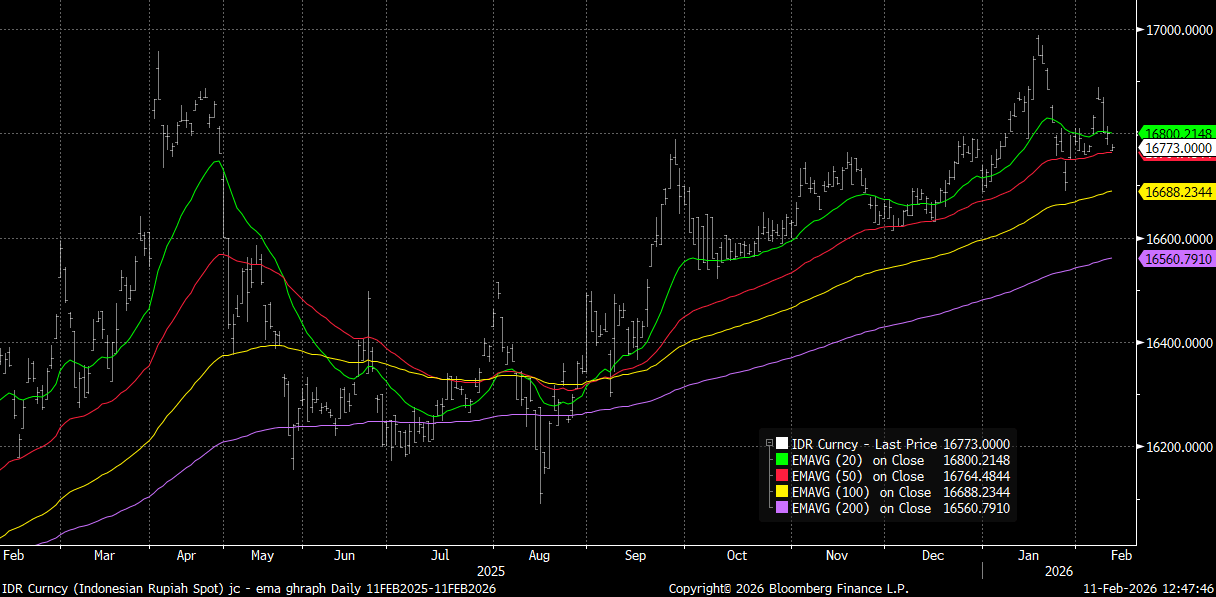

IDR: USD/IDR Testing Key Tech Support Levels as USD Weakness Returns

- Strong regional gains against the USD has seen USDIDR test a key resistance level this morning. USDIDR opened at 16,773 and has traded in a 16,764 - 16,778 range and is currently near 16,764 / 16,775 on USD weakness.

- We are testing 50-day EMA support a break below now brings the 100-day EMA into play at 16,702 . Still, moves under the 50-day EMA have bene very short lived going back to Sep last year.

- Yesterday FTSE Russell said that it will postpone a review planned for March following feedback from an advisory committee and considering "adverse turnover and the uncertainty in determining the accurate free float percentages of Indonesian securities." FTSE Russell will freeze new entrants to benchmarks nor any adjustment to existing. This comes on the back MSCI announcement, creating uncertainty for Indonesia stocks and risk sentiment in general.

- IDR is close to flat month to date versus the USD, and down 0.50% YTD, one of weaker performers in EM Asia in 2026 to date.

- Still, risk sentiment in Indonesia today is good with the JCI up +0.50% and bond yields lower by 1 to 1.5bps following global leads. This is likely aiding IDR, but it remains to be seen how much follow through there is.

- Yesterday the BI deputy governor quoted low inflation as a supportive factor for further rate cuts. Short term momentum indicators are broadly neutral leaving USDIDR vulnerable to USD moves.

Source: Bloomberg Finance L.P/MNI

TWD: USD/TWD Back Under 31.50, But TWD Gains Likely To Remain A Grind

Spot USD/TWD is seeing a little more downside today, last back under 31.50. We are around 0.25% stronger in TWD terms so far today, but still comfortably above late Jan lows for the pair (near 31.27). The 200-day EMA is around 31.14, which we haven't been under since Oct last year.

- Outside of broader USD weakness, macro trends look favourable for TWD, amidst an equity market rally (Taiex up a further 1.8% today to fresh cycle highs), supported by offshore inflows. The past trading month has seen around $1.8bn in cumulative offshore inflows, which is not stretched from an historical standpoint. The growth backdrop looks to be on firm ground in early 2026 given the export/tech demand outlook.

- Implied vols remain close to recent lows, the 1 month last around 5.825%. Market expectations are for TWD gains to likely be a steady grind rather than a dramatic shift against this backdrop.

- 2025 highs in implied vol were above 16% in early May, as spot USD/TWD plunged under 30.00 in quick order. A repeat of such a sharp move seems unlikely given shifts in lifer FX hedging practices and with a US-Taiwan trade agreement now in play.

- For the lunar new year break, Taiwan markets are out for Feb 16-20 (next Mon-Fri). Before than we get 2025 GDP estimates this Friday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 11/02/2026 | 0900/1000 | * | Industrial Production | |

| 11/02/2026 | 1020/1120 | ECB's Cipollone In Digital Finance Conference Fireside Chat | ||

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | - | *** | New Loans | |

| 11/02/2026 | - | *** | Money Supply | |

| 11/02/2026 | - | *** | Social Financing | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture At Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada meeting minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack | ||

| 12/02/2026 | 0700/0700 | *** | UK Monthly GDP | |

| 12/02/2026 | 0700/0700 | ** | Trade Balance | |

| 12/02/2026 | 0700/0700 | ** | Index of Production | |

| 12/02/2026 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/02/2026 | 0700/0700 | ** | Index of Services | |

| 12/02/2026 | 0700/0700 | *** | GDP First Estimate | |

| 12/02/2026 | 0900/1000 | ECB's Cipollone At Commissione Europa Conference |