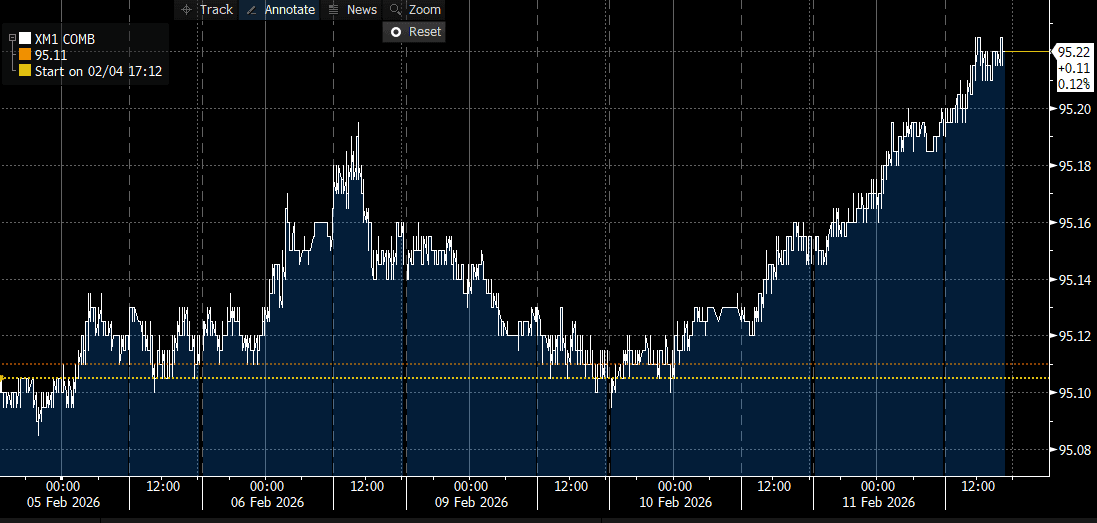

AUSSIE BONDS: Richer Ahead Of US NFP, Stronger Demand Drove Hike - RBA Hauser

ACGBs (YM +3.0 & XM +6.5) are stronger.

- MNI: The Reserve Bank of Australia’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply, Deputy Governor Andrew Hauser said.

- There has no cash US tsys dealings in today's Asia-Pac session, with Japan out on holiday.

- All focus turns to today's US employment data. Monthly payroll growth is currently expected at 70k in January for a slight acceleration from the 50k in December and 56k in November.

- Cash ACGBs are 2-5bps richer, with the 3/10 curve flatter.

- The latest ACGB April 2037 auction attracted solid demand, with the weighted average yield printing 0.68bps through prevailing mid-yields.

- Moreover, the cover ratio jumped sharply to 4.1429x from 3.4933x at the previous auction. The AOFM also plans to sell A$1000mn of the 2.50% 21 May 2030 bond on Friday.

- The bills strip has bull-flattened, with pricing flat to +3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 93% by June and 146% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data alongside the RBA’s Senate Testimony and RBA Hunter’s Speech.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUR: EUR/USD - Catches A Bid In Asia, Look For Sellers Back Toward 1.1665-95

The Friday night range was 1.1618 - 1.1660, Asia is currently trading around {EURUSD Curncy}. The pair is getting an early bounce in Asia as the USD gets sold on reports the FED is to potentially be indicted. We are firmly back in the 1.1450-1.1850 range which dominated the last 6 months of the year and we need a catalyst to get a break and some sort of a trend going again. It will be interesting to see how much of a headwind this news brings for the USD as it was just looking to build a head of team to test higher. On the day look for sellers to reemerge in EUR/USD back toward the 1.1665-1.1695 area.

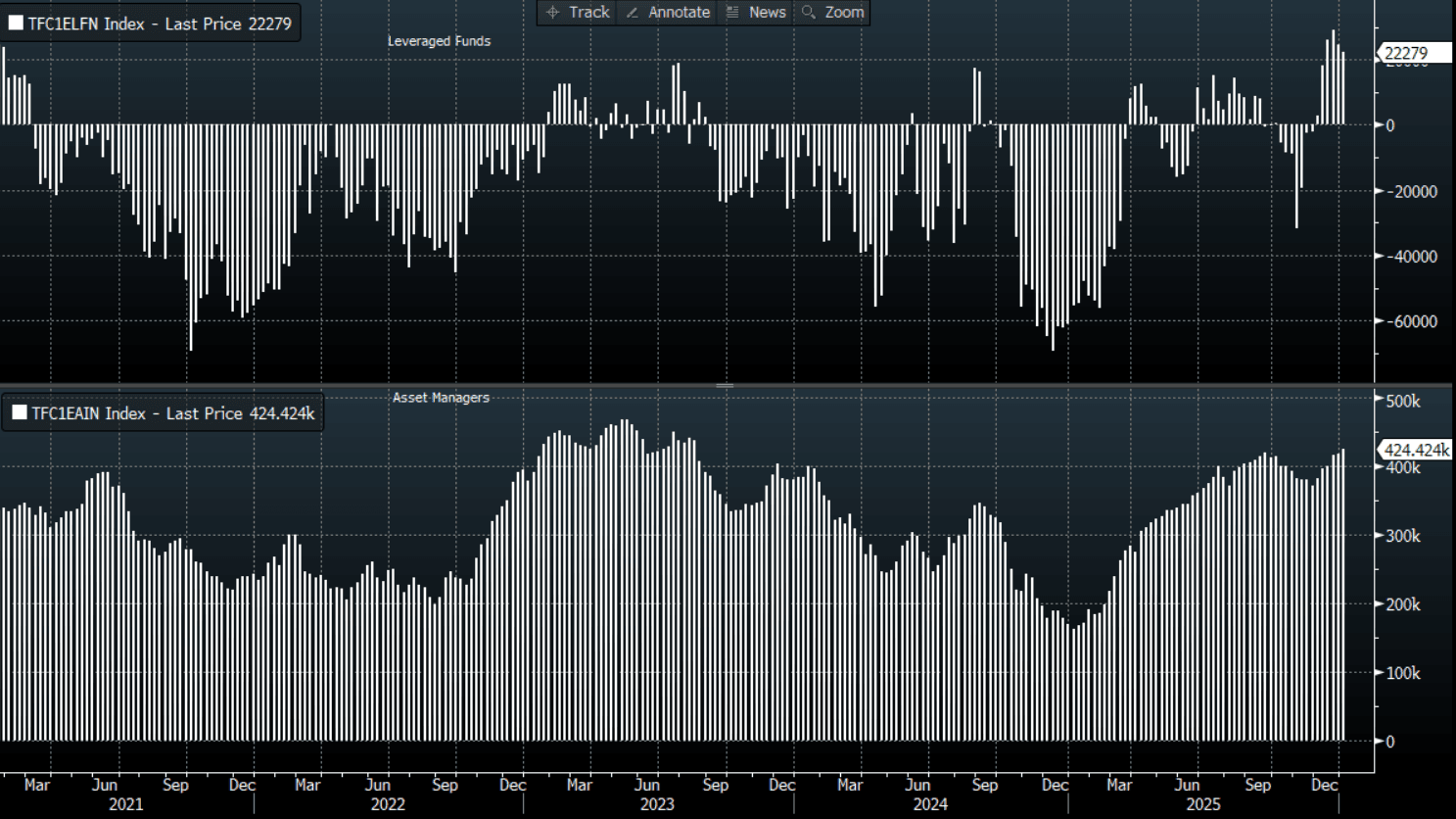

- CFTC Data of last week shows Asset Managers slightly increasing their long positions in the EUR, +424 424(Last +416 483). The Leveraged community reduced their own longs slightly which have only recently been built up, +22279(Last +24505).

- The EUR/USD Average True Range for the last 10 Trading days: 44 Points

Fig 1 : EUR CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

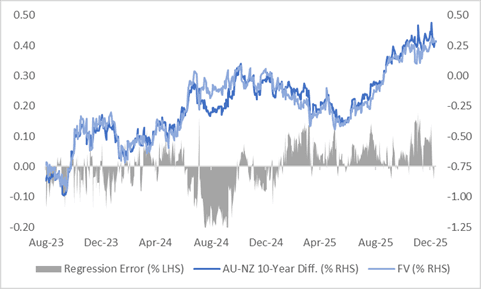

AUSSIE BONDS: AU-NZ 10Y Differential At FV

The AU–NZ 10-year yield differential currently sits at +28bps, around 10–15bps below its recent peak of approximately +40bps, the widest since October 2020.

- The widening in the long-end spread has been mirrored by shifts in market expectations for the policy rate differential over the next year, as reflected in the AU–NZ 1-year forward 3-month swap (1Y3M) spread.

- A simple regression analysis of the AU-NZ 10-year yield differential against the AU-NZ 1Y3M spread over the past two years shows that the 10-year differential is around fair value based on the regression model.

Figure 1: AU-NZ: 10-Year Yield Differential Vs. FV

Source: Bloomberg Finance LP / MNI

USD: BBDXY - Knee-Jerk Lower To Start The Week On FED News

The BBDXY range Friday night was 1209.18 - 1213.00, Asia is currently trading around {BBDXY Index}. The USD was looking like it was reestablishing some upward momentum to start the year, but this morning's news of possible indictments on the FED have put a dent in that for now. The market's perception is that this is clear political pressure being brought to bare on the FED and so has worrying implications for its so-called independence. The USD has understandably had a knee-jerk lower in Asia, the question is if that move is enough considering what's at stake. On the day, I suspect rallies could remain heavy in the short-term as the market tries to work through what this means. First support is back between 1205-1207, the USD has lacked any clear direction for at least 6 months now and the wider 1185-1230 range looks set to continue for now. This lack of a trend is being reflected in the CFTC data which shows very little positioning in the USD to start the year.

- The Market Ear on X - "US flip from exceptionalism to expansionism is best case for a contrarian US dollar long" (Hartnett)

- Barchart on X - “Google Searches for Dollar "Debasement" soared last quarter to the highest level in history.”

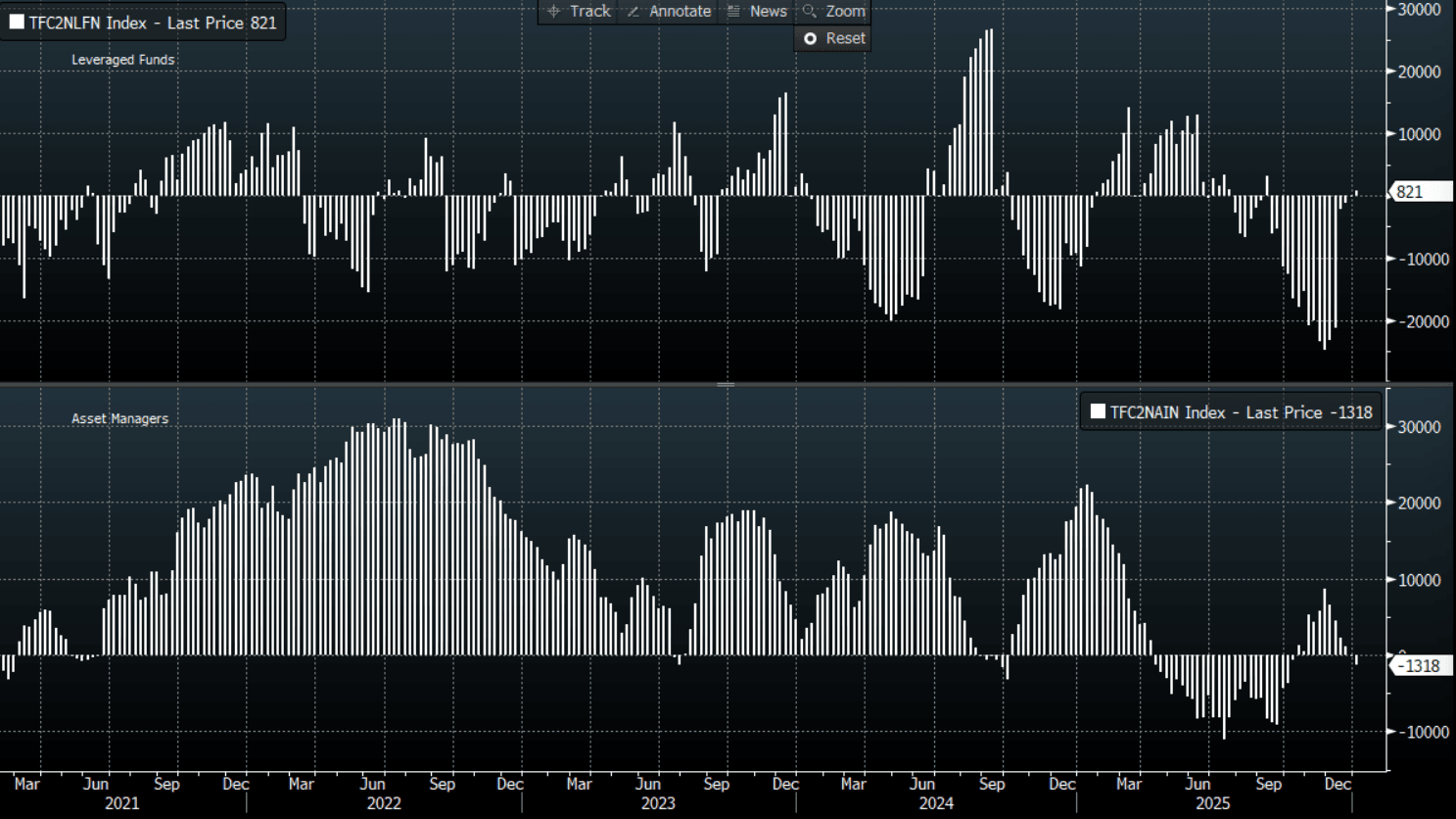

- CFTC Data last week shows Asset managers turning slightly entering the first quarter, -1318(Last +1168). The Leveraged community has turned slightly long after rapidly reducing its short into the end of year, +821(Last +45).

- The BBDXY Average True Range for the last 10 Trading days: 381 Points

Fig 1: USD Index CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P