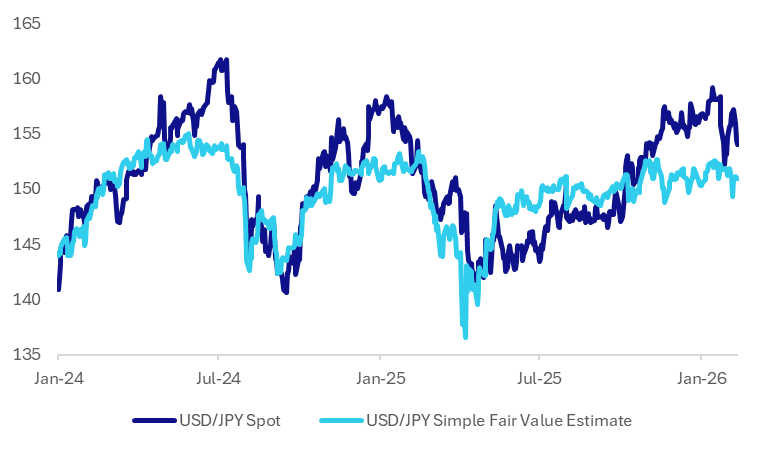

JPY: USD/JPY Correction Lower Continues, But Still Above Simple Fair Value

USD/JPY continues to correct lower, last near 153.90/95, earlier we had fresh lows in the pair (153.84) back to the end of Jan. The run higher in USD/JPY in lead up to the weekend election continues to be unwound. Plotted below is USD/JPY versus our simply fair value estimate, which is written off US-JP 2yr swap rate differentials and global equities. The fair value estimate is lower, last under 151.00. We have see the 2yr spread continue to narrow, last under +200bps, which is lows back to the first part of 2022. Global equities are up from recent lows, but aren't showing a strong upward trend at this stage. The recent low in the fair value estimate was 149.3, which reflected a combination of softer global equities and lower swap rate differentials.

- The wedge between current spot levels and the fair value estimate is back to around 1.95%, the narrowest since Jan 27. We have seen a fairly persistent wedge between spot and fair value since Nov last year.

- Some premium appears to be coming out of the so called Takaichi trade (the tendency for a weaker yen, JGBs, stronger equities, although local Japan equities are performing strongly), with comments from the PM around responsible fiscal management (lowering debt to GDP etc) and wanting to build trust with the market has no doubt helped both JPY and JGB sentiment.

- Our policy team also noted - Takaichi, whose coalition secured a two-thirds supermajority in Sunday’s general election, maintains that decisions on raising borrowing costs rest with the BOJ, despite her strong mandate to tackle the cost-of-living crisis.

- Softer US data outcomes, ahead of tonight's US NFP print, have also helped US-JP downside yield momentum. US yields have fallen sharply in recent sessions, so is a poor NFP print already priced in to some extent? Perhaps, but the longer term trends around US-JP yield differentials look skewed lower.

- Our FX technical team notes important support on the downside: 152.10 Low Jan 27 and the bear trigger.

Fig 1: Spot USD/JPY Versus Simple Fair Value Estimate

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Net Inflows Lagging SK/Taiwan Equity Gains, Mixed Trends Elsewhere

Despite South Korean and Taiwan equities mostly staying on the front foot, last Friday saw offshore selling, with South Korean outflows most notable (see the table below). It has been a volatile start to the year for South Korean net offshore flows, although we were net positive last week and for 2026 to date. For Taiwan though we remain at a net outflow for both of these metrics. Broader AI/chip related sentiment was boosted on Friday as TSMC posted solid Dec revenue (up 20% y/y). The company posts quarterly earnings this week. Both the Kospi and Taiex are tracking with positive biases of around 1% so far in Monday trade.

- Elsewhere, Indian net outflows were evident to start 2026. This fits with the weaker aggregate headline equity performance, with the NIFTY off around 2.65% last week.

- In South East Asia, Indonesia and Philippines have seen a positive start to offshore flow momentum for 2026. Philippines equities have performed strongly since the start of the year and track back around August levels from 2025 in early dealings today.

- Thailand net outflows are consistent with a flat SET index trend. Markets may be awaiting the election outcome in February for fresh direction, although this is still close to a month away (Feb 8).

Table 1: Asian Market Net Equity Flows

| Yesterday | Past 5 Trading Days | 2026 To Date | |

| South Korea (USDmn) | -1217 | 464 | 973 |

| Taiwan (USDmn) | -243 | -864 | -293 |

| India (USDmn)* | -413 | -466 | -803 |

| Indonesia (USDmn) | 15 | 121 | 185 |

| Thailand (USDmn) | -53 | -153 | -153 |

| Malaysia (USDmn) | 47 | 10 | -47 |

| Philippines (USDmn) | 5 | 36 | 44 |

| Total (USDmn) | -1858 | -851 | -95 |

| * Data Up To Jan 8 |

Source: Bloomberg Finance L.P./MNI

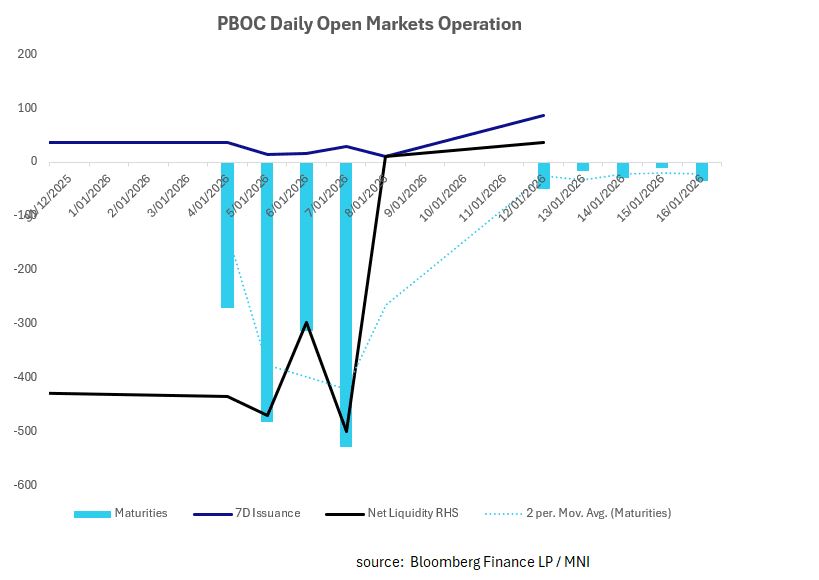

CHINA: Central Bank Injects CNY36.1bn via OMO

A modest injection to start the week as repo rates remain contained and the maturity schedule for the week ahead modest. There appears at this stage no major impacts from the significant liquidity withdrawal last week.

- The PBOC issued CNY86.1bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY50bn.

- Net liquidity injection CNY36.1bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.42%, from prior close of 1.47%.

- The China overnight interbank repo rate is at 1.27%, from the prior close of 1.28%.

- The China 7-day interbank repo rate is at 1.52%, from the prior close of 1.50%.

MNI: CHINA PBOC CONDUCTS CNY86.1 BLN VIA 7-DAY REVERSE REPO MON

- CHINA PBOC CONDUCTS CNY86.1 BLN VIA 7-DAY REVERSE REPO MON