ASIA STOCKS: Positive Bias Continues on JN / AI Optimism; Eyes on NFP

- Despite Japanese markets closed today, optimism from the PM's recent landslide victory continued to provide a supportive regional backdrop. The day’s primary driver was cooling U.S. retail sales. This raised expectations for Federal Reserve rate cuts later this year, boosting risk appetite across the region. Markets look ahead tonight to non farm payrolls for further indications for rates with Trump talking up NFP prospects, whilst FED officials suggest rates are on hold for some time.

- China's CPI for January missed expectations whilst the PPI remained in contraction, though base effects were strong. While this underscored weak domestic demand, it also increased expectations for further stimulus from Beijing to hit its 2026 growth target. Moves in China's major bourses were muted today with HSI up +0.4% whilst CSI 300 was down -0.15%

- The KOSPI and TAIEX - both considered tech heavy - were higher today with the TAIEX up +1.6% on TSMC gains of +2.4% and the KOSPI up +1.2% despite a mixed day for AI stocks. Despite recent global volatility in tech valuations, Asian tech hubs like South Korea and Taiwan remain well supported by global investors with recent days seeing in a surge of inflows into Taiwan stocks.

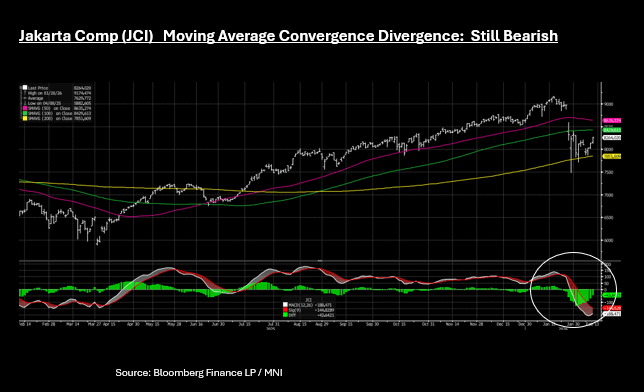

- The JCI has delivered three consecutive days of strong gains, up +1.6% today at 8,270; near to the upside resistance via the 100-day EMA at 8,359. Momentum indicators remain bearish for the JCI with the MACD line below the signal. A negative MACD value means the 12-day Exponential Moving Average (EMA) is significantly below the 26-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Slightly Cheaper After Stronger Than Expected HH Spend

ACGBs (YM -1.0 & XM -0.5) are slightly weaker after today’s household spending data.

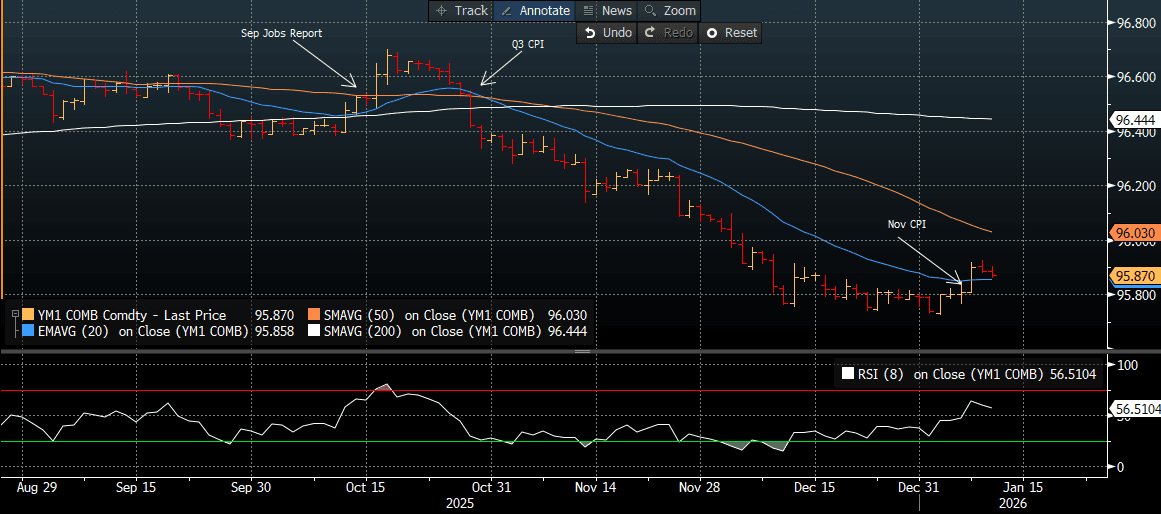

- MNI Techs: Prices bounced Thursday. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support (see chart).

- Earlier data showed stronger than expected Nov household spending figures. This series has replaced the retail sales print as the main monthly indicator for household spending trends in Australia.

- The spending data may add a little to the RBA hike case for 2026, although inflation data is likely to remain the key swing factor.

- Cash US tsys have traded in today’s Asia-Pac session due to Japan being out on holiday.

- Cash ACGBs are 1bp cheaper with the AU-US 10-year yield differential at +53bps.

- The bills strip is little changed.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 32% for February to 93% by June and 138% by December 2026.

- Tomorrow, the local calendar will see Westpac Consumer Confidence.

- The AOFM plans to sell A$300mn 4.75% 2054 bond on Tuesday, A$1bn 4.25% 2036 bond on Wednesday and A$700mn 3.25% 2029 bond on Friday.

Bloomberg Finance LP

FOREX: USD - BBDXY Slides Lower On FED Independence Concerns

The BBDXY has had a range today of 1208.84 - 1212.76 in the Asia-Pac session; it is currently trading around {BBDXY Index}. The USD was looking like it was reestablishing some upward momentum to start the year, but this morning's news of possible indictments on the FED have put a dent in that for now. This market's perception is that this is clear political pressure being brought to bear on the FED and so has worrying implications for its so-called independence. The USD has understandably had a knee-jerk lower in Asia, the question is if that move is enough considering what's at stake. On the day, I suspect rallies could remain heavy in the short-term as the market tries to work through what this means. First support is back between 1205-1207, the USD has lacked any clear direction for at least 6 months now and the wider 1185-1230 range looks set to continue for now. This lack of a trend is being reflected in the CFTC data which shows very little positioning in the USD to start the year.

- EUR/USD - Asian range 1.1622-1.1671, Asia is currently trading {EURUSD Curncy}. The pair has bounced nicely in early Asia as the USD reacts to the FED news. On the day look for sellers to reemerge in EUR/USD back toward the 1.1665-1.1695 area.

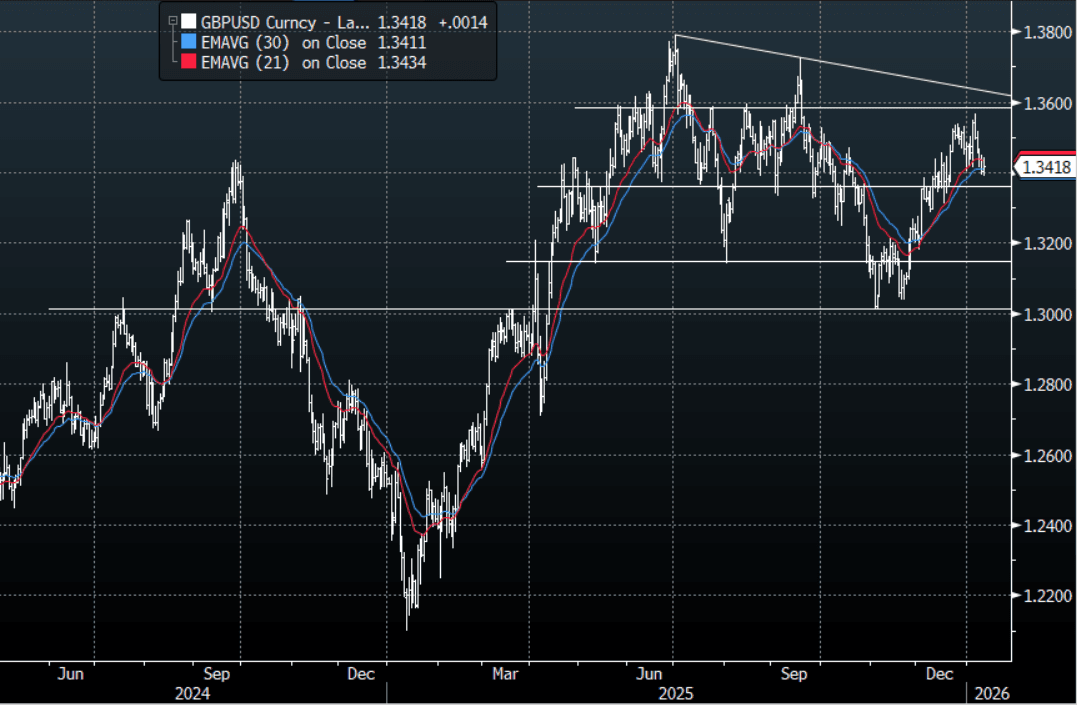

- GBP/USD - Asian range 1.3391-1.3441, Asia is currently dealing around {GBPUSD Curncy}. The pair had the look of potentially topping out above 1.3500 but it will be important to see how it reacts over the day to the USD headwinds. On the day, I am looking for a rally back toward the 1.3460-1.3490 to find sellers initially.

- Cross asset : SPX -0.55%, Gold $4570, BBDXY 1211, Crude Oil $59.15

- Data/Events : Germany Current Account Balance, EZ Sentix Investor Confidence

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Subdued Session With No Cash US Tsys

NZGBs closed a subdued session, with benchmark yields flat to 1bp richer.

- Cash US tsys have traded in today’s Asia-Pac session due to Japan being out on holiday.

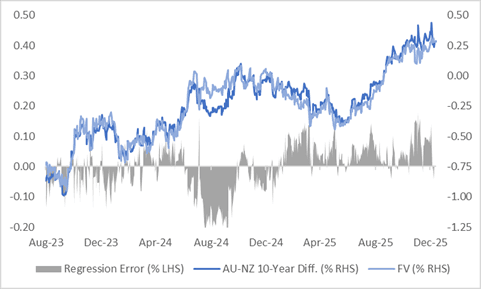

- The AU–NZ 10-year yield differential currently closed at +29bps, around 10bps below its recent peak of approximately +40bps, the widest since October 2020.

- The widening in the long-end spread has been mirrored by shifts in market expectations for the policy rate differential over the next year, as reflected in the AU–NZ 1-year forward 3-month swap (1Y3M) spread.

- Markets are presently pricing a further widening of the AU–NZ 3-month rate spread of around 10bps over the next 12 months.

- A simple regression analysis of the AU-NZ 10-year yield differential against the AU-NZ 1Y3M spread over the past two years shows that the 10-year differential is around fair value based on the regression model.

- Swap rates closed unchanged.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while October 2026 assigns 19bps.

- Tomorrow, the local calendar will see NZIER Business Opinion Survey data

- On Thursday, the NZ Treasury plans to sell NZ$250 Million 4.5% 2035 bond, NZ$200 Million 4.5% 2030 bond and NZ$25 Million 3.25% 2050 Linkers.

Figure 1: AU-NZ: 10-Year Yield Differential Vs. FV

Source: Bloomberg Finance LP / MNI