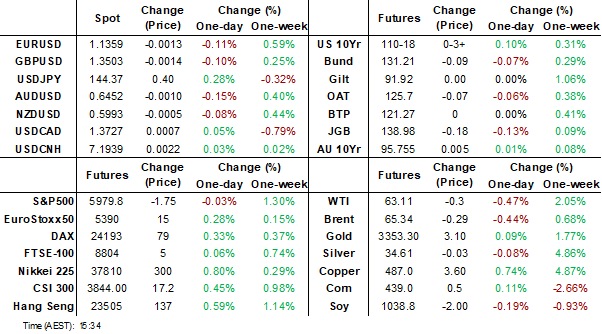

MNI EUROPEAN MARKETS ANALYSIS: AU GDP Soft, But Q2 May Improve

- South Korean markets have been in focus post the Presidential election result. The local Tsy curve is steeper, with yields up on fiscal stimulus hopes. Local equities have also surged, while FX has lagged somewhat.

- In Australia, Q1 GDP growth was below expectations, but a recovery in Q2 is possible. AUD/USD weakness post the print was short lived. RBA-dated OIS pricing is little changed across meetings.

- Later the Fed’s Cook & Bostic and ECB’s Machado appear. The BoC is expected to leave rates at 2.75%. US May services ISM/PMI, May ADP employment and May European services PMIs print. The focus remains on Friday’s US payrolls.

MARKETS

US TSYS: Asia Wrap - Yields In The Long-End A Little Lower

The TYU5 range has been 110-15 to 110-18+ during the Asia-Pacific session. It last changed hands at 110-17, up 0-02 from the previous close.

- The US 2-year yield is unchanged, dealing around 3.947%.

- The US 10-year yield has edged lower, trading around 4.446%, down 0.1 from its close.

- Jens Nordvig on X: “It is rare for the Fed to set rates at a level similar to nominal GDP growth. Normally, there is a large gap, with nominal policy rates well below nominal growth. The last times we were here were in the early 2000s and around 2006-2007. Something to think about.”(Graph Below)

- MNI US: Senate GOP Conference To Meet Weds To Discuss Accelerated Megabill Schedule: Laura Weiss at Punchbowl News reports on X that Senate Republicans will hold an all-conference meeting to discuss the 'One Big Beautiful' reconciliation bill on Wednesday afternoon.

- The 10-year yield continues to find good support around 4.35/40%. Yields need to hold above this area to continue to build for a move higher.

Data/Events: ADP, S&P Services PMI, ISM Services Index, Fed Beige Book

Fig 1: Fed Funds Effective rate vs Nominal GDP Growth

Source - Jens Nordvig/Bloomberg

JGBS: Bear-Steepener, Tomorrow's 30Y Supply In Focus

JGB futures are holding weaker, -16 compared to settlement levels, on a data-light local session.

- Bloomberg - "The 10-year auction earlier this week drew strong demand, but attention now shifts to Thursday's 30-year sale -- the true litmus test for investor appetite. Ultra-long bonds remain the market's weak point, and their performance will determine whether recent volatility persists."

- MNI POLICY: Bank of Japan officials will closely watch the upcoming June Tankan survey, due July 1, for signs of resilience in non-manufacturers' sentiment and upward revisions to major firms' capital investment plans, which would support its baseline view for a gradual rate-hike path, MNI understands.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest losses. Today’s US calendar will see ADP, S&P Services PMI, ISM Services Index and Fed Beige Book data.

- Cash JGBs are flat to 3bps cheaper across benchmarks, with a steeper curve. The benchmark 30-year yield is 1.1bps higher at 2.955% ahead of tomorrow’s supply.

- Swap rates are flat to 3bps higher.

- Tomorrow, the local calendar will see Cash Earnings and International Investment Flow data alongside 30-year supply.

AUSSIE BONDS: Flat Despite Weak Q1 GDP, Q2 GDP Bounce Back Likely

ACGBs (YM flat & XM +0.5) are little changed after today's Q1 GDP release.

- While Q1 GDP was weaker than expected and slower than Q4, it was impacted by extreme weather events in the quarter, which impacted exports and domestic demand. Thus, there is likely to be some positive payback in Q2 and so a reaction by the RBA to the weakness at its July 8 decision is not assured. Given special factors, it is likely to watch the monthly data closely for signs of a Q2 recovery.

- There was no progress on the productivity front in Q1, with GDP per hour worked posting its second consecutive unchanged quarter, leaving it down 0.9% y/y.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's modest losses.

- Cash ACGBs are flat with the AU-US 10-year yield differential at -19bps.

- The bills strip is little changed.

- RBA-dated OIS pricing is little changed across meetings. A 25bp rate cut in July is given an 83% probability, with a cumulative 79bps of easing priced by year-end.

- Tomorrow, the local calendar will see Trade Balance and Household Spending data.

- The AOFM plans to sell A$800mn of the 1.50% 21 June 2031 bond on Friday.

AUSTRALIA DATA: GDP Details Signal Gradual Recovery Still In Place

While Q1 GDP was weaker than expected and slower than Q4, it was impacted by extreme weather events in the quarter which impacted exports and domestic demand. Thus there is likely to be some positive payback in Q2 and so a reaction by the RBA to the weakness at its July 8 decision is not assured. Given special factors, it is likely to watch the more timely monthly data closely for signs of a Q2 recovery.

Australia GDP %

Source: MNI - Market News/ABS

- Real GDP rose 0.2% q/q in Q1 leaving annual growth stable at 1.3% but domestic demand slowed to 0.2% q/q & 1.9 y/y from 0.7% & 2.2%. Q4 GDP rose 0.6% q/q. The largest contribution was from household expenditure at 0.2pp, while exports detracted 0.2pp. Inventories added 0.1pp.

- The ABS noted that shipments of LNG and coal were particularly impacted by “severe weather disruptions to production and shipping”, which is likely to have rebounded over Q2. Weather impacted mining, tourism and shipping.

- Household spending rose 0.4% q/q to be up 0.7% y/y down from Q4’s 0.9% y/y. There was a pickup in the savings rate to 5.2% from 3.9% due to higher government income support and insurance claims in Queensland.

- Government consumption was flat with annual growth slowing to 3.4% y/y from 5.0% in Q4, but is also likely to rebound. There was less spending on electricity rebates and benefits but a pickup in defence. Investment by public corporations fell sharply but was still up 7.1% y/y.

- Private capex rose 0.7% q/q to be up 2.3% y/y driven by construction, while equipment contracted for a second straight quarter.

- Weak investment resulted in lower imports of capex goods which drove the 0.4% q/q decline in total imports which are now up only 0.4% y/y. The drop added 0.1pp to growth resulting in a net export detraction of 0.1pp.

Australia domestic demand y/y%

Source: MNI - Market News/ABS

AUSTRALIA DATA: Weak Productivity, Rising Compensation & ULC Above 5% y/y

There was no progress on the productivity front in Q1 with GDP per hour worked posting its second consecutive unchanged quarter leaving it down 0.9% y/y. A 0.2% q/q drop in Q2 is needed to reach the RBA’s May Q2 productivity forecast of -0.6% y/y, and so that remains possible but may be a little pessimistic. Unit labour costs growth rose again at 5.1% y/y up from 4.7% and the highest since Q2 2024.

Australia productivity vs ULC y/y%

Source: MNI - Market News/ABS

- Average compensation per employee rose 1.0% q/q, the second straight quarterly rise around 1% or above since Q3 2022. Annual growth picked up to 3.7% y/y from 3.5%. Q1 WPI inflation rose 0.2pp to 3.4% y/y. While wage growth is subdued it appears to be picking up and with weak productivity growth is not consistent with the RBA’s inflation target.

- Total employee compensation rose 1.5% q/q to be up 6.5% y/y in Q1, the highest in a year, after 2.0% & 6.0%.

- The current RBA GDP outlook and slower but steady hours worked doesn’t achieve sustained productivity growth of the historical average of 1%. If hours fall over the rest of 2025, then some solid growth can be realised above 2%.

- Unit labour cost growth would slow to around 2.5% y/y if hours worked continue to rise but if they fall then it will trough at around 0.5% y/y.

Australie average compensation per employee y/y%

Source: MNI - Market News/LSEG

BONDS: Closed Richer & On Best Levels, Outperforms $-Bloc

NZGBs closed at bests, with benchmark yields 5-6bps lower, on a data-light local session.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's modest losses. The 10-year yield continues to find good support around 4.35/40%. Today’s US calendar will see ADP, S&P Services PMI, ISM Services Index and Fed Beige Book data.

- The NZ–US 10-year yield differential closed 8 basis points tighter at +10bps, marking one of the tightest levels since February. For context, the spread was around +40bps in early April.

- Swap rates closed 4-7bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 3bps softer across meetings, with early 2026 leading. 6bps of easing is priced for July, with a cumulative 31bps by November 2025.

- Tomorrow, the local calendar will see Cotality Home Value, Volume of All Buildings and ANZ Commodity Price data alongside NZ Government 10-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$200mn of the 3.00% Apr-29 bond, NZ$200mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

FOREX: Asia FX Wrap - Quiet Session

The BBDXY has had a range of 1211.72 - 1214.14 in the Asia-Pac session, it is currently trading around 1214. "NATO is pushing European members to expand ground-based air-defense capabilities fivefold in response to the threat of Russian aggression, people familiar said. Trump will attend the alliance’s summit in The Hague later this month, the White House said.”(BBG)

- EUR/USD - Asian range 1.1366 - 1.1393, Asia is currently trading 1.1370. EUR has drifted sideways during the Asian session. Dips should continue to find support, the demand back towards 1.1200 proved to be solid last week.

- GBP/USD - Asian range 1.3513 - 1.3545, Asia is currently dealing around 1.3515. The GBP is attempting another run higher but is struggling to gain any momentum on a 1.3500 handle. Look for an opportunity to buy again back towards the 13300/3400 area if seen.

- USD/CNH - Asian range 7.1829 - 7.1944, the USD/CNY fix printed 7.1886. Asia is currently dealing around 7.1915. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.07%, Gold $3356, US 10-Year 4.44%, BBDXY 1214, Crude oil $63.13

Data/Events : Spain Industrial Production & Services PMI, Italy Serv PMI, France Serv PMI, Germ Serv PMI, EC Serv PMI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - Tries Lower On GDP Miss But Demand Found Again

The AUD/USD has had a range of 0.6454 - 0.6480 in the Asia- Pac session, it is currently trading around 0.6460. The AUD tried lower on the GDP missing lower, but the bids that were around overnight again provided support towards the 0.6450 area.

- AUSTRALIA DATA: GDP Details Signal Gradual Recovery Still In Place. While Q1 GDP was weaker than expected and slower than Q4, it was impacted by extreme weather events in the quarter which impacted exports and domestic demand. Thus there is likely to be some positive payback in Q2 and so a reaction by the RBA to the weakness at its July 8 decision is not assured. Given special factors, it is likely to watch the more timely monthly data closely for signs of a Q2 recovery..

- The AUD is basically back to where it started the day, we may have to wait for NFP on Friday to get some clearer direction.

- Price is back in the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate. The dips look to be well supported while above 0.6350.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6450(AUD625m), 0.6455(AUD449m). Upcoming Close Strikes : 0.6300(AUD 1.47b June 6)

AUD/JPY - Today's range 92.83 - 93.17, it is trading currently around 93.000. Range looks 92.00 - 94.00 for now, a sustained break sub 91.50/92.00 will bring focus back to towards the lows again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

JPY: Asia Wrap - Quiet session trading Around 144.00

The Asia-Pac USD/JPY range has been 144.28 - 143.67, Asia is currently trading around 144.15. USD/JPY had a brief spike going into the Japanese Fix but drifted back off that high for the rest of our session before finding a bid late on.

- Bloomberg - “"Japanese government bonds may find short-term support as authorities signal efforts to rein in volatility. A draft of the government's annual fiscal blueprint highlights the need to boost domestic holdings of JGBs to help cap rising yields, Bloomberg News reports. While the proposal lacks specifics, it underlines broader plans for fiscal consolidation and more stable issuance.”

- “The 10-year auction earlier this week drew strong demand, but attention now shifts to Thursday’s 30-year sale -- the true litmus test for investor appetite. Ultra-long bonds remain the market’s weak point, and their performance will determine whether recent volatility persists.”

- MNI POLICY: June Tankan To Offer BOJ View On Rate Hike Path. TOKYO - Bank of Japan officials will closely watch the upcoming June Tankan survey, due July 1, for signs of resilience in non-manufacturers' sentiment and upward revisions to major firms’ capital investment plans, which would support its baseline view for a gradual rate-hike path, MNI understands.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risks of pullbacks increase. Resistance around the 146.00 area held perfectly and the JPY bulls would be quite relieved as well as vindicated by the price action.

- A break below 142.00 in USD/JPY and all eyes will once again turn to the pivotal 140.00 area. Sellers should emerge on this bounce back towards the 144.00/145.00 area for now. The market might have to wait for Friday’s NFP print to see if it can make another attempt lower.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.50($698m), 145.00($629m). Upcoming Close Strikes : 140.00($2b June 5), 142.00($1.17b June 5), 148.00($1.21b June 5).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

NZD: Asia Wrap - Quiet Session As NZD Tries To Hold 0.6000

The NZD/USD had a range of 0.5994 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6000. The NZD has found some demand just below the 0.6000 area as the US stock market pushed higher again overnight.

- Robin Brooks on X: “China was heading for deflation before US tariffs. Now goods pile up in ports and exporters struggle with rising inventories. Tariffs are inflationary for the US, but the big story is China, which will now tip into full-scale deflation. https://x.com/robin_j_brooks/status/1929784783195836689”

- The NZD held up ok with demand seen just below 0.6000, this while the USD continued to retrace higher overnight. NZD bulls will be hoping this demand holds in order to have another go at breaking above 0.6050. This might be a big ask though before we get NFP on Friday.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050 could provide the spark for the next leg higher.

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community pared back only a little of the decent short they had initiated the week before.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5900(NZD401m). Upcoming Close Strikes : 0.5990(NZD390m June 5), 0.5895(NZD305m June 5)

AUD/NZD range for the session has been 1.0752 - 1.0784, currently trading 1.0765. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ last week and AUD/NZD could now see supply on bounces. The sell zone is back towards 1.0800/25 with the first target being around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Major Bourses Up Strongly

The better than expected US labour market data dampened fears of an immediate economic downturn and gave stocks in Asia a boost today. This added to the election result in South Korea which is widely tipped to be good for stocks and growth with various policies to be implemented that are viewed as pro-stocks and an expected new stimulus package.

- The Hang Seng rose +0.72% today, the CSI 300 was up +0.52%, Shanghai up +0.43% and Shenzhen up +0.88%

- The KOSPI was closed yesterday and following the completion of the election, is up strongly today by +2.46%, it strongest single day gain for the year.

- The FTSE Malay KLCI's poor run continued and is down -0.06% for a seventh successive day of declines.

- After three days of declines, the Jakarta Composite bounced back today to rise +0.53%.

- The FTSE Straits Times in Singapore fell -0.13% and the PSEi in the Philippines was down -0.38%

- The NIFTY 50 is up modestly this morning by +0.15% after three successive days of falls.

ASIA STOCKS: Flows Continue to Reverse in Key markets

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows, with Taiwan, Indonesia and India the latest to experience a significant outflow.

- South Korea: Recorded inflows of +$172m the 2nd, bringing the 5-day total to +$265m. 2025 to date flows are -$11,205. The 5-day average is +$53m, the 20-day average is +$53m and the 100-day average of -$112m.

- Taiwan: Had outflows of -$351m as yesterday, with total outflows of -$3,109 m over the past 5 days. YTD flows are negative at -$13,128. The 5-day average is -$622m, the 20-day average of +$165m and the 100-day average of -$138m.

- India: Had outflows of -$246m as of the 2nd, with total outflows of -$383m over the past 5 days. YTD flows are negative -$10,774m. The 5-day average is -$77m, the 20-day average of +$58m and the 100-day average of -$114m.

- Indonesia: Had outflows of -$45m as of yesterday, with total outflows of -$126m over the prior five days. YTD flows are negative -$2,943m. The 5-day average is -$25m, the 20-day average +$6m and the 100-day average -$30m.

- Thailand: Recorded outflows of -$47m as of 29th, outflows totaling -$84m over the past 5 days. YTD flows are negative at -$1,755m. The 5-day average is -$17m, the 20-day average of -$2m and the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$29m as of yesterday, totaling -$254m over the past 5 days. YTD flows are negative at -$3,452m. The 5-day average is -$54m, the 20-day average of +$8m and the 100-day average of -$25m.

- Philippines: Saw inflows of +$3m yesterday, with net outflows of -$255m over the past 5 days. YTD flows are negative at -$512m. The 5-day average is -$51m, the 20-day average of -$13m the 100-day average of -$5m.

OIL: Canadian Reopening After Fires Drives Oil Lower, US Steel Tariffs Rise

Oil prices are lower after rising over 4% in the last two days as US 50% steel and aluminium tariffs come into effect. Rain is also helping to bring fires in Canada’s oil sands region under control. WTI is down 0.4% to $63.13/bbl, close to the intraday low, but still above the 5-day EMA at $62.47. Brent is 0.4% lower at $65.36/bbl, just above resistance at $65.28. The USD index is slightly higher.

- Fires shut down around 350kbd or 7% of Canadian output, according to Bloomberg, which is close to the 411kbd increase OPEC agreed last weekend. The development helped drive oil prices higher this week but one producer has now reopened production.

- As the US increases its import tariffs on steel and aluminium today, the OECD revised down its 2025 growth forecast by 0.2pp to 2.9% a slowdown from 2024’s 3.3%. Oil markets have been concerned about the impact on global energy demand from the increase in trade protectionism.

- Bloomberg reported that there was a crude destocking of 3.29mn barrels last week, according to people familiar with the API data. Product inventories rose strongly with gasoline up 4.73mn and distillate +761k barrels. The official EIA data is out today.

- Later the Fed’s Cook & Bostic and ECB’s Machado appear. The BoC is expected to leave rates at 2.75%. US May services ISM/PMI, May ADP employment and May European services PMIs print. The focus remains on Friday’s US payrolls.

Gold Off Intraday High, Increased US Steel Tariffs Introduced

Gold prices are slightly higher today as US 50% steel and aluminium tariffs come into effect. They fell 0.8% on Tuesday. It remains a safe haven asset as trade uncertainty continues. Bullion is 0.1% higher at $3355.7/oz after a high of $3372.67 which followed a low of $3346.57, trading between initial resistance and support. The USD index is up slightly.

- Trade negotiations with the US continue as the end of the 90-day reprieve on July 8 approaches but it remains unclear whether there will be an agreement with Europe and China before then. The OECD revised 2025 global growth down 0.2pp to 2.9% after 3.3% in 2024.

- Equities are generally higher with the Hang Seng up 0.7% and Kospi +2.4% but S&P e-mini down 0.1%. Oil prices are lower with WTI -0.5% to $63.12/bbl, copper is 0.9% higher and silver is down 0.1% to $34.48.

- Later the Fed’s Cook & Bostic and ECB’s Machado appear. The BoC is expected to leave rates at 2.75%. US May services ISM/PMI, May ADP employment and May European services PMIs print. The focus remains on Friday’s US payrolls.

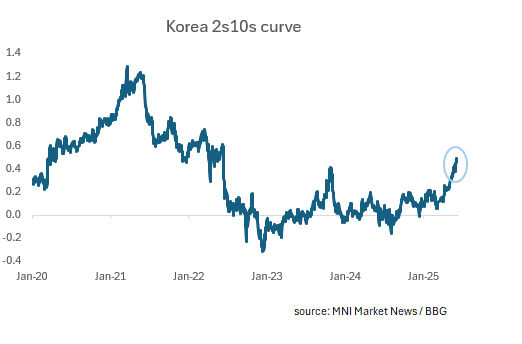

SOUTH KOREA: Could the Curve Steepen More from Here Part 2

- Last week we looked at the 2s10s curve in South Korea, comparing back to recent history and just prior to the May 29th BOK meeting where rates were cut.

https://www.mnimarkets.com/articles/could-the-curve-steepen-more-from-here-1748228269623

- We asked the question whether the curve could re-calibrate growth expectations for 2025, especially if Lee Jae-myung is elected on the promise of a further 'extra budget' to stimulate growth.

- A few headlines have crossed from new President Lee this morning as well: "*SKOREA LEE: TIME TO REVIVE PEOPLE'S LIVELIHOODS, RESTORE GROWTH" - BBG, "*S. KOREA'S LEE: WILL ACTIVATE EMERGENCY ECONOMIC TASK FORCE" - BBG

- These point to more fiscal stimulus coming down the pipe.

- As a recent example we looked at the experience of 2020 when the COVID impacted budget deficit reached -2.7% and GDP growth the following year touched 4.6%. The deficit for 2024 was -3.4% with a skew to the back end of the year. The 2025 budget forecast was originally for -1.8% and now is set to grow.

- Returning to 2020 the curve steepened to +83bps at year end with significant budget spend driving growth expectations.

- Last week the 10s2s was at +40bps and today stands at +49bps.

- Interestingly today’s 30-year auction drew the lowest bid-to-cover ratio since April 2022 at 2.12 times.

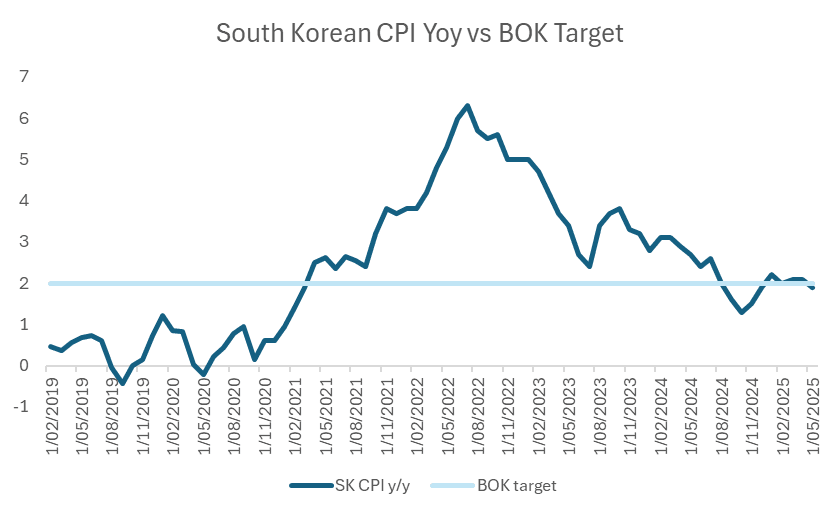

SOUTH KOREA: CPI Slides Further

- May's CPI declined further providing room for the BOK to cut rates again.

- The YoY CPI declined to +1.9%, from +2.1% in May

- The MoM figure declined to -0.01%, a decline from 0.1% in May

- The YoY figure represents the lowest print since March 2021, dipping below the BOK 2% target

- The MoM figure represents the lowest prints since November 2024

- The BOK next meets on July 10 and will be armed with not only the weaker CPI, but perhaps some formation of what the policies will look like from the new government - particularly around the further stimulus package of KRW35tn proposed during the election run up.

INDIA: Country Wrap: India Appeals to WTO on extra US tariffs

- India has approached the WTO over 25% additional US tariffs on auto parts, calling them unjust safeguard measures. With $6B in annual exports at stake, India seeks consultations, citing lack of WTO notification. The move follows US rejection of India's earlier steel and aluminium retaliation bid. (source Financial Express)

- Moody’s says Indian banks’ asset quality will remain stable despite global uncertainty, citing strong domestic growth, government spending, and RBI’s regulatory measures. Loans to grow 11–13% in FY26; secured retail loans to stay resilient, while unsecured loan stress may persist. (source Financial Express)

- The NIFTY 50 is up modestly this morning by +0.15% after three successive days of falls.

- The rupee was the worst regional performer today down -0.30% to 85.84

- Bonds are quiet in morning trade with the IGB 10yr at 6.25%

ASIA FX: Won Lags Equity Gains Post Election, Steady CNH & TWD Trends

In North East Asia FX markets, we saw early USD weakness give way to more stability as the Wednesday Asia Pac session has unfolded. There has been focus on the won, post Lee's Presidential election win, but greater focus has arguably been in the equity and bond space. USD/CNH dipped but is back above 7.1900 now. USD/TWD spot is holding just under 30.00, little changed for the session.

- Spot USD/KRW got to lows of 1371.3, but sits near 1375 in latest dealings, still around 0.30% stronger in won terms versus end Monday levels. Still, it has lagged the +2.5% gain for local stocks, as optimism grows new President Lee will be able to do more to boost domestic growth and corporate value. Offshore investors have bought $559.1mn of local stocks today. Bond yields are higher as well, particularly towards the back end of the curve. FX markets may be mindful of how trade talks will unfold from here, with new President Lee not in a rush to sign a deal.

- Spot USD/CNH tracked towards 7.1800 in the first part of trade, but sits back at 7.1915 in latest dealings. This is little changed on end Tuesday levels in the US. The USD/CNY fixing was little changed, while the fixing error returned to negative territory as the USD recovered from recent lows. Focus remains on whether Trump and Xi will speak, with the White House stating a call was likely soon between the two leaders.

- Spot USD/TWD is little changed, holding just under 30.00 in latest dealings.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/06/2025 | 0700/0900 | ** | Industrial Production | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 04/06/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/06/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/06/2025 | 1430/1030 | BOC press conference | ||

| 04/06/2025 | 1800/1400 | Fed Beige Book | ||

| 05/06/2025 | - | European Central Bank Meeting | ||

| 05/06/2025 | 2330/0830 | ** | average wages (p) | |

| 05/06/2025 | 0130/1130 | ** | Trade Balance | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/06/2025 | 0545/0745 | ** | Unemployment | |

| 05/06/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/06/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 05/06/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/06/2025 | 0745/0845 | BOE's Greene Opening Remarks at Econdat Conference 2025 | ||

| 05/06/2025 | 0800/1000 | * | Retail Sales | |

| 05/06/2025 | 0830/0930 | Decision Maker Panel data | ||

| 05/06/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/06/2025 | 0900/1100 | ** | PPI | |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference |