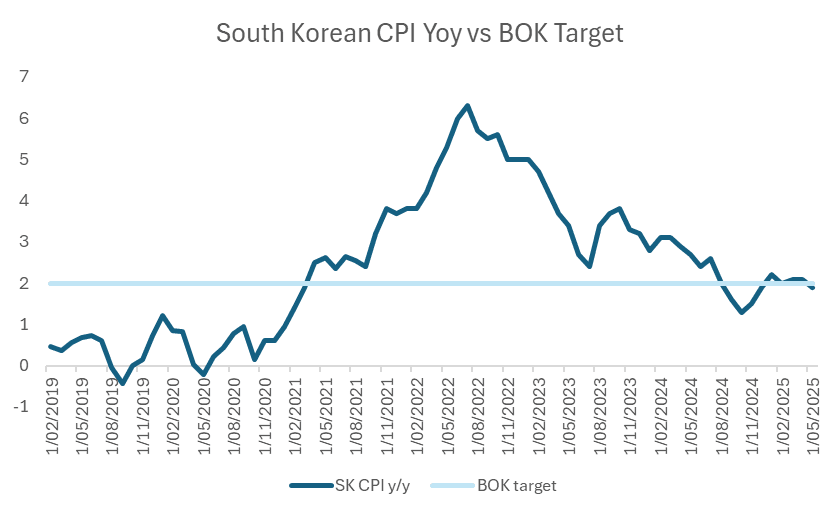

SOUTH KOREA: CPI Slides Further

Jun-03 23:10

- May's CPI declined further providing room for the BOK to cut rates again.

- The YoY CPI declined to +1.9%, from +2.1% in May

- The MoM figure declined to -0.01%, a decline from 0.1% in May

- The YoY figure represents the lowest print since March 2021, dipping below the BOK 2% target

- The MoM figure represents the lowest prints since November 2024

- The BOK next meets on July 10 and will be armed with not only the weaker CPI, but perhaps some formation of what the policies will look like from the new government - particularly around the further stimulus package of KRW35tn proposed during the election run up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Safe Haven Bid Diminishing from Gold for Now

May-04 23:04

- Gold had its worst week since late February as news of potential trade agreements gave markets a boost and pushed some equity bourses back above pre tariff announcement levels.

- Gold was down -2.39% for the week, and opens today in Asia at US$3,239.76.

- From the late April high of $3,423.98, gold is now down over 5% as a combination of profit taking and a redistribution back into equities dictates its fortunes.

- For the first time since early April, gold now sits on the 20-day EMA of $3,243.05. Any break below could see a move lower to the 50-day EMA of $3,119.98

BONDS: NZGBS: Cheaper With US Tsys After Stronger Than Expected US NFP

May-04 23:04

In local morning trade, NZGBs are 4bps cheaper after US tsys sold off on Friday following stronger-than-expected non-farm payrolls data.

- US tsys finished near session lows on Friday after trading richer at the open. Higher-than-expected nonfarm payrolls at 177k (sa, cons 138k), of which private contributed 167k (sa, cons 125k), triggered the early reversal. However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs. -48k two-month revision).

- US stocks are back near four-week highs—pre-"Liberation Day" levels—as optimism about a trade deal improved.

- The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump".

- Swap rates are 4-6bps higher with the 2s10s curve steeper.

- RBNZ dated OIS pricing is little changed across meetings. 26bps of easing is priced for May, with a cumulative 77bps by November 2025.

- Today, the local calendar will be empty.

AUSTRALIA: Little To Stand Out This Week, Household Spending Tuesday

May-04 22:53

There are number of monthly data releases this week but nothing in particular that stands out. The closest to a highlight will be Tuesday’s March household spending data, which is set to replace retail sales in the middle of the year.

- Bloomberg consensus expects that household spending will rise 0.2% m/m & 3.9% y/y in March after rising 0.2% m/m & 3.3% y/y. March retail sales rose 0.3% m/m but flat Q1 volumes disappointed.

- The Melbourne Institute’s April inflation gauge prints on Monday and it has been running close to the trimmed CPI in recent months. It was 2.8% in March.

- ANZ job ads for April are also on Monday. Q1 saw vacancies continuing to moderate but the ratio with unemployment remains above average.

- The final April S&P Global composite and services PMIs print on Monday. The preliminary reading is consistent with positive but moderate growth.

- March building approvals are released on Tuesday and forecast to fall 1.8% m/m after a 0.3% drop the previous month.

- There are no RBA events scheduled for the week. The next meeting is May 20.