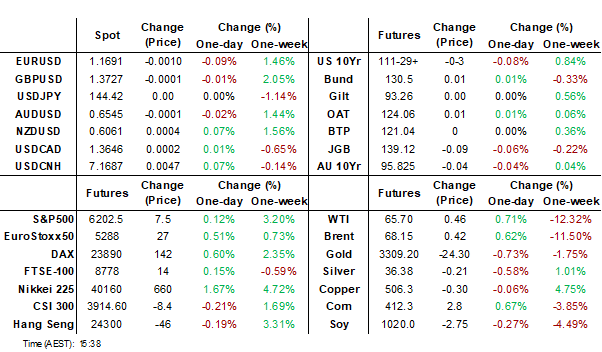

MNI EUROPEAN MARKET ANALYSIS: US/CHINA Trade Agreement Done

- US Commerce Secretary Lutnick says US China Trade Agreement signed

- Major Bourses Deliver Modest Gains for the week.

- USD Weakness Delivers Strong week for Asia FX.

- Oil Suffers Huge Falls for the week.

- Later France PPI, EU Consumer Confidence, US Personal Income & Consumption.

MARKETS

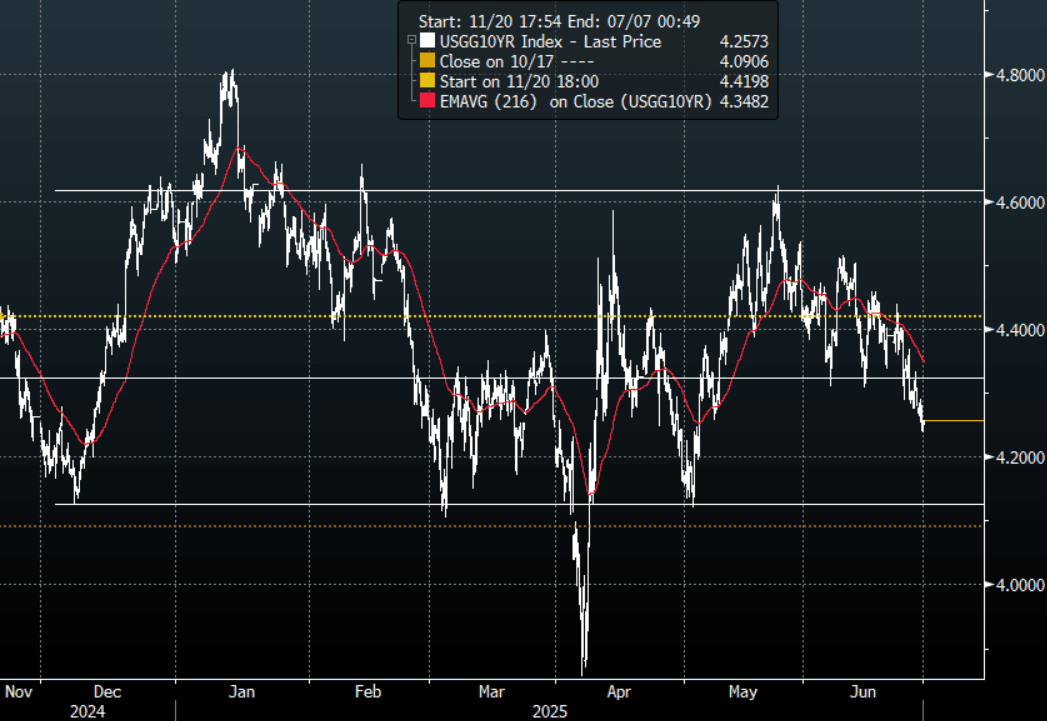

US TSYS: Asia Wrap - Yields Drift Higher, Led By The Front-End

The TYU5 range has been 111-29 to 112-02 during the Asia-Pacific session. It last changed hands at 111-30, down 0-02+ from the previous close.

- The US 2-year yield has moved higher trading around 3.74%, up 0.02 from its close.

- The US 10-year yield has edged higher trading around 4.255%, up 0.01 from its close.

- The 10-year yield has accelerated through its support, this should clear the way for a move lower with the 4.10% area the first target.

- 10-year yields should now find demand on any bounce back to the 4.35/40% area.

- Bloomberg - “Republican lawmakers will remove the Section 899 protective measure — or so-called revenge tax — from Trump’s bill after a request from Scott Bessent.”

- Guy LeBas on X: “(Section 899 removal)Worth more to the long end of the curve than the SLR relief proposal. Explains the persistent afternoon bid in USTs.”

- Data/Events:Personal Income, PCE, Core PCE, U. of Mich. Sentiment

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Little Changed, Subdued Session Despite Tokyo Core CPI Miss

JGB futures are weaker and at session lows, -11 compared to the settlement levels.

- Tokyo's core inflation slowed to 3.1% y/y in June from 3.6% in May, but remained above the Bank of Japan's 2% target for the eighth consecutive month. The core-core CPI, which excludes both fresh food and energy and is a key indicator of underlying inflation, also eased to 3.1% y/y in June from 3.3% in May, but stayed above 2% for the fourth straight month.

- (Bloomberg) - "Kato says that there were diverging opinions at the primary dealers' meeting regarding debt buybacks. He added that discussions have taken place about the potential impact of buybacks on the market. Govt not in a situation now where debt buybacks can be implemented, given the need to go through the budgetary process."

- (Bloomberg) -- Japan will take additional action to ease the impact of US tariffs on the auto sector as needed and “without hesitation,” its economy minister says.

- Cash US tsys are 1-2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's gains.

- Cash JGBs are mixed across benchmarks, with yield 2bps lower (40-year) to 1bp higher (10-year).

- Swap rates are little changed.

- On Monday, the local calendar will see Industrial Production and Housing Starts.

AUSSIE BONDS: Cheaper & At Cheaps On A Data-Light Session

ACGBs (YM -3.0 & XM -4.0) are weaker and at lows on a data-light day.

- Cash US tsys are 1-2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's gains. Today's US Calendar: Personal Income, PCE, Core PCE, U. of Mich. Sentiment.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at -11bp.

- The bills strip is slightly weaker, with pricing -1 to -2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 94% probability, with a cumulative 81bps of easing priced by year-end.

- On Monday, the local calendar will see Melbourne Institute Inflation and Private Sector Credit.

- Next week, the AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Wednesday and A$1000mn of the 2.25% 21 May 2028 bond on Friday.

- In 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2billion and $3 billion.

BONDS: NZGBS: Closed With A Bear Steepener As Short End Reverses Losses

NZGBs closed showing a modest bear-steepener, with benchmark yields flat to 3bps higher. Short end to medium term NZGBs did, however, manage to finish off the session’s worst levels (2bp cheaper).

- The NZ-US 10-year yield differential closed 4bps wider at +26bps.

- Cash US tsys are 1-2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's gains. Today's US Calendar: Personal Income, PCE, Core PCE, U. of Mich. Sentiment.

- Lending to all borrowers NZ$8.58b — most since November 2021, according to the RBNZ. Gains 24% y/y.

- Swap rates closed 1-2bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed flat to 1bp firmer across meetings. 4bps of easing is priced for July, with a cumulative 33bps by November 2025.

- Interest rate expectations across dollar-bloc economies softened over the past week, led by an 18bp decline in the US. New Zealand followed with an 11bp drop, while Canada and Australia each saw a 7–8bp easing.

- On Monday, the local calendar will see Filled Jobs and ANZ Business Confidence.

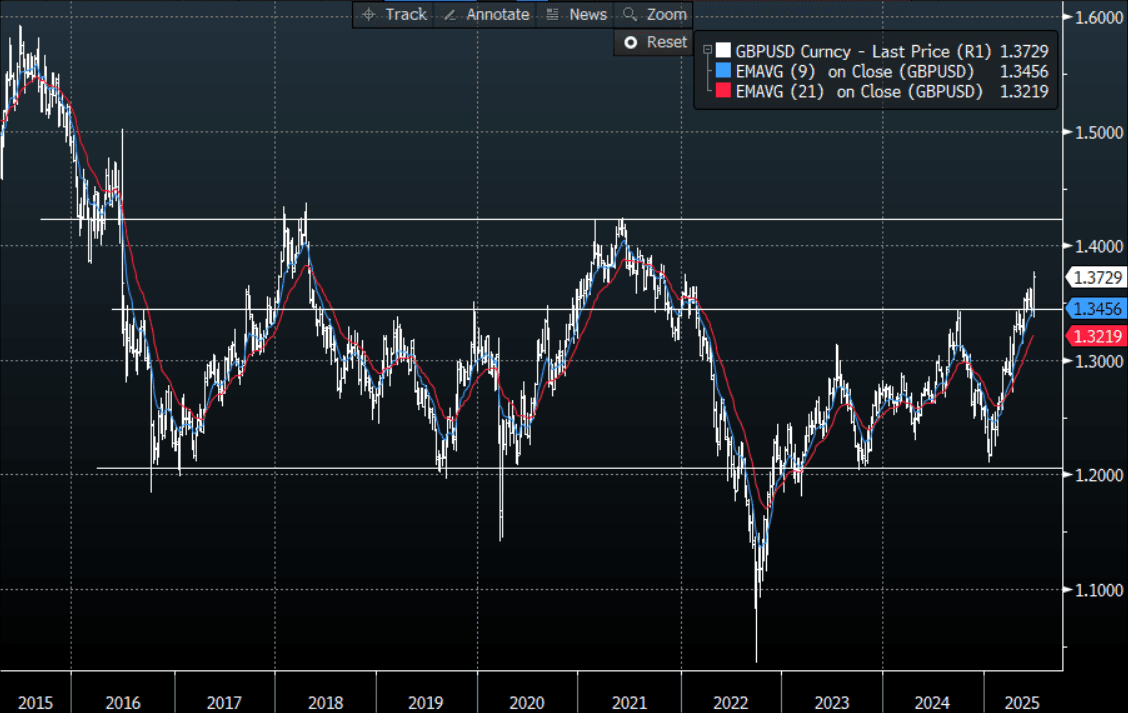

FOREX: Asia FX Wrap - The USD Sell-Off Takes A Breather In The Asian Session

The BBDXY has had a range of 1193.62 - 1195.64 in the Asia-Pac session, it is currently trading around 1194. A very quiet trading range in Asia today. With the market now looking for more US rate cuts, an already bearish outlook for the USD has seen the move lower gather pace overnight. The move sub 1200 is potentially signalling the start of a deeper move back to 1150 and beyond. “FX traders are focusing on call options in the 1.20-to-1.25 area, along with higher implied volatility. That’s a clear signal that fresh funds are piling into bullish euro strategies.”(BBG). “KASHKARI: WOULDN'T BET AGAINST DOLLAR AS PREEMINENT CURRENCY.”(BBG)

- EUR/USD - Asian range 1.1681 - 1.1710, Asia is currently trading 1.1695. While the USD remains on the back foot the EUR will continue to be supported first support back towards 1.1500. This move seems to be accelerating and will now be looking towards 1.2000 and beyond.

- GBP/USD - Asian range 1.3717 - 1.3750, Asia is currently dealing around 1.3735.This move higher now looks to have broken convincingly higher and with the USD looking like it is set for another leg lower Cable could now target levels back towards 1.4200.

- USD/CNH - Asian range 7.1618 - 7.1717, the USD/CNY fix printed 7.1627. Asia is currently dealing around 7.1685. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.2%, Gold $3355, US 10-Year 4.385%, BBDXY 1207, Crude oil $65.67

- Data/Events : Spain GDP & PPI, France Consumer Confidence

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

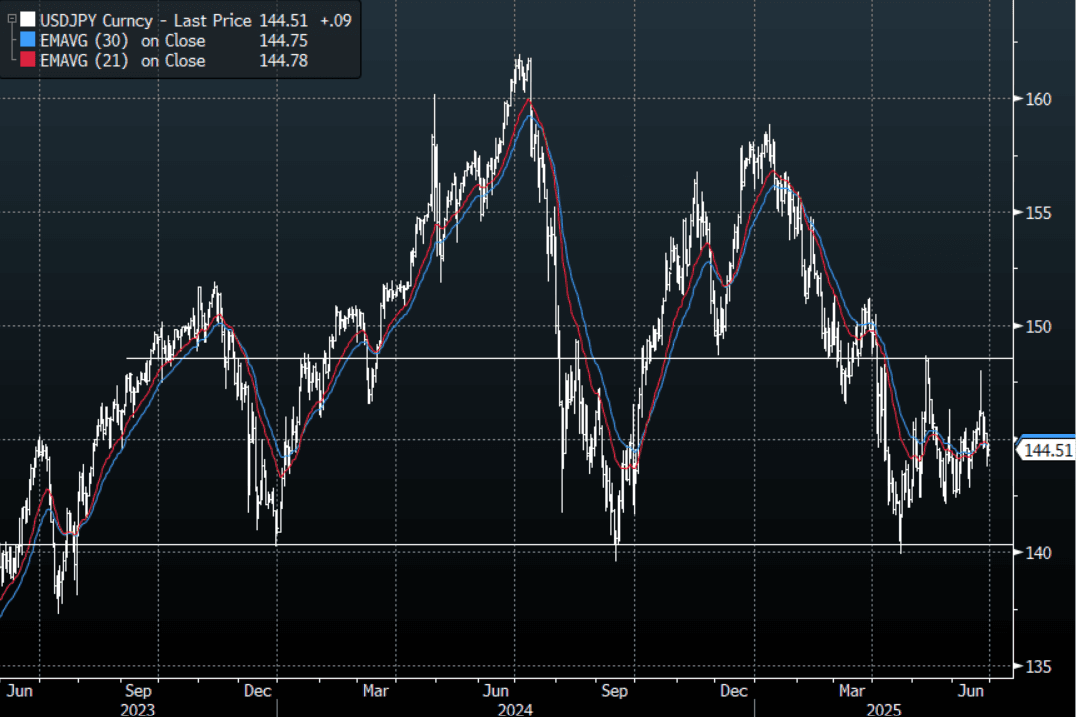

JPY: Asia Wrap - USD/JPY Back In The Middle Of Its Range

The Asia-Pac USD/JPY range has been 144.20 - 144.81, Asia is currently trading around 144.55, +0.1%. USD/JPY has been directionless in our session, drifting back into the middle of its wider 142.00 - 148.00 range. Surprisingly the removal of the section 899 or so called revenge tax from Trump’s bill has had little impact so far on the USD or US Yields.

- (Bloomberg) - “Kato says that there were diverging opinions at the primary dealers’ meeting regarding debt buybacks. He added that discussions have taken place about the potential impact of buybacks on the market. Govt not in a situation now where debt buybacks can be implemented, given the need to go through the budgetary process”

- “Japan has been monitoring developments surrounding the US Section 899 “revenge tax”. Kato says there’s a need to seek US understanding regarding the OECD’s global corporate tax framework.”

- JAPAN DATA - Tokyo's core inflation slowed to 3.1% y/y in June from 3.6% in May, but remained above the Bank of Japan's 2% target for the eighth consecutive month. The deceleration was mainly driven by a smaller rise in crude oil prices (+3.6% vs. +8.7% in May), though this was partially offset by higher prices for non-perishable food (+7.2% vs. +6.9%) and household durable goods (+3.3% vs. +2.7%)

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY is looking for a fresh catalyst in the middle of its range, while the USD continues to move lower this should see sellers on any bounce for now.

- Price now back in its wider 142.00 - 148.00 range, I am not sure that the brief spike higher would have seen positioning altered too much and the long JPY trade remains alive and well.

- Options : Close significant option expiries for NY cut, based on DTCC data: 143.05($600m).Upcoming Close Strikes : 143.85($885m June 30), 145.00($923m July 1)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

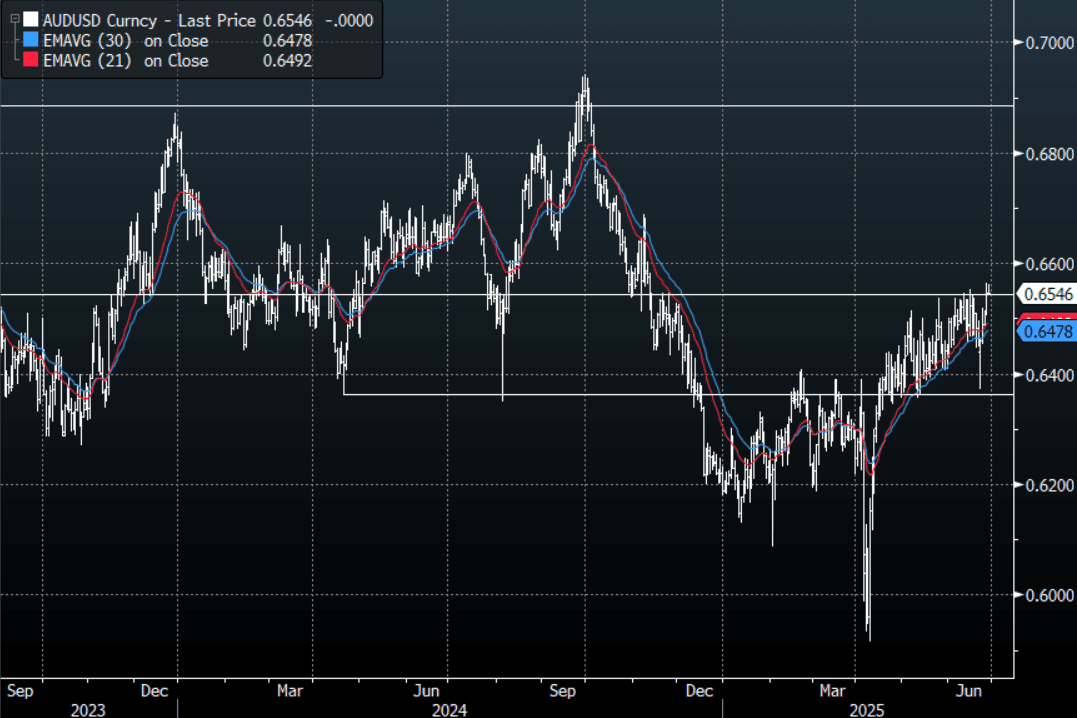

AUD: Asia Wrap - Quiet Session

The AUD/USD has had a range of 0.6543 - 0.6561 in the Asia- Pac session, it is currently trading around 0.6545. A tight range in a very quiet Asian session, the announcement that a trade deal has been finalised with China and that the section 899 or so called revenge tax was removed from Trump’s bill has had little impact so far. The USD has broken some key levels and is still looking vulnerable, this could see the AUD/USD continue to probe above 0.6550 looking to gain some momentum to ultimately break higher. CFTC data showed that both Asset managers and Leverage Funds remain short the AUD, this would potentially be pared back should the move higher accelerate.

- Bloomberg - “The US and China finalized a trade understanding reached last month in Geneva, Howard Lutnick said, adding that the White House has imminent plans to reach agreements with a set of 10 major trading partners. The US will ease China trade limits after receiving rare earths.”

- “Republican lawmakers will remove the Section 899 protective measure — or so-called revenge tax — from Trump’s bill after a request from Scott Bessent.”(BBG)

- The AUD/USD is attempting to break through the top of its recent range as the pressure on the USD increases.

- The AUD needs a sustained break above 0.6550/0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn towards the 0.6900/0.7000 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD526m), 0.6500(AUD 480m), 0.6570(AUD 350m). Upcoming Close Strikes : 0.67500(AUD1.27b July 2).

- AUD/JPY - Today's range 94.45 - 94.85, it is trading currently around 94.55. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

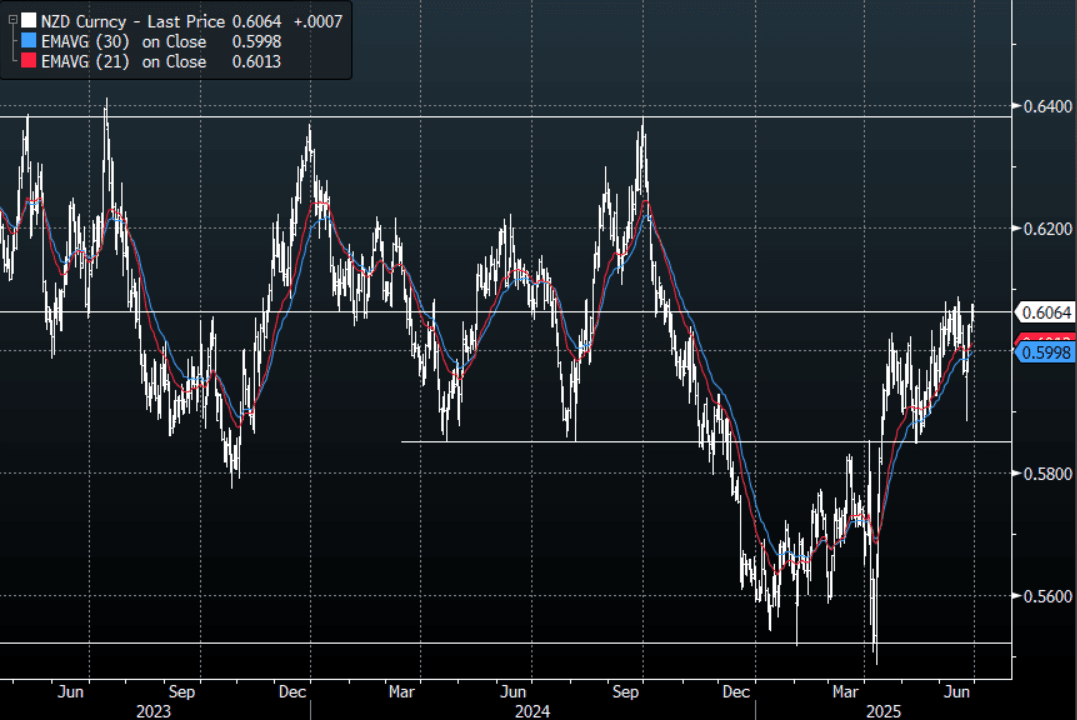

NZD: Asia Wrap - NZD/USD Consolidating Gains, Eyes 0.6100

The NZD/USD had a range of 0.6046 - 0.6076 in the Asia-Pac session, going into the London open trading around 0.6065, +0.12%. A tight range in a very quiet Asian session, the announcement that a trade deal has been finalised with China and that the section 899 or so called revenge tax was removed from Trump’s bill has had little impact so far. The USD has broken some key levels and is still looking vulnerable, this could see the NZD/USD continue to probe the 0.6100 area looking to gain the momentum to ultimately break higher.

- (Bloomberg) - “RBNZ publishes new residential mortgage lending data for May, on website. Lending to all borrowers NZ$8.58b — most since November 2021, Gains 24% y/y, Increases 1.4% m/m after seasonal adjustment.”

- “NZ JUNE CONSUMER CONFIDENCE RISES 6.4% M/M, NZ JUNE CONSUMER CONFIDENCE INDEX RISES TO 98.8: ANZ”(BBG)

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD404m July 1)

- AUD/NZD range for the session has been 1.0791 - 1.0815, currently trading 1.0795. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Key Bourses Deliver Strong Weekly Gains

Following the simmering of tensions in the Iran-Israel conflict, several key bourses in Asia are on track to deliver a positive week. As news circulates that a trade deal has been reached between the US and China coupled with renewed hope of cuts from the Federal Reserve, sentiment improved towards the end of the week and it will be interesting to see if it can extend into next week.

- China's Hang Seng did very little today yet is on track to finish the week up +3.3%. The CSI 300 was flat also yet remains up +2.5% for the week. The Shanghai Comp fell -0.20% but is up +2.4% for the week and the Shenzhen Comp is up +0.73% and over +4.6% for the week.

- In Taiwan, TAIEX is marginally softer but remains up +1.8% for the week buoyed by from strong inflows and a surging TWD.

- The KOSPI finished the week off with two consecutive days of near on -1% falls but is holding onto weekly gains of +0.94%

- The FTSE Straits Times in Singapore is up +0.64% today and over 2% for the week whilst the PSEi in the Philippines jumped +1.13% today and is just shy of +1% for the week.

- The NIFTY 50 has opened flat in morning trade having delivered a +1.2% gain yesterday. For the week currently it is up +1.7% for the week.

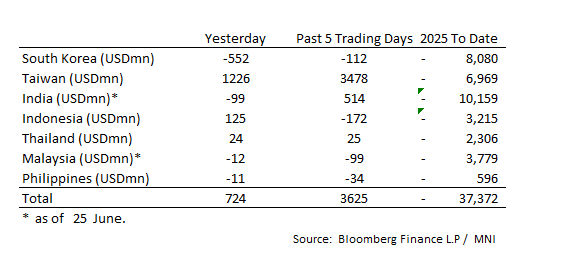

ASIA STOCKS: Taiwan Enjoys Huge In Flows

Taiwan has had three consecutive days of huge inflows nearing $4bn

- South Korea: Recorded outflows of -$552m yesterday, bringing the 5-day total to -$112m. 2025 to date flows are -$8,080. The 5-day average is -$22m, the 20-day average is +$172m and the 100-day average of -$76m.

- Taiwan: Had inflows of +$1,226m yesterday, with total inflows of +$3,478 m over the past 5 days. YTD flows are negative at -$6,969. The 5-day average is +$696m, the 20-day average of +$167m and the 100-day average of -$52m.

- India: Had outflows of -$99m as of the 25th, with total inflows of +$514m over the past 5 days. YTD flows are negative -$10,159m. The 5-day average is +$103m, the 20-day average of -$21m and the 100-day average of -$37m.

- Indonesia: Had inflows of +$125 yesterday, with total outflows of -$172m over the prior five days. YTD flows are negative -$3,215m. The 5-day average is -$34m, the 20-day average -$20m and the 100-day average -$30m.

- Thailand: Recorded inflows of +$24m yesterday, with inflows totaling +$25m over the past 5 days. YTD flows are negative at -$2,306m. The 5-day average is +$5m, the 20-day average of -$29m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$12m as of the 25th, totaling -$99m over the past 5 days. YTD flows are negative at -$3,779m. The 5-day average is -$18m, the 20-day average of -$27m and the 100-day average of -$22m.

- Philippines: Recorded outflows of -$11m yesterday, with net outflows of -$34m over the past 5 days. YTD flows are negative at -$596m. The 5-day average is -$7m, the 20-day average of -$17m the 100-day average of -$5m.

Oil Suffers Huge Falls for the Week

- Oil finished the US session up with minor gains overnight and carried that over into the Asian trading day.

- WTI opened at US$65.30 bbl and gained +0.61% to reach $65.63

- Despite gains for the last three days the huge falls on Monday and Tuesday sees WTI currently down over -12%

- Brent finished the US session with minor gains and that continued today, rising +0.50% to $68.10.

- For the week however Brent is down -11.60%

- CNN reports that the US has discussed the lifting of sanctions on Iran as a possible incentive to begin talks as an Iranian law comes into place to suspend cooperation with the UN Nuclear watchdog.

- Shell Plc (+0.50%) has no intention of making a takeover offer for BP Plc (+1.50%), refuting earlier reports of active merger talks between the two companies.

- Oil's attention for now may veer away from the Iran-Israel tensions and focus on a possibly announcement on a trade agreement between the US and China.

- Gold finished the US session modestly down and that weakness flowed over into the Asia trading day, with bullion down by just over 1%

- At US$3,291.42 gold sits fractionally above the 50-day EMA of $3,209.90 having traded through the 20-day EMA earlier

- For the week, gold has lost ground by -2.27% yet remains over 24% higher year to date

- The Shanghai Gold Exchange has expanded to Hong Kong with two new contracts and a bullion vault, broadening its international reach and strengthening China's influence in commodity and currency markets. The new contracts will be denominated in yuan and settled by cash or physical delivery, with the goal of promoting wider use of the yuan in international trade and reducing reliance on the US dollar.

- Calls to bring Germany’s gold home are growing, and now voices in Italy are urging that country’s government to do the same. Germany owns the second-largest gold reserves in the world at 3,352 tonnes. Italy ranks number three with 2,452 tonnes. Both countries utilize the New York Federal Reserve Bank, storing more than a third of their gold reserves in the bank’s Manhattan vaults. (source FX Street)

SOUTH KOREA: Country Wrap: Korea Could Issue More International Bonds

- South Korea is in talks with the US about raising its defense spending, a key demand of President Donald Trump as he calls on allies to ramp up their outlays on security and lessen the burden on the US. “Such discussions are ongoing between working-level officials. We need to decide how to respond,” National Security Adviser Wi Sung-lac told reporters late Thursday, indicating that progress in talks on trade would also support discussions on security. “It’s true the United States is currently making similar requests to several allies, similar to NATO.” (source BBG)

- The South Korean government may tap foreign debt markets again in the second half after pricing its largest-ever euro-denominated bond offering on Thursday, according to the nation’s finance ministry. The sovereign sold €1.4 billion ($1.6 billion) of notes in a two—part deal, its largest ever in euros, which attracted orders of about €19 billion, the Ministry of Economy and Finance said in a statement. (source BBG)

- The KOSPI finished the week off with two consecutive days of near on -1% falls but is holding onto weekly gains of +0.94%

- The Won lost ground today by -0.33% to 1,357.85 yet remains up for the week by +0.93%

- Bonds had a strong week with the KTB10YR -5bp lower for the week to 2.82%

CHINA: Country Wrap: Industrial Profits Turn Negative

- Signs of impact from tariffs were evident in the May China Industrial Profit numbers released today. China's companies saw profits drop year to date given tariffs and ongoing weakness in PPI. Industrial profits declined -9.1% YoY and the YTD number turned down to -1.1%. If the downturn is sustained it could lead to further policy intervention as the government program to subsidize equipment upgrades hasn't translated to profits. (source MNI)

- China's total nonfinancial outbound direct investment rose 2.3 percent year-on-year to $61.6 billion in the first five months, underscoring the nation's sustained efforts to deepen international cooperation, said the Ministry of Commerce on Thursday. In the meantime, the country's nonfinancial ODI in countries and regions involved in the Belt and Road Initiative reached $15.52 billion, surging 20.8 percent on a yearly basis, said He Yadong, a ministry spokesman. (source China Daily)

- China's Hang Seng did very little today yet is on track to finish the week up +3.3%. The CSI 300 was flat also yet remains up +2.5% for the week. The Shanghai Comp fell -0.20% but is up +2.4% for the week and the Shenzhen Comp is up +0.73% and over +4.6% for the week.

- Yuan Reference Rate at 7.1627 Per USD; Estimate 7.1744

- Bonds remain subdued with the CGB 10yr unchanged on the week at 1.64%

INDIA: Country Wrap: FTA Signed with the US

- US President Donald Trump on Thursday said that the United States has signed a trade agreement with China, and hinted that a “very big” trade deal could soon follow with India. (source MINT)

- The Indian economy will grow at a mostly steady pace this fiscal year and next after marking a four-year low in 2024-25, according to economists polled by Reuters, who have mostly either kept their forecasts unchanged or made marginal upgrades. That stable outlook comes despite the Reserve Bank of India cutting interest rates by a full percentage point since early this year, including an unexpected 50 basis point reduction on June 6, to boost growth in the face of rising global uncertainties. (source India Economic Times)

- The NIFTY 50 has opened flat in morning trade having delivered a +1.2% gain yesterday. For the week currently it is up +1.7% for the week.

- The Rupee is up today by +0.20% at 85.53 and has gained +1.2% for the week.

- Bonds have seen yields only marginally lower with the 10YR at 6.28% (-2bps for the week)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 27/06/2025 | 0600/0800 | ** | PPI | |

| 27/06/2025 | 0645/0845 | *** | HICP (p) | |

| 27/06/2025 | 0645/0845 | ** | PPI | |

| 27/06/2025 | 0645/0845 | ** | Consumer Spending | |

| 27/06/2025 | 0700/0900 | *** | HICP (p) | |

| 27/06/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 27/06/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 27/06/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/06/2025 | 1000/1200 | ** | PPI | |

| 27/06/2025 | 1130/0730 | New York Fed's John Williams | ||

| 27/06/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 27/06/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 27/06/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 27/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 27/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 27/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 27/06/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 27/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 27/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |