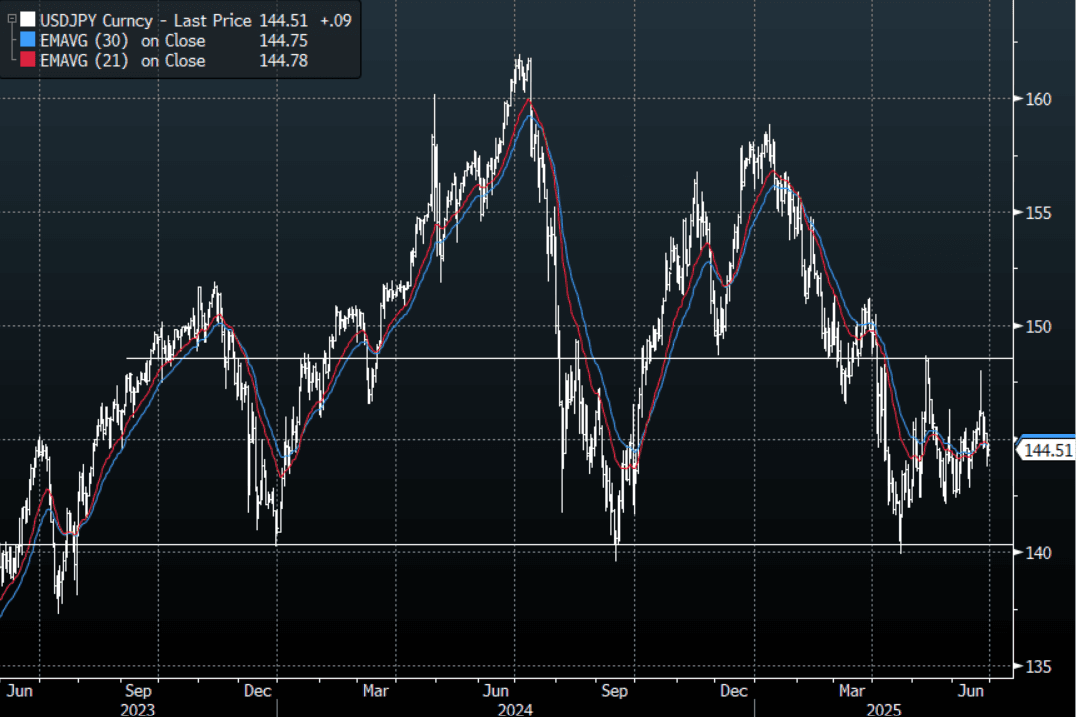

JPY: Asia Wrap - USD/JPY Back In The Middle Of Its Range

The Asia-Pac USD/JPY range has been 144.20 - 144.81, Asia is currently trading around 144.55, +0.1%. USD/JPY has been directionless in our session, drifting back into the middle of its wider 142.00 - 148.00 range. Surprisingly the removal of the section 899 or so called revenge tax from Trump’s bill has had little impact so far on the USD or US Yields.

- (Bloomberg) - “Kato says that there were diverging opinions at the primary dealers’ meeting regarding debt buybacks. He added that discussions have taken place about the potential impact of buybacks on the market. Govt not in a situation now where debt buybacks can be implemented, given the need to go through the budgetary process”

- “Japan has been monitoring developments surrounding the US Section 899 “revenge tax”. Kato says there’s a need to seek US understanding regarding the OECD’s global corporate tax framework.”

- JAPAN DATA - Tokyo's core inflation slowed to 3.1% y/y in June from 3.6% in May, but remained above the Bank of Japan's 2% target for the eighth consecutive month. The deceleration was mainly driven by a smaller rise in crude oil prices (+3.6% vs. +8.7% in May), though this was partially offset by higher prices for non-perishable food (+7.2% vs. +6.9%) and household durable goods (+3.3% vs. +2.7%)

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY is looking for a fresh catalyst in the middle of its range, while the USD continues to move lower this should see sellers on any bounce for now.

- Price now back in its wider 142.00 - 148.00 range, I am not sure that the brief spike higher would have seen positioning altered too much and the long JPY trade remains alive and well.

- Options : Close significant option expiries for NY cut, based on DTCC data: 143.05($600m).Upcoming Close Strikes : 143.85($885m June 30), 145.00($923m July 1)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia Wrap - AUD Stays Under Pressure

The AUD/USD has had a tight range of 0.6426 - 0.6454 in the Asia- Pac session, it is currently trading around 0.6430 drifting down back towards the days lows.

- April headline inflation was unchanged at 2.4% y/y, slightly higher than expected, while the trimmed mean picked up 0.1pp to 2.8% y/y. The focus is on the latter as headline is likely to be impacted by government electricity rebates until year end.

- We head into the corporate month-end and this could see more demand for USD’s over the next day or 2.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6325(AUD430m). Upcoming Close Strikes : 0.6400(AUD 556m June 2), 0.6500(AUD 532m May 30)

AUD/JPY - Today's range 92.75 - 93.23, it is trading currently around 93.00. The pair has again found supply above the 93.00 area in today's session, a break back above 93.50 could see the focus return once more to the 95/96 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

MNI EXCLUSIVE: MNI Discusses Potential For Deeper China, EU Ties

NEW ZEALAND: VIEW: Westpac Expects Unemployment Rate To Rise In 2025

Filled jobs fell 0.1% m/m in April signalling that employment remains subdued and Westpac notes that the trend is “flat to slightly downward”. It expects the unemployment rate to rise from Q1’s 5.1% this year even as the economy recovers since the labour market lags.

- Westpac observes that “here was a combined 0.3% downward revision to previous months”.

- Also, “the weekly snapshots provided by Stats NZ were notably softer in the second half of April. It’s possible that this was affected by the timing of public holidays – with Easter Monday and Anzac Day falling in the same week, many people will have taken the opportunity for an extended break. The snapshots in the next few weeks should reveal whether this was the case.”

- “Separately, we’ve seen that job advertisements remain at very low levels, indicating that businesses are still not back in hiring mode – some may still be finding themselves overstaffed, having held on to workers during the slowdown period.”

- “Construction and business services continue to see the biggest job losses, while public services (including health and education) are gradually rising. No other sectors are showing a clear trend one way or the other, aside from a lift in jobs in the relatively small mining sector.”