US TSYS: Asia Wrap - Yields Drift Higher, Led By The Front-End

The TYU5 range has been 111-29 to 112-02 during the Asia-Pacific session. It last changed hands at 111-30, down 0-02+ from the previous close.

- The US 2-year yield has moved higher trading around 3.74%, up 0.02 from its close.

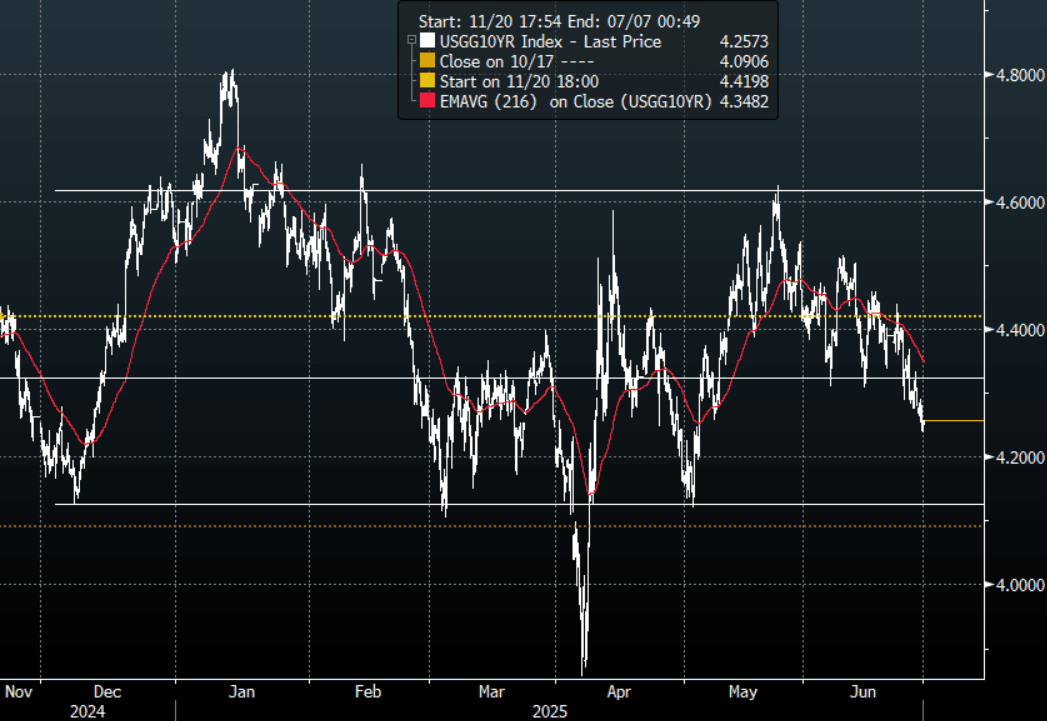

- The US 10-year yield has edged higher trading around 4.255%, up 0.01 from its close.

- The 10-year yield has accelerated through its support, this should clear the way for a move lower with the 4.10% area the first target.

- 10-year yields should now find demand on any bounce back to the 4.35/40% area.

- Bloomberg - “Republican lawmakers will remove the Section 899 protective measure — or so-called revenge tax — from Trump’s bill after a request from Scott Bessent.”

- Guy LeBas on X: “(Section 899 removal)Worth more to the long end of the curve than the SLR relief proposal. Explains the persistent afternoon bid in USTs.”

- Data/Events:Personal Income, PCE, Core PCE, U. of Mich. Sentiment

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: VIEW: Westpac Expects Unemployment Rate To Rise In 2025

Filled jobs fell 0.1% m/m in April signalling that employment remains subdued and Westpac notes that the trend is “flat to slightly downward”. It expects the unemployment rate to rise from Q1’s 5.1% this year even as the economy recovers since the labour market lags.

- Westpac observes that “here was a combined 0.3% downward revision to previous months”.

- Also, “the weekly snapshots provided by Stats NZ were notably softer in the second half of April. It’s possible that this was affected by the timing of public holidays – with Easter Monday and Anzac Day falling in the same week, many people will have taken the opportunity for an extended break. The snapshots in the next few weeks should reveal whether this was the case.”

- “Separately, we’ve seen that job advertisements remain at very low levels, indicating that businesses are still not back in hiring mode – some may still be finding themselves overstaffed, having held on to workers during the slowdown period.”

- “Construction and business services continue to see the biggest job losses, while public services (including health and education) are gradually rising. No other sectors are showing a clear trend one way or the other, aside from a lift in jobs in the relatively small mining sector.”

US TSYS: Asia Wrap - 2s10s Steepens

The TYM5 range has been 110-09 to 110-15 during the Asia-Pacific session. It last changed hands at 110-09, down 0-07 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.965%, down 0.02 from its close.

- The US 10-year yield has edged higher, dealing around 4.467%, up 0.02 from its close.

- This has seen the yield curve steepen in Asia - 2s10s +3.73 at 49.583.

- (Bloomberg) “The JGB 40-year sale has come in weak after all. The bid-to-cover dropped back to 2.21, the weakest since July. And the yield of 3.135% is above the poll estimate of 3.085%. That global bond bounce may fade.”

- “The Fed’s Tom Barkin said elevated uncertainty has led businesses to freeze hiring and hold off on future investment decisions. Neel Kashkari said there’s a “healthy debate” among policymakers about whether to look through the inflation effect of tariffs as a transitory shock, or a lasting issue.”(BBG)

- " FED'S WILLIAMS: WE HAVE TO BE VERY AWARE THAT INFLATION EXPECTATIONS COULD SHIFT IN ANY WAYS THAT COULD BE DETRIMENTAL - [RTRS]

- The 10-year look likely to see supply on any dips in yield in the short-term, should yields hold above 4.35/40% the target looks to be the 4.75% area. Watch for any announcements though relating to the SLR, this could have an impact on a market that is already quite short.

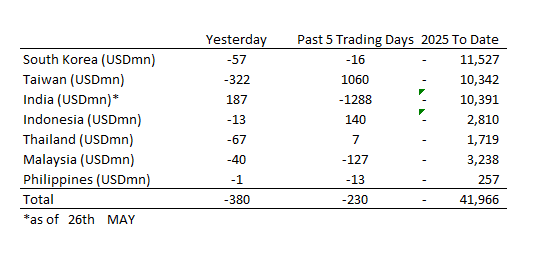

ASIA STOCKS: The Period of Big Inflows Appears to have Stalled

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows.

- South Korea: Recorded outflows of -$57m yesterday, bringing the 5-day total to -$16m. 2025 to date flows are -$11,527. The 5-day average is -$3m, the 20-day average is +$76m and the 100-day average of -$115m.

- Taiwan: Had outflows of -$322m as yesterday, with total inflows of +$1,060m over the past 5 days. YTD flows are negative at -$10,342. The 5-day average is +$212m, the 20-day average of +$414m and the 100-day average of -$115m.

- India: Had inflows of +$187m as of the 26th, with total outflows of -$1,288m over the past 5 days. YTD flows are negative -$10,391m. The 5-day average is -$258m, the 20-day average of +$153m and the 100-day average of -$115m.

- Indonesia: Had outflows of -$13m as of yesterday, with total inflows of +$140m over the prior five days. YTD flows are negative -$2,810m. The 5-day average is +$28m, the 20-day average +$13m and the 100-day average -$31m.

- Thailand: Recorded outflows of -$67m as of yesterday, inflows totaling +$7m over the past 5 days. YTD flows are negative at -$1,719m. The 5-day average is +$1m, the 20-day average of -$4m and the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$40m as of yesterday, totaling -$127m over the past 5 days. YTD flows are negative at -$3,238m. The 5-day average is -$28m, the 20-day average of +$27m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$1m yesterday, with net outflows of -$13m over the past 5 days. YTD flows are negative at -$257m. The 5-day average is -$3m, the 20-day average of +$2m the 100-day average of -$3m.