MNI ASIA OPEN:Trump's EU Trade Stance Hardens, Fed in Blackout

EXECUTIVE SUMMARY

- MNI TARIFFS: Trump Pushing For Minimum Tariff of 15-20% on EU - FT

- MNI US: Senate Likely To Take Up Second Major Crypto Bill In September - Sen. Scott

- Bloomberg: Japan Leader Ishiba Vows to Stay On Despite Election Setback

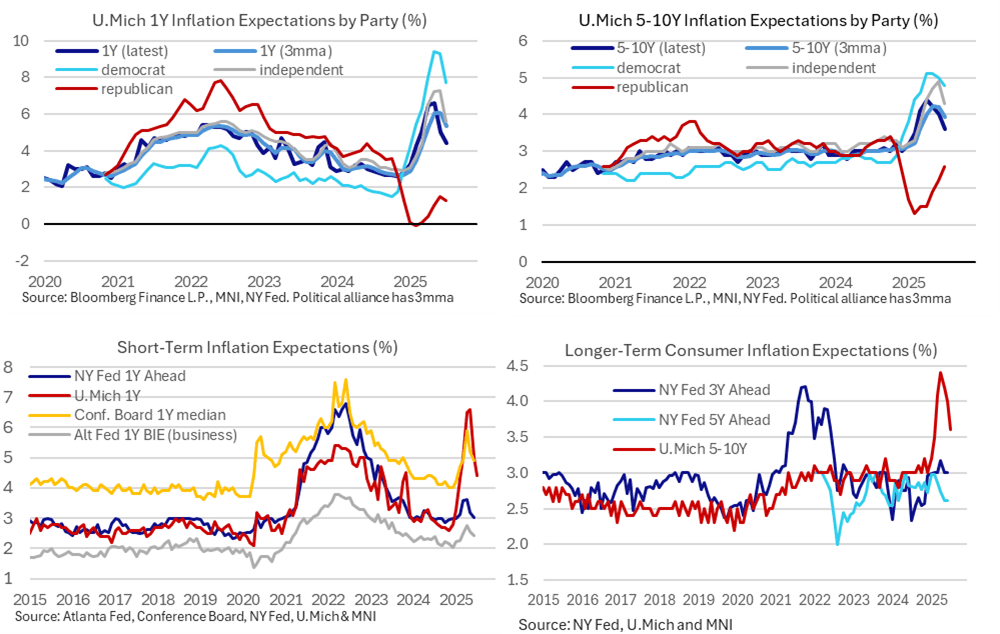

- MNI US DATA: Surprise Drop In U.Mich Inflation Expectations Faded

US

MNI TARIFFS: Trump Pushing For Minimum Tariff of 15-20% on EU - FT

Some snippets: "Donald Trump has escalated his demands in trade negotiations with the EU, pushing for a minimum tariff of 15 to 20 per cent in any deal with the bloc, according to three people briefed on the talks."

- "The US president’s hardened stance aims to test the EU’s pain threshold after weeks of talks on a framework agreement that would have maintained a baseline tariff of 10 per cent on most goods. People familiar with the negotiations say Trump has also been unmoved by the latest EU offer to reduce car tariffs, and would be happy to keep duties on the sector at 25 per cent as planned."

NEWS

Bloomberg: Japan Ruling Bloc Likely to Lose Upper House Majority, NHK Says

Bloomberg: Japan Leader Ishiba Vows to Stay On Despite Election Setback

Japanese Prime Minister Shigeru Ishiba said he intended to stay on even as his ruling coalition headed for a historic setback in an upper house election Sunday, an outcome likely to further unsettle markets.

MNI US: Trump Appointees' Involvement In Fed Renovation Degrades Case Against Powell

The Associated Press reports that appointees of President Donald Trump were involved in the planning process of the Federal Reserve headquarters renovation, which may have contributed to some of the cost overruns that Trump and OMB Director Russell Vought appear to be investigating as a potential 'just case' for dismissing Fed Chair Jerome Powell.

- AP: "The Fed’s architects said the central bank had wanted glass walls to reflect the Fed as a transparent institution, but three Trump appointees to a local commission felt marble best fit the building’s historic character. Marble was added as a result, according to the minutes of the Commission of Fine Arts, which advises the federal government on architecture."

MNI US: Senate Likely To Take Up Second Major Crypto Bill In September - Sen. Scott

Eleanor Mueller at Semafor reporting that Senate Banking Chair Tim Scott (R-SC) hopes to release a discussion draft of the Senate's version of the CLARITY Act next week. "We'll take that home for August, fight over it, make it better ... and then have a markup in September," Scott said.

MNI MIDEAST: Hamas Warn Of 'Long Battle' As Mediators Await Response To New Proposal

Reuters carrying comments from a spokesperson of Hamas’ armed wing, stating that the militant group is “ready for the long battle with Israel,” as ceasefire talks continue between Israel, Hamas, and intermediaries in Qatar. The spokesperson says that Hamas, “offered to all hostages in Gaza as part of a deal to end the war,” and warns that “if an agreement is not reached during current ceasefire talks, the group may not agree to an interim truce in future.”

US TSYS

MNI US TSYS: Tsys Near Steady on Week Heading Into Fed Backout

- Treasuries look to finish firmer - near steady for the week as rates bounce off the week's 4W lows Friday, light volumes (TYU5 under 920k) ahead of the weekend and the start of the Fed's media Blackout on policy (through July 31).

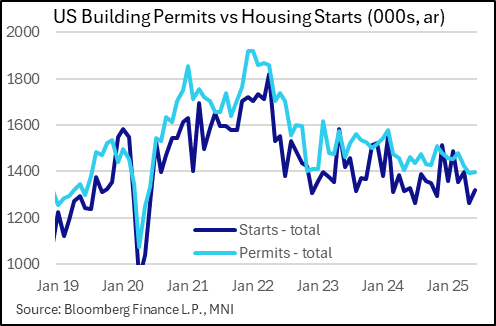

- Early data driven volatility: Treasuries pared support slightly after higher than expected Housing Starts & Build Permit data: starts came in at 1,321k (1,300k expected, 1,263k prior upwardly rev by 7k), with permits up 3k to 1,397k. Building permits remained below the 1,400k mark for a 2nd consecutive month.

- Treasuries extended highs briefly then pared move to pre-UofM release levels as UofM sentiment came out slightly higher while inflation expectations look lower. Inflation expectations surprise lower in the preliminary July survey, with the 1Y at 4.4% (cons 5.0 after 5.0 in June) and 5-10Y at 3.6% (cons 3.9 after 4.0 in June). The 1Y is the lowest since January and the 5-10Y is the lowest since February.

- Pres Trump signed landmark crypto bill into law Friday: GENUIS Act, a bill to create a regulatory framework for stablecoins.

- Sep'25 10Y contract trades +10 at 110-26.5 vs. -29 high. Initial resistance is at 110-30+, the 20-day EMA, followed by 111-13.5/111-28 (High Jul 10 / High Jul 3). Curves mildly steeper: 2s10s +0.761 at 55.030, 5s30s +2.221 at 103.902.

- Cross asset: Bbg US$ index well off lows: BBDXY -1.19 at 1206.39 (1202.46 Low); stocks mildly lower (SPX eminis -10 at 6330.75); gold up 9.7 at 3348.67.

OVERNIGHT DATA

MNI US DATA: Surprise Drop In U.Mich Inflation Expectations Faded

- The U.Mich consumer survey saw inflation expectations surprise lower in the preliminary July survey, with the 1Y at 4.4% (cons 5.0 after 5.0 in June) and 5-10Y at 3.6% (cons 3.9 after 4.0 in June). The 1Y is the lowest since January and the 5-10Y is the lowest since February. Markets have largely ignored the miss though, which we think aligns with some concerns over the signal from it.

- The breakdown by political leaning in particular shows some signs of further normalization after huge discrepancy around the initial imposition of tariffs, with democrats and independents’ expectations surging and republican expectations sliding.

- A reminder when looking at the charts below that the readings by political party are shown with a three-month average, although in the past there appears to have been some weight changes between months which can confuse when it comes to comparing with changes in the aggregate value.

- The U.Mich survey has generally seen a more pronounced spike in inflation expectations than its counterparts, with the year-ahead reading in the Conference Board survey coming closest to it.

MNI US DATA: Single-Family Housing Activity Continues To Deteriorate

Residential construction activity slightly surprised to the upside in June, with starts partially rebounding from a very weak May and permits unexpectedly increasing. Overall activity remains very weak, however. Starts came in at 1,321k (1,300k expected, 1,263k prior upwardly rev by 7k), with permits up 3k to 1,397k. Building permits remained below the 1,400k mark for a 2nd consecutive month for the first time since the pandemic, and are 2% below year-before levels.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 181.26 points (-0.41%) at 44303.5

S&P E-Mini Future down 10 points (-0.16%) at 6330.5

Nasdaq down 14.4 points (-0.1%) at 20871.58

US 10-Yr yield is down 2.4 bps at 4.4275%

US Sep 10-Yr futures are up 9.5/32 at 110-26

EURUSD up 0.0023 (0.2%) at 1.1619

USDJPY up 0.21 (0.14%) at 148.79

WTI Crude Oil (front-month) down $0 (0%) at $67.52

Gold is up $10.01 (0.3%) at $3348.78

European bourses closing levels:

EuroStoxx 50 down 17.92 points (-0.33%) at 5359.23

FTSE 100 up 19.48 points (0.22%) at 8992.12

German DAX down 81.42 points (-0.33%) at 24289.51

French CAC 40 up 0.67 points (0.01%) at 7822.67

US TREASURY FUTURES CLOSE

3M10Y -1.972, 8.668 (L: 7.138 / H: 10.007)

2Y10Y +0.516, 54.785 (L: 53.474 / H: 56.627)

2Y30Y +1.965, 111.823 (L: 108.672 / H: 113.711)

5Y30Y +2.221, 103.902 (L: 100.468 / H: 104.684)

Current futures levels:

Sep 2-Yr futures up 2.25/32 at 103-21.375 (L: 103-19.75 / H: 103-22.625)

Sep 5-Yr futures up 6.5/32 at 108-7.5 (L: 108-02.75 / H: 108-10)

Sep 10-Yr futures up 9/32 at 110-25.5 (L: 110-19 / H: 110-29)

Sep 30-Yr futures up 11/32 at 112-15 (L: 112-06 / H: 112-21)

Sep Ultra futures up 9/32 at 115-2 (L: 114-25 / H: 115-12)

MNI US 10YR FUTURE TECHS: (U5) Bear Threat Remains Present

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-13+/111-28 High Jul 10 / High Jul 3

- RES 1: 110-30+ 20-day EMA

- PRICE: 110-21+ @ 11:08 BST Jul 18

- SUP 1: 110-08+ Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures are trading above their recent highs but maintain a softer tone. An important support at 110-17, 61.8% of the May 22 - Jul 1 bull leg, has been breached. Note that price has also traded through a trendline support at 110-26. The line is drawn from the May 22 low. A continuation would open 110-03, the 76.4% retracement. Initial resistance is at 111-30+, the 20-day EMA.

SOFR FUTURES CLOSE

Sep 25 +0.025 at 95.835

Dec 25 +0.025 at 96.10

Mar 26 +0.030 at 96.355

Jun 26 +0.035 at 96.595

Red Pack (Sep 26-Jun 27) +0.040 to +0.050

Green Pack (Sep 27-Jun 28) +0.050 to +0.050

Blue Pack (Sep 28-Jun 29) +0.040 to +0.050

Gold Pack (Sep 29-Jun 30) +0.030 to +0.040

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (+0.00), volume: $2.743T

- Broad General Collateral Rate (BGCR): 4.33% (+0.00), volume: $1.140T

- Tri-Party General Collateral Rate (TCR): 4.33% (+0.00), volume: $1.110T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $113B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $273B

FED Reverse Repo Operation

RRP usage inches up to $199.298B this afternoon from $193.660B yesterday, total number of counterparties at 36. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Maintain Underperformance For The Week

European yields rose modestly Friday, with curve steepening seen in both EGBs and Gilts.

- There were few evident macro/headline catalysts, with yields weighed down early (with a pickup in energy prices and equities) and no subsequent recovery.

- For the third consecutive session, Gilt yields gapped higher at the cash open, and didn't deviate much through the session. 10Y yields saw the highest intraday yields since June 2 and highest close since May 28, with the curve twist steepening.

- Bund yields also picked up modestly in early trade but remained within Thursday's ranges for the rest of the session. The German curve bear steepened.

- Periphery EGBs erased a bit of early weakness to close very slightly tighter to Bunds.

- For the week, Gilts badly underperformed Bunds, partly on the back of more solid-than-expected labour market and CPI data.

- The UK curve bear steepened mildly on the week, with Bunds easily outperforming as German yields moved lower in parallel across the curve: UK 2Y yields +4.6bp / 10Y + 5.2bp; German 2Y yields -3.0bp / 10Y -3.0bp.

- Next week's main event is the ECB decision Thursday - with a rate hold expected, focus will be President Lagarde’s characterisation of risks at the press conference, which will likely shape the market reaction. Flash July PMIs and the ECB's Q2 Bank Lending Survey will also garner attention.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 1.87%, 5-Yr is up 1.1bps at 2.24%, 10-Yr is up 2bps at 2.695%, and 30-Yr is up 3.4bps at 3.232%.

- UK: The 2-Yr yield is down 0.3bps at 3.902%, 5-Yr is up 0.1bps at 4.089%, 10-Yr is up 1.9bps at 4.674%, and 30-Yr is up 2.9bps at 5.511%.

- Italian BTP spread down 0.4bps at 85.5bps / Spanish flat at 61.6bps

MNI FOREX: USDJPY Consolidates Weekly Advance Ahead of Japan UH Election

- Despite trading with a softer tone for much of Friday’s session, some late greenback strength has seen the USD index pare losses to remain just moderately lower on the session. Some late weakness for equities appears to have been behind the dollar reversal, but overall, currency markets have lacked conviction across the session.

- Scandinavian currencies remain at the top of the G10 leaderboard, while the likes of AUD (+0.40%) and NZD have remained resilient (+0.59%). In contrast, the Japanese yen is lower on Friday, as markets remain concerned regarding this week’s upper house election in Japan, and the potential fiscal ramifications ahead. GBP is unchanged having briefly flirted back above the significant trendline break this week. A short-term bear cycle in GBPUSD remains in place.

- Despite the softer USD index today, it has broadly consolidated a solid weekly advance of around 0.5% and fresh recovery highs this week underpin the more constructive short-term outlook. Both the Australian dollar and the Japanese yen have been particular laggards across the week, as domestic developments weigh.

- In Australia, a much weaker-than-expected jobs report has bolstered RBA easing bets, while the increased volatility surrounding the Trump-Powell spat has likely provided an additional headwind to higher beta currencies. AUDUSD support at the 50-day EMA, at 0.6490, was temporarily breached. A clear break of this EMA would highlight a stronger reversal and signal scope for an extension lower.

- In Japan, the ruling party is still projected to lose its majority in the upper house, and this has allowed USDJPY to reach fresh 3-month highs this week above 149.00. Above here, attention will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high. On the downside, initial support is seen at 146.92 (Jul 16 low), however key short-term support is located at 145.66, the 50-day EMA.

- On Monday, New Zealand Q2 CPI highlights the economic calendar.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 21/07/2025 | 0900/1100 | EZ Quarterly GDP Third Estimate | ||

| 21/07/2025 | 0900/1100 | Eurozone Q1 Deficit/Debt Data | ||

| 21/07/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/07/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 21/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 21/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill |