MNI ASIA OPEN: Trump To Make Iran Decision Within Two Weeks

EXECUTIVE SUMMARY

- Trump plans to decide within two weeks on whether to strike Iran - White House

- EU officials say US negotiations on the reciprocal tariff rate are becoming harder - Reuters

- The Norges Bank surprised with a 25bp cut - see MNI's post-decision interview with Governor Wolden Bache below

- No surprises from the SNB cutting 25bps or the BOE on hold, although the latter saw a dovish dissents surprise

- A geopolitics driven risk-off set the tone in thin trading ahead of early closes for rates and equity futures owing to the Juneteenth holiday in the US

- However, the Trump two-week window comments came after those closes, driving a 3% intraday drop in WTI August futures and the Bloomberg USD index easing 0.1% for back unchanged

NEWS

Middle East

MIDEAST (BBG): Trump Plans to Decide Within Two Weeks on Whether to Strike Iran

President Donald Trump will decide within two weeks whether to strike Iran, his spokeswoman said, as Israel hit more Iranian nuclear sites and warned its attacks may bring down the leadership in Tehran. White House spokeswoman Karoline Leavitt said Trump’s message on Thursday is that “based on the fact that there’s a substantial chance of negotiations that may or may not take place with Iran in the near future, I will make my decision whether or not to go within the next two weeks.”

MIDEAST (BBG): Israel’s War on Iran Intensifies as Trump Weighs Joining Attacks

[From before Trump's two-week window but for context on the escalation of strikes] Israel struck more of Iran’s nuclear sites and warned its attacks could bring down Tehran’s leadership as both sides await US President Donald Trump’s decision on whether to join the offensive on the Islamic Republic.

MIDEAST (CBS): Trump Sees Disabling Fordo Nuclear Site As "Necessary"

President Trump has been briefed on both the risks and the benefits of bombing Fordo, Iran's most secure nuclear site, and his mindset is that disabling it is necessary because of the risk of weapons being produced in a relatively short period of time, multiple sources told CBS News.

MIDEAST (RTRS/MNI): Iranian FM & US' Witkoff Have Held Direct Calls Since Escalation

Reuters reports "U.S. special envoy Steve Witkoff and Iranian Foreign Minister Abbas Araqchi have spoken by phone several times since Israel began its strikes on Iran last week, in a bid to find a diplomatic end to the crisis, three diplomats told Reuters." If the foreign minister's stance remains intact, this could limit the prospect of any return to talks, given that Israel appears committed to

eliminating Iran's nuclear enrichment capabilities, which would likely prove a protracted process

U.S./CHINA

US-CHINA (AFP): Trump Extends Deadline For TikTok Sale By 90 days

President Donald Trump announced Thursday he had given social media platform TikTok another 90 days to find a non-Chinese buyer or be banned in the United States.

US-CHINA (BBG): China to Cooperate With US on Drug Control, Illegal Immigrants

Chinese Minister of Public Security Wang Xiaohong meets with US ambassador David Perdue in Beijing, according to a report from Xinhua. China willing to cooperate with the US on drug control and deportation of illegal immigrants on basis of mutual trust

Europe

TARIFFS (RTRS): EU Officials Say Negotiations on Reciprocal Tariff Rate Becoming Harder

European officials are increasingly resigned to a 10% rate on "reciprocal" tariffs being the baseline in any trade deal between the United States and the European Union, five sources familiar with the negotiations said.

SPAIN (BBG): Spain Opposes Plan to Raise NATO’s Spending Target to 5%

Spain will oppose NATO plans to raise the target for members’ defense spending to 5% of GDP, potentially setting up a clash with US President Donald Trump, who wants Europe to spend more on its own security.

ITALY (RTRS/MNI): Continued Pessimistic Comments On EU Defence Spending Facilities

Reuters offers headlines echoing Italy's well-known pessimistic stance with respect to the EU defence spending proposals

Central Banks

BOE (MNI): Bank On Hold As MPC Splits Again

The Bank of England's Monetary Policy Committee kept interest rates unchanged at 4.25% at its June meeting, though more members than expected dissented, voting for a 25-basis-point cut. The MPC voted by six to three to keep rates on hold, with Deputy Governor Dave Ramsden -- often seen as an early mover among the Bank insiders - and external members Alan Taylor and Swati Dhingra dissenting. They pointed to lower wage growth, signs of subdued consumer demand, risks to global growth and a continuing disinflation process.

NORGES BANK (MNI): MNI Norges Bank Review: Jun '25 - Cut Against All Odds

Norges Bank surprisingly delivered a 25bp cut to 4.25%, going against analyst expectations and market pricing that were overwhelmingly in favour of a hold. Higher confidence in the inflation outlook was the key driver of the pivot, with some attention also given to gradually rising unemployment rates. The policy statement noted that "if the economy evolves broadly as currently projected, the policy rate will be reduced further in the course of 2025"

MNI INTERVIEW (MNI): Cut Surprise Just Timing Issue - Norges Governor

Norges Bank's 25-basis-point cut in its policy rate to 4.25% at its June meeting, which again caught markets off balance after its March hold, puts the Norwegian central bank back on track for gradual easing with the broader economic picture having remained steady for some time, Governor Ida Wolden Bache told MNI.

SNB (MNI): Cut To Zero As Trade Disputes Cloud Outlook

The Swiss National Bank cut its key policy rate by 25 basis points to 0% on Thursday, as inflationary pressures across the economy decreased compared to the previous quarter. "We took heightened downside risks into account with our interest rate cut in March - and these downside risks have since materialised," President Martin Schlegel said following the decision.

OVERNIGHT DATA

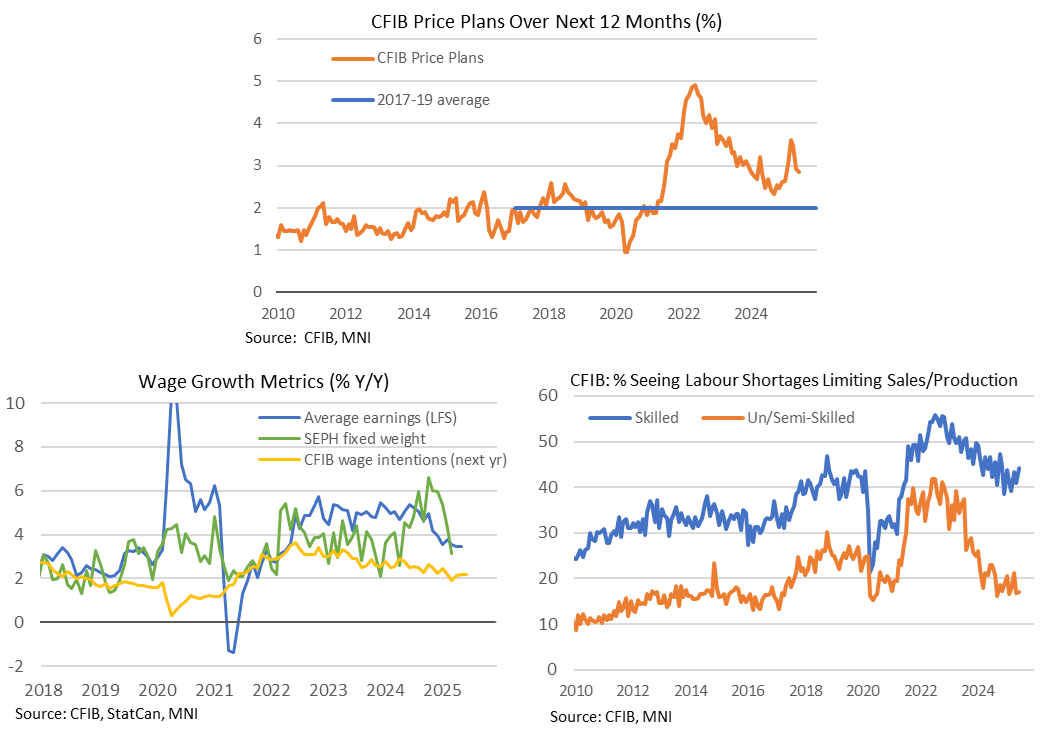

CANADA DATA: Small Business Optimism Improves, Price Plans Still On Higher Side

- CFIB small business confidence increased to 47.3 in June from 40.1 for a third monthly increase off historical lows of 25.5 in March seen on the threat of a US trade war.

- It’s still below the 50 level considered a balanced economic outlook, with the index generally in line with the BoC’s view that sentiment is low but not heading for a disaster scenario.

- Within the survey, expected average price increases over the next twelve months held steady at 2.9% (a touch lower unrounded at 2.85% after 2.91%).

- These expected price increases have pulled back from 3.46% in April and the recent high of 3.6% in March – highest since mid-2023 – but are above the 2.65% averaged in 2024 and more notably the 2.0% pre-pandemic.

- Wage growth intentions remain on the softer side meanwhile, holding at 2.2% for a second month and having also averaged 2.2% in the year to date. This is down from 2.6% averaged in 2024 and close to the 2.0% seen pre-pandemic.

- The report notes that "Full-time staffing plans remain muted with no real appetite for hiring". That's despite still high levels of those reporting skilled labour shortages are limiting sales or production, with 44% the highest since January.

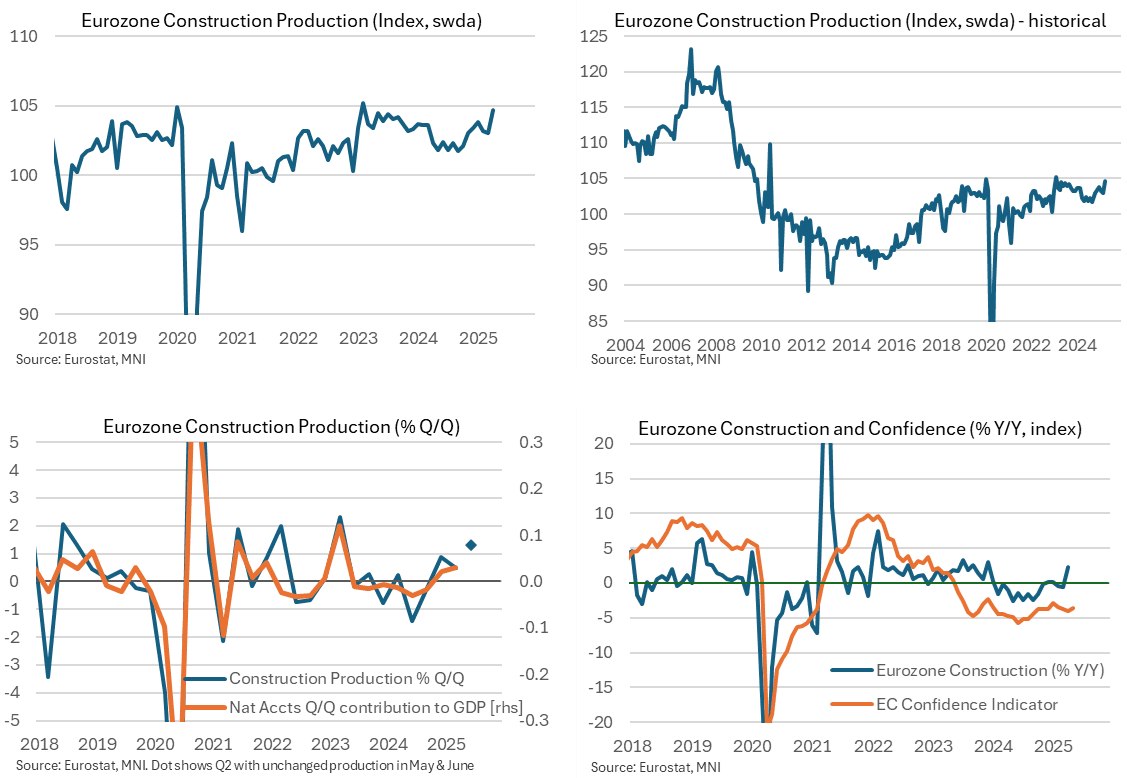

EUROZONE DATA: Construction Increases By Most Since Early 2023

Construction production saw an unusually strong increase in April, boding slightly better for Q2 GDP growth tracking, but it looks out of sorts with forward-looking indicators.

- Eurozone construction production increased a particularly strong 1.7% M/M in April (swda) for its strongest monthly increase since Feb 2023.

- It does however follow a -0.2% M/M in March (revised from 0.1%) and -0.6% M/M in February.

- The year-ago rate of 2.3% Y/Y (also swda) was its strongest since Dec 2023.

- Whilst we’d imagine some payback is likely in the months ahead, a crude assumption of two flat months in May and June would see construction rise 1.3% Q/Q non-annualised in Q2 after 0.5% in Q1.

- It’s promising as a sign of broader response to lower interest rates (the ECB had already cut a cumulative 150bp up to March with another 25bp in mid-April before a further 25bp earlier this month), but direct impact on GDP growth is limited.

- Construction added 0.03pps to real GDP growth in Q1 (non-annualised) with current tracking suggesting about double that for Q2.

- What’s more, improvements look unlikely to be sustained when looking at the EC confidence indicator.

MARKETS OVERVIEW

US TSYS: Mildly Firmer With Early Close In Shadow Of Trump Iran Deliberations

- Treasury futures dealt mildly firmer at the early close on Juneteenth day, with TUU5 at 103-21 3/8 (+ 00 7/8) and TYU5 at 110-28 (+ 03).

- TYU5 saw a session high of 110-31+ on continued geopolitical escalation fears captured by WTI +2.9% and ESM5 -0.9% [with a caution that WTI has since slipped 3%, with equity futures closed].

- It remained within yesterday’s range which included a snap 111-08 on the FOMC decision and dot plot. Resistance is seen at 111-13 (Jun 13 high) and 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg) whilst support is seen at 110-10+ (Jun 16 low).

- Trump is still to decide on striking Iran - CBS reports he deems it “necessary” to disable the Fordow nuclear site.

- Volumes have been unsurprisingly extremely thin, only just above 250k for TY.

- In rates space, SOFR futures ranged from flat to 3 ticks firmer in 2027 contracts, retracing part of yesterday’s steepening on the FOMC dot plot and Powell’s presser (SFRZ5/Z6 -0.625 vs -0.65 pre Fed and an overnight high of -0.59).

- The terminal SOFR yield of 3.25% (SFRH7) continues to imply a little over 100bp of cuts for the rest of the cycle.

- As for the near-term path, Fed Funds futures still point to a next cut coming in October with a cumulative 30.5bp priced. The 48bp cumulative to year-end is close to the more dovish than most expected 50bp indicated in the dot plot.

- Attention will likely continue to be firmly on Trump’s Iran deliberations. Tomorrow meanwhile sees a thin docket headlined by the Philly Fed manufacturing survey for June and with no Fedspeak scheduled for the first day of the FOMC blackout lifted.

FOREX: AUD and NZD Weakest in G10 as Bullish USD Index Signal Developing

- The USD index switched back to unchanged on the day on Trump headlines having been furtively firmer on Thursday.

- It had edged to new weekly highs as renewed geopolitical risks permeate on the building expectation that US officials are preparing for a possible strike on Iran "in the coming days" - a move that could prompt retaliation against US assets in the region.

- What's notable about this greenback recovery is that it's triggered a bullish signal for the DXY via a break and possible close above the downtrendline drawn off the early February high. This trendline has helped define the dollar weakness across Trump's administration, and this week's move raises the risk of a correction higher in the near-term.

- Today’s dollar strength is most notable against antipodean fx which have declined close to 1% on the session, reflective of weaker equity benchmarks and NZDUSD in particular was helped by a break below a cluster of daily lows around the 0.6000 mark. 50-day EMA support is seen just below 0.5950, before the May lows at 0.5847.

- AUDUSD recovered off session lows with the two-week decision comments but remained lower on the day. It narrows the gap with the next key support at 50-day EMA - the first real test of any correction lower. Most recent weakness emphasises the significance of 0.6550 resistance (Nov 25 high) which has capped the topside across June. A break of the 50-day at 0.6432 is required to highlight a potential short-term reversal and target 0.6357, the May 12 low.

- Elsewhere, USDJPY gained further traction to the topside on a breach of last week’s high of 145.46, reaching a session high of 145.77. The renewed dollar strength amid the geopolitical concerns and the hawkish tilt to the June FOMC meeting have provided tailwinds for the pair, signalling scope for a stronger bounce to key short-term resistance at 146.28, the May 29 high.

- The data calendar includes both UK and Canadian retail sales on Friday. BOJ Governor Ueda is also due to speak at the Annual Meeting of the National Association of Shinkin Banks.

COMMODITIES: Crude Pares Gains Amid Iran Talk Hopes, Gold Unchanged

- Oil has pared gains after the White House said that President Trump believes there is a substantial chance of negotiations with Iran, and that he would make a decision on a military strike within two weeks.

- This supports previous reporting that he has not yet made a decision on military action, and leaves the door open for diplomacy and negotiations.

- WTI Jul 25 is up by 0.1% at $75.1/bbl, having traded as high as high as $77.6 earlier in the session.

- For WTI futures, price action is likely to remain volatile near-term, and from a technical standpoint, the trend is in an extreme overbought position.

- A continuation higher would expose the $80.00 handle, while a firm support is noted $67.11, the Jun 13 low.

- Elsewhere, spot gold has traded in a tight range and remains broadly unchanged around $3,369/oz amid quieter markets with the US on holiday for Juneteenth.

- Analysts at Phillip Nova Pte have said that with gold hovering near record highs, safe-haven flows are being redirected towards platinum and silver.

- From a technical perspective, however, a bullish theme in gold remains intact. Resistance at $3,435.6, the May 7 high, has been pierced, and a clear break of this level would strengthen the uptrend and open $3,500.1, the Apr 22 all-time high.

- Initial key support to monitor is $3,279.1, the 50-day EMA.