CANADA DATA: Small Business Optimism Improves, Price Plans Still On Higher Side

Jun-19 12:00

- CFIB small business confidence increased to 47.3 in June from 40.1 for a third monthly increase off historical lows of 25.5 in March seen on the threat of a US trade war.

- It’s still below the 50 level considered a balanced economic outlook, with the index generally in line with the BoC’s view that sentiment is low but not heading for a disaster scenario.

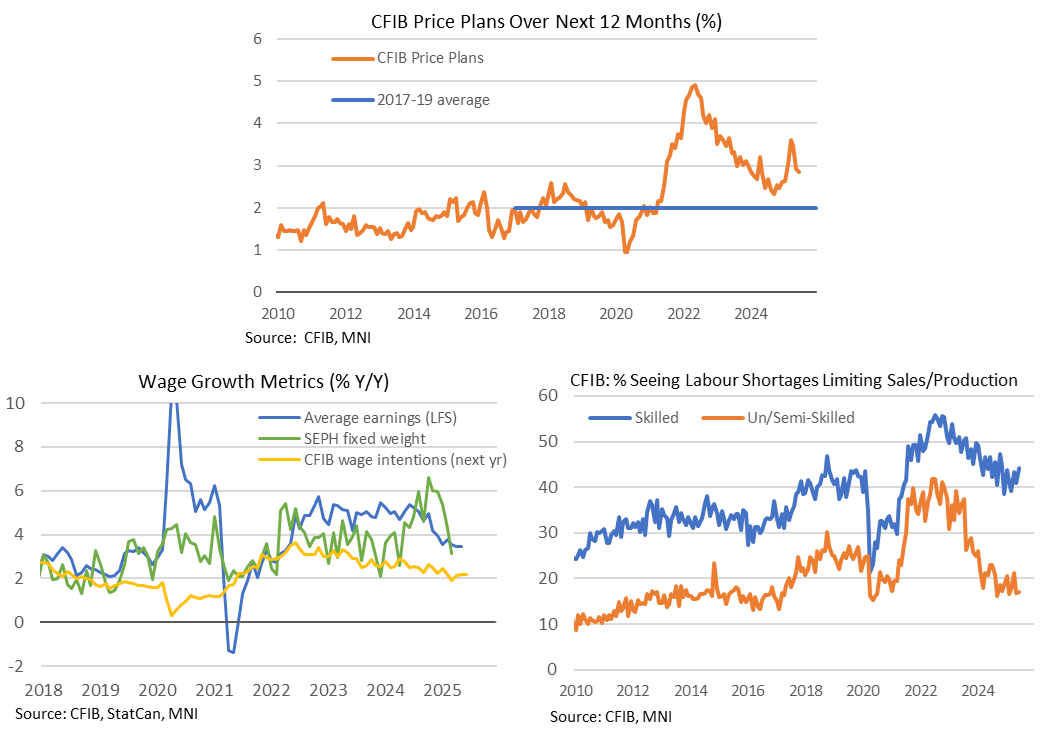

- Within the survey, expected average price increases over the next twelve months held steady at 2.9% (a touch lower unrounded at 2.85% after 2.91%).

- These expected price increases have pulled back from 3.46% in April and the recent high of 3.6% in March – highest since mid-2023 – but are above the 2.65% averaged in 2024 and more notably the 2.0% pre-pandemic.

- Wage growth intentions remain on the softer side meanwhile, holding at 2.2% for a second month and having also averaged 2.2% in the year to date. This is down from 2.6% averaged in 2024 and close to the 2.0% seen pre-pandemic.

- The report notes that "Full-time staffing plans remain muted with no real appetite for hiring". That's despite still high levels of those reporting skilled labour shortages are limiting sales or production, with 44% the highest since January.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA: OPTIONS: SFIQ5 96.10/96.25/96.40 Call Fly Lifted

May-20 11:58

SFIQ5 96.10/96.25/96.40 call fly paper paid 2.5 on 6K.

US TSY FUTURES: June'25-September'25 Roll Update

May-20 11:56

The latest Tsy quarterly futures roll volumes from June'25 to September'25 below. Percentage complete only 5%-10% across the curve ahead the "First Notice" date on May 30. Current roll details:

- TUM5/TUU5 appr 6,600 from -8.88 to -8.62, -8.75 last, appr 5% complete

- FVM5/FVU5 appr 44,300 from -3.75 to -3.25, -3.5 last, appr 10% complete

- TYM5/TYU5 appr 25,300 from -1.75 to -1.0, -1.5 last, appr 7% complete

- UXYM5/UXYU5 appr 4,100 from 3.25 to 3.5, 3.5 last, appr 2% complete

- USM5/USU5 appr 1,400 from 10.25 to 10.75, 10.25 last, appr 5% complete

- WNM5/WNU5 appr 1,400 from 6.0 to 7.0, 6.25 last, appr 5% complete

- Reminder, June futures won't expire until next month: 10s, 30s and Ultras on June 18, 2s and 5s on June 30. June Tsy options, however, expire May 23.

STIR: Modest SONIA Weakness Noted; SFI/ER Z5 Spread Pierces 200bps

May-20 11:38

SONIA futures have come under some pressure over the last ~40 minutes, now underperforming Euribor and SOFR counterparts on the session. We haven’t seen a clear headline trigger for the weakness, which may instead represent a delayed assessment of Chief Economist Pill’s remarks earlier this morning (see above for our thoughts).

- Yesterday’s low of 96.220 has contained downside in SFI Z5 today, with the contract now -2.0 ticks at 96.225.

- That sees the Sonia/Euribor Z5 spread pierce 200bps for the first time since April 22, and before that April 3.

- MNI's preview of tomorrow's April UK inflation print will be released in due course.

- Eurozone headline and data flow has been relatively light. The hawkish-leaning Knot did not rule out a June ECB cut, but needs to see the June macroeconomic projections before making a decision.

- It’s likely that the ECB will revise its GDP and inflation projections lower relative to March, even after the recent reduction in US/China tariff rates.

- A reminder that the ECB’s March projections saw headline inflation at 2.3% in 2025 and 1.9% in 2026. In its Spring forecasts released yesterday, the EC projected 2025 inflation at 2.1% and 2026 at 1.7%. That provides an initial indication of where the ECB’s June forecasts might end up, assuming broadly similar methodologies across the EC and national central banks/the ECB.