MNI ASIA OPEN: Trade Optimism, Dovish Fed Speak Buoy Markets

EXECUTIVE SUMMARY

- MNI FED: Gov Waller: Layoffs A Bigger Concern Than Inflation In Tariff Uncertainty

- MNI US DATA: Jobless Claims Still Robust

- MNI US DATA: Core Orders Flat Whilst Aircraft Orders Surge

- MNI US DATA: KC Fed Manufacturing Survey Shows Further Tariff Stagflation Effects

- MNI US DATA: Multiple Signs Of Weakness In Existing Home Sales Report

US

MNI FED: Gov Waller: Layoffs A Bigger Concern Than Inflation In Tariff Uncertainty

Fed Gov Waller on Bloomberg TV reinforces his credentials as one of the most dovish members on the FOMC, clearly emphasizing concerns over the growth impact of tariffs, vs what he sees as the likelihood that their inflation impact will only be a one-off. Previously he's said that he sees rate cuts either way, either in "good news/lower tariff" or "bad news/large tariff" scenarios, and his latest commentary reflects this though it's notable he doesn't think that the FOMC will have enough data to make a decision until later in the year though emphasizes that there are multiple downside signals that could warrant a cut before it is too "late".

- Waller says that in the "smaller tariff world" of 10-12%, most private firms can deal with it - however it would "not surprise me" to see layoffs tick up going forward if the "big tariffs come back up". Overall "every person I have talked to in the private sector" are "just kind of frozen", and "capex and everything has come to a stop".

NEWS

MNI TARIFFS: White House Nearing Deal With India That Could Act As Trade Template

Charles Gasparino at Fox Business reporting on X that, “People inside the Trump White House are alerting Wall Street execs they are nearing an agreement in principle on trade with India”. Gasparino adds: “No details on timing, and recall that we have been here before with Japan only to have the goal posts changed, and terms renegotiated. But if this holds, the India deal being envisioned … could be used as a template for a deal with Japan, South Korea and Australia, my sources add.”

MNI NATO: Rutte In Washington Amid Faltering Ukraine Peace Process

NATO Secretary General Mark Rutte is in Washington, D.C., today and tomorrow, holding talks with US Secretary of State Marco Rubio, Secretary of Defense Pete Hegseth, and National Security Adviser Mike Waltz. While the agenda for the meeting is not yet public, the apparent faltering of the US' commitment to reaching a peace deal in Ukraine is likely to dominate proceedings. Meeting due to get underway at 1500ET (2000BST, 2100CET).

MNI ECB Review Looks To Limit “Constraining” Forward Guidance – BBG Sources

Bloomberg sources suggest the ECB is set to consider changing its monetary policy strategy to enable “more nimble responses to price shocks as the global environment becomes increasingly volatile”. “ECB Governing Council members will discuss the case for such a shift at an informal retreat on May 6-7 in Porto, Portugal, where they will conduct their first in-depth debate on an ongoing review of their strategy, according to people familiar with the preparations who asked not to be identified citing confidential discussions.”

MNI UKRAINE: Zelenskyy-No Strong Pressure On Russia At Present

Comments from President Volodymyr Zelenskyy being reported by Reuters. Says "Ukraine is ready to do everything [its] partners propose, but cannot do things which contravene Ukraine's constitution." In an indirect criticism of the US, says he does not see "strong pressure on Russia at present", and that to negotiate with Russian "terrorists" after the ceasefire is implemented is "already a big compromise" on Ukraine's part.

MNI INDIA: PAKISTAN-Tensions Escalate Amid Flurry Of Reciprocal Punitive Measures

Tensions between India and Pakistan are at their highest level in years following a terrorist attack in Indian-administered Kashmir on 22 April that killed 26 in the tourist town of Pahalgam. India, which blames Pakistan for the attack, has closed its main border crossing with Pakistan, suspended a water-sharing treaty, ordered the expulsion of military diplomats, and halted visa services to Pakistani nationals 'with immediate effect'.

MNI US TSYS: Trade Negotiation Optimism Spurs Strong Risk-On Support

- Treasuries are holding at/near late Thursday session highs after the bell, as are stocks - in a positive reaction to trade "negotiations" headlines with India and South Korea: "nearing an agreement in principle on trade" on the former.

- Cautious risk-on tone has stocks climbing through the session, SPX eminis are currently (5514.75) at the highest levels since April 9 when Pres Trump granted 75 other countries get a 90 day pause and reduction in reciprocal tariffs.

- Jun'25 10Y futures currently +17 at 111-06 vs. 111-08 high, next resistance to watch remains 111-25, 50.0% of the Apr 7 - 11 bear leg sell-off. Clearance of this level would undermine the bearish theme.

- Treasuries pared gains after latest Durable Goods orders surge high, weekly claims in-line, continuing climbs lower than expected, Chicago Fed activity index lower than expected (prior up-revised). Existing home sales came in well below expectations at 4.02M (4.13M expected, 4.27M prior rev from 4.26M). That's the lowest figure since September, and a 2.4% Y/Y drop, suggesting that activity is slowing again.

- Rates rebounded after Cleveland Fed Hammack sees potential move from Fed in June if data is "convincing". Meanwhile, Fed Gov Waller emphasized concerns over the growth impact of tariffs, vs. what he sees as the likelihood that their inflation impact will only be a one-off.

- Markets will be watching Friday's University of Michigan sentiment and inflation expectations data at 1000ET.

OVERNIGHT DATA

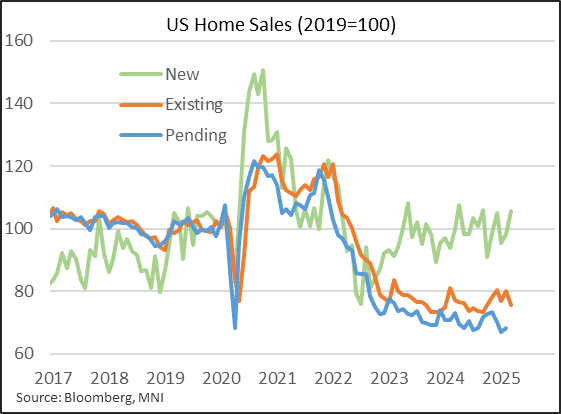

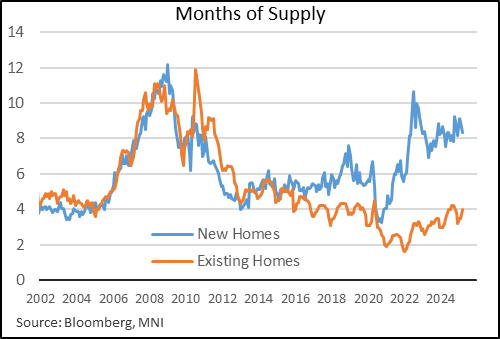

MNI US DATA: Multiple Signs Of Weakness In Existing Home Sales Report

Existing home sales came in well below expectations at 4.02M (4.13M expected, 4.27M prior rev from 4.26M). That's the lowest figure since September, and a 2.4% Y/Y drop, suggesting that activity is slowing again after a bit of a pickup in late 2024/early 2025 which largely reflected a temporary dip in mortgage rates. There were several signs of weakness in this report, even beyond the sharp slowdown in sales in the month.

- First, inventory picked up to the equivalent of 4.0 months of supply, a 5-month high and continuing the rise from 3.2 in December (which was a 9-month low). These are still fairly tight levels on a historical basis, but clearly trending toward a looser market. Inventory was up 19.8% Y/Y.

- Second, the weakness in sales was broad-based, with all four US regions seeing a decline - the first time that's happened since October 2023.

- Third, while median prices rose by 2.7% Y/Y to $403.7k, this was the weakest growth in 7 months.

- The NAR press release cited high mortgage rates as a key dampener on activity: "Home buying and selling remained sluggish in March due to the affordability challenges associated with high mortgage rates," said NAR Chief Economist Lawrence Yun. "Residential housing mobility, currently at historical lows, signals the troublesome possibility of less economic mobility for society."

- Mortgage rates have risen further since March along with a broader tariff-related selloff in Treasuries.

- If anything it looks from pending home sales - a leading indicator as though existing sales could pull back further.

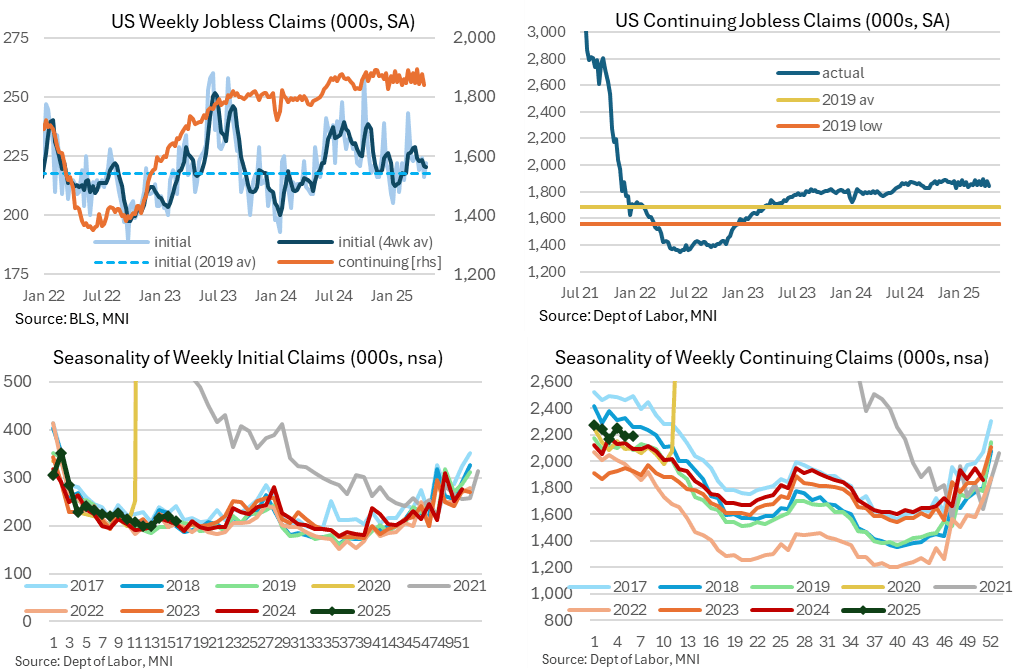

MNI US DATA: Jobless Claims Still Robust

The latest weekly jobless claims report continued to show no sign of latest deterioration in the labor market, with initial claims at historically low level and continuing claims broadly averaging where they’ve been for six months now hinting at softer rehiring conditions but nothing dramatic. The report chimes with recent labor comments from '26 voters Hammack and Kashkari and appears a little more robust than a further slight deterioration seen in yesterday's Beige Book.

- 222k (sa, cons 222k) in the week to Apr 19 after a marginally upward revised 216k (initial 215k).

- The four-week average dipped 1k to 220k for its lowest since mid-Feb, with the usual comparison that initial claims averaged 218k in 2019 for a prior period of labor market tightness.

- Continuing claims: 1841k (sa, cons 1869k) in the week to Apr 12 after a downward revised 1878k (initial 1885k).

- This latest continuing claims data covers a payrolls reference period and helps consolidate a pullback to some better readings in recent months: 1841k after 1847k in both Mar and Feb reference weeks, 1849k in Jan and 1882k in Dec and 1892k in Nov.

- The report chimes with Hammack a little earlier with “*HAMMACK: FIRMS STILL HESITANT TO LET WORKERS GO” – bbg and Kashkari two days ago: *KASHKARI: NOT SEEING EVIDENCE OF WIDESPREAD LAYOFFS; *KASHKARI: FEDERAL JOB CUTS NOT MAKING BIG DENT IN ECONOMY” - bbg

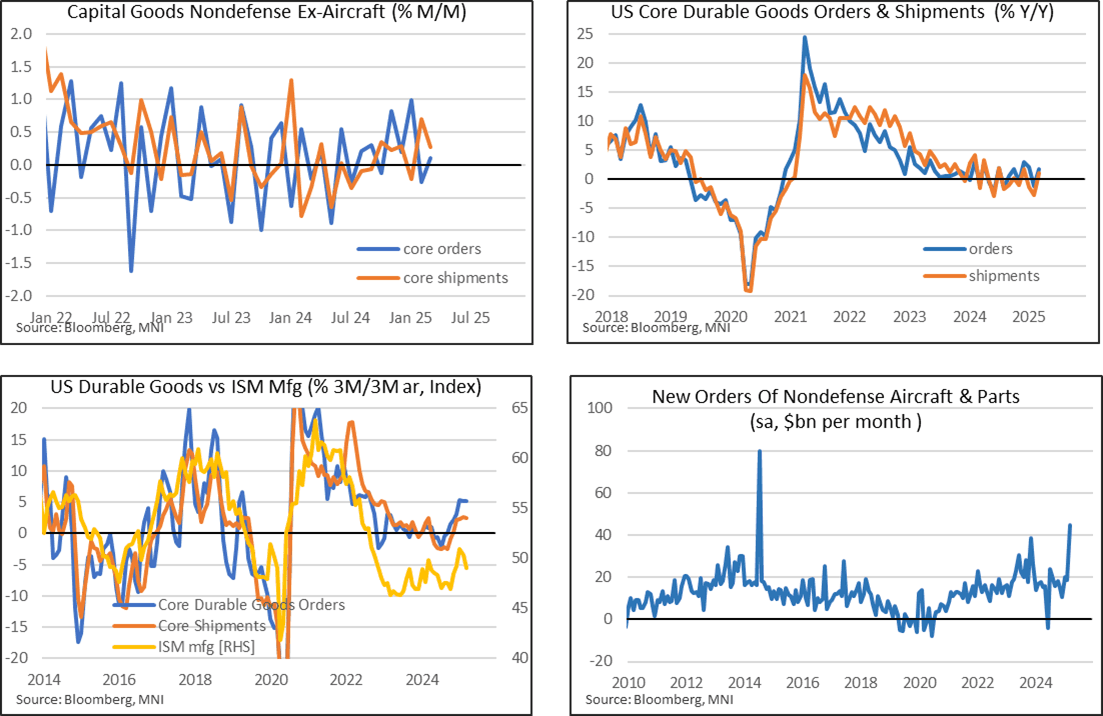

MNI US DATA: Core Orders Flat Whilst Aircraft Orders Surge

- Durable goods orders surged 9.2% M/M (sa, cons 2.0%) in March preliminary data after 0.9% M/M (initially 1.0%) in February.

- Core orders meanwhile were as expected, and tepid, at 0.1% M/M (cons 0.1) after -0.3% M/M (initially -0.3%).

- The wedge came as nondefense aircraft & parts orders surged 139% M/M after -7.4% in Feb and 93% in Jan. See the levels of new orders in the chart below.

- Whilst core orders have essentially paused in Feb and March, prior momentum still points to a healthy 3m/3m rate of 5% annualized although this could fade ahead. The Y/Y meanwhile runs at 1.8%.

MNI US DATA: KC Fed Manufacturing Survey Shows Further Tariff Stagflation Effects

The Kansas City Fed's Tenth District Manufacturing survey showed a deterioration of activity in April after March's surprising 15-month high. The month-over-month composite index fell to -4 in April from -2 prior (-6 was expected). While the composite index remains basically at the same negative level it's been since late 2022, the continued dip in the 6-month outlook (to 6 from 10 prior and the 4th consecutive decline) was notable albeit still positive.

- Price pressures were pronounced: while current prices paid remained at 42.0 (still a joint 31-month high), the 6-month outlook rose 14 points to 71, a 36-month high. Regional manufacturers reported much higher current prices received however (up 14 points to 29, a 32-month high), with the 6-month outlook rising 20 points to to 59, a 34-month high.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 486.83 points (1.23%) at 40093.4

S&P E-Mini Future up 121 points (2.24%) at 5521.75

Nasdaq up 458 points (2.7%) at 17166.04

US 10-Yr yield is down 7.4 bps at 4.3071%

US Jun 10-Yr futures are up 17.5/32 at 111-6.5

EURUSD up 0.007 (0.62%) at 1.1386

USDJPY down 0.79 (-0.55%) at 142.66

Gold is up $53.94 (1.64%) at $3342.46

European bourses closing levels:

EuroStoxx 50 up 16.24 points (0.32%) at 5114.98

FTSE 100 up 4.26 points (0.05%) at 8407.44

German DAX up 102.54 points (0.47%) at 22064.51

French CAC 40 up 20.42 points (0.27%) at 7502.78

US TREASURY FUTURES CLOSE

3M10Y -6.512, -0.61 (L: -1.063 / H: 5.099)

2Y10Y +1.009, 51.63 (L: 50.359 / H: 52.753)

2Y30Y +2.753, 97.486 (L: 94.354 / H: 98.785)

5Y30Y +3.752, 83.566 (L: 79.672 / H: 84.12)

Current futures levels:

Jun 2-Yr futures up 4.25/32 at 103-24.375 (L: 103-19.375 / H: 103-24.625)

Jun 5-Yr futures up 11.75/32 at 108-14.25 (L: 108-01 / H: 108-14.75)

Jun 10-Yr futures up 18/32 at 111-7 (L: 110-20.5 / H: 111-08)

Jun 30-Yr futures up 1-0/32 at 115-5 (L: 114-08 / H: 115-08)

Jun Ultra futures up 1-08/32 at 119-15 (L: 118-10 / H: 119-19)

MNI US 10YR FUTURE TECHS: (M5) Resistance Remains Intact

- RES 4: 113-04 76.4% retracement of the Apr 7 - 11 bear leg

- RES 3: 112-12 61.8% retracement of the Apr 7 - 11 bear leg

- RES 2: 111-25 50.0% retracement of the Apr 7 - 11 bear leg

- RES 1: 111-18+ High Apr 23

- PRICE: 111-06 @ 1350 ET Apr 24

- SUP 1: 110-15/109-08 Low Apr 15 / 11 and the bear trigger

- SUP 2: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 3: 108-21 Low Feb 19

- SUP 4: 108-03+ Low Dec 12 ‘24 and a key support

Treasury futures traded higher Wednesday, rallying to touch 111-18+ before reversing. This reinforces recent gains as corrective. The next resistance to watch remains 111-25, 50.0% of the Apr 7 - 11 bear leg sell-off. Clearance of this level would undermine the bearish theme. The trend condition is bearish, a resumption of weakness would refocus attention on 109-08, the Apr 11 low and the bear trigger.

SOFR FUTURES CLOSE

Jun 25 +0.020 at 95.880

Sep 25 +0.045 at 96.250

Dec 25 +0.060 at 96.525

Mar 26 +0.080 at 96.710

Red Pack (Jun 26-Mar 27) +0.090 to +0.095

Green Pack (Jun 27-Mar 28) +0.090 to +0.095

Blue Pack (Jun 28-Mar 29) +0.080 to +0.085

Gold Pack (Jun 29-Mar 30) +0.070 to +0.080

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (-0.02), volume: $2.475T

- Broad General Collateral Rate (BGCR): 4.27% (-0.02), volume: $1.025T

- Tri-Party General Collateral Rate (TCR): 4.27% (-0.02), volume: $989B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $290B

FED Reverse Repo Operation

RRP usage recedes to $130.004B this afternoon from $171.780B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 33.

MNI PIPELINE: Corporate Bond Update: $1.75B Micron 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 04/24 $3B *Bank of America perpNC5 6.625%

- 04/24 $1.75B #Micron $500M +7Y +158, $1.25B +10Y +175

- 04/24 $1.5B #Nippon Life 30NC10 6.5%

- 04/24 $600M #Pacific Life 3Y +65

- 04/24 $500M #Western-Southern Global Funding 5Y +100

- 04/24 $500M *Tokyo Metro Gov WNG 5Y SOFR+77

- 04/24 $500M ADB tap 2028 SOFR+37a

- 04/24 $1.75B #Micron $500M +7Y +158, $1.25B +10Y +175

- 04/24 $500M #SMFG 5Y +128

MNI BONDS: EGBs-GILTS CASH CLOSE: ECB Commentary Spurs German Bull Steepening

European yields pulled back Thursday, with the German short-end and UK long-end showing relative strength.

- ECB commentary was a key focus in the session, with Rehn and Lane discussing the possibility of larger-than-25bp rate cuts albeit in more of a "philosophical" sense than guidance to a future move.

- That helped deepen ECB rate cut pricing, in turn spurring front-end EGB outperformance on the curve. UK instruments firmed in sympathy, while broader global core FI benefited from comments by Fed officials perceived as dovish-leaning.

- Data took a back seat: German Ifo data beat expectations but had little lasting impact.

- The German curve bull steepened, with the UK's bull flattening. 10Y Gilts saw their lowest closing level Since Apr 4, with 10Y Bunds 0.5bp off their lowest close since February.

- Periphery / semi-core EGB spreads tightened, with BTPs leading.

- Friday's calendar includes UK retail sales and French confidence indicators, with an appearance by BOE's Greene.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 6.1bps at 1.685%, 5-Yr is down 6bps at 1.988%, 10-Yr is down 4.9bps at 2.448%, and 30-Yr is down 3.4bps at 2.877%.

- UK: The 2-Yr yield is down 3.7bps at 3.879%, 5-Yr is down 4.4bps at 3.995%, 10-Yr is down 5.2bps at 4.5%, and 30-Yr is down 6.5bps at 5.244%.

- Italian BTP spread down 3.6bps at 109.7bps / Spanish down 2.6bps at 64.3bps

MNI FOREX: Major Pairs Hold Relatively Tight Ranges Despite Equities Surge

- Currency markets were relatively stable for much of Thursday's session, as major pairs held narrow ranges throughout the US session. Bbg US$ index extended lows in late trade, BBDXY -5.29 at 1223.31.

- The more constructive tone for risk sentiment may have been driven by headlines regarding the White House "nearing an agreement in principle on trade with India". This has boosted the likes of AUD and NZD to outperform. Given the surrounding sentiment around the broader dollar, AUDUSD may have a lot of room to appreciate, particularly in the context of AUDUSD remaining 4.5% below the US election related highs, at 0.6688. The significance of 0.6400 as a pivot point on the chart leaves the pair at an important juncture.

- USDCHF highs of 0.8311 overnight fell around 20 pips shy of the prior breakdown point at 0.8333, the 2023 low. With bearish conditions prevailing, spot has reverted back towards 0.8270. We noted yesterday that Danske have updated their 12-month forecast for USDCHF to 0.7500.

- In emerging markets, ZAR (-1%) weakness stands out despite the firmer risk tone. USDZAR is through resistance at the 20-day EMA, and the next level to watch is 19.1531, the Apr 14 high. Implications of the ZAR75bln hole left in the 2025 Budget is clearly in focus for markets.

- Tokyo CPI is due during APAC on Friday, and will be followed by UK and Canadian retail sales data later in the session. Notably, SNB President Schlegel is due to speak at the central bank’s AGM – likely to acknowledge the recent firming of the Swiss Franc, but to not provide a view on nominal CHF valuations.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/04/2025 | 0600/0700 | *** | Retail Sales | |

| 25/04/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 25/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 25/04/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 25/04/2025 | 1915/2015 | BOE's Greene on Inflation, growth and moentary policy | ||

| 25/04/2025 | 2000/1600 | Kevin Warsh |