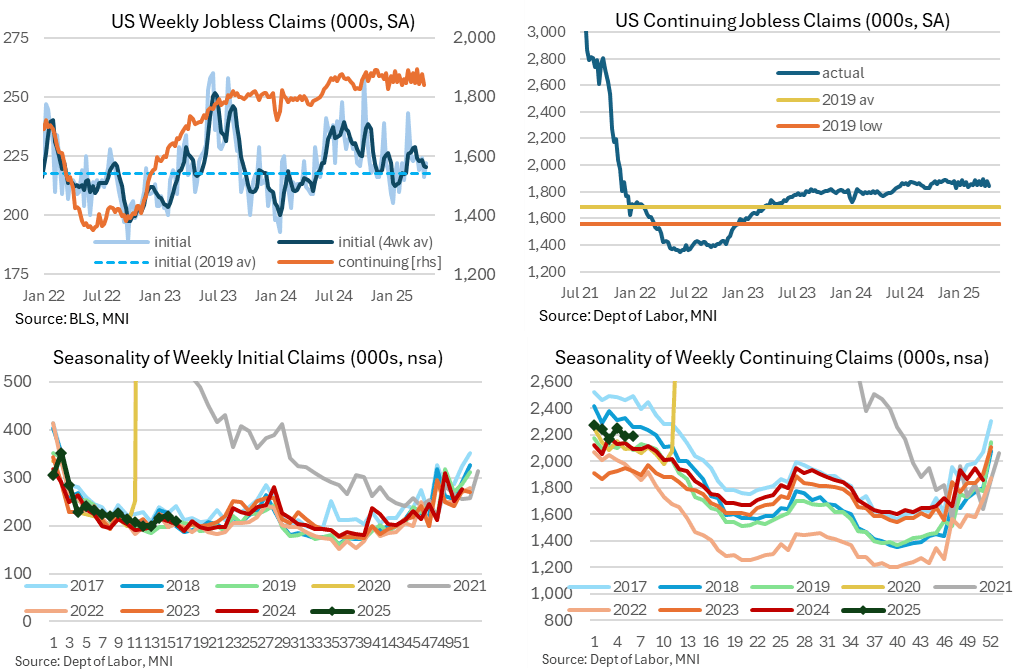

US DATA: Jobless Claims Still Robust

The latest weekly jobless claims report continued to show no sign of latest deterioration in the labor market, with initial claims at historically low level and continuing claims broadly averaging where they’ve been for six months now hinting at softer rehiring conditions but nothing dramatic. The report chimes with recent labor comments from '26 voters Hammack and Kashkari and appears a little more robust than a further slight deterioration seen in yesterday's Beige Book.

- 222k (sa, cons 222k) in the week to Apr 19 after a marginally upward revised 216k (initial 215k).

- The four-week average dipped 1k to 220k for its lowest since mid-Feb, with the usual comparison that initial claims averaged 218k in 2019 for a prior period of labor market tightness.

- Continuing claims: 1841k (sa, cons 1869k) in the week to Apr 12 after a downward revised 1878k (initial 1885k).

- This latest continuing claims data covers a payrolls reference period and helps consolidate a pullback to some better readings in recent months: 1841k after 1847k in both Mar and Feb reference weeks, 1849k in Jan and 1882k in Dec and 1892k in Nov.

- The report chimes with Hammack a little earlier with “*HAMMACK: FIRMS STILL HESITANT TO LET WORKERS GO” – bbg and Kashkari two days ago: *KASHKARI: NOT SEEING EVIDENCE OF WIDESPREAD LAYOFFS; *KASHKARI: FEDERAL JOB CUTS NOT MAKING BIG DENT IN ECONOMY” - bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT PAOF RESULTS: The PAOF for the 4.75% Oct-43 Gilt was not taken up.

- GBP500.0mln had been on offer.

- This leaves GBP30.479bln of the gilt in issue.

FED: Gov Kugler Concerned About Public Inflation Sensitivity And Goods Prices

Gov Kugler (permanent FOMC voter)'s overall view on rates is unsurprisingly very similar to pre-FOMC and the Committee's overall signalling of a wait-and-see stance on rate moves, per a speech Tuesday (text here) - consistent with a Fed that is not looking to ease until later in the year.

- "Given the economy’s overall solid position and the heightened level of uncertainty, I supported the Federal Open Market Committee’s decision last week to maintain the policy rate at its current level...I see current policy as continuing to be restrictive and I judge that FOMC policy is well positioned. The committee can react to new developments by holding at the current rate for some time as we closely monitor incoming data and the cumulative effects of new policies."

- On March 7 she said "it could be appropriate to continue holding the policy rate at its current level for some time", so this is arguably slightly more foreceful language on holding rates for an extended period.

- It is noticeable as the next round of tariff announcements loom in April that - like Powell last week - she calls out the apparent end of goods price disinflation as an "unhelpful" development as this category that "has often kept a lid on total inflation and also affects inflation expectations... I am paying close attention to the acceleration of price increases and higher inflation expectations, especially given the recent bout of inflation in the past two years".

- As for the latter, another interesting recent theme is that Fed officials are concerned public inflation expectations are arguably more sensitive to the upside now that consumers have had a taste of prolonged elevated inflation. Atlanta's Bostic said yesterday: “We’ve just gone through a period of elevated inflation so it’s very much on the consumer’s mind... I fear that they might be more sensitive to higher prices today than they have been in the past, but they might not, and we’ll just have to see how it plays out.”

GILTS: Steepening Risks Remain, Spring Statement Eyed

The UK's fiscal and monetary mix continues to point to further curve steepening over the medium-term.

- We previously highlighted this theme, while signalling some short-term risks, including already crowded positioning, impending event risk and the inability of both 2s10s and 5s30s to close above the next round of psychological levels (50bp & 100bp, respectively).

- A hawkish vote outcome at last week’s BoE decision added to a short-term flattening theme, before the monthly public finance data helped reintroduce a steepening bias.

- A reminder that most have pointed to 2s10s as their preferred steepener play, given expectations surrounding the DMO's maturity preference for funding any fiscal gaps, partly driven by the ongoing structural shift in pension demand.

- Any break higher in the 2s10s curve would target the '22 closing high (56.02bp), while a break higher in the 5s30s curve would target the May '21 closing high (103.03bp), which protects the '21 closing high (109.30bp).

- Chancellor Reeves has intimated that tax hikes are not in store at this week's Spring Statement, meaning that a combination of cost cutting and debt issuance is expected to plug the gap.

- Sell-side expectations that we have seen show a gilt remit range of GBP292 321bln, with a median of GBP303bln

- Terming out of the additional debt or an issuance target that is towards the higher end of/above those expectations would add to steepener conviction.

- Our full Spring statement preview is available here.

Fig. 1: UK 2-/10-Year & 5-/30-Year Yield Curves (bp)

Source: MNI - Market News/Bloomberg