MNI ASIA OPEN: Heavy Midweek Data, Mixed Jolts Jobs Data

EXECUTIVE SUMMARY

- MNI SECURITY: White House In "Close Correspondence" w/Interim VEN Authorities

- MNI US: Trump Pushes To Ban Institutional Investors From Buying Single-Family Homes

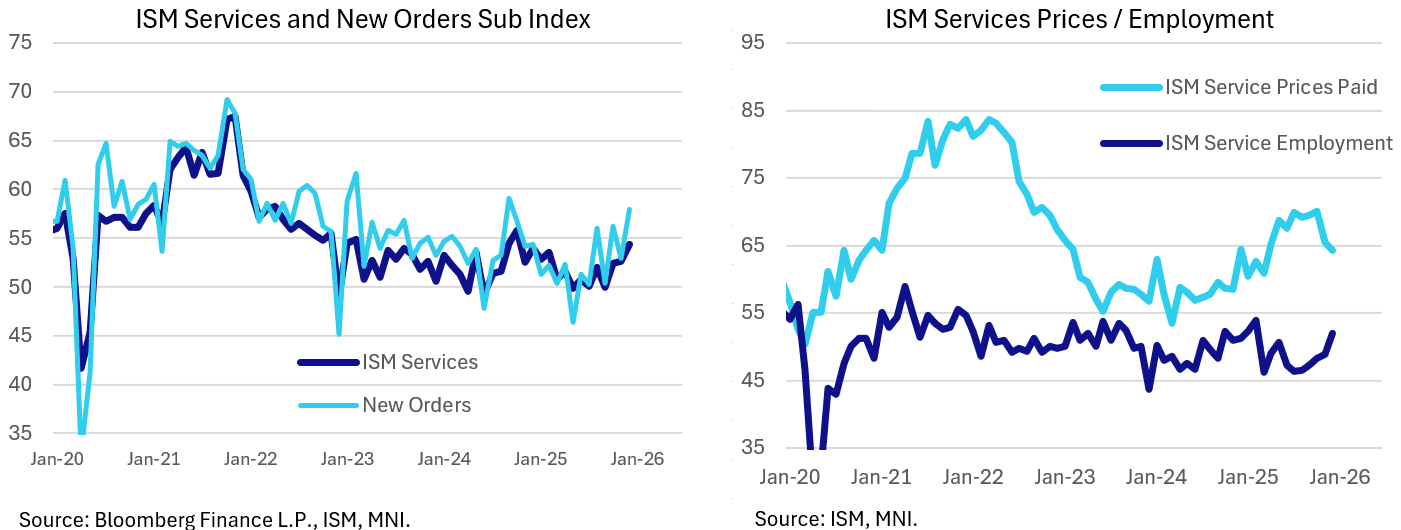

- MNI US DATA: Broad-Based Strength In ISM Services With Better Orders, Jobs

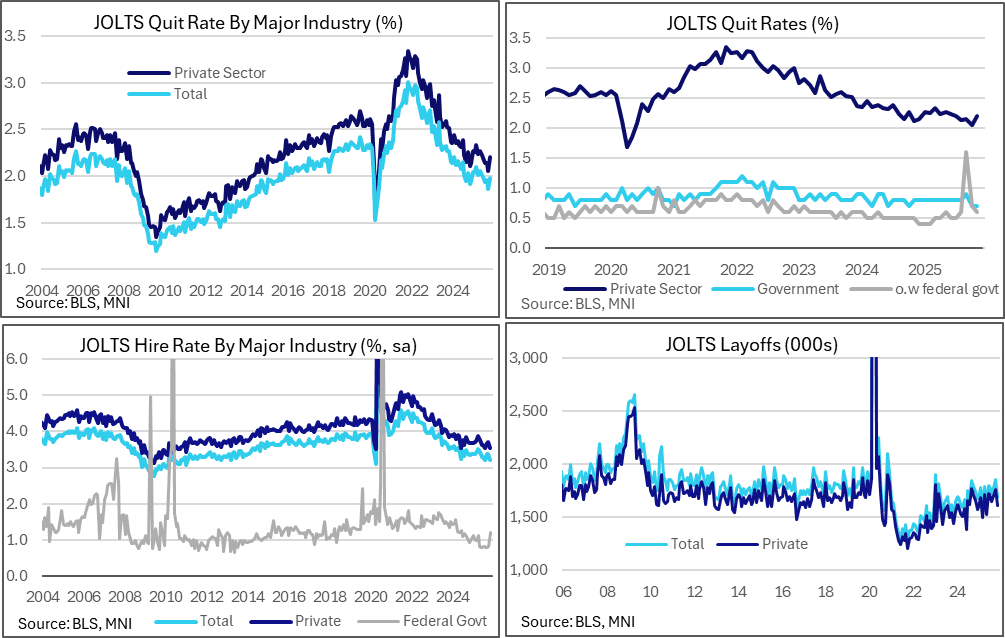

- MNI US DATA: Job Openings Surprisingly Slide In A Particularly Mixed JOLTS Report

- MNI US DATA: Quit Rate Improves And Layoffs Ease But Hire Rate Very Low

NEWS

Donald J. Trump: All United State Defense Contractors, and the Defense Industry as a whole, BEWARE: While we make the best Military Equipment in the World (No other Country is even close!), Defense Contractors are currently issuing massive Dividends to their Shareholders and massive Stock Buybacks, at the expense and detriment of investing in Plants and Equipment. This situation will no longer be allowed or tolerated!

MNI US: Trump Pushes To Ban Institutional Investors From Buying Single-Family Homes

Trump on Truth Social, pushing to ban large institutions from buying single-family homes. Bloomberg reports that Blackstone shares have extended their decline to 6% on the plan. "For a very long time, buying and owning a home was considered the pinnacle of the American Dream. It was the reward for working hard, and doing the right thing, but now, because of the Record High Inflation caused by Joe Biden and the Democrats in Congress, that American Dream is increasingly out of reach for far too many people, especially younger Americans. It is for that reason, and much more, that I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it."

MNI SECURITY: White House In "Close Correspondence" w/Interim VEN Authorities

White House Press Secretary Karoline Leavitt has told reporters at the White House that the Trump administration is in "close correspondence" with the "interim authorities" in Venezuela. She says that it is "too premature for an election timetable for Venezuela." Adds that the US will be "selectively rolling back sanctions" on the country to facilitate oil sales. Leavitt says, echoing Secretary of State Marco Rubio's comments moments ago on Capitol Hill, "we have maximum leverage" over the interim authority, whose decisions will be dictated by the US.

MNI SECURITY: Rubio Outlines '3-Fold' Process To Leverage VEN Oil To Enact Change

US Secretary of State Marco Rubio has outlined to reporters a “three-fold process” to leverage control over Venezuelan oil to dictate the terms of new administration in the country, following a classified briefing with Senators. He notes that he is unable to discuss “a lot of operational details.” LINK

MNI US: MNI POLITICAL RISK - Rubio Briefs Congress On Rising Military Tensions

The White House is prepping alternative strategies, as the Supreme Court prepares to release a ruling on Trump's tariffs. The US is reportedly demanding Venezuela reduce its relationships with China, Russia, Iran, and Cuba. Trump said Venezuela will be "turning over" 30 to 50 million barrels of oil to the US. Secretary of State Marco Rubio downplayed reports the US could acquire Greenland by force. Senate Democrats will force a vote Thursday on a war powers resolution requiring congressional approval for additional military action in Venezuela.

'China Tells Tech Companies to Halt Nvidia H200 Chip Orders; Officials May Mandate Domestic Ai Chip Purchases With Nvidia Orders' - The Information

US TSYS

MNI US TSYS: Midweek Data Dump Sees Treasury Futures Rebound, Curves Bull Flatten

- Treasuries look to finish stronger, upper half of a relatively volatile session range on heavier volumes (TYH6 over 1.8M) after the bell, curves bull flattening: 2s10s -3.941 at 66.838, 5s30s -2.641 at 112.372.

- Midweek data dump kicked off with monthly ADP - Treasury futures extend gains after ADP employment data came out lower than expected (prior drop up-revised slightly). Futures paring gains after stronger than expected ISM services, new orders and employ print, prices paid declines slightly; JOLTS openings & layoffs retreat while quits levels rise.

- Job openings ended November much lower than expected at 7146k (cons 7648k) after a downward revised 7449k in Oct (initial 7670k) and 7658k in Sep. It’s the lowest level of openings since Sep 2024 and before that Dec 2020.

- December's ISM Services report was meaningfully stronger than expected, with the headline PMI index surprisingly jumping to a 14-month high 54.4 (52.2 consensus, 52.6 prior). This was a strong report across the board, with all four major subindices in expansionary territory (Business Activity, New Orders, Employment, Supplier Deliveries) for the first time since February 2025, and a further downtick in price pressures.

- Some posts from Pres Trump rattled equities somewhat, at least housing and defense stocks after he pushed to ban large institutions from buying single-family homes, and warned defense contractors and the industry as a whole that executives should be prevented from making more than $5M annually, while the sector should be barred from allowing dividends and share buybacks.

- FX markets have been lacking conviction to start the year, potentially in anticipation of this Friday’s US employment report.

OVERNIGHT DATA

MNI US DATA: Quit Rate Improves And Layoffs Ease But Hire Rate Very Low

The JOLTS quit rate increased in November to a joint high since June, an encouraging development but still at a relatively low level, and layoffs surprised lower, but the hire rate is at one of its lowest levels in more than ten years. Quits recovered in November after a weak October, with the level rising to 3161k (cons 2995k, albeit just 4 responses) after an upward revised 2973k in Oct to nudge back above the 3128k in Sep.

- The quit rate increased to 1.98% after 1.86% in Oct (initially 1.84) and 1.96% in Sep, with 1.98% a joint high since June. Recent moves have been driven by private sectors with a quit rate at 2.20% after 2.06% in Oct (initially 2.03) and 2.15% in Sep.

- Government quit rates saw a second month at 0.7% having increased to 0.9% in Sep after sustained 0.8% readings before that. The push higher in Sep was driven by DOGE deferred resignations, with the federal govt quit rate jumping from 0.6% to 1.6% at the time after (it’s currently back at 0.6%).

- Layoffs were also encouraging as they fell to 1687k (cons 1816k, just 3 responses) after the 1850k in Oct was its highest since Jan 2023. That sees layoffs back at the lowest since May.

MNI US DATA: Job Openings Surprisingly Slide In A Particularly Mixed JOLTS Report

The November JOLTS report marked the opposite of last month’s two-month update, with this time a large miss for job openings but higher quits and lower layoffs. That said, hires also offered a more pessimistic take although it was at least broadly similar to last month’s previously estimated decline before latest revisions.

- Job openings ended November much lower than expected at 7146k (cons 7648k) after a downward revised 7449k in Oct (initial 7670k) and 7658k in Sep. It’s the lowest level of openings since Sep 2024 and before that Dec 2020.

MNI US DATA: Broad-Based Strength In ISM Services With Better Orders, Jobs

December's ISM Services report was meaningfully stronger than expected, with the headline PMI index surprisingly jumping to a 14-month high 54.4 (52.2 consensus, 52.6 prior). This was a strong report across the board, with all four major subindices in expansionary territory (Business Activity, New Orders, Employment, Supplier Deliveries) for the first time since February 2025, and a further downtick in price pressures.

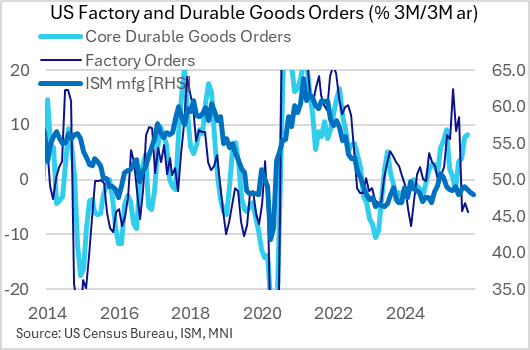

MNI US DATA: Factory Orders Remain Both Soft And Volatile, But Core More Solid

The delayed October Factory Orders data was roughly in line with expectations with a 1.3% M/M contraction (-1.2% M/M expected, +0.2% prior) whose weakness was heavily influenced by volatile aircraft orders (by comparison. ex-transport orders were down 0.2% M/M). We take more signal for the macro outlook from the relatively solid core data but overall manufacturing sector activity continues to look soft, with equipment investment implications mixed.

MNI US DATA: Chicago Fed CARTS Another Sign Of Solid Consumption At End-2025

The Chicago Fed Advance Retail Trade Summary (CARTS)'s preliminary estimate for December ex-auto retail sales growth is 0.4% M/M. That would be a pickup from the 0.3% M/M estimated in November (their est is unchanged) though we don't get the Census Bureau report for November until next week. It also brings the pace back up to the 0.4% actually posted in October (which CARTS accurately estimated).

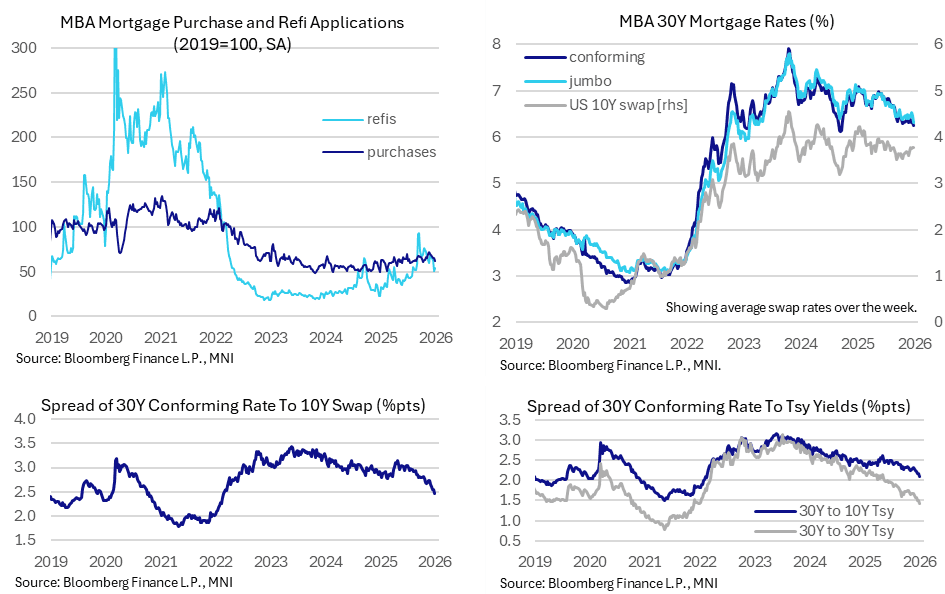

MNI US DATA: Mortgage Demand Slips Again Over Holidays Despite Spread Tailwind

MBA mortgage applications fell further over a two-week update although the data should be taken with caution over the holiday period. With that caveat in mind, there was another notable narrowing in mortgage swap rate spreads. The two-week update saw MBA composite applications increase just 0.3% in the latest week after a -10% drop in the week to Dec 26 around Christmas (all seasonally adjusted).

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 479.57 points (-0.97%) at 48983.27

S&P E-Mini Future down 25.25 points (-0.36%) at 6963

Nasdaq up 33.6 points (0.1%) at 23581.08

US 10-Yr yield is down 3.5 bps at 4.1377%

US Mar 10-Yr futures are up 7/32 at 112-17.5

EURUSD down 0.0009 (-0.08%) at 1.168

USDJPY up 0.13 (0.08%) at 156.78

WTI Crude Oil (front-month) down $0.89 (-1.56%) at $56.24

Gold is down $37.91 (-0.84%) at $4456.74

European bourses closing levels:

EuroStoxx 50 down 8.22 points (-0.14%) at 5923.57

FTSE 100 down 74.52 points (-0.74%) at 10048.21

German DAX up 230.06 points (0.92%) at 25122.26

French CAC 40 down 3.51 points (-0.04%) at 8233.92

US TREASURY FUTURES CLOSE

Curve update:

3M10Y -4.011, 53.939 (L: 51.616 / H: 57.557)

2Y10Y -3.952, 66.827 (L: 66.435 / H: 70.386)

2Y30Y -5.113, 134.87 (L: 133.946 / H: 139.368)

5Y30Y -2.785, 112.228 (L: 111.229 / H: 114.919)

Current futures levels:

Mar 2-Yr futures up 0.25/32 at 104-12.125 (L: 104-11.375 / H: 104-13.62)

Mar 5-Yr futures up 3.25/32 at 109-11 (L: 109-08.25 / H: 109-14)

Mar 10-Yr futures up 7.5/32 at 112-18 (L: 112-11 / H: 112-22)

Mar 30-Yr futures up 22/32 at 115-27 (L: 115-04 / H: 116-01)

Mar Ultra futures up 27/32 at 118-6 (L: 117-11 / H: 118-15)

MNI US 10YR FUTURE TECHS: (H6) Fades Off Highs

- RES 4: 113-00+ 6.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-19+/22 50-day EMA/High Jan 7

- PRICE: 112-15 @ 15:59 GMT Jan 7

- SUP 1: 112-01+/111-29 Low Dec 23 / 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Treasuries continue to trade above key support at 111-29, the Dec 10 low and bear trigger. An early rally briefly topped the 112-19+ 50-day EMA before prices quickly reversed. This keeps the trend set-up bearish and a breach of 111-29 would confirm a resumption of the bear cycle. This would open 111-19 initially, a Fibonacci projection. On the upside, key short-term resistance is unchanged at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 -0.010 at 96.455

Jun 26 steady00 at 96.670

Sep 26 +0.005 at 96.830

Dec 26 +0.010 at 96.890

Red Pack (Mar 27-Dec 27) +0.010 to +0.020

Green Pack (Mar 28-Dec 28) +0.025 to +0.035

Blue Pack (Mar 29-Dec 29) +0.035 to +0.035

Gold Pack (Mar 30-Dec 30) +0.035 to +0.045

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (-0.04), volume: $3.390T

- Broad General Collateral Rate (BGCR): 3.62% (-0.04), volume: $1.354T

- Tri-Party General Collateral Rate (TCR): 3.62% (-0.04), volume: $1.317T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $178B

FED Reverse Repo Operation

RRP usage inches up to $4.582B with 8 counterparties this afternoon vs. $2.582B Tuesday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Roundup: Over $32B to Price Wednesday

At least $32.45B corporate debt issued/to price Wednesday. Still waiting on BNP Paribas and Mutual of Omaha, see below:

- Date $MM Issuer (Priced *, Launch #)

- 01/07 $4.5B *Quebec 5Y SOFR+45

- 01/07 $3.5B #Turkiye +2B 7Y 6.35%, $1.5B 12Y 6.9%

- 01/07 $2.6B #Toyota Motor Cr $750M 2Y +32, $600M 2Y SOFR+45, $750M 5Y +52, $500M 10Y +67

- 01/07 $2.25BB #BFCM $1.5B 5Y +85, $750M 10Y +97

- 01/07 $2B *BNG Bank 10Y SOFR+54

- 01/07 $2B #Bank of Hapoalim $1B 3.5Y +120, $1B 7Y +135

- 01/07 $2B #T-Mobile USA $1.15B 10Y +87, $850M 30Y +103

- 01/07 $1.8B #Rabobank $400M 2Y +28, $500M 2Y SOFR+41, $500M 5Y +47, $400M 5Y SOFR+70

- 01/07 $1.5B *Kommunalbanken 5Y SOFR+38

- 01/07 $1.1B #Bank of Montreal 6NC5 +75

- 01/07 $1B *Council of Europe (CoE) Dev Bank 5Y SOFR+31

- 01/07 $1B #Daimler Truck NA $600M 3Y +67, $400M +5Y +83

- 01/07 $1B #Niagara Mohawk Power $650M 10Y +97, $350M 2055 tap +107

- 01/07 $1B *Riyad Bank 10NC5 +210

- 01/07 $1B #Aldar 30.25NC7.25 5.95%

- 01/07 $1B *AIIB 10Y SOFR+43

- 01/07 $850M #Rep of Chile +5Y +68

- 01/07 $750M *First Abu Dhabi Bank (FAB) 5Y +60

- 01/07 $600M #Met Tower 3Y +52

- 01/07 $500M *FMO 2.5Y SOFR+25

- 01/07 $500M #Banco Actinver WNG 12Y +155

- 01/07 $Benchmark Mutual of Omaha 5Y +85

- 01/07 $Benchmark BNP Paribas 8NC7 +102

- Expected Thursday:

- 01/08 $Benchmark OKB 5Y SOFR+37a

- 01/08 $Benchmark CAF 10Y SOFR+90a

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Shine As Rally Extends

The ongoing rally in EGBs and Gilts continued Wednesday, with gains extending to a 3rd consecutive session.

- The German and UK curves both bull flattened on the day, with some spillover from the softer-than-anticipated inflation data in the Eurozone national-level flash reports, though the aggregate Euro-wide reading this morning didn't have much impact having been by now well-anticipated.

- Gains faded by mid-afternoon after a strong US ISM Services report, offset by very mixed job openings/hiring data. Additionally Italy's mandate for a dual tranche syndication weighed across the EGB space.

- Gilts saw one of their best sessions in months, outperforming Bunds, with various factors including a solid UK auction and soft UK construction PMI.

- Periphery / semi-core EGB spreads widened slightly, with Italy and Spain underperforming.

- Thursday's schedule includes the latest BoE DMP survey in the UK,

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1bps at 2.09%, 5-Yr is down 2.6bps at 2.398%, 10-Yr is down 3bps at 2.812%, and 30-Yr is down 3.3bps at 3.447%.

- UK: The 2-Yr yield is down 1.8bps at 3.679%, 5-Yr is down 5.4bps at 3.861%, 10-Yr is down 6.4bps at 4.416%, and 30-Yr is down 7bps at 5.157%.

- Italian BTP spread up 1.1bps at 70.4bps / French OAT up 0.4bps at 71.3bps

MNI FOREX: Contained Major Ranges, NOKSEK Declines 0.5% Ahead of Regional Data

- FX markets have been lacking conviction to start the year, potentially in anticipation of this Friday’s US employment report. A strong ISM services release countered softer JOLTS job openings on Wednesday, keeping the dollar index in a very contained range post release, with both EURUSD and USDJPY are close to unchanged levels on the session.

- The most notable price action on Wednesday occurred during APAC hours following the release of Australian CPI. Markets quickly shrugged off lower-than-expected headline data, keeping AUD very well supported on dips. Subsequently, AUD spiked to a fresh cycle high of 0.6767, keeping topside levels of 0.6795 and 0.6858 as the next chart points of note. Meanwhile AUDNZD briefly rose to the highest level since 2013 at 1.1693.

- Elsewhere, the Swedish krona is outperforming today, rising around 0.25% against the Euro and 0.5% against the Norwegian Krone. Although the domestic growth outlook (supported by loose monetary policy and expansionary but still-responsible fiscal policy) remains SEK-supportive, analysts are cognizant that a lot of good news is already priced in.

- Technical conditions in EURSEK remain bearish, and clearance of the December 26 low of 10.7622 has narrowed the gap to key support at 10.6652 (March 4 low). We remain cognizant of key long-term support in NOKSEK at 0.9065 (April 9 low). Inflation data in Sweden (tomorrow) and Norway (Friday) will be the regional focus for the remainder of the week.

- In emerging markets, lower metals prices have stalled the impressive advance for the South African rand, prompting a 0.6% pull higher for USDZAR. Despite this, bearish conditions remain firmly intact, with initial resistance seen further out at 16.6687, the 20-day EMA.

- Swiss CPI and US jobless claims data highlight Thursday’s data calendar.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/01/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 08/01/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 08/01/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 08/01/2026 | 0730/0830 | *** | CPI | |

| 08/01/2026 | 0745/0845 | * | Foreign Trade | |

| 08/01/2026 | 0830/0930 | ECB de Guindos Fireside Chat at Next Spain | ||

| 08/01/2026 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 08/01/2026 | 0930/0930 | BOE Decision Maker Panel data | ||

| 08/01/2026 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 08/01/2026 | 1000/1100 | ** | EZ PPI | |

| 08/01/2026 | 1000/1100 | ** | EZ Unemployment | |

| 08/01/2026 | 1330/0830 | *** | Jobless Claims | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/01/2026 | 1500/1000 | ** | Wholesale Trade | |

| 08/01/2026 | 1500/1000 | ** | Wholesale Trade | |

| 08/01/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 08/01/2026 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/01/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/01/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/01/2026 | 2000/1500 | * | Consumer Credit | |

| 09/01/2026 | 2330/0830 | ** | Household spending | |

| 09/01/2026 | 0130/0930 | *** | CPI | |

| 09/01/2026 | 0130/0930 | *** | Producer Price Index |