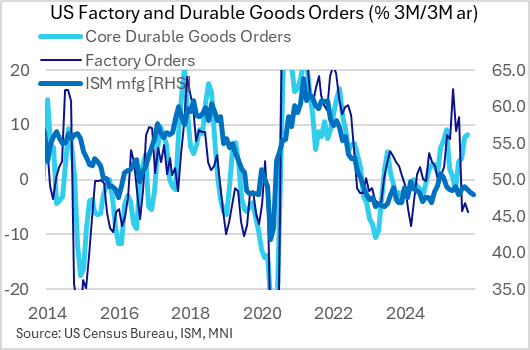

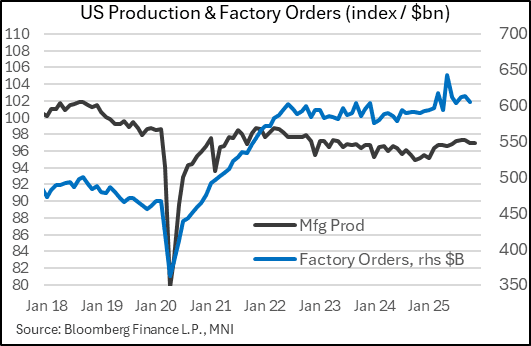

US DATA: Factory Orders Remain Both Soft And Volatile, But Core More Solid

Jan-07 15:57

The delayed October Factory Orders data was roughly in line with expectations with a 1.3% M/M contraction (-1.2% M/M expected, +0.2% prior) whose weakness was heavily influenced by volatile aircraft orders (by comparison. ex-transport orders were down 0.2% M/M). We take more signal for the macro outlook from the relatively solid core data but overall manufacturing sector activity continues to look soft, with equipment investment implications mixed.

- This had been presaged by the preliminary Durable Goods report which showed a 2.2% M/M contraction (confirmed in today's final data) with ex-transport durables up 0.1% (rev from 0.2%), with nondefense and defense aircraft down 20% M/M and 32% M/M respectively.

- Looking just at ex-transport manufacturing orders, there's been a slowdown in growth to 1.8% 3M/3M (around 3% the prior 2 months), with overall orders down 6.0% on that basis (weakest since early 2024). Overall in nominal terms, the level of factory orders is basically flat since mid-2022.

- The saving grace is in core durable goods orders momentum which has actually been accelerating, to an 8.3% 3M/3M growth rate in October, one of the fastest in recent years (and on another metric, was up 6.4% Y/Y). So while broader factory orders are weak, we attribute a large chunk of this to volatility.

- From a sectoral perspective, computers/electronics remain a key upside driver (outside of aircraft), up 3.8% Y/Y, perhaps reflecting AI-related buildout, with machinery goods up 4.2% Y/Y.

- Of course this data is lagged due to the government shutdown and various manufacturing activity surveys (including ISM and regional Feds) point to a potential slowdown in the latter months of the year.

- Somewhat strangely, the Census Bureau is due to publish the advance November data on January 26 but the final just three days later on January 29. But we are beginning to catch up on these data after the government shutdown (though December's postponed data is yet to be rescheduled).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Mar'26 SOFR Midcurve Call Spread Sale

Dec-08 15:52

- -20,000 0QH6 97.25/97.50 call spds, 2.25 ref 96.79

OPTIONS: Expiries for Dec09 NY cut 1000ET (Source DTCC)

Dec-08 15:50

- EUR/USD: $1.1585-90(E1.7bln), $1.1600(E755mln), $1.1675(E784mln), $1.1760(E1.3bln)

- EUR/GBP: Gbp0.8785-92(E530mln)

- AUD/USD: $0.6330-35(A$1.2bln)

US TSYS: Mar'26 10Y Futures Nearing Round Number Support

Dec-08 15:48

- Treasury futures continue to extend lows as momentum/sell-flow on heavier volumes appears to be main driver rather than headlines.

- Through key technical support at 112-07.5, the Mar'26 10Y contract trades down to 112-02.5 Sep 25 low). Holding above round number support at 112-00.

- Heavy selling has pushed TYH6 contract volume to 940,000 at the moment.

- Lone data for the day coming up at 1000ET: NY Fed Consumer Sentiment Survey (3.24% prior).