MNI ASIA OPEN - Dem's Senate Chances Tick Higher

EXECUTIVE SUMMARY:

- IRAN HOLDS STRAIT OF HORMUZ EXERCISES IN RESPONSE TO US THREATS

- DEMOCRAT CHANCES OF WINNING SENATE TICK HIGHER

- UK PM STARMER DROPS PLAN TO CANCEL LOCAL ELECTIONS

- UK AVERAGE EARNINGS EXPECTED TO SLOW, BUT STAY WELL NORTH OF INFLATION

- CANADIAN CORE INFLATION SEEN EDGING HIGHER

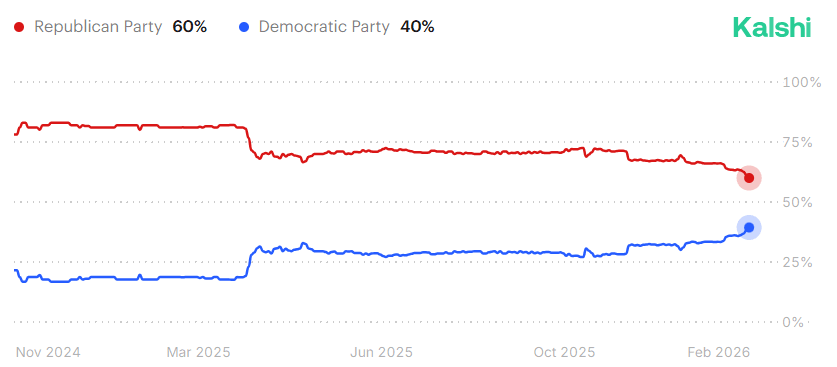

Figure 1: Which party will win the US Senate?

Source: Kalshi

NEWS:

US/IRAN (NYT): Iran Holds Exercises in Strait of Hormuz After Trump Threatens Military Action

The day before nuclear talks were set to resume, Iran conducted live drills in the Strait of Hormuz, a strategic waterway for oil and gas shipments. Iran held live military exercises on Monday in the Strait of Hormuz a day before nuclear talks between the United States and Iran were set to resume, an apparent show of its power as President Trump threatens military action and calls for regime change if diplomacy fails.

US (MNI): Democrats' Chances Of Winning Senate Tick Up

The implied probability of the Democratic Party gaining control of the US Senate at November's midterm elections has ticked up to 40%, according to Kalshi. Democrats have been strongly favoured to win the House of Representatives since a mini 'blue wave' in last November's off-year elections. Winning the Senate would block Trump from confirming executive branch nominees, including potentially a Supreme Court seat, should it become vacant.

FED (MNI): Bowman: "A Little Softer" CPI In Line With Her Expectations

Bowman (voter, dove) a little earlier in Q&A comments at the ABA conference, including Friday’s inflation data being “a little softer” than most expected but in line with her expectations: “Since I see the current policy stance as moderately restrictive, I do think there’s room for at least 75bp of more cuts in 2026 […] that’s what I wrote into my forecasts last December”. [That’s not a surprise having indicated as such in remarks on Jan 30, when she added that while she didn't elect to cut rates in January, she could be ready to cut in March]

SECURITY (MNI): US And Iran Manage Expectations Ahead Of Nuclear Talks In Geneva

Iranian foreign ministry spokesman Esmail Baghaei said Iran “gains no benefit from prolonged negotiations” with the US, adding that Tehran enters a second round of nuclear talks with Washington in Geneva tomorrow, with a “full political, legal, economic and technical team”, per Iran International. Both sides are managing expectations of a breakthrough, with discussions likely to continue hammering out the parameters of future talks rather than on the substantive details of a new nuclear agreement. Iran’s Deputy Parliament Speaker Hamidreza Hajibabaei said Tehran is "willing to engage in talks but does not trust Washington", per Iran Int.

US (MNI): DHS Shutdown Unlikely To Impact Operations Until Early March

The Department of Homeland Security ran out of funding on Friday evening, but the lapse of appropriations is unlikely to cause disruptions to operations until early March. Lawmakers are due to return from recess next week, but there is little to suggest that ending the 'mini shutdown' is a priority for either Democrats or Republicans. Punchbowl News notes, “DHS has more than 260,000 employees across an array of agencies. Somewhere around 90% of DHS employees are classified as essential, including 95% of TSA agents, most of the Coast Guard and Secret Service. These federal employees will work without pay throughout the funding lapse...”

US/HUNGARY (BBG): Rubio Wraps Hungary’s Orban in US Embrace Before Tight Election

Secretary of State Marco Rubio showered Viktor Orban with praise on a visit to Hungary as the US doubled down on its support for the strongman leader before an election that could bring an end to his 16 years in power.

UK (Telegraph): Starmer abandons plan to cancel local elections

Sir Keir Starmer has abandoned plans to cancel local elections in May following a Telegraph campaign. Elections in 30 local authorities will now go ahead, reversing a previous decision to delay them until 2027. The Prime Minister’s latest about-turn follows the launch of The Telegraph’s Campaign for Democracy, which called for the delayed elections to go ahead this year.

US TSYS: Holiday Test Of Next TY Resistance Pared Before Early Close

Treasuries slowly drifted higher today although pulled back after a brief test of resistance two hours out from the early close, with reasonable volumes considering the US was out for Presidents’ Day. Headlines have generally been light but with likely seemingly some geopol risk premia supporting the core FI space after it became apparent that Iran’s IRGC is holding ‘Smart Drills’ near the Strait of Hormuz to “test readiness in the face of 'possible security and military threats”.

- TYH6 trades at 113-07+ (+02) having earlier touched 113-12 to extend the post-CPI high of 113-07+ and more notably tested 113-11 (Dec 1, 2025 high). Volumes were relatively solid for a US holiday at 489k.

- With the short-term bull cycle remaining in play, a stronger clearance here could open a key 113-22+ (Nov 22, 2025 high). Potentially before then, 113-15 would mark a 4.00% 10Y yield having closed Friday at 4.048%.

- Rates meanwhile sees SOFR futures up to 1.5 ticks lower on the day, led by the U6. The terminal implied yield of 3.01% (M7) follows Friday's close of 3.005% for its lowest since late November.

- Fed Funds futures have 25bp cuts fully priced for July and October, with just 2.5bp of cuts for the next FOMC meeting in March.

- Fed Vice Supervision Bowman (voter, dove) earlier today described Friday's CPI inflation data being "a little softer" than most expected but in line with her expectations. She reiterated that she sees at least 75bp of cuts for 2026, unchanged from her December SEP submission.

- Tomorrow sees weekly ADP covering up to Jan 31 plus some early February surveys with Empire Manufacturing and the NAHB housing index. This week’s data calendar is heavily backloaded with Q4 GDP/Dec PCE and flash Feb PMIs all on Friday.

- Friday also sees the next scheduled SCOTUS opinion day, followed by further opinion days on Feb 24/25. As before, markets will have to wait for the sessions themselves to determine if a tariff ruling is on the agenda, usually from 10ET onwards.

FOREX: USDJPY Recovers Following Soft Growth Data in Japan

- The dollar index stands around 0.2% firmer on Monday, with FX market volatility contained by the US Presidents’ Day holiday. The greenback advance has been driven by a 0.55% rally for USDJPY, which has reacted to a softer-than-expected set of GDP data in Japan.

- The data signals that more needs to be done to boost economic growth, a key goal for the Takaichi regime, and renewed fiscal concerns will be driving the latest reversal in fortune for the yen. Short-term USDJPY parameters appear well established; the January lows at 152.10 provide key support, while the post-NFP highs at 154.65 offer the most notable resistance.

- The UK will see a data-heavy week with key inputs from the labour market, inflation and flash PMIs scheduled. For GBPUSD, broader dollar dynamics have been dominating allowing the pair to consolidate between the February 9 and 11 extremes of 1.3587 and 1.3712. On the downside, key S/T support lies at the 50-day EMA, at 1.3527.

- A positive session for USDCAD on Monday would mark a fourth consecutive day of gains for the pair as we approach tomorrow’s CPI report. A bearish condition for USDCAD remains intact, and sights are on key support at 1.3482, the Jan 30 low, just over 1% from current spot levels.

- Elsewhere, market participants also await the RBNZ decision Wednesday, the first with Governor Breman in charge. Despite the latest pullback for NZDUSD, spot remains within 100pips of 0.6120, of which a break would place the pair at the highest point since October 2024. Meanwhile, AUDNZD would be a key beneficiary of any dovish tilt following last week’s extension to 1.1807, the highest level reached dating back to July 2013.

- RBA minutes, UK labour market data and Canada CPI data are highlights tomorrow. China remains out for the lunar new year holiday.

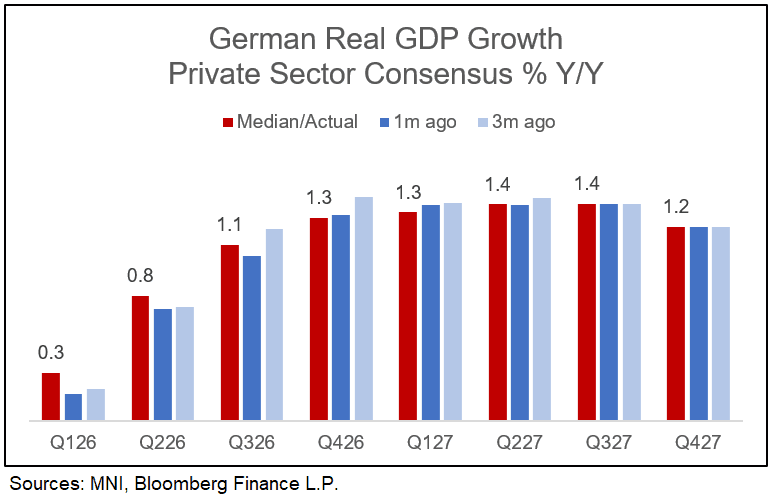

MACRO UPDATE: German Growth Seen Being More Front-Loaded

Private sector German short-to-medium-term GDP forecasts have seen some contained upward pressure over the past month. This comes as some but not all hard data has been starting to pick up in recent readings. Having said that, the longer-term view remains mixed at best with some structural reforms in the pipeline but analysts seemingly not convinced if these will bring a trend reversal to the upside.

- Updating a median estimate from seven sellside analysts that we track, Y/Y growth is expected to start accelerating in Q2 before topping out at 1.4% Y/Y over the course of 2027. For 2026 as a whole, this results in a current 1.0% median projection vs 0.8% a month ago.

- These latest estimates are consistent with the German government's view, also at 1.0% for 2026, whilst the IFO institute is marginally more pessimistic at 0.8% this year.

- Key metrics to track on the near-term pace of the growth uptick are the flash PMI and IFO current conditions readings, to be published Friday / Monday, respectively. Detailed January spending data on the infrastructure and military push is scheduled to be released this Friday. Early next month, January IP will be interesting to watch as it will show to what extent the December factory orders jump will start to filter through.

In terms of longer term trend growth, action taken by the government so far does not seem to result in resounding impact. There are some additional reforms in the pipeline but with mixed chances of implementation. The more sceptical picture here is well-illustrated by analysts' growth estimates starting to taper off once the initial fiscal push is expected to fade.

- An income tax reform/cut proposal from CDU general secretary Linnemann flagged over the weekend would cost roughly E9bln/year, institute DIW has calculated, and has been met with resistance from coalition partner SPD. This means large moves here over the near term seem unlikely.

- On the German social security system, a commission has suggested a reform package which has been received rather positively by commentators, seen to lead to less bureaucracy through combining services as well as increasing incentives to work. Labour minister Bas (SPD) has excluded benefit cuts. Comments from both government parties have also been rather positive, so chances are the package will be implemented while keeping its core intact.

US INFLATION: MNI US Inflation Insight: Underlying Pressures Remain

We have published and e-mailed to subscribers the MNI US Inflation Insight, found here: https://media.marketnews.com/US_Inflation_Insight_Feb2026_696747e852.pdf

UK DATA: MNI UK Data Preview: February 2026 Release

For the full preview including summaries of analyst expectations click here.

- It’s a huge week for UK data with labour market data (Tuesday), inflation data (Wednesday) as well as flash PMIs, retail sales and public finance data on Friday.

- In terms of market reaction, we think the easiest read is likely to come from labour market data where consensus expectations are aligned with the expectations from the February MPR. There will be one more labour market print ahead of the March MPC decision, but a print in line with expectations keeps a March cut very much in play.

- Things are trickier on the inflation side. The Bank’s updated staff forecasts put January headline CPI at 2.90%Y/Y which is a full tenth below consensus expectations of 3.0%Y/Y, and it seems as though this is pretty broad-based across categories. We look at the potential for market reaction and also the details of the print.

- In addition, we summarise 17 sellside views.

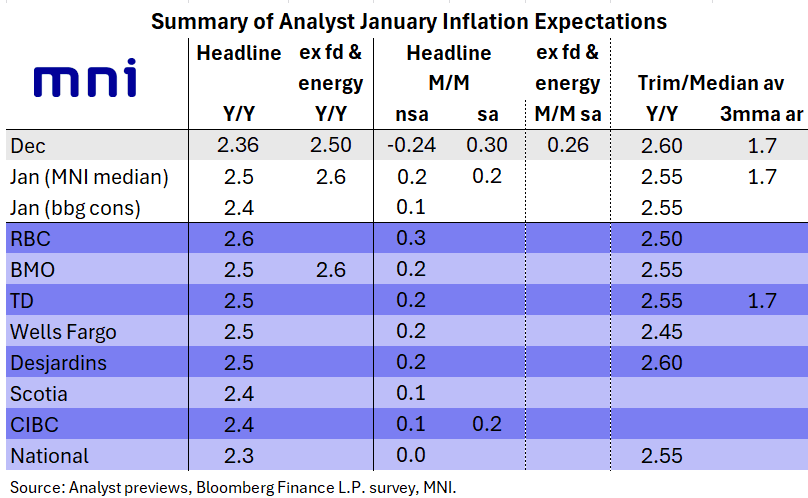

CANADA: Jan CPI Preview: Underlying Pressures Expected To Continue Abating (1/3)

Underlying inflation is expected to remain on a downward trend in January's CPI report (Tuesday Feb 17, 830ET), though headline will see some upward pressures largely as a result of base effects. An as-expected January report won't do much to dampen speculation over a BOC rate hike by near-end, but by the same token it won't take a cut off the table either.

- Overall MNI's analyst median is for a 2.5% Y/Y headline CPI rate (Bloomberg consensus 2.4%), which would represent a modest uptick from the 2.36% reading in December. More closely eyed will be the trim/median average which printed 2.60% Y/Y in December, but is expected to dip to 2.55% in January (largely on account of a dip in the median gauge).

- Put another way, the dynamics of the January report are largely expected to resemble those of the prior release in December. To recap: on the surface, headline/core prices were on the warmer side in December. Sequentially, headline CPI picked up 0.30% M/M on a seasonally-adjusted basis, after 0.24%, while the core measure of 0.26% was double November's 0.13%. And Y/Y, headline rose to a 3-month high 2.4% after 2.2% prior (2.2% expected), withgbpeur ex-food/energy picking up a tenth to 2.5% (2.3-2.4% expected).

- However, the main culprit was higher food prices, which soared 6.2% Y/Y largely to a base effect from the prior year's sales tax holiday; similarly, services inflation accelerated to an 8-month high 3.3% Y/Y but this was related in part to the restaurant base effect. Ex-food CPI dipped to 1.6% after 1.9%, and In some large categories there was little to no aggregate inflation. Sequential trim / median inflation decelerated to the weakest since early 2024, to 0.09% M/M / 0.05% respectively. The Y/Y readings fell to 2.7% trim / 2.5% median for an average 2.60% - a 12-month low.

- Summing up the disinflationary progress beneath the surface in December was MNI's underlying CPI composite (unweighted average of CPI-trim, CPI-median, CPIxFE and CPIX) falling to 2.6% Y/Y from 2.8%, marking a 9-month low and off the Sept/Oct highs of 2.9%. At 2.1% on a 3-month moving average, this is the closest the measure has been to 3% since September 2024, with momentum clearly converging on that level.

- The BOC's January meeting deliberations shows that this was Governing Council's general take: "members agreed that CPI inflation was evolving as expected. Recent data had pushed up the headline number to 2.4%, largely due to base-year effects from last year’s GST/HST holiday and higher inflation in food prices" but "The Bank’s preferred measures of core inflation had also eased from 3% in October to around 2½% in December. Three- and six-month measures of CPI-median and CPI-trim were now close to or below 2%, which members noted was a sign of continued easing in core inflation."

- Indeed a figure close to expectations for trim/median would keep the 2.5% projection for Q1 in the January projections on track.

CANADA: Jan CPI Preview: Higher Food Prices To Offset Another Energy Drop (2/3)

The table in the image below shows the range of expectations for January's inflation report. Around the 2.5% Y/Y headline median is a range of 2.3% (National) to 2.6% (RBC), while trim/median average expectations range from 2.45% (Wells Fargo) to 2.60% (Desjardins) with an overall median of 2.55%.

- The main dynamic driving headline Y/Y inflation in January is the boost from base effects, following the previous year's temporary GST/HST sales tax holiday. This is seen continuing to boost food prices (6.2% Y/Y in December), both for groceries (5.0% prior) and restaurants.

- Going the other way, energy prices (-8.8% Y/Y) will remain firmly negative on a Y/Y basis as the base effect from last April's removal of the consumer carbon tax continues to play a deflationary role. However at 6% of the CPI basket vs 16% for food, the latter will have the greater impact.

- Shelter prices, which are almost 1/3 of the CPI basket, remain on a secular downtrend but further disinflationary impetus may be elusive after the 2.1% Y/Y reading in December marked the lowest since early 2021.

- In a similar vein, continued disinflationary impetus in durable goods prices would be surprising after December's 1.9% Y/Y for the lowest since April.

CANADA: Jan CPI Preview: Analysts Focused On Base Effects (3/3)

Some analyst commentary on what to expect in the January inflation report:

- CIBC: "The various CPI measures should point to a 12-month underlying inflation rate still in the 2½% range, not nearly far enough above target to bring on any discussion of a rate hike given all the uncertainties surrounding economic growth ahead. ..While gasoline prices were broadly flat on the month, food prices likely added to inflation once again... On an annual basis measures of core inflation should continue to ease, driven in large part by a softening in shelter inflation...Measures of underlying inflation are easing closer to 2%, and headline inflation could, temporarily, dip slightly below that mark in the coming months as last year’s GST cut falls out of the annual comparison. However, inflation isn’t on its own slow enough to justify further rate cuts, and we continue to see no change in interest rates this year."

- Desjardins: The uptick in Y/Y headline inflation to 2.5% reflects "continued upward pressures from base effects tied to last year’s GST/HST holiday. Falling energy prices should partially offset an anticipated further increase in food prices. Given these forecasts, we expect the Bank of Canada’s preferred core inflation measures held steady at 2.6% on a 12‑month basis, with three‑month annualized core measures also probably remaining below 2% for a second consecutive month. Overall, inflation continues to be muted enough for the Bank of Canada to focus squarely on supporting growth should any negative shocks hit the economy."

- National: Behind the expected downtick to 2.3% Y/Y in headline :"The slight increase in gasoline prices during the month was probably not enough to move the needle, and the headline index likely remained unchanged (M/M)".

- RBC: The 2.6% Y/Y headline inflation report is "largely due to tax-related distortions — the prior year’s GST/HST holiday was not repeated this year – alongside still elevated grocery price growth. Food price growth could spike above 7%, driven by rising restaurant costs compared to tax-exempt levels a year ago. But, grocery store price growth also likely remained high after hitting 5% in November. Energy prices, meanwhile, are tracking 11% below a year ago with gasoline down 17%—roughly half attributable to the removal of the carbon tax. The BoC has limited control over global commodity trends affecting energy and food prices. The central bank will continue monitoring broader underlying price growth measures more closely. Median and trim CPI measures ... have been gradually edging lower—but remain above the 2% target."

- Wells Fargo: Base effects are seen "peaking" in January with a 2.5% Y/Y headline reading. "Base effects reflect the lowering of prices between December 2024 and February 2025 because of the temporary GST/HST holiday...The temporary rise in year-over-year headline inflation is likely to keep the market and consensus baseline view for an on hold Bank of Canada (BoC) intact near-term. We believe these base effects are worth about 0.6-0.8 percentage points and imply a substantial stepdown in inflation as early as the February report....We believe headline inflation is likely to step down to below 2% as soon the February report (1.8% per our nowcast). As such, the macro narrative is likely to shift from the noise of elevated headline inflation to cooling underlying core inflation. This, combined with sub-trend growth, economic slack and downside risks to growth from continued trade uncertainty with the US, we see greater room for the BoC to cut rates than hike."

CAD: CPI Data Tuesday, Underlying Pressures Expected To Continue Abating

- A positive session for USDCAD on Monday would mark a fourth consecutive day of gains for the pair. Despite this, spot remains within last Monday’s range as the recent greenback decline consolidates overall, keeping a bearish condition for USDCAD intact.

- Sights remain on key support at 1.3482, the Jan 30 low. A clear break of this level would confirm a resumption of the medium-term downtrend. Key short-term resistance is unchanged at 1.3725, the Feb 2 high. A move through this hurdle would suggest scope for a stronger short-term recovery.

- The focus turns to tomorrow’s CPI report, where underlying inflation is expected to remain on a downward trend in January, though headline will see some upward pressures largely as a result of base effects.

- An as-expected January report won't do much to dampen speculation over a BOC rate hike by year-end, but by the same token it won't take a cut off the table either. Overall MNI's analyst median is for a 2.5% Y/Y headline CPI rate (Bloomberg consensus 2.4%), which would represent a modest uptick from the 2.36% reading in December.

- Some analyst commentary on what to expect in the January inflation report can be found here: https://mni.marketnews.com/4bYxJFU

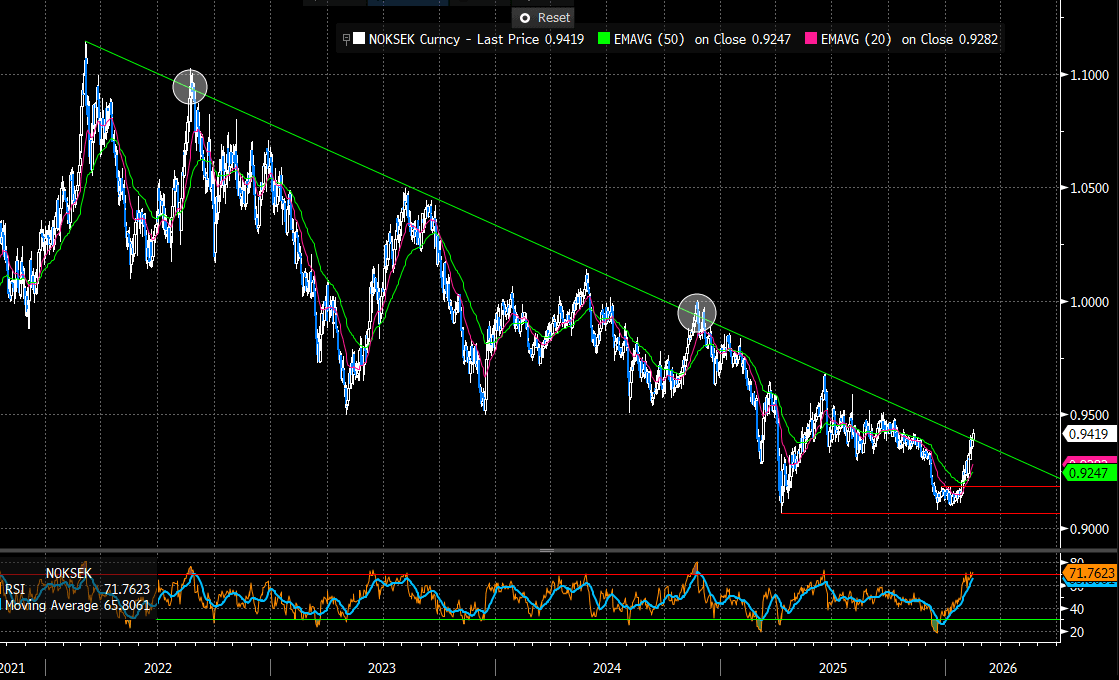

SCANDIS: Interaction With Trendline Resistance Is Key For NOKSEK

NOKSEK is off session highs but remains up 0.38% today at 0.9420. The cross has pierced trendline resistance drawn from the March 2022 high. A clear break of this trendline would reinforce bullish conditions, but we caution that it has failed to do so on a few occasions over the past three years (e.g. August 2022, November 2024). Next resistance levels to watch are around 0.9450 and 0.9500.

- Spot has narrowed the gap to our simple fair value estimate based on 2-year nominal rate differentials and an oil/gas composite proxy (currently at ~0.95).

- Several analysts made hawkish revision to their Norges Bank projections last week following the higher-than-expected January CPI-ATE reading. SEB have followed suit, delaying their forecast for the next cut from June till December (followed by another cut in March to a terminal of 3.50%). Danske Bank meanwhile have pushed their June cut call to September (followed by cuts in December and March to a terminal of 3.25%)

- There was little reaction to this morning’s Swedish LFS data, with the pullback in the volatile unemployment rate fully driven by participation changes.

- The remainder of this week’s Scandi calendar is light until Swedish final January inflation on Friday.

Figure 1: NOKSEK Since 2022 (Source: Bloomberg Finance L.P)

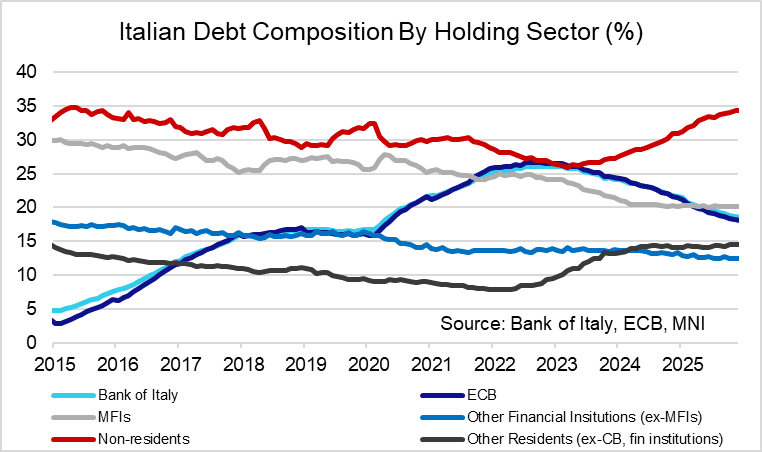

EGBS: Non-resident Demand Has Been A Key Source Of BTP Outperformance

Increased demand from non-resident investors has been a key driver of BTP/Bund spread tightening in recent years. A combination of easier ECB policy, lower EUR rates vol, buoyant risk sentiment and an improved domestic fiscal outlook (the latter particularly in the context of Germany’s recent expansionary plans) has supported this demand.

- However, the 10-year BTP/Bund spread has struggled to consolidate below the 60bp level in recent weeks. While current levels are potentially still attractive from a carry perspective, further material spread narrowing may require evidence of continued domestic fiscal consolidation and an easing of concerns around AI-related equity risks.

- Non-resident demand or Italian debt has been solid since 2023, with the sector absorbing most of the supply made available from a reduced central bank footprint. The February 3 15-year BTP syndication saw non-residents allotted 83.7% of the E14bln issued (36% to UK investors, 10.5% to Nordic investors, 28.5% to other European investors and 25% to other foreign investors).

- Bank of Italy data indicates that the share of Italian debt held by non-residents was 34.3% in November, up from 26.3% at the start of 2023.

- That comes as ECB holdings of Italian debt declined from 26.5% to 18.2% over the same period, as a result of the central bank's quantitative normalisation efforts.

EGBS: /SWAPS/STIR: Most See Higher Bund Yields YE26, ECB Pricing "Fair" (1/2)

Sell-side notes that we have seen generally continue to point towards higher Bund yields come year-end despite last week’s rally, with ongoing focus on the German fiscal expansion, albeit with short-term risks surrounding slower seasonal supply noted. EGB spread positioning views also centre on the German fiscal expansion idea. Most desks deem the short end to be fairly priced/a little too dovish, while the bias in core long end swap spreads remains geared towards further bonds outperformance linked to the Dutch pension reform.

- Bank of America: Stronger H226 German growth and our updated ECB call (no cut in Mar ‘26 but 2 cuts to 1.50% in H127) lead us to lift our 2026 Bund yield forecasts. We now see 10-Year yields at 3.00% by YE26 (from 2.75%), then drifting lower to 2.70% by YE27 (from 2.85%) as softer growth reasserts itself and the ECB delivers cuts. With supply pressures set to ease into March-early April, Bunds can rally-creating an opportunity to establish shorts ahead of fiscal driven growth surprises in H226. Stay in forward starting Euribor/€STR wideners as reserve competition to increase as we do not expect the ECB to slow or stop QT over the foreseeable future.

- Commerzbank: Adjustments to the DFA's issuance plans seem unlikely this year, as the funding plan already accounts for some undershooting and we expect the cash-relevant spending to gradually gain pace. With this, we affirm our view of a gradual widening trend in longer-dated Bund asset swap spreads. While the first major supply wave of the year has been cleared in stride, the slow grind wider in longer-dated spreads to the cheapest levels since October underscores that the record issuance is leaving traces in core duration. As we still expect more Dutch unwinds throughout the year during relief phases, we keep our 30y Bund swap spread forecast for year-end unchanged, which at 35bp is close to current levels. The short to intermediate part of the curve looks set to stay better anchored via well-behaved repo-spreads and solid demand from euro area banks and foreign central banks. We expect a modest cheapening to take hold only during the second half of the year.

- Goldman Sachs: Combined with stability in EUR duration, our model is capturing a build-up in term premium. We think this broadly fits the current macro landscape, front-end rates will likely struggle to shift in the absence of more inflationary data. At the same time, all roads lead to fiscal expansion for Europe, limiting the ability for core duration to rally.

- J.P.Morgan: Given the lack of immediate domestic catalysts we expect 10-Year German yield to range trade near-term in the recent 2.75-2.95% range on Bund Feb-36. However, given our medium-term bullish duration bias we prefer to trade duration from the long-side and therefore will be looking to scale in overweight duration exposures if yields move back to upper-half our expected trading range. We hold a 10s/30s German flattener vs. 10s/30s U.S. Tsy steepener recommendation on attractive valuations and fading Euro supply seasonals. We find the current ECB pricing on the €STR curve to be broadly fair over the next couple of years and thus stay neutral at the front-end. We hold 30s/50s Spain flattener to express our 30Y+ extension theme. The 30s/50s Spain curve flattened few bps in early January and at current levels still close to flat we find flatteners offering quite attractive upside with limited downside.

EGBS: /SWAPS/STIR: Most See Higher Bund Yields YE26, ECB Pricing "Fair" (2/2)

- Morgan Stanley: We keep our portfolio unchanged, waiting for better levels to go long at the long end: hold longs at the front end, 10s30s steepeners and EGB tighteners. Carry-to-risk in derivatives: ratios have improved on longs over the past year. On curves, 10s30s continue to give the best ratio at ~0.6. Carry-to-risk in EGBs: longs and steepeners in cash look better than in spot derivatives. On EGB spreads, 5y and 10y remain the most attractive points. Currently neutral EU 30s but see better value after the recent sell off.

- Natixis: In the short term, risk-off sentiment and concerns about the US tech sector have pushed the Bund out of its recent range. This move is legitimate as a safe haven if concerns about valuations or the sustainability of US tech sector AI investment plans persist. The move is also relatively consistent with the growing easing bias in monetary policy expectations. We maintain our medium-term outlook for a gradual rise in Bund yields on the back the better growth outlook for Germany, we target 3.10% for Bund yields in December 2026. We have a long bias on the Schatz, which should reflect a dovish market pricing bias regarding monetary policy, given that the macro and market environment tilts the risk balance toward a rate cut by the ECB by the end of 2026.

- Societe Generale: We recommend going tactically long Bunds vs swaps, with risk‑off, seasonality, easing term‑repo conditions, and swap flows all aligned and supporting a widening of swap spreads. The remaining pricing of ECB rate hikes remains good carry to pick up, as long as EUR 2–5y is above 22bp. Long‑maturity EUR rates should continue moving more than the front end and the belly. This is only to some extent priced in by the swaption market, implying value in conditional curve trades. The wider EGB space is lacking impetus, with tight spreads and low volatility. As a result, investors are taking advantage of the carry and looking for signals in this low noise market. Seasonals may lead to some periphery underperformance, but we don’t expect it to last long.

- TD Securities: Pay EUR 2y1y. A stronger EURUSD is, in principle, disinflationary for the euro area, which could reinforce expectations of a more accommodative ECB. However, we believe the ECB is less likely to react mechanically if the currency strength reflects hedging flows or capital rotation, rather than tightening in financial conditions. The latter is still not the case. At the same time, domestic resilience, as captured by recent surveys, continue to suggest that ECB policy remains in a good place. We are not suggesting a big move in market pricing of longer term terminal (2.25-2.40%) but more so a fading of the recent received positions via our short trade.

- UBS: EUR spreads have tightened as fiscal risks are converging and political risks are limited in the near-term. Long 30y Italy vs Germany was one of the top trades in our 2026 outlook and we expect further performance seeing the spread tighten to 70bps. Italy is on track to potentially exit the EU’s excessive deficit procedure, whereas Germany is moving to a new fiscal regime. One noteworthy implication is that twin deficits in Germany and Italy are expected to converge for the first time since the early 2000s. We think this convergence is not reflected in the spread, especially as we expect further steepening of the German curve.

| Date | GMT/Local | Impact | Country | Event |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0900/1000 | Foreign Trade | ||

| 17/02/2026 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI | |

| 17/02/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/02/2026 | 1745/1245 | Fed Governor Michael Barr | ||

| 17/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 17/02/2026 | 1930/1430 | San Francisco Fed's Mary Daly |