CANADA: Jan CPI Preview: Underlying Pressures Expected To Continue Abating (1/3)

Underlying inflation is expected to remain on a downward trend in January's CPI report (Tuesday Feb 17, 830ET), though headline will see some upward pressures largely as a result of base effects. An as-expected January report won't do much to dampen speculation over a BOC rate hike by near-end, but by the same token it won't take a cut off the table either.

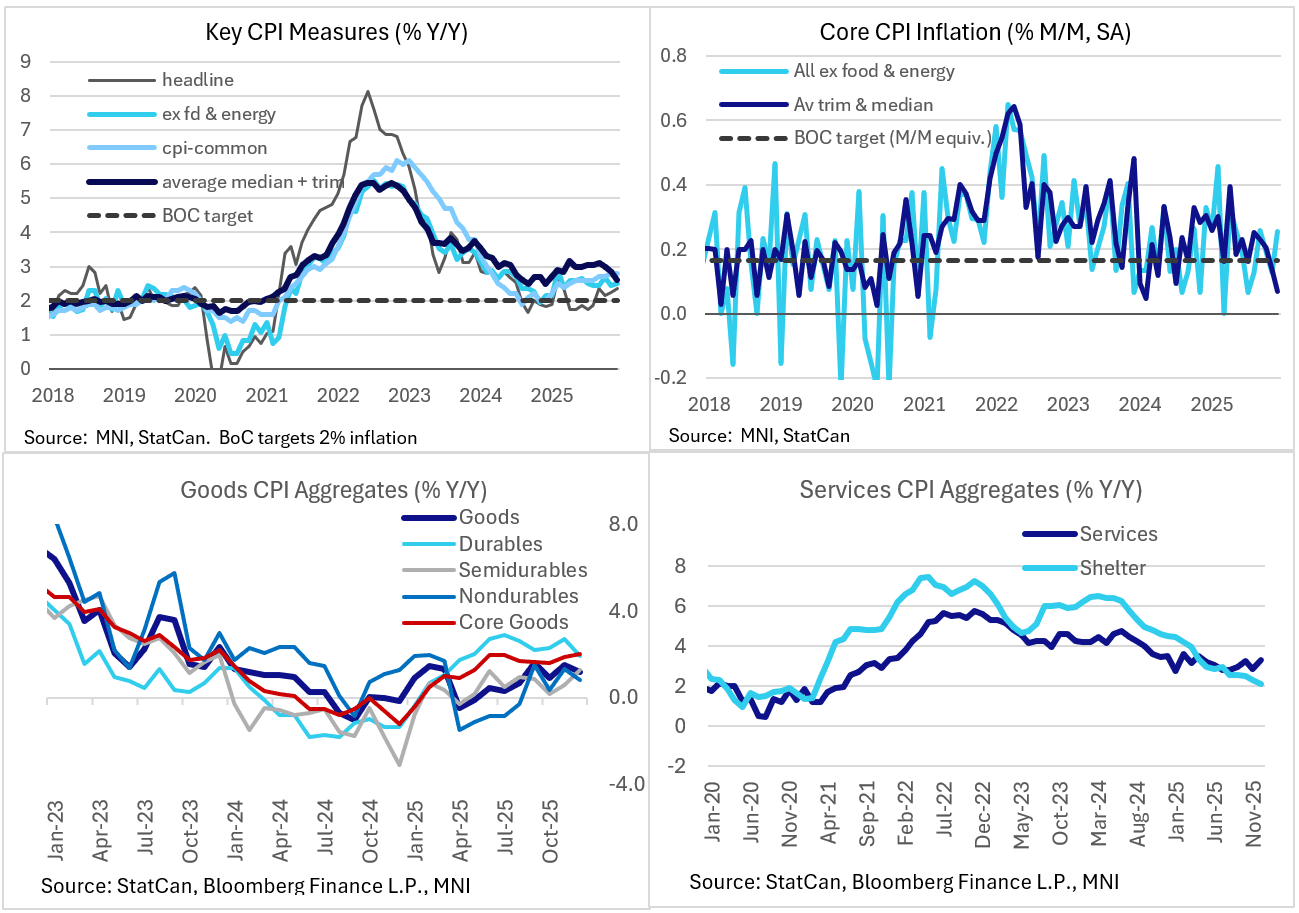

- Overall MNI's analyst median is for a 2.5% Y/Y headline CPI rate (Bloomberg consensus 2.4%), which would represent a modest uptick from the 2.36% reading in December. More closely eyed will be the trim/median average which printed 2.60% Y/Y in December, but is expected to dip to 2.55% in January (largely on account of a dip in the median gauge).

- Put another way, the dynamics of the January report are largely expected to resemble those of the prior release in December. To recap: on the surface, headline/core prices were on the warmer side in December. Sequentially, headline CPI picked up 0.30% M/M on a seasonally-adjusted basis, after 0.24%, while the core measure of 0.26% was double November's 0.13%. And Y/Y, headline rose to a 3-month high 2.4% after 2.2% prior (2.2% expected), with ex-food/energy picking up a tenth to 2.5% (2.3-2.4% expected).

- However, the main culprit was higher food prices, which soared 6.2% Y/Y largely to a base effect from the prior year's sales tax holiday; similarly, services inflation accelerated to an 8-month high 3.3% Y/Y but this was related in part to the restaurant base effect. Ex-food CPI dipped to 1.6% after 1.9%, and In some large categories there was little to no aggregate inflation. Sequential trim / median inflation decelerated to the weakest since early 2024, to 0.09% M/M / 0.05% respectively. The Y/Y readings fell to 2.7% trim / 2.5% median for an average 2.60% - a 12-month low.

- Summing up the disinflationary progress beneath the surface in December was MNI's underlying CPI composite (unweighted average of CPI-trim, CPI-median, CPIxFE and CPIX) falling to 2.6% Y/Y from 2.8%, marking a 9-month low and off the Sept/Oct highs of 2.9%. At 2.1% on a 3-month moving average, this is the closest the measure has been to 3% since September 2024, with momentum clearly converging on that level.

- The BOC's January meeting deliberations shows that this was Governing Council's general take: "members agreed that CPI inflation was evolving as expected. Recent data had pushed up the headline number to 2.4%, largely due to base-year effects from last year’s GST/HST holiday and higher inflation in food prices" but "The Bank’s preferred measures of core inflation had also eased from 3% in October to around 2½% in December. Three- and six-month measures of CPI-median and CPI-trim were now close to or below 2%, which members noted was a sign of continued easing in core inflation."

- Indeed a figure close to expectations for trim/median would keep the 2.5% projection for Q1 in the January projections on track.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late Treasury Roundup: Holding Near Highs, Scotus Kicks Can on Tariffs

- US Treasuries look to finish moderately higher Wednesday, holding a relatively narrow band since midmorning after the Supreme Court opted to not comment on Pre Trump's IEEPA tariff actions for the second time (and no word as to when they may make any comments).

- Some sporadic selling kept a lid on Tsys prices after this morning's PPI MoM came in as estimated, strong core as YoY rises slightly, Retail Sales gained marginally with prior down-revised.

- Our crude proxy for PPI inputs in core PCE shows a modest 0.05pp contribution to M/M inflation in November after one of its strongest in recent years with 0.18pp in October. It sees a return of monthly contributions towards the 0.08pp in Sept (revised up from 0.07pp in the last published report) and 0.05pp back in Aug.

- Treasury futures extended highs late morning - not headline driven but more likely mirroring Bund bid into the London close. Currently, TYH6 trades 112-15 (+6.5) vs 112-18 high, key short-term resistance is unchanged at 112-31, the Dec 18 high. Curves flatter: 2s10s -2.060 at 62.198, 5s30s -0.7 at 107.495.

- On the flipside, a bear threat in Treasuries remains present and for now, short-term gains are considered corrective. Attention is on support at 111-29, the Dec 10 low and bear trigger. A break of it would confirm a continuation of the bear cycle. Note too that a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. Scope is seen for a move towards 111-19 initially, a Fibonacci projection.

- Conviction over the short-term trajectory for the dollar continues to be lacking, amid the plethora of risks surrounding the new Fed Chair and developments regarding Greenland and Iran.

US TSYS: Late SOFR/Treasury Option Roundup: Reposition, Unwinds & Vol Sales

SOFR & Treasury options overnight volumes remained rather modest on net, two-way positioning and a decent amount of vol selling (note TYJ6 111/113.5 strangle seller block below) on the day as underlying futures holding moderate gains/off highs. Projected rate cut pricing gains slightly vs. late Tuesday levels (*): Jan'26 steady at -1.2bp, Mar'26 at -7.1bp (-6.3bp), Apr'26 at -11.7bp (-10.7bp), Jun'26 at -24.4bp (-22.5bp).

- SOFR Options:

- +5,000 SFRU6 96.62/97.12 1x2 call spds, 8.75 ref 96.77

- -12,500 0QJ6/0QG6 96.87 call spds, 5.0

- -20,000 SFRJ6 96.43 puts, 1.75 vs. 96.59 to -.58/0.20%

- -5,000 SFRH6 96.37/96.50 1x2 call spds, 0.0 ref 96.39

- Block, 4,000 SFRU6 96.75/97.12 2x3 call spds, 12.25 net ref 96.76

- Block, 25,000 SFRJ6 96.43/96.50 3,2 put spds, 3.75 net ref 96.58

- 5,000 SFRF6 96.37 straddles ref 96.39

- -10,000 SFRH6 96.43/96.56/96.68/96.81 call condor, 1.75 ref 96.39

- 10,000 0QU6 96.50 puts vs. 97.00/97.50 call spds ref 96.78

- 2,500 0QG6 97.00/97.18 call spds

- 3,500 0QH6 96.68/96.81/96.87/96.93 put condors ref 96.85

- over 5,000 SFRJ6 96.37/96.43 put spds ref

- 3,000 SFRH6 96.25/96.31/96.37 put flys

- over 15,000 SFRJ6 96.43/96.50 3x2 put spds ref 96.59

- Treasury Options:

- Block, +10,000 USH6 111/USJ6 109 put spds, 7

- Block, +10,000 USH6 123/USJ6 121 call spds, 17

- Blocks, -20,546 TYJ6 111/113.5 strangles, 46

- 5,000 TYH6 111.5/113 strangles, 35

- 5,000 TYH6 116 call vs. TYK6 110.5 put ref

- 3,800 TUH6 104.5/104.75 call spds ref 104-09.12

- Block, +6,480 USH6 123 call vs. USJ6 121 call, 17 net Apr over

- Block: +6,210 USH6 111 put vs. USJ6 109 puts, 7 net Apr over

- Block, -10,000 TYH6 113.5 calls, 13 ref 112-11.5

- +10,000 TYG6/TYH6 112 put spds, 19 ref 112-11

- Block, 8,000 TYH6 112.5 straddles, 1-09

- -2,000 TYG6 112.25 calls, 14 ref 112-06.5

- 1,275 FVH6/FVJ6 110 put spds on 2x1 ratio

EURJPY TECHS: Sights Are On The Bull Channel Top

- RES 4: 186.83 Bull channel top drawn from the Feb 28 low

- RES 3: 186.41 2.618 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 2: 185.77 2.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 185.57 Jan 14 High

- PRICE: 184.42 @ 16:14 GMT Jan 14

- SUP 1: 183.51/182.64 20-day EMA / Low Jan 8

- SUP 2: 182.25 Low Dec 19

- SUP 3: 181.74 50-day EMA

- SUP 4: 180.50 Low Dec 8

The trend structure in EURJPY remains bullish, even as prices fade from the weekly top. The cross has this week traded to a fresh cycle high, clearing resistance at 184.92, the Dec 22 high. The move higher confirms a recent bull flag on the daily chart and confirms a resumption of the uptrend. This signals scope for a climb towards 186.83, the top of a bull channel drawn from the Feb 28 low. Key support to watch lies at 181.74, the 50-day EMA.