FOREX: USDJPY Recovers Following Soft Growth Data in Japan

Feb-16 17:44

- The dollar index stands around 0.2% firmer on Monday, with FX market volatility contained by the US Presidents’ Day holiday. The greenback advance has been driven by a 0.55% rally for USDJPY, which has reacted to a softer-than-expected set of GDP data in Japan.

- The data signals that more needs to be done to boost economic growth, a key goal for the Takaichi regime, and renewed fiscal concerns will be driving the latest reversal in fortune for the yen. Short-term USDJPY parameters appear well established; the January lows at 152.10 provide key support, while the post-NFP highs at 154.65 offer the most notable resistance.

- The UK will see a data-heavy week with key inputs from the labour market, inflation and flash PMIs scheduled. For GBPUSD, broader dollar dynamics have been dominating allowing the pair to consolidate between the February 9 and 11 extremes of 1.3587 and 1.3712. On the downside, key S/T support lies at the 50-day EMA, at 1.3527.

- A positive session for USDCAD on Monday would mark a fourth consecutive day of gains for the pair as we approach tomorrow’s CPI report. A bearish condition for USDCAD remains intact, and sights are on key support at 1.3482, the Jan 30 low, just over 1% from current spot levels.

- Elsewhere, market participants also await the RBNZ decision Wednesday, the first with Governor Breman in charge. Despite the latest pullback for NZDUSD, spot remains within 100pips of 0.6120, of which a break would place the pair at the highest point since October 2024. Meanwhile, AUDNZD would be a key beneficiary of any dovish tilt following last week’s extension to 1.1807, the highest level reached dating back to July 2013.

- RBA minutes, UK labour market data and Canada CPI data are highlights tomorrow. China remains out for the lunar new year holiday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US LABOR MARKET: Macro Since Last FOMC: No Sign Of Alarm In Jobless Claims [3/3]

Jan-16 21:25

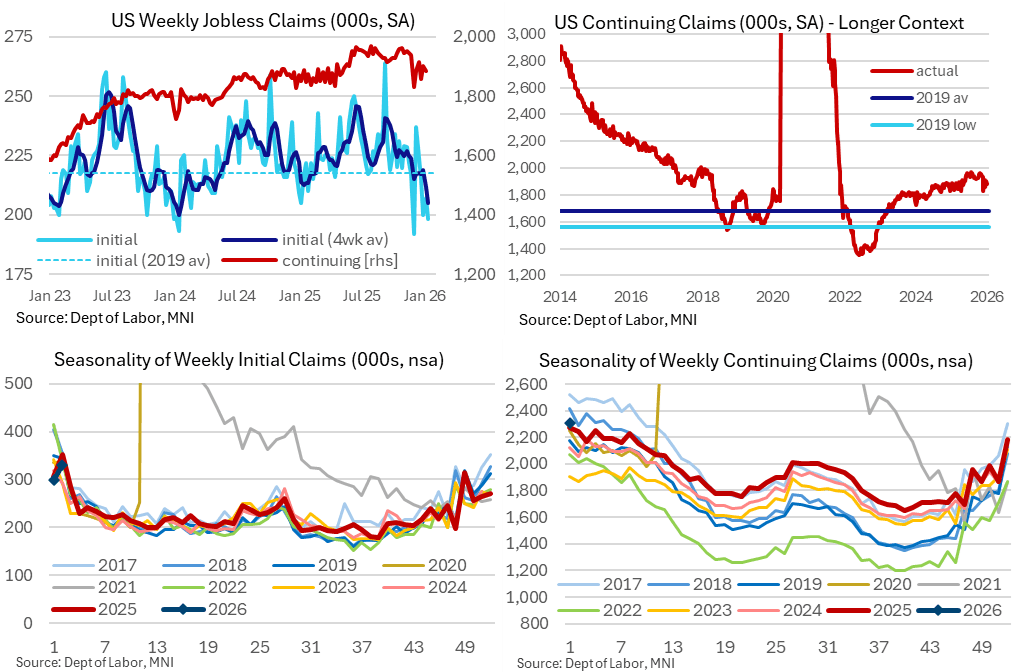

- Away from the top tier BLS labor releases, weekly jobless claims have been of note in recent weeks as initial claims have consistently pushed lower.

- There are concerns over residual seasonality here, which could start to see increases heading into February, but levels are nevertheless particularly low with a four-week average at its lowest since Jan 2024.

- Continuing claims have also held their pulling back from cycle highs seen throughout June-October, suggesting that re-hiring conditions may have cooled when looking at a long-term trend but that conditions have at least improved compared to the summer and fall.

- These claims data clearly point to a labor market in an unusual low fire, low hire state, which appears to give some on the FOMC more concern than others.

US LABOR MARKET: Macro Since Last FOMC: U/E Rate Lower, Hits Median Fcast [2/3]

Jan-16 21:20

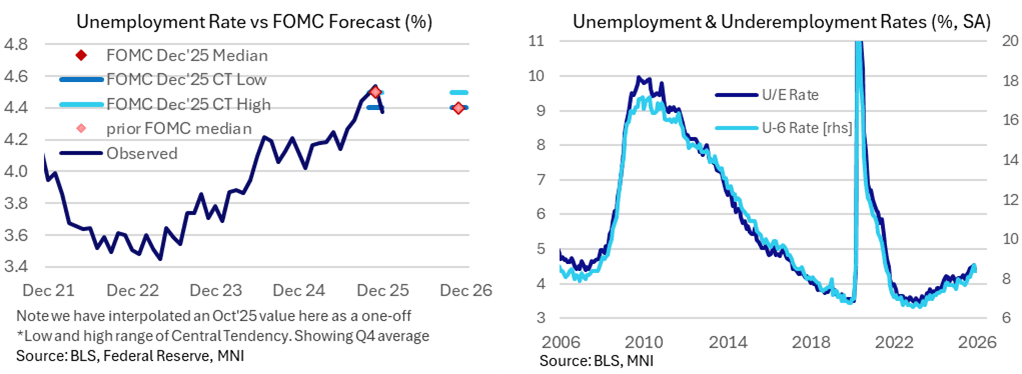

- Looking to the household survey for a better sense of labor market balance, the unemployment rate stood at 4.38% in December to placate fears of further deterioration.

- It more than unwound a push higher to 4.54% in November (revised from 4.56% first reported before annual seasonal adjustment revisions) having been 4.44% in September (unrevised) in the latest update prior to the December FOMC meeting.

- NY Fed Williams had estimated after the delayed release of the November report that it might have been overstated by 0.1pp and Fed Chair Powell had specifically warned of its potential technical distortions ahead of time.

- We’re left with an average unemployment rate of 4.47% in Q4 (using an interpolated value for Oct with no household survey conducted) to match the 4.5% the median FOMC participant forecast in the Dec SEP.

- In doing so, it importantly ruled out a further increase to 4.6-4.7% that seven members had pencilled for what’s an increasingly divided committee. Nevertheless, there has been a clear uptrend in the second half of the year having averaged 4.15% in 1H25.

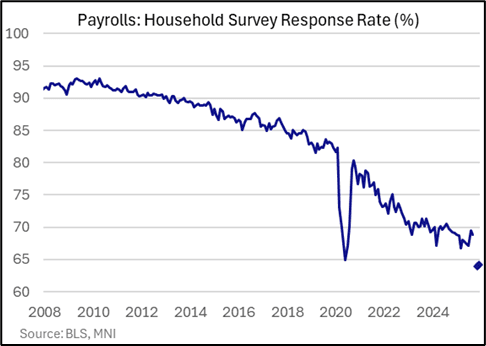

- Data quality concerns are still elevated though, particularly with the household survey response rate barely increasing from November’s record low.

US LABOR MARKET: Macro Since Last FOMC: Payrolls Slowly Rise After Oct Hit [1/3]

Jan-16 21:15

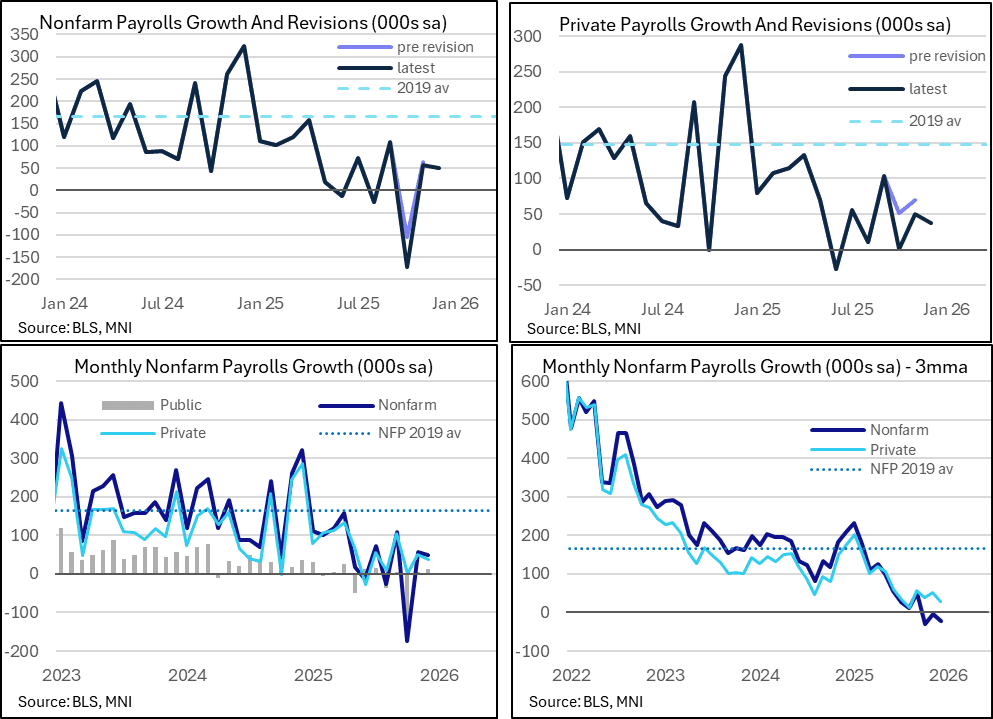

We take an early look at what economic data the FOMC has received since the Dec 9-10 meeting, starting with the labor data where it's had a huge amount to assess along with various distortions to consider.

- Having received three months of data within two BLS nonfarm payrolls reports, the FOMC is left with two latest months of subdued but at least resilient nonfarm payrolls growth of 50k/56k in Dec/Nov. That’s right around estimates of the recent breakeven pace such as the St Louis Fed’s range of 30-80k.

- It does however follow a hugely weak -173k in October, on DOGE-driven federal government deferred resignations showing up with a -174k hit but with the private sector exhibiting weakness as well in October with just a 1k increase.

- For a better sense of underlying jobs growth, private payrolls increased an average 29k over three months to December but strip out the ever-large contribution from the cyclically insensitive health & social assistance sector and private payrolls would have averaged -19k, with only one of the past eight months seeing net job creation.

- We suspect colder than usual weather had a modestly adverse impact on the December data, with the 37k private sector jobs growth potentially understated specifically on that front, but it’s unlikely a big needle mover and an impact that is likely dominated by regular revisions as more data comes in.

- Whilst broadly expected, recall that annual benchmark revisions, due with the January report to be released in February, are also set to show significant downtrend revisions to payrolls, such that payrolls growth is perhaps overstated by about 60k per month.

Trending Top

Mar-27 20:13