EGBS: /SWAPS/STIR: Most See Higher Bund Yields YE26, ECB Pricing "Fair" (1/2)

Sell-side notes that we have seen generally continue to point towards higher Bund yields come year-end despite last week’s rally, with ongoing focus on the German fiscal expansion, albeit with short-term risks surrounding slower seasonal supply noted. EGB spread positioning views also centre on the German fiscal expansion idea. Most desks deem the short end to be fairly priced/a little too dovish, while the bias in core long end swap spreads remains geared towards further bonds outperformance linked to the Dutch pension reform.

- Bank of America: Stronger H226 German growth and our updated ECB call (no cut in Mar ‘26 but 2 cuts to 1.50% in H127) lead us to lift our 2026 Bund yield forecasts. We now see 10-Year yields at 3.00% by YE26 (from 2.75%), then drifting lower to 2.70% by YE27 (from 2.85%) as softer growth reasserts itself and the ECB delivers cuts. With supply pressures set to ease into March-early April, Bunds can rally-creating an opportunity to establish shorts ahead of fiscal driven growth surprises in H226. Stay in forward starting Euribor/€STR wideners as reserve competition to increase as we do not expect the ECB to slow or stop QT over the foreseeable future.

- Commerzbank: Adjustments to the DFA's issuance plans seem unlikely this year, as the funding plan already accounts for some undershooting and we expect the cash-relevant spending to gradually gain pace. With this, we affirm our view of a gradual widening trend in longer-dated Bund asset swap spreads. While the first major supply wave of the year has been cleared in stride, the slow grind wider in longer-dated spreads to the cheapest levels since October underscores that the record issuance is leaving traces in core duration. As we still expect more Dutch unwinds throughout the year during relief phases, we keep our 30y Bund swap spread forecast for year-end unchanged, which at 35bp is close to current levels. The short to intermediate part of the curve looks set to stay better anchored via well-behaved repo-spreads and solid demand from euro area banks and foreign central banks. We expect a modest cheapening to take hold only during the second half of the year.

- Goldman Sachs: Combined with stability in EUR duration, our model is capturing a build-up in term premium. We think this broadly fits the current macro landscape, front-end rates will likely struggle to shift in the absence of more inflationary data. At the same time, all roads lead to fiscal expansion for Europe, limiting the ability for core duration to rally.

- J.P.Morgan: Given the lack of immediate domestic catalysts we expect 10-Year German yield to range trade near-term in the recent 2.75-2.95% range on Bund Feb-36. However, given our medium-term bullish duration bias we prefer to trade duration from the long-side and therefore will be looking to scale in overweight duration exposures if yields move back to upper-half our expected trading range. We hold a 10s/30s German flattener vs. 10s/30s U.S. Tsy steepener recommendation on attractive valuations and fading Euro supply seasonals. We find the current ECB pricing on the €STR curve to be broadly fair over the next couple of years and thus stay neutral at the front-end. We hold 30s/50s Spain flattener to express our 30Y+ extension theme. The 30s/50s Spain curve flattened few bps in early January and at current levels still close to flat we find flatteners offering quite attractive upside with limited downside.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US LABOR MARKET: Macro Since Last FOMC: No Sign Of Alarm In Jobless Claims [3/3]

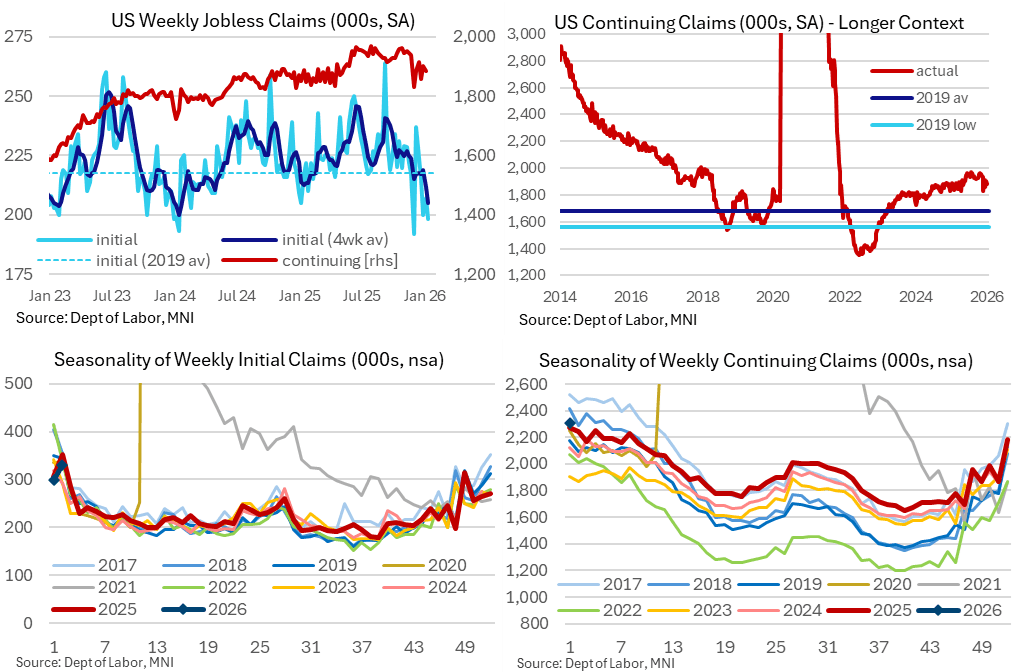

- Away from the top tier BLS labor releases, weekly jobless claims have been of note in recent weeks as initial claims have consistently pushed lower.

- There are concerns over residual seasonality here, which could start to see increases heading into February, but levels are nevertheless particularly low with a four-week average at its lowest since Jan 2024.

- Continuing claims have also held their pulling back from cycle highs seen throughout June-October, suggesting that re-hiring conditions may have cooled when looking at a long-term trend but that conditions have at least improved compared to the summer and fall.

- These claims data clearly point to a labor market in an unusual low fire, low hire state, which appears to give some on the FOMC more concern than others.

US LABOR MARKET: Macro Since Last FOMC: U/E Rate Lower, Hits Median Fcast [2/3]

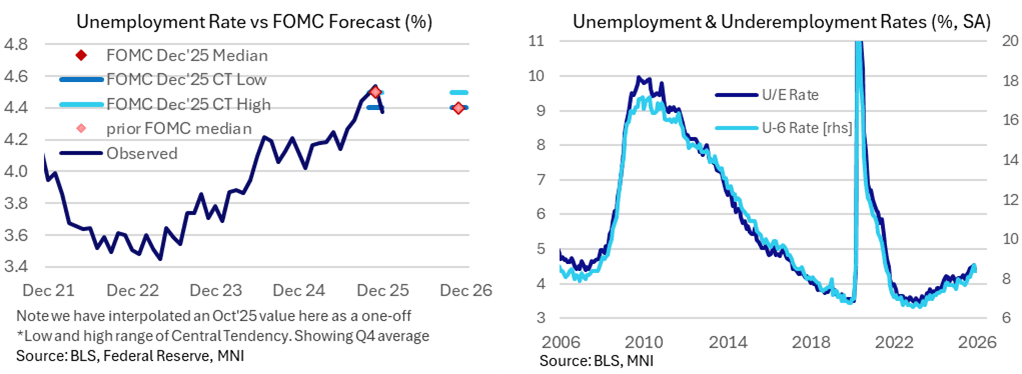

- Looking to the household survey for a better sense of labor market balance, the unemployment rate stood at 4.38% in December to placate fears of further deterioration.

- It more than unwound a push higher to 4.54% in November (revised from 4.56% first reported before annual seasonal adjustment revisions) having been 4.44% in September (unrevised) in the latest update prior to the December FOMC meeting.

- NY Fed Williams had estimated after the delayed release of the November report that it might have been overstated by 0.1pp and Fed Chair Powell had specifically warned of its potential technical distortions ahead of time.

- We’re left with an average unemployment rate of 4.47% in Q4 (using an interpolated value for Oct with no household survey conducted) to match the 4.5% the median FOMC participant forecast in the Dec SEP.

- In doing so, it importantly ruled out a further increase to 4.6-4.7% that seven members had pencilled for what’s an increasingly divided committee. Nevertheless, there has been a clear uptrend in the second half of the year having averaged 4.15% in 1H25.

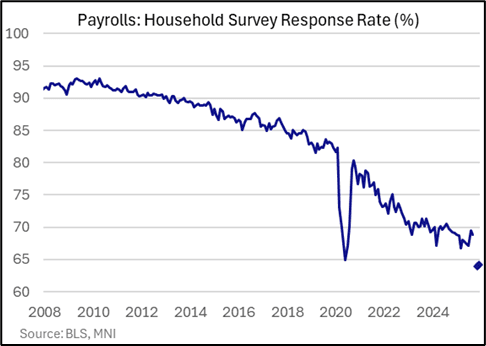

- Data quality concerns are still elevated though, particularly with the household survey response rate barely increasing from November’s record low.

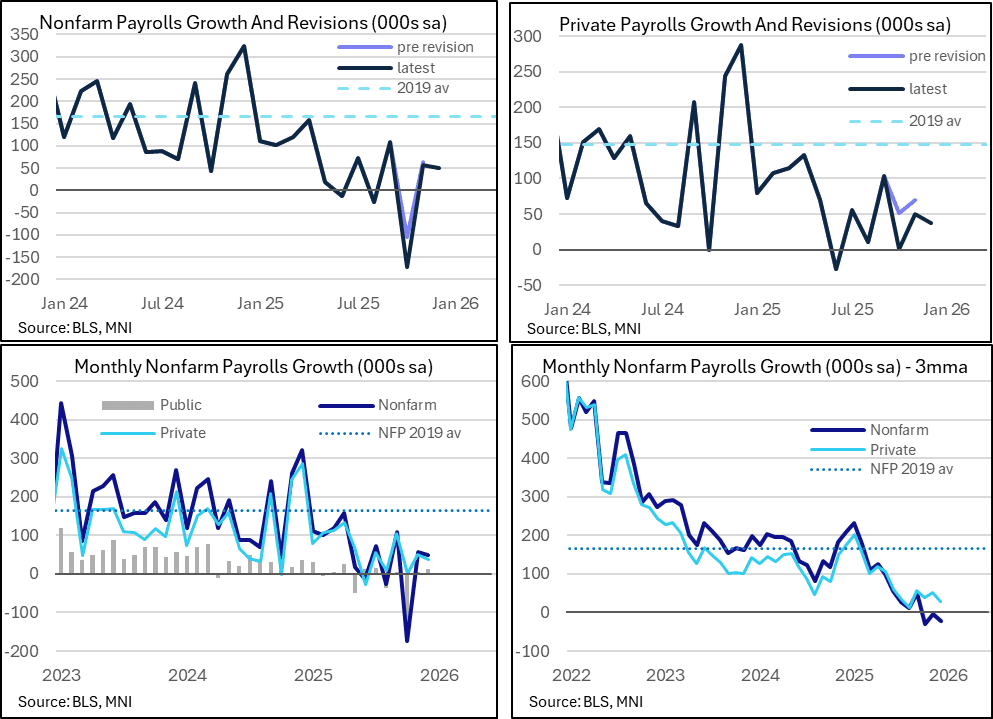

US LABOR MARKET: Macro Since Last FOMC: Payrolls Slowly Rise After Oct Hit [1/3]

We take an early look at what economic data the FOMC has received since the Dec 9-10 meeting, starting with the labor data where it's had a huge amount to assess along with various distortions to consider.

- Having received three months of data within two BLS nonfarm payrolls reports, the FOMC is left with two latest months of subdued but at least resilient nonfarm payrolls growth of 50k/56k in Dec/Nov. That’s right around estimates of the recent breakeven pace such as the St Louis Fed’s range of 30-80k.

- It does however follow a hugely weak -173k in October, on DOGE-driven federal government deferred resignations showing up with a -174k hit but with the private sector exhibiting weakness as well in October with just a 1k increase.

- For a better sense of underlying jobs growth, private payrolls increased an average 29k over three months to December but strip out the ever-large contribution from the cyclically insensitive health & social assistance sector and private payrolls would have averaged -19k, with only one of the past eight months seeing net job creation.

- We suspect colder than usual weather had a modestly adverse impact on the December data, with the 37k private sector jobs growth potentially understated specifically on that front, but it’s unlikely a big needle mover and an impact that is likely dominated by regular revisions as more data comes in.

- Whilst broadly expected, recall that annual benchmark revisions, due with the January report to be released in February, are also set to show significant downtrend revisions to payrolls, such that payrolls growth is perhaps overstated by about 60k per month.