CANADA: Jan CPI Preview: Higher Food Prices To Offset Another Energy Drop (2/3)

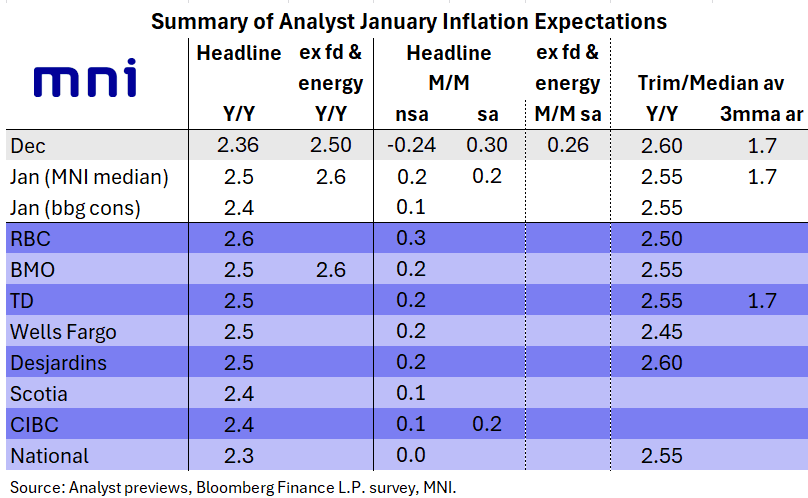

The table in the image below shows the range of expectations for January's inflation report. Around the 2.5% Y/Y headline median is a range of 2.3% (National) to 2.6% (RBC), while trim/median average expectations range from 2.45% (Wells Fargo) to 2.60% (Desjardins) with an overall median of 2.55%.

- The main dynamic driving headline Y/Y inflation in January is the boost from base effects, following the previous year's temporary GST/HST sales tax holiday. This is seen continuing to boost food prices (6.2% Y/Y in December), both for groceries (5.0% prior) and restaurants.

- Going the other way, energy prices (-8.8% Y/Y) will remain firmly negative on a Y/Y basis as the base effect from last April's removal of the consumer carbon tax continues to play a deflationary role. However at 6% of the CPI basket vs 16% for food, the latter will have the greater impact.

- Shelter prices, which are almost 1/3 of the CPI basket, remain on a secular downtrend but further disinflationary impetus may be elusive after the 2.1% Y/Y reading in December marked the lowest since early 2021.

- In a similar vein, continued disinflationary impetus in durable goods prices would be surprising after December's 1.9% Y/Y for the lowest since April.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Monitoring Support

- RES 4: 0.6872 38.2% retracement of the 2021 - 2025 L/T downtrend

- RES 3: 0.6858 1.000 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 2: 0.6795 0.764 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 1: 0.6767 High Jan 7 and the bull trigger

- PRICE: 0.6683 @ 16:16 GMT Jan 14

- SUP 1: 0.6664 Low Jan 9

- SUP 2: 0.6632 50-day EMA

- SUP 3: 0.6593 Low Dec 18

- SUP 4: 0.6553 Low Dec 3

Recent weakness in AUDUSD still appears corrective and has allowed an overbought condition to unwind. Initial firm support around the 20-day EMA, at 0.6681, has been pierced. A clear break of it would expose support at the 50-day EMA, at 0.6632. The area between the two EMAs still represents a key support zone. For bulls, a resumption of the uptrend would open 0.6795 next, a Fibonacci projection.

US TSYS: Late Treasury Roundup: Holding Near Highs, Scotus Kicks Can on Tariffs

- US Treasuries look to finish moderately higher Wednesday, holding a relatively narrow band since midmorning after the Supreme Court opted to not comment on Pre Trump's IEEPA tariff actions for the second time (and no word as to when they may make any comments).

- Some sporadic selling kept a lid on Tsys prices after this morning's PPI MoM came in as estimated, strong core as YoY rises slightly, Retail Sales gained marginally with prior down-revised.

- Our crude proxy for PPI inputs in core PCE shows a modest 0.05pp contribution to M/M inflation in November after one of its strongest in recent years with 0.18pp in October. It sees a return of monthly contributions towards the 0.08pp in Sept (revised up from 0.07pp in the last published report) and 0.05pp back in Aug.

- Treasury futures extended highs late morning - not headline driven but more likely mirroring Bund bid into the London close. Currently, TYH6 trades 112-15 (+6.5) vs 112-18 high, key short-term resistance is unchanged at 112-31, the Dec 18 high. Curves flatter: 2s10s -2.060 at 62.198, 5s30s -0.7 at 107.495.

- On the flipside, a bear threat in Treasuries remains present and for now, short-term gains are considered corrective. Attention is on support at 111-29, the Dec 10 low and bear trigger. A break of it would confirm a continuation of the bear cycle. Note too that a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. Scope is seen for a move towards 111-19 initially, a Fibonacci projection.

- Conviction over the short-term trajectory for the dollar continues to be lacking, amid the plethora of risks surrounding the new Fed Chair and developments regarding Greenland and Iran.

US TSYS: Late SOFR/Treasury Option Roundup: Reposition, Unwinds & Vol Sales

SOFR & Treasury options overnight volumes remained rather modest on net, two-way positioning and a decent amount of vol selling (note TYJ6 111/113.5 strangle seller block below) on the day as underlying futures holding moderate gains/off highs. Projected rate cut pricing gains slightly vs. late Tuesday levels (*): Jan'26 steady at -1.2bp, Mar'26 at -7.1bp (-6.3bp), Apr'26 at -11.7bp (-10.7bp), Jun'26 at -24.4bp (-22.5bp).

- SOFR Options:

- +5,000 SFRU6 96.62/97.12 1x2 call spds, 8.75 ref 96.77

- -12,500 0QJ6/0QG6 96.87 call spds, 5.0

- -20,000 SFRJ6 96.43 puts, 1.75 vs. 96.59 to -.58/0.20%

- -5,000 SFRH6 96.37/96.50 1x2 call spds, 0.0 ref 96.39

- Block, 4,000 SFRU6 96.75/97.12 2x3 call spds, 12.25 net ref 96.76

- Block, 25,000 SFRJ6 96.43/96.50 3,2 put spds, 3.75 net ref 96.58

- 5,000 SFRF6 96.37 straddles ref 96.39

- -10,000 SFRH6 96.43/96.56/96.68/96.81 call condor, 1.75 ref 96.39

- 10,000 0QU6 96.50 puts vs. 97.00/97.50 call spds ref 96.78

- 2,500 0QG6 97.00/97.18 call spds

- 3,500 0QH6 96.68/96.81/96.87/96.93 put condors ref 96.85

- over 5,000 SFRJ6 96.37/96.43 put spds ref

- 3,000 SFRH6 96.25/96.31/96.37 put flys

- over 15,000 SFRJ6 96.43/96.50 3x2 put spds ref 96.59

- Treasury Options:

- Block, +10,000 USH6 111/USJ6 109 put spds, 7

- Block, +10,000 USH6 123/USJ6 121 call spds, 17

- Blocks, -20,546 TYJ6 111/113.5 strangles, 46

- 5,000 TYH6 111.5/113 strangles, 35

- 5,000 TYH6 116 call vs. TYK6 110.5 put ref

- 3,800 TUH6 104.5/104.75 call spds ref 104-09.12

- Block, +6,480 USH6 123 call vs. USJ6 121 call, 17 net Apr over

- Block: +6,210 USH6 111 put vs. USJ6 109 puts, 7 net Apr over

- Block, -10,000 TYH6 113.5 calls, 13 ref 112-11.5

- +10,000 TYG6/TYH6 112 put spds, 19 ref 112-11

- Block, 8,000 TYH6 112.5 straddles, 1-09

- -2,000 TYG6 112.25 calls, 14 ref 112-06.5

- 1,275 FVH6/FVJ6 110 put spds on 2x1 ratio