MNI ASIA OPEN: Consumers Pessimistic on Current Conditions

EXECUTIVE SUMMARY

- MNI FED: Reserves Tick Up Slightly In Latest Week, But Still Near "Ample"

- MNI US DATA: NY Fed Consumer Inflation Expectations Relatively Contained In October

- MNI US DATA: Mixed U.Mich Inflation Expectations But Political Bias Questions Remain

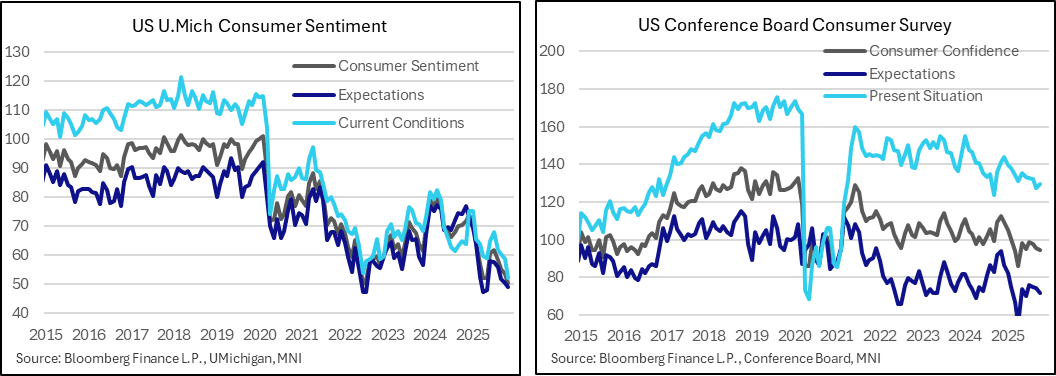

- MNI US DATA: Consumers See Most Pessimistic Current Conditions On Record – U.Mich

US

MNI FED: Financial Stability Report Eyes Term Premia And "Opaque" Financing Risks

A few highlights from the Fed's latest Financial Stability report out today (link):

- In terms of asset valuations, "Prices remained high relative to their historical relationship with fundamentals across a range of markets." The report highlights high leverage in the financial sector: "Vulnerabilities associated with financial leverage remained notable. Over the past few years, hedge funds’ leverage has steadily increased across a broad range of strategies, including those involving Treasury securities, interest rate derivatives, and equities"

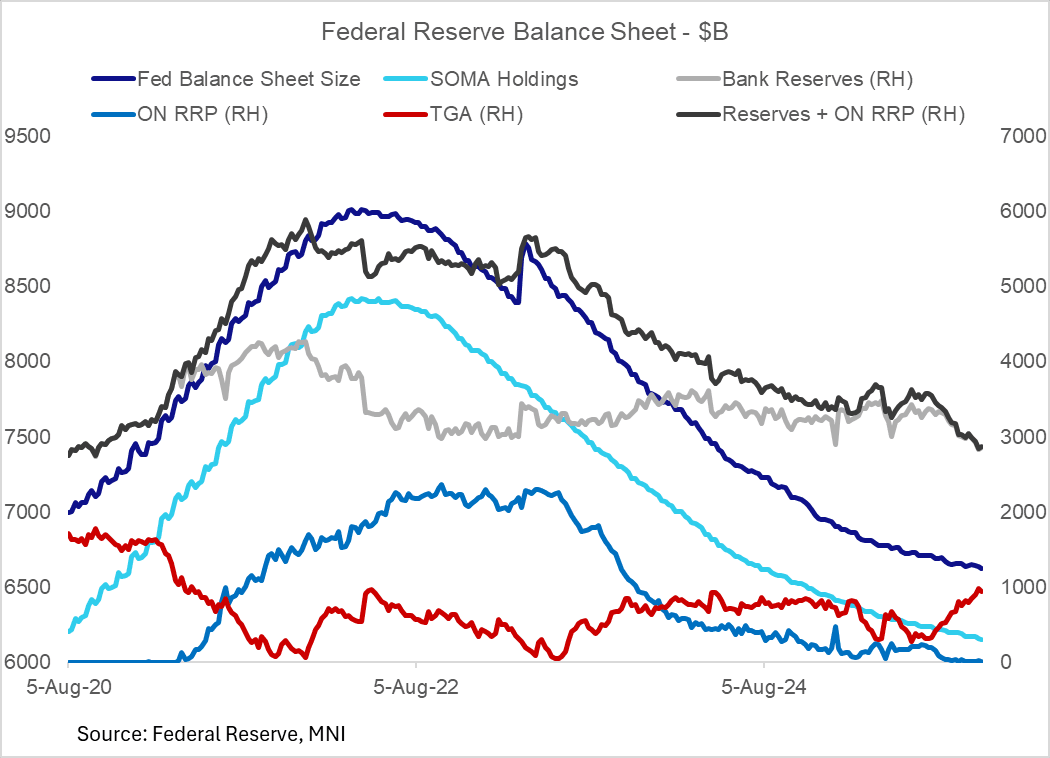

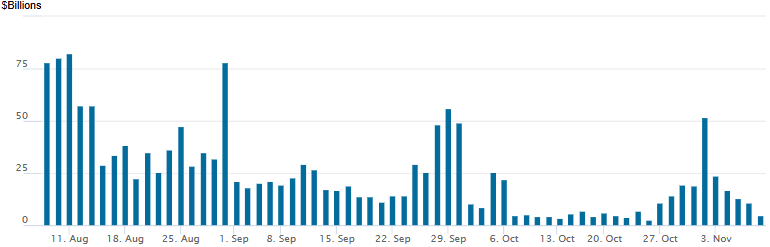

MNI FED: Reserves Tick Up Slightly In Latest Week, But Still Near "Ample"

The Fed's latest H.4.1 release on Nov 5 showed reserves picked up from the prior week's post-2020 lows to $2.85T, up $24B in the latest week but still down $182B over the last month. This of course has been the mirror image of movements in the Treasury General Account which briefly touched $1T though settled Wednesday at $943B (a fall of $41B on the week, but a rise of $149B in a month).

NEWS

MNI US: Inability To Reform ACA Could Prolong Gov Shutdown, Awaiting News On CR Vote

Burgess Everett at Semafor notes a technical issue surrounding Affordable Care Act premium enhanced tax credits, which could impact a potential deal to reopen the US government: "One interesting thing I've heard from people in both parties is that the ACA subsidies probably could only get a straight extension for 2026, any changes (income cap etc.) would come for 2027. That's because the insurance markets are already open," Everett wrote on X.

US TSYS

MNI US TSYS: Risk-Off Sentiment Recedes Late, US Gov Shutdown To Enter Week 6

- Treasuries look to finish mixed Friday - well off midday highs as early risk-off tone moderated. Republicans reject Senate Democrats off on ACA subsidy as the US Govt shutdown looks to enter it's sixth week next week.

- Currently, the Dec'25 10Y contract trades +1.5 at 112-28 after testing resistance above at 113-02, clearance of this level would highlight a potential bullish reversal.

- A short-term bearish threat in Treasuries remains intact. Sights are on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-07. Clearance of these price points would expose a trendline support at 112-00 - the trendline is drawn from the May 22 low.

- The preliminary University of Michigan consumer survey for November saw a sharp decline in consumer sentiment as the perception of current conditions slid to their lowest on record: Consumer sentiment: 50.3 (Bloomberg consensus 53.0) after 53.6 – lowest since Apr 2022; Current conditions: 52.3 (cons 59.0) after 58.6 – lowest on record; Expectations: 49.0 (cons 49.0) after 50.3.

- Fed Vice Chair Jefferson (voter) on wanting to proceed slowly being closer to a neutral level rather than talking on Powell’s “fog”. He does though note a meeting-by-meeting stance being especially prudent with a lack of official data.

- Stocks well off midday lows, Materials, Consumer Staples and Energy sector shares continued to advance in the second half. Late-cycle earnings expected next Monday: Blackstone Secured Lending, Terawulf Inc, Occidental Petroleum, Paramount Skydance, Getty Images Holdings, Rocket Lab Corp and CoreWeave Inc.

OVERNIGHT DATA

MNI BRIEF: China Oct CPI Unexpectedly Rises On Holiday Demand

China’s Consumer Price Index unexpectedly rose 0.2% y/y in October, reversing September's 0.3% fall and beating expectations for a 0.1% drop, as policies kicked in and week-long holidays drove demand, according to data from the National Bureau of Statistics released Sunday. On a monthly basis, CPI rose 0.2%, edging up from September's 0.1% growth. Core CPI, which excludes food and energy, rose 1.2% from September's 1.0%, marking the sixth consecutive month of increase and reaching its highest level since Mar 2024.

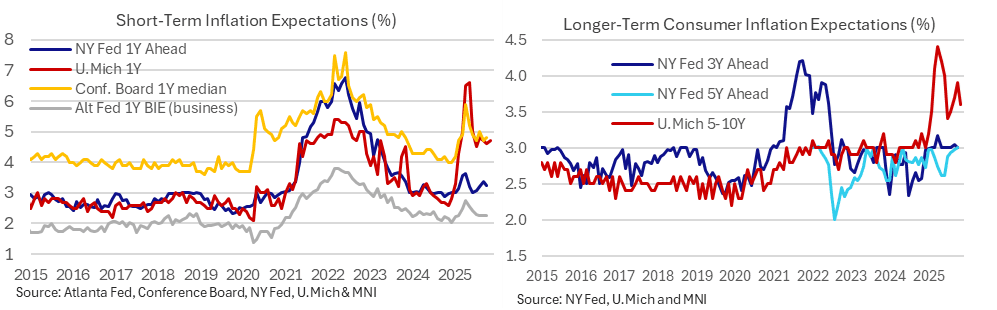

MNI US DATA: NY Fed Consumer Inflation Expectations Relatively Contained In October

The NY Fed consumer survey for October saw 1Y inflation expectations ease back to keep them relatively contained whilst 3Y and 5Y inflation expectations saw little change.

- 1Y inflation expectations: 3.24% in October after 3.38% in Sept, back close to the 3.20% in Aug. 5Y inflation expectations: Essentially unchanged at 3.00% after 2.97% in Sept and 2.93% in Aug.

- A reminder that these metrics within the NY Fed survey have shown much less of a surge in inflation expectations under the Trump administration than has been the case with its U.Mich counterpart.

MNI US DATA: Consumers See Most Pessimistic Current Conditions On Record – U.Mich

The preliminary University of Michigan consumer survey for November saw a sharp decline in consumer sentiment as the perception of current conditions slid to their lowest on record.

- Consumer sentiment: 50.3 (Bloomberg consensus 53.0) after 53.6 – lowest since Apr 2022

- Current conditions: 52.3 (cons 59.0) after 58.6 – lowest on record

- Expectations: 49.0 (cons 49.0) after 50.3

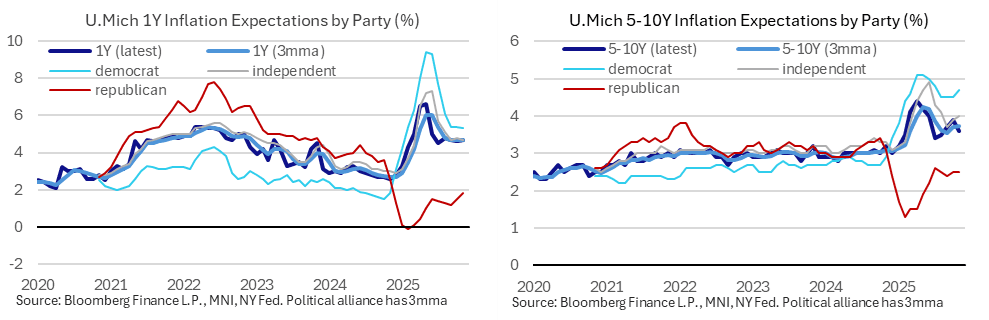

MNI US DATA: Mixed U.Mich Inflation Expectations But Political Bias Questions Remain

U.Mich inflation expectations were mixed in the preliminary November survey although once again appear to be susceptible to people of differing political affiliations answering the survey at different points in the collection period. We suspect that the decline in long-term inflation expectations came to heavier Republican relative representation than will be the case come the full month release.

- 1Y inflation expectations: 4.7% (cons 4.6) after 4.6% in October

- 5-10Y inflation expectations: 3.6% (cons 3.8) after 3.9% in October

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 22.14 points (0.05%) at 46945.55

S&P E-Mini Future down 6.25 points (-0.09%) at 6742.25

Nasdaq down 98.7 points (-0.4%) at 22962.37

US 10-Yr yield is up 0.4 bps at 4.0869%

US Dec 10-Yr futures are up 2/32 at 112-28.5

EURUSD up 0.0019 (0.16%) at 1.1566

USDJPY up 0.32 (0.21%) at 153.39

WTI Crude Oil (front-month) up $0.31 (0.52%) at $59.73

Gold is up $23.6 (0.59%) at $4000.36

European bourses closing levels:

EuroStoxx 50 down 44.65 points (-0.8%) at 5566.53

FTSE 100 down 53.21 points (-0.55%) at 9682.57

German DAX down 164.06 points (-0.69%) at 23569.96

French CAC 40 down 14.59 points (-0.18%) at 7950.18

US TREASURY FUTURES CLOSE

3M10Y +0.241, 22.94 (L: 21.129 / H: 25.531)

2Y10Y +0.78, 53.356 (L: 52.621 / H: 54.12)

2Y30Y +1.762, 114.038 (L: 112.193 / H: 115.207)

5Y30Y +2.05, 101.865 (L: 99.364 / H: 103.059)

Current futures levels:

Dec 2-Yr futures up 0.75/32 at 104-7 (L: 104-05.125 / H: 104-08.375)

Dec 5-Yr futures up 1.5/32 at 109-12.25 (L: 109-08 / H: 109-16.25)

Dec 10-Yr futures up 2/32 at 112-28.5 (L: 112-22 / H: 113-02)

Dec 30-Yr futures down 2/32 at 117-5 (L: 116-26 / H: 117-14)

Dec Ultra futures down 4/32 at 120-27 (L: 120-14 / H: 121-06)

MNI US 10YR FUTURE TECHS: (Z5) Testing Recovery High

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-02 High Nov 5 and a key near-term resistance

- PRICE: 113-01+ @ 16:57 GMT Nov 7

- SUP 1: 112-09+ Low Nov 5

- SUP 2: 112-08+ 38.2% retracement of May - Oct Upleg

- SUP 3: 112-07/06 100-dma / Low Sep 25 and a reversal trigger

- SUP 4: 112-00 Trendline support drawn from the May 22 low

Treasuries again traded stronger through the first half of the session, keeping the near-term recovery high into 113-02 under pressure. Clearance of this level would highlight a potential bullish reversal. Despite intraday recoveries, a short-term bearish threat in Treasuries remains intact. Sights are on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-07. Clearance of these price points would expose a trendline support at 112-00 - the trendline is drawn from the May 22 low.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.005 at 96.250

Mar 26 +0.010 at 96.460

Jun 26 +0.015 at 96.695

Sep 26 +0.010 at 96.845

Red Pack (Dec 26-Sep 27) +0.005 to +0.015

Green Pack (Dec 27-Sep 28) +0.005 to +0.015

Blue Pack (Dec 28-Sep 29) +0.005 to +0.010

Gold Pack (Dec 29-Sep 30) steadysteady0 to +0.005

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.92% (+0.01), volume: $3.156T

- Broad General Collateral Rate (BGCR): 3.89% (+0.01), volume: $1.219T

- Tri-Party General Collateral Rate (TCR): 3.89% (+0.01), volume: $1.189T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.87% (+0.00), volume: $87B

- Daily Overnight Bank Funding Rate: 3.87% (+0.00), volume: $160B

FED Reverse Repo Operation

RRP usage slips to $4.903B with 9 counterparties this afternoon - from $10.754B Thursday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

PIPELINE

Modest issuance Friday after $13.15B priced Thursday, $69.2B/wk:

- 11/07 $1.5B #Atlas Warehouse Lending $750M 3Y +110, $750M 5Y +130

- Date $MM Issuer (Priced *, Launch #)

- 11/06 $6.2B #Global Payments $1.75B 3Y +95, $1.7B 5Y +120, $1B 7Y +135, $1.75B 10Y +150

- 11/06 $2.25B *Brazil $1.5B +7Y 5.75%, $750M 2035 tap 6.2%

- 11/06 $1.75B #Targa Resources $750M +3Y +80, $1B +10Y +132

- 11/06 $1.5B #Equinor $250M 3Y Tap +38, $250M 5Y tap +48, $1B 10Y +73

- 11/06 $700M #Canadian National $300M +5Y +55, $400M 10Y +70

- 11/06 $750M #Eagle Materials 10Y +105

MNI BONDS: EGBs-GILTS CASH CLOSE: Bear Steepening Confirmed For The Week

European yields rose again Friday, capping a bear-steepening move for the week as a whole.

- Core bonds gained strongly in morning trade as global equities hit the weakest levels of the month so far.

- Despite a lack of a US nonfarm payrolls report due to government shutdown, bonds would reverse lower in the middle of the European afternoon session.

- This reversal was not really triggered by any particular macro / headline trigger, but rather order-related selling flows that saw curves bear steepen.

- For the week, both the German (2Y yield +2.2bp, 10Y +3.3bp) and UK (2Y +2.7bp, 10Y +5.7bp) bear steepened, with Gilts underperforming despite what had been perceived as a dovish-vs-expectations BOE meeting.

- Periphery/semi-core EGB spreads widened slightly, mirroring the continued pullback in equities.

- Next week's calendar highlight is UK labour market data, with various other data including German ZEW.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 1.99%, 5-Yr is up 0.9bps at 2.256%, 10-Yr is up 1.6bps at 2.666%, and 30-Yr is up 2.8bps at 3.266%.

- UK: The 2-Yr yield is up 1.2bps at 3.798%, 5-Yr is up 3.1bps at 3.928%, 10-Yr is up 3.3bps at 4.466%, and 30-Yr is up 3.2bps at 5.25%.

- Italian BTP spread up 0.5bps at 76.7bps / French OAT up 0.3bps at 79.7bps

MNI FOREX: Equity Selloff Has Limited FX Impact, CAD Boosted on Jobs Data

- Further volatility and bearish sentiment for the major equity benchmarks on Friday had a relatively limited impact in the currency space. Underperformance of the US indices and another 1.6% move in the Nasdaq weighed on the dollar index, with the likes of EUR and GBP outperforming on the session.

- In general, the broader dollar rally that had been playing out following the FOMC showed signs of fatigue this week. The DXY reaching its initial objective at the August highs (~100.25) may have also contributed to the reversal lower across Thursday and Friday trade. Amid this dynamic, EURUSD is now roughly 100 pips above the recent pullback lows, trading around 1.1580 as we approach the weekend close.

- Additionally, and following the dovish hold by the Bank of England on Thursday, sterling has traded in a resilient manner with cable rising back above the prior breakdown level of 1.3140 to trade around 1.3175 at typing. Positioning dynamics has likely been assisting the bounce, while the move higher is allowing an oversold trend condition to unwind.

- CAD has been one of the best performers across the G10, following a stellar employment report released today. USDCAD sits 0.45% lower on the session, notably falling back below the prior breakout level at 1.4080. Furthermore, the latest price action sees USDCAD edge further away from previously touted resistance, the top of a bull channel, drawn from the July 23 low. Having highlighted this area as a key obstacle to further USDCAD strength, price has subsequently respected the line twice, bolstering the potential of a short-term bearish signal.

- China PPI/CPI data crosses over the weekend, before the focus turns to UK labour market data on Tuesday.

MONDAY DATA CALENDAR

| Date | ET | Impact | Period | Release | Prior | Consensus | |

| 10/11/2025 | 1130 | * | 14-Nov | Bid to Cover Ratio | -- | -- | |

| 10/11/2025 | 1130 | * | 14-Nov | Bid to Cover Ratio | -- | -- | |

| 10/11/2025 | 1200 | *** | 15/16 | Corn Ending Stocks current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Corn Production current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Corn yield per acre current year | -- | -- | |

| 10/11/2025 | 1200 | *** | 15/16 | Cotton Ending Stocks current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Cotton Production current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Soybeans - Ending Stocks current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Soybeans Production current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Soybeans yield per acre current year | -- | -- | |

| 10/11/2025 | 1200 | *** | 15/16 | Wheat - Ending Stocks current year | -- | -- | (m) |

| 10/11/2025 | 1200 | *** | 15/16 | Wheat Production current year | -- | -- | (m) |

| 10/11/2025 | 1300 | *** | Nov | Bid to Cover Ratio | -- | -- |