MNI ASIA MARKETS ANALYSIS:Rate Hike Pricing Jumps on Weak Data

HIGHLIGHTS

- Treasuries gapped higher after a flurry of weaker data early Friday: lower than expected jobs gain & prior sharply down-revised, softer ISMs & UofM sentiment while 1Y inflation expectations climbs slightly.

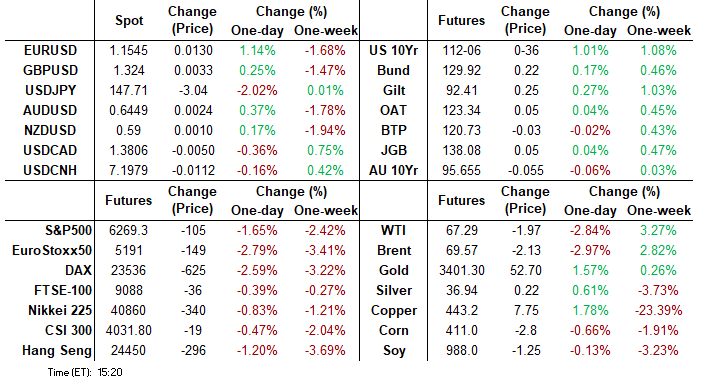

- Tsy curves bull steepened (2s10s +9.886 at 51.372) while projected rate cut pricing jumped vs. pre-data (*) levels: Sep'25 at -20.9bp (-10.8bp), Oct'25 at -38.4bp (-19.9bp), Dec'25 at -57.7bp (-34.4bp), Jan'26 at -68.9bp (-42.4bp).

- Tsy Sep'25 10Y futures climbed to July 1 highs (TYU5 +1-05.5 to 112-07.5), stocks tumbled off Wednesday's record highs (SPX eminis & Nasdaq), while US Greenback retreated from late May highs.

- Headline risk at least partially discounted: Pre Trump said to deploy two nuclear submarines due to provocative statements of the Former President of Russia, Dmitry Medvedev.

- Trump to fire "Biden Appointee, Dr. Erika McEntarfer, the Commissioner of Labor Statistics" for today's soft employment data.

US TSYS

MNI US TSYS: Tsys Gap Higher on Weak Jobs Data, Rate Cut Pricing Surges

- Treasury futures gapped higher after lower than expected jobs gain for July, June gains sharply down-revised, while unemployment rate held steady.

- Nonfarm payrolls growth was weaker than expected in July at 73k (cons 104k) after huge downward revisions in both June (-133k to just 14k) and May (-125k to 19k). The downward revisions came from a combination of large shifts in both private and public payrolls, equally spread over both May and June.

- Treasury futures extending highs (TYU5 +1-03 112-05) after lower than expected ISMs, lower UofM sentiment while 1Y inflation expectations climbs slightly. The ISM manufacturing survey was weaker than expected in July at 48.0 (cons 49.8) after 49.0 in June, falling to its lowest since October. Prices paid saw the largest downside surprise, falling to 64.8 (cons 70.0 from 8 responses vs 60 for the headline) from 69.7 in June for its lowest since February.

- Tsy Sep'25 10Y futures continued to extend highs in late trade (112-07.5), next level in focus at 112-12+ High Jul 1 and a bull trigger.

- Headline risk at least partially discounted: Pre Trump said to deploy two nuclear submarines due to provocative statements of the Former President of Russia, Dmitry Medvedev. Trump to fire "Biden Appointee, Dr. Erika McEntarfer, the Commissioner of Labor Statistics" for today's soft employment data.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (+0.07), volume: $2.933T

- Broad General Collateral Rate (BGCR): 4.36% (+0.05), volume: $1.134T

- Tri-Party General Collateral Rate (TCR): 4.36% (+0.05), volume: $1.111T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $208B

FED Reverse Repo Operation

RRP usage falls to $97.426B (lowest levels since April 25) this afternoon from $214.445B yesterday, total number of counterparties at falls to 21 from 52. Lowest usage of the year at $54.772B on Wednesday, April 16 -- in turn the lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Heavy SOFR & Treasury option volumes reported Friday, mixed flow with buyers of low delta calls and puts on the day. Underlying futures gapping higher after lower than expected jobs gain, prior sharply down-revised, unemployment rate steady. Projected rate cut pricing jumped vs. pre-data (*) levels: Sep'25 at -20.9bp (-10.8bp), Oct'25 at -38.4bp (-19.9bp), Dec'25 at -58.3bp (-34.4bp), Jan'26 at -69.4bp (-42.4bp).

SOFR Options:

+90,000 0QZ5 98.37/98.50 call spds, 0.5

Block, 6,041 SFRZ5 96.50/96.75 call spds 4.25 vs. 96.26/0.12%

Block, 5,000 SFRU5 96.12/96.18 call spds, 0.75

+20,000 SFRZ5 95.81 puts, 2.5 ref 96.25

+12,000 SFRU5 95.68/95.75 put spds, 1.25 ref 95.925

+7,000 SFRZ5 95.75 puts, 1.5

+50,000 SFRV5 96.37/96.62 call spds, 5.0 ref 96.24

+20,000 SFRU5 95.68/95.75/95.81 put flys 0.75-0.62 ref 95.94

Block: 15,000 SFRU5 96.25/96.75 1x2 call spds, 0.25 net ref 95.93

-40,000 SFRU5 95.81 puts 2.75-2.5 ref 95.925

+3,000 SFRU5 96.12/96.25/96.37 call flys, 0.75 ref 95.93

-15,000 SFRZ5 96.43/96.75 1x2 call spds 0.5-0.25 ref 96.185

1,500 SFRZ5 95.68 puts, 2.75 ref 96.175, total volume over 12,200

Block, 5,000 0QZ5 97.00/97.37 call spds, 10.0 ref 96.89

1,750 SFRU5 95.87/95.93/96.00 call flys ref 95.77

4,500 SFRZ5 95.75/95.87/96.25/96.37 put condors ref 95.975

over 13,500 SFRQ5 95.87 calls

over 7,700 SFRQ5 95.81 calls

3,000 0QU5 97.00/97.25 call spds ref 96.625

6,000 SFRZ5 95.93/96.00/96.06 call flys ref 95.985

2,000 SFRQ5 95.68/95.75 2x1 put spds ref 95.77

1,800 SFRQ5 95.75/0QQ5 96.43 put spds

1,000 0QU5 96.25/96.50 2x1 put spds ref 96.62

4,000 SFRQ5 95.93 calls, 0.5 ref 95.77

3,250 SFRV5 95.93/0QV5 96.56 put spds

+3,000 SFRZ5 95.56 puts, 0.75 vs. 95.97/0.08%

Treasury Options:

+11,500 TYU5 111/113 strangles, 29-32

Block, 7,500 TYU5 112/TYZ5 113.5 1x2 call spds, 105

-27,500 FVV 107.5/108.5 put spds, 16 vs. 109-02.25/0.20%

9,000 TYX5 107/108.5 put spds ref 111-31.5

+10,000 TYU5 112 straddles, 109-110 appr implied vol 5.30% followed by selling at 112

+50,000 TYU5 111 puts, 12 ref 112-03, total volume over 73.4k, OI 94,639

4,000 TYV5 111.5.112.5 2x1 put spds ref 111-28

4,000 TUU5 104/104.25 call spds ref 103-15.88

2,100 TYU5 110.25 puts, 19 ref 110-28.5

over 8,100 FVU5 109 calls, 7.5 last

over 2,800 FVU5 107.5 puts, 10.5 last

2,800 FVV5 110/111 call spds

2,000 FVZ5 108.25 straddles

1,500 TUU5 103.62/104 call spds ref 103-15.62

+5,000 TYU5 109.5 puts, 9 ref 110-29

4,250 wk1 TY 110 puts, ref 110-29.5 to -30 (exp today)

+13,000 TYU5 110.5 puts, 22 vs. 111-01/0.38%

1,500 TYU5 112/113.5 call spds ref 110-31

Block, -7,000 USU5 116 calls, 27 ref 113-30, total volume over 10,700

MNI FOREX: Accelerated Fed Timeline Undermines Week's USD Rally

- A rush forward in Fed rate cut expectations for September (and through the rest of 2025) followed a soft NFP print Friday, with pricing of a 25bps cut shifting from 10bps to over 20bps very swiftly - dragging the USD with it. The resultant USD downdraft tipped the USD Index well through both the Thursday and Wednesday lows. With payrolls growth weaker than expected in July, another huge downward revision in both June and May, the building pressure on the FOMC to move on rates will build - evident in the dissenting statement issued by Bowman and Waller Friday.

- Volatile markets Friday extended the spell of JPY uncertainty, with the currency rallying sharply against all others. USD/JPY has traded a wide range this week, and the correction lower in USD/JPY tips the price back below the 200-dma. Importantly for bulls, support at 147.63, the 20-day EMA, and 147.63, the 50-day EMA, remain intact.

- Focus in the coming week shifts to the BoE rate decision, at which anything other than a 25bp cut would be a major surprise. Markets are currently pricing a 93% probability of that outcome, and guidance is also widely expected to be unchanged with the "gradual", "restrictive" and "careful" buzzwords all likely to remain.

- Into the decision, a bearish theme in GBPUSD remains intact, despite the Friday bump higher. This week’s sell-off has resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low.

MNI OPTIONS: Expiries for Aug04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1445-50(E1.1bln), $1.1500-10(E1.9bln), $1.1550-65(E3.0bln), $1.1585-00(E1.8bln), $1.1600(E1.1bln)

- USD/JPY: Y148.65-80($549mln), Y149.50($753mln), Y150.00($1.2bln), Y150.50($967mln)

- EUR/JPY: Y173.00(E570mln)

- AUD/USD: $0.6445-65(A$1.4bln)

- NZD/USD: $0.6030-50(N$590mln)

- USD/CAD: C$1.3778-90($783mln)

MNI US STOCKS: Late Equities Roundup: Broadly Weaker But Off Lows

- Stocks remain broadly weaker - but off late session lows despite some citing Pres Trump firing Dr. Erika McEntarfer, the Commissioner of Labor Statistics for jobs numbers Trump says are faked. Stocks fell off this week's record highs (SPX eminis & Nasdaq) after this morning's lower than expected jobs gains for July & large down-revisions to prior June data, as well as soft ISM manufacturing, prices paid & new orders data.

- Currently, the DJIA trades down 492.61 points (-1.12%) at 43632.73, S&P E-Minis down 90.25 points (-1.42%) at 6283.25, Nasdaq down 373.3 points (-1.8%) at 20746.86.

- Consumer Discretionary, Energy, Financial and Materials sectors led a broad swath of decliners in late trade: Eastman Chemical -20.22%, Coinbase Global -16.51%, Ingersoll Rand -11.37%, WW Grainger -11.15%, Amazon -8.57%, Moderna -7.75%, LyondellBasell Industries -6.28%, Fair Isaac -5.81%, Apollo Global Management -5.76%, UnitedHealth Group -5.41%, APA -5.03% and Dow Inc -4.92%.

- On the positive side, Consumer Staples, Estate management and Health Care sectors led gainers: Align Technology +5.41%, DR Horton +4.52%, Kimberly-Clark +4.41%, Paramount Global +4.38%, Builders FirstSource +3.83%, Extra Space Storage +3.80%, Sherwin-Williams +3.73%, AbbVie +3.67% and Howmet Aerospace +3.32%.

- Of note, earnings resume Saturday with Berkshire Hathaway reporting in the morning. On Monday: Wayfair Inc, Waters Corp, ON Semiconductor Corp, Diamondback Energy Inc, ONEOK Inc, Vertex Pharmaceuticals Inc, Coterra Energy Inc, Hims & Hers Health, Palantir Technologies, Williams Cos, Navitas Semiconductor Corp and Axon Enterprise.

MNI EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6269.25 @ 14:47 BST Aug 1

- SUP 1: 6264.25 Intraday low

- SUP 2: 6288.25 Low Jul 17

- SUP 3: 6241.00 Low Jul 16

- SUP 4: 6189.50 50-day EMA

The trend set-up in S&P E-Minis remains bullish and short-term weakness is considered corrective. Note that the contract has traded through support at the 20-day EMA, at 6336.64. The breach signals scope for a deeper retracement and opens the 50-day EMA at 6189.50. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, key short-term resistance and the bull trigger is 6468.50, the Jul 31 high.

COMMODITIES

MNI AMERICAS OIL: WTI crude is under increased pressure after weak US economic data

August 1 - Americas End-of-Day Oil Summary: WTI crude is under increased pressure after a series of weak US data releases today, adding to global economic concerns amid President Trump’s tariffs. Crude remains set for a net weekly rise overall due to Trump’s threats of secondary tariffs on Russia, though has reversed most of the gains seen earlier in the week.

- Nonfarm payrolls growth was weaker than expected at 73k (cons 104k) after huge downward revisions in both June (-133k to just 14k) and May (-125k to 19k).

- Manufacturing data also underperformed estimates, with the US ISM Manufacturing Index at a nine-month low of 48, compared to an estimated 49.5, in a recent release.

- US President Trump slapped steep tariffs on exports from dozens of trading partners, pressing ahead with his plans to reorder the global economy ahead of a Friday trade deal deadline, Reuters reports.

- Any perceived disruption to Russian volumes could propel Brent prices into the $80s or higher, according to JP Morgan.

- WTI Sep futures were down 2.8% at $67.33

- WTI Oct futures were down 2.9% at $66.18

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/08/2025 | 0630/0830 | *** | CPI | |

| 04/08/2025 | 0700/0300 | * | Turkey CPI | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/08/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 05/08/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |