MNI ASIA MARKETS ANALYSIS:Projected Rate Cuts Gain on Weak ADP

HIGHLIGHTS

- Treasury futures gap higher after lower than expected ADP private employ data. Support eased after the Sep ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity.

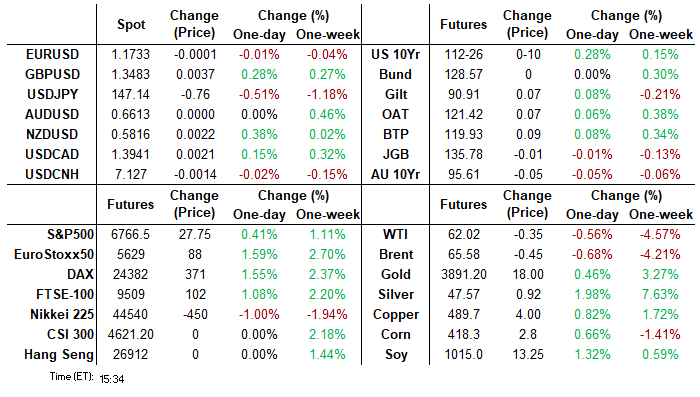

- Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

- Wednesday’s session was dominated by the appreciating Japanese Yen, with several factors contributing to the extension of strength this week.

- Thursday's weekly jobless/continuing claims as well as Factory New Orders will not be released due to the Government shutdown, nor will Friday's employment report.

US TSYS

MNI US TSYS: Taking Delayed/Suspended Data In Stride As Shutdown Gets Underway

- Treasuries look to finish higher - off first half highs after September's ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity. Rates initially gapped higher after much lower than estimated private ADP employment numbers.

- The ADP release for September was weak, showing the biggest private payrolls drop (-32k) since March 2023 and before that, Jun 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. This was a significant miss for private payrolls versus +51k expected.

- ADP was re-benchmarked, however, resulting in a reduction of 43,000 jobs in September compared to pre-benchmarked data. The trend was unchanged; job creation continued to lose momentum across most sectors."

- Underlying futures climbing again after paring back from late morning highs. Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

- Thursday's scheduled economic data largely delayed/suspended due to the shutdown - weekly jobless/continuing claims as well as Factory New Orders will not be released

- In other news: Supreme Court rejects Pres Trump's firing of Fed Gov Cook - until at least an oral argument on the case is heard in January 2026. VP Vance expects federal layoffs to start in the next one to two days.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.24% (+0.11), volume: $3.148T

- Broad General Collateral Rate (BGCR): 4.20% (+0.08), volume: $1.140T

- Tri-Party General Collateral Rate (TCR): 4.20% (+0.08), volume: $1.101T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $155B

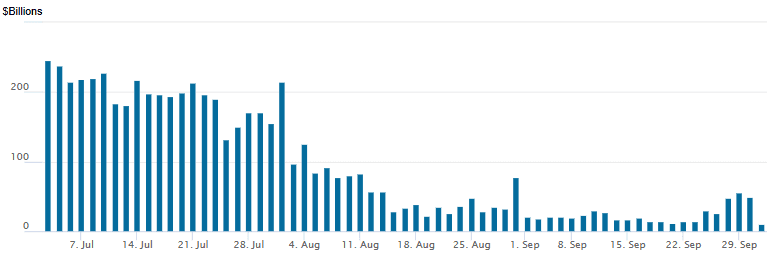

FED Reverse Repo Operation - New Multi Year Low

With October underway - RRP usage falls to the lowest level since early April 2021 this afternoon: $10.179B with 15 counterparties, down from $49.071B Tuesday. Compares to the year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Better SOFR/Treasury call volumes on net Wednesday, some notable put spreads as well (+60k SFRZ5 96.06/96.12 put spd). Underlying futures climbing again after paring back from late morning highs. Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

SOFR Options:

Block, 8,000 0QZ5 97.12/97.50 call spds vs. 3QZ5 96.87/97.25 call spd, 1.5 net - conditional curve steepener

Block, 2,500 0QZ5 97.00/97.25 2x5 call spds, 3.5 net

+10,000 0QZ5 96.25/96.56 2x1 put spds, 1.0 ref 96.955

-6,000 0QZ5 96.37/96.62 2x1 put spds, 1.0 ref 96.955

Block, 5,000 SFRZ5 96.56/96.68 call spds, 1.25 ref 96.355

3,000 SFRZ5 96.25/96.31/96.50/96.56 call condors

5,000 SFRH6 96.37/96.50 2x1 put spds ref 96.56

over 7,400 SFRV5 96.43 calls, ref 96.355

-7,000 SFRZ5 95.93/96.06/96.18/96.31 call condors, 3.25

Block, 6,250 SFRZ5 96.50 calls, 3.75 ref 96.36

over +59,000 SFRZ5 96.06/96.12 put spds, 0.75 ref 96.32/0.05%

3,800 SFRG6 96.75 calls ref 96.515

+2,500 0QX5 96.75 puts, 5.0 vs. 96.92/0.29%

+1,500 SFRZ5 96.25/96.37/96.50 call flys, 4.75 vs. 96.33/0.08%

-1,500 0QZ5 96.87 straddles, 30.5

+2,000 SFRZ5 96.25/96.31/96.50/96.56 call condors, 3.5 vs. 96.325/0.07%

5,200 SFRH6 96.12/96.25/96.50/96.75 call condors

Treasury Options:

6,500 TUZ5 103.87/104.37/104.50/104.87 broken put flys ref 104-09.62

5,700 TYX5 112.5/TYZ5 112 put spds

2,500 TUX5 103.87/104.12 put spd vs. 104.5 calls ref 104-08.75

1,400 TYZ5 113 straddles, 1-47 ref 112-21

2,500 TYX5 112.75 straddles, 1-07 ref 112-21.5

1,200 FVZ5 109.25 straddles, 1-19 ref 109-11.5

over 11,900 FVX5 109 puts, 12.5 ref 112-26

10,000 Wed wkly TU 104.37 calls, .5 (exp today)

over 5,000 TYZ5 113/113.5/114 call trees (total volumes: 113 call over 9.3k, 114 call over 13.7k. Note: yesterday's continuation of low delta call buying: over 186k TYZ5 113 calls, OI +133,664; over 65.3k TYZ5 113.5 calls, OI +22,147; over 108k TYZ5 114 calls, OI +20,739)

+2,000 TYX5 114/TYZ 114.5 call diagonal, 9 net/Dec over

2,000 TYX 114/114.5 call spds ref 112-20

5,500 FVX5 109.75 calls, 11 ref 109-07.25

5,500 TYX5 113 calls, 24 ref 112-16

+1,500 TYZ5 113/114/115 call flys, 8 vs. 112-10/0.05%

-2,000 FVX5 108/109 put spds, 14.5 vs. 109-08.25/0.08%

2,500 Wed wkly 112.75 calls, 2 ref 112-16 (expire today)

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Fade Early Rise

European curves steepened Wednesday, with Gilts slightly outperforming Bunds.

- Yields were higher in early trade, amid uncertainty over the U.S. federal government shutdown that started overnight, and supply weighing somewhat (E5B of 10Y Bund).

- However, the tone was lightened as data proved to be on the dovish side: Italian and Spanish PMIs disappointed, while yields saw the biggest move of the day (to the downside) as US ADP private payrolls unexpectedly contracted. Eurozone HICP came in broadly in line with consensus.

- On the day, the German and UK curves both twist steepened.

- Periphery/semi-core EGB spreads closed a little tighter, with BTPs outperforming.

- Thursday's schedule includes French industrial production and Spanish labor market data, with DMP inflation expectations the highlight of the UK docket. There will also be attention on Swiss inflation, as well as appearances by ECB's Makhlouf, Villeroy and de Guindos.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 2.013%, 5-Yr is down 0.8bps at 2.301%, 10-Yr is up 0.2bps at 2.713%, and 30-Yr is up 1.8bps at 3.298%.

- UK: The 2-Yr yield is down 2bps at 3.965%, 5-Yr is down 1.9bps at 4.117%, 10-Yr is down 0.3bps at 4.696%, and 30-Yr is up 0.5bps at 5.511%.

- Italian BTP spread down 1bps at 81.3bps / French OAT down 0.5bps at 81.7bps

MNI OPTIONS: Flurry Of Sonia Call Spread And Condor Buying Wednesday

Wednesday's Europe rates/bond options flow included:

- RXX5 129/129.50cs, bought for 17 in 5k and 15 in 12k, looking at volumes close to 20k

- ERZ5 98.12/98.00ps 1x2, sold at 6.5 in 7k

- ERH6 98.4375/98.1875/98.125p ladder, bought for 7.75 in 3.5k

- ERH6 98.625/98.375/98.00p ladder, bought for 18.75 in 2.25k

- ERM6 98.25/98.37cs, bought for 2 in 5k.

- ERM6/H6 98.31/98.43cs calendar, bought the June for 1.25 in 5k

- SFIG6 96.30/96.40/96.50/96.60c condor, bought for 1.75 in 4k

- SFIH6 96.35/96.45/96.50/96.55c condor bought for 1.25 in 4k, this was also bought Tuesday for 1 in 4k

- SFIH6 96.60/96.70cs, bought for 0.75 in 8k

- SFIH6 96.30/96.40/96.50/96.60c condor, bought for 1.75 in 2k

- SFIM6 96.60/96.80cs, bought for 3.5 in 11.6k total. Desks note paper bought 9K at the same price on Tuesday

MNI FOREX: JPY Strength Extends Amid US Shutdown, Soft ADP Jobs Data

- Wednesday’s session was dominated by the appreciating Japanese Yen, with several factors contributing to the extension of strength this week. First of all, ongoing concerns surrounding the US Government shutdown and uncertainty regarding upcoming data releases have weighed on USDJPY. Secondly, Tankan survey indicated solid business sentiment and earnings in September, likely to increase the odds of an October BOJ rate hike. Thirdly, weaker-than-expected US ADP employment data prompted a bump lower for US yields, providing an additional yen tailwind.

- USDJPY dipped to a low of 146.59 following the US data, extending the pullback from last week’s highs to 2.25%. Subsequently, the pair has found some support and risen back above the 147 handle as we approach the APAC crossover. Potentially assisting the bounce was comments by US speaker Johnson stating he hopes for a shutdown breakthrough today.

- The New Zealand dollar has also been an outperformer across G10, with NZDUSD notably rising back above the significant 0.5800 pivot point. Kiwi’s outperformance has helped stall the topside momentum of AUDNZD, which registered a fresh 3-year high of 1.1418 yesterday. The cross has moved back to 1.1365 today, and support is not seen until 1.1250, the 20-day EMA.

- The Canadian Dollar is among the worst performers in G10 today as USDCAD holds close to recent highs. A breach of 1.3959 would place the pair at four-month highs. Additionally, a number of CAD crosses are at notable technical levels, with CADJPY breaching an important cluster of support and AUDCAD threatening to break above trendline resistance, drawn from the 2021 highs.

- The Swiss Franc also weakened by 0.25% Wednesday ahead of September CPI data due on Thursday. Despite this, EURCHF remains in consolidation mode, respecting the well established and familiar range between 0.93-0.94.

- US jobless claims would be in focus Thursday ahead of NFP on Friday, although the release of the data remains unlikely owing to the current government shutdown.

MNI FX OPTIONS: Expiries for Oct02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1580(E1.0bln), $1.1615-30(E1.6bln), $1.1675-80(E950mln), $1.1695-00(E1.6bln), $1.1720-25(E964mln), $1.1750(E1.2bln), $1.1785-90(E2.9bln), $1.1850(E760mln), $1.1900(E950mln)

- USD/JPY: Y147.95-00($1.6bln), Y149.50($1.0bln)

- AUD/USD: $0.6600(A$1.9bln)

- USD/CAD: C$1.3900($777mln)

MNI US STOCKS: Late Equities Roundup: New Record High for SPX Eminis

- Stocks continue to rise late Wednesday, ignoring for the moment at least, last night's US government shutdown as SPX eminis quietly rise to a new record high in late trade (6,768.0 +29.25).

- Much lower than expected ADP data contributed to a rise in rate cut projections helped kindle risk appetites in the irst half, as did the shift in focus from the shutdown to fundamentals and the Supreme Court denying Trump from firing Fed Gov Cook until oral argument on the case is heard in January 2026.

- Currently, the DJIA trades up 91.02 points (0.2%) at 46484.55, S&P E-Minis up 27.75 points (0.41%) at 6766.25, Nasdaq up 111.2 points (0.5%) at 22770.28.

- Leading gainers in the second half included Health Care and Utility sector shares, pharmaceuticals leading the former: Eli Lilly +9.08%, Thermo Fisher Scientific +8.74%, Biogen +7.97%, Merck & Co +7.84% and Regeneron Pharmaceuticals +7.71%

- The Utilities sector was buoyed by AES - surging 16.57% higher as wires reported BlackRock's GIP is in advanced talks to purchase the energy company. Follow-through support for other energy companies includes: Constellation Energy +5.33%, Vistra +3.22% and PG&E +3.05%.

- Conversely, Materials and Financial sectors led decliners in the second half. Weighing on Materials: Corteva -8.87%, CF Industries Holdings -2.83%, Vulcan Materials -2.45% and Ecolab -2.01%.

- Meanwhile, Raymond James Financial -3.23%, Robinhood Markets -3.10%, Wells Fargo -3.05%, Northern Trust -2.99% and Charles Schwab-2.95% weighed on the Financials sector.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bulls Remain In The Driver’s Seat

- RES 4: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6800.00 Round number resistance

- RES 2: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6756.75 High Sep 22

- PRICE: 6735.50 @ 1145 ET Oct 1

- SUP 1: 6656.22 20-day EMA

- SUP 2: 6577.25 Low Sep 10

- SUP 3: 6541.51 50-day EMA

- SUP 4: 6481.75 Low Sep 3

A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, initial support to watch lies at the 20-day EMA, at 6656.22. It has been pierced, a clear break of it would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6541.51.

MNI COMMODITIES: Crude Extends Losses, Silver At 14-Year High Amid US Shutdown

- Crude prices are drifting lower after falling sharply this week amid oversupply concerns ahead of OPEC’s Sunday meeting, with conflicting reports on the size of a potential November hike. The US government shutdown is also bearish for prices.

- WTI Nov 25 is down by 0.8% at $61.9/bbl.

- The move leaves WTI 7% below Friday’s highs, with this reversal lower refocussing attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend, opening $57.50, May 30 low.

- Meanwhile, spot gold printed another new record high at $3,895/oz earlier in the session, before unwinding most of the day’s gains to leave the yellow metal broadly unchanged around $3,864 at typing.

- Further gains in gold this week reflect rising haven demand amid concerns surrounding the US government shutdown which started today.

- The trend condition in gold is unchanged, and a bull cycle remains in play. Sights are on $3,909.4 next, a Fibonacci projection. On the downside, support to watch lies at $3,699.4, the 20-day EMA. A pullback would be considered corrective.

- Similarly, silver has rallied by 1.7% to $47.5/oz, taking the precious metal to its highest level since April 2011.

- Trend signals in silver remain bullish, with sights on $47.857 next, a 2.618 projection of the Sep 4 - 16 - 17 price swing, which was tested earlier today. Clearance of this level would pave the way for a climb towards the $49.00 handle.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 02/10/2025 | 0630/0830 | *** | CPI | |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University | ||

| 03/10/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/10/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI |