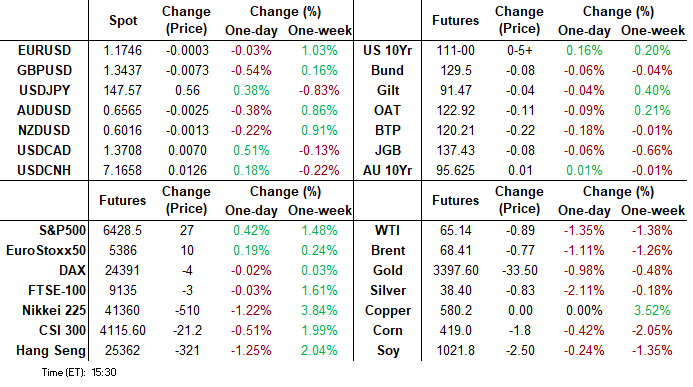

MNI ASIA MARKETS ANALYSIS: Ylds Slip, Stocks Up on Trade Talk

HIGHLIGHTS

- Treasuries marched off early Friday lows, look to finish near the top end of the range, curves turning flatter (2s10s -1.044 at 46.491) amid early trade related headlines ("nearing deal with China", "50/50" chance of deal with EU).

- June's advance durable goods report showed renewed weakness in core orders to end Q2, a potential sign of softer business investment and manufacturing in the months ahead.

- Broad greenback strength might be reflective of President’s Trump relatively more benign stance on Fed Chair Powell late Thursday.

US TSYS

MNI US TSYS: Risk Sentiment Improves Over Early Trade Headlines

- Treasuries look to finish near late session highs (curve reverse early steepening to mildly flatter) after a lower open, risk sentiment gained after early trade related headlines ("nearing deal with China", "50/50" chance of deal with EU).

- Little initial reaction in Tsys after mixed data (Durable orders slightly better than expected), Cap orders lower than expected w/ prior up-revised. June's advance durable goods report showed renewed weakness in core orders to end Q2, a potential sign of softer business investment and manufacturing in the months ahead.

- The Kansas City Fed's Tenth District Services survey showed a sharp drop in the composite index in July to -5 from positive 3 prior, marking a 19-month low. This was in contrast to the previously released KC regional manufacturing survey which showed an unexpectedly strong improvement.

- Tsy Sep'25 10Y contract trades +5 at 110-31.5 (111-00.5 high). Initial technical resistance at 111-14.5 (Jul 22 high), a clear break of it would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support remains intact at 110-08+, the Jul 14 and 16 low. A move through this support would reinstate a bearish theme. Curves bull flatten: 2s10s -.831 at 46.704, 5s30s -0.077 at 97.326.

- Cross asset: Bbg US$ index off early highs: BBDXY +3.35 at 1198.55; stocks extending record highs (SPX eminis at 6431.0); gold down -29.02.52 at 3339.66.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.30% (+0.02), volume: $2.725T

- Broad General Collateral Rate (BGCR): 4.29% (+0.02), volume: $1.128T

- Tri-Party General Collateral Rate (TCR): 4.29% (+0.02), volume: $1.108T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $109B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $281B

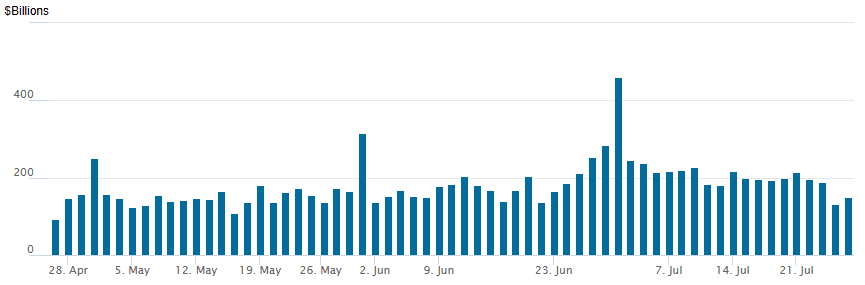

FED Reverse Repo Operation

RRP usage rebounds to $150.509B this afternoon from $132.186B yesterday, total number of counterparties at 24. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options continued to rotate around downside put structures Friday with a couple exceptions (+25k Sep'25 2Y Call spd for instance). Underlying futures well off lows after the bell, curves mixed with 2s10s -0.831 at 46.704, 5s30s +.231 at 97.634. Projected rate cut pricing gained slightly vs. morning (*) levels: Jul'25 at -0.06bp, Sep'25 at -16.6bp (-16.4bp), Oct'25 at -28.1bp (-27.1bp), Dec'25 at -44.2bp (-43.1bp). Year end projection well off early July level of appr -65.0bp.

SOFR Options:

+10,000 0QZ5 96.37/96.62 2x1 put spds, 1.25/legs

Block 5,000 SFRV5 96.06/96.18/96.31/96.50 call condors, 2.0 net

8,750 SFRZ5 95.37/95.62 2x1 put spds ref 96.08

-40,000 SFRZ5 95.37/95.62 put spds, 0.37 ref 96.07

8,000 SFRZ5 95.93/96.18 put spds vs. SFRH6 96.25/96.50 put spds

10,000 SFRQ5 95.62/95.87 put spds ref 95.825

1,250 SFRQ5 95.93/96.06 2x3 call spds ref 95.825

Blocks, 5,000 SFRQ5 95.75/95.87 call spds, 6.5

Blocks, 10,000 SFRQ5 95.75/95.81/95.87/95.93 put condors, 2.5 net

1,000 SFRZ5 96.25/96.37/96.62/96.75 call condors ref 96.055

1,750 0QQ5 96.56 puts, ref 96.68

Treasury Options:

3,000 TYU5 106.5/108 put spds, ref 110-31

+25,000 TUU5 104.25/104.5 call spds, 1 vsd. 103-18.5/0.05%

-10,000 TYU5 109.5/112 strangles, 29 ref 110-26.5 (appr 5.49% imp vol)

2,500 TYU5 112/113/114 call flys, 5 net ref 110-26

5,000 TYU5/TYV5 109.5 put spds 21

4,875 FVU5 108.75 calls ref 108-05.75

4,000 TUU5 104.25 calls ref 103-19.25

8,000 USU5 109 puts, 19

3,750 TYU5 111.5 calls, 25

over 5,000 TYQ5 110.75 puts, 4 last

over 7,400 TYU5 111 calls, 37 ref 110-25.5

5,000 wk1 TY 109/109.75 put spds (exp 8/1)

MNI BONDS: EGBs-GILTS CASH CLOSE: Partial Recovery From Weak Start

European core FI partially recovered from a weak start Friday.

- EGBs and Gilts weakened from the start, on follow-through from Thursday's hawkish-leaning ECB communications and a hawkish BOJ sources piece overnight (pointing to potential for another rate hike in Japan this year).

- Pressure began to ease thereafter though, with Bunds in particular rallying steadily throughout the session.

- Attention was on multiple encouraging EU-US trade headlines throughout the day, punctuated after the cash close by EU's von der Leyen saying that she would discuss trade with President Trump on Sunday.

- UK retail sales were softer-than-expected, adding to evidence of increasing consumer caution. German July IFO survey was slightly weaker-than-expected, while French and Italian consumer confidence improved.

- On the day, German yields shifted slightly higher in parallel across the curve, while the UK saw twist flattening. For the week, the UK curve bull flattened (2Y -1.8bp, 10Y -3.9bp), with Germany's bear flattening (2Y +7.8bp, 10Y +2.3bp).

- Periphery/semi-core EGB spreads tightened, led by Greece and Italy.

- Apart from this weekend's US-EU trade talks, attention next week will be Eurozone data including Q2 Flash GDP and July Flash Inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.6bps at 1.948%, 5-Yr is up 1.7bps at 2.298%, 10-Yr is up 1.6bps at 2.718%, and 30-Yr is up 1.5bps at 3.207%.

- UK: The 2-Yr yield is up 2.2bps at 3.884%, 5-Yr is up 2.6bps at 4.058%, 10-Yr is up 1.3bps at 4.635%, and 30-Yr is down 1.1bps at 5.449%.

- Italian BTP spread down 1.4bps at 83.4bps / Greek down 1.6bps at 67.9bps

MNI OPTIONS: Downside Favoured After Hawkish-Leaning ECB

Friday's Europe rates/bond options flow included:

- ERV5 98.18/98.31/98.37/98.56 call condor (vs 98.095) 7K given at 1.5

- ERV5 98.12/98.25 call spread vs. 98.00/97.87 put spread paper paid 2.25 for the call spread

- ERU5 98.06/98.18 call spread (vs. 98.05) vs. 2RU5 97.93/98.06 call spread (vs. 97.825) 10K given at 0.75

- ERZ5 98.375/98.625 call spread 7K given at 2.25

- ERZ5 97.93 puts 10K given at 1.0

- ERM6 98.06/18/50/62 call condor vs 97.75 puts 5K given at -0.25

- 2RV5 97.37 puts paper paid 3.0 on 10K

MNI FOREX: EURGBP Highest Since Nov 2023, USD Firms Ahead of Key Data

- The combination of weaker-than-expected UK retail sales data and the disappointing composite and services PMIs yesterday have continued to weigh on GBP. This dynamic has allowed EURGBP (+0.50%) to extend its recent rally following the break above a cluster of daily highs near 0.8700, eventually bridging the gap to key resistance at 0.8738, the Apr 11 high. This places the cross at the highest level since Nov 2023, signalling scope for a move towards 0.8781, the 2.236 projection of the Mar 3 - 11 - 28 price swing.

- A firmer dollar has also seen GBPUSD fall 0.68%, edging back towards the 1.3400 handle as we approach the weekend close. Broad greenback strength might be reflective of President’s Trump relatively more benign stance on Fed Chair Powell late Thursday. Initially, higher treasury yields on Friday had also supported the dollar, which remained immune to the subsequent turn lower for yields late in the session.

- USDJPY has risen 0.5% to trade back toward 148.00 as the cautious yen optimism following the upper house lection dissipates and concerns linger surrounding the short-term future of PM Ishiba. USDJPY has extended its powerful bounce off the 50-day EMA, rising over 200 pips from Thursday’s session low.

- EURJPY has also printed fresh 12-month highs in the process. Today’s move above 173.43 provides another bullish technical development for EURJPY, and a close at current levels would cement a ninth consecutive week of gains, the longest winning streak since 2008. Above here, 174.86 (Fib projection) provides the next target before 175.43, the July 11 ‘24 high and a key medium-term resistance

- Next week’s central bank calendar is stacked, with decisions from the Fed, BOC and the BOJ all scheduled. US Q2 advance GDP and July employment are data highlights.

MNI FX OPTIONS: Expiries for Jul25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E679mln), $1.1740-50(E1.7bln), $1.1800(E2.1bln)

- USD/JPY: Y145.00($1.2bln), Y146.00($841mln), Y147.75-85($600mln)

- EUR/GBP: Gbp0.8725-50(E892mln)

- AUD/USD: $0.6450($552mln)

- USD/CAD: C$1.3700-20($1.2bln)

MNI US STOCKS: Late Equities Roundup: Earnings, Trade Deal Chatter Drive New Highs

- Stocks continue to gain incrementally Friday, SPX eminis and Nasdaq indexes marking new record highs (6430.25 & 21159.80 respectively), the Dow firmer, but still off December 4 '24 record high of 45073.63. Debatably positive trade related headlines ("nearing deal with China", "50/50" chance of deal with EU) and generally positive earnings continued to buoy risk sentiment.

- Currently, the DJIA trades up 220.13 points (0.49%) at 44913.39, S&P E-Minis 27.75 points (0.43%) at 6429.25, Nasdaq up 89.1 points (0.4%) at 21146.65.

- A mix of Consumer Discretionary, Industrials and Insurance sector shares continued to outperform in late trade: Deckers Outdoor +12.07%, VeriSign +6.75%, Newmont +6.10%, Axon Enterprise +4.56%, Tesla +3.81%. Insurance providers & care services followed closely: Centene +5.72%, Aon +4.98%, Edwards Lifesciences +4.02%, Molina Healthcare +3.68%, Globe Life +3.59% and Humana +3.53%.

- Meanwhile, Communication Services, IT and pharmaceutical shares continued to lead declines in the second half: Charter Communications -18.26%, Intel Corp -9.74%, Comcast -5.29%, West Pharmaceutical Services -4.87%, Pfizer Inc -2.23% and HCA Healthcare -2.21%.

- Earnings resume Monday with the following reporting: Revvity Inc, Cantor Equity Partners, Woodward Inc, Whirlpool Corp, Waste Management, Brown & Brown, Cadence Design Systems, Beyond Inc, Universal Health Services, Nucor Corp, Welltower Inc and The Western Union Co.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6500.00 Round number resistance

- RES 3: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 2: 6439.88 1.500 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6430.25 Intraday high

- PRICE: 6428.00 @ 1507 ET Jul 25

- SUP 1: 6289.07 20-day EMA

- SUP 2: 6142.04 50-day EMA

- SUP 3: 6075.25 Low Jun 24

- SUP 4: 5959.00 Low Jun 23

S&P E-Minis have traded to fresh cycle highs this week. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. With the 6400.00 handle cleared, sights are on 6439.88, a Fibonacci projection. Key support is at the 50-day EMA, at 6142.04. Support at the 20-day EMA is at 6289.07

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 28/07/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 28/07/2025 | 1400/1000 | ** | housing vacancies | |

| 28/07/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 28/07/2025 | 1530/1130 | * | US Treasury Auction Result for 2 Year Note | |

| 28/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 28/07/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/07/2025 | 1700/1300 | * | US Treasury Auction Result for 13 Week Bill | |

| 28/07/2025 | - | FOMC Meeting | ||

| 29/07/2025 | 2301/0001 | * | BRC Monthly Shop Price Index |