MNI ASIA MARKETS ANALYSIS: Welcoming 2026 with Higher Yields

HIGHLIGHTS

- Treasuries look to finish off late session lows Friday, curves bear steepening on rather decent volumes on the first full session of 2026.

- Economic data limited to December S&P Global Manufacturing PMI: unchanged from the flash reading of 51.8, the report detailed a broad-based softening amid overall growth in manufacturing.

- Focus on the first two full weeks of the year see nonfarm payrolls (next Friday) and CPI reports (Jan 13) for December with those two key reports back on their original schedules having been prioritized by the BLS.

- Early strength for broad dollar indices on Friday was short-lived, with volatility in equity markets and potential fix-related flows helping to stall any topside momentum for the greenback and contain G10 FX ranges.

US TSYS

MNI US TSYS: Tsys Find Lower Footing at Start of 2026, Focus on Next Week's NFP

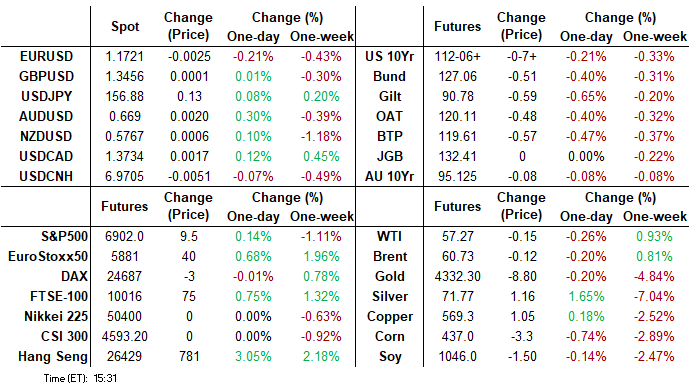

- Treasuries look to finish the first full session of 2026 weaker - near late session lows Friday on rather decent volumes: TYH6 currently -7 at 112-07 vs. 112-04.5 low on just over 1.1M contracts; 10Y yield at 4.1848% (+.0178) vs. 4.1946% high.

- Curves bear steepened (2s10s +1.955 at 70.941, 5s30s +.893 at 112.555) as projected rate cut pricing steady to mildly firmer vs. early morning levels (*): Jan'26 steady at -3.7bp, Mar'26 at -13.7bp (-12.8bp), Apr'26 at -19.2bp (-18.7bp), Jun'26 steady at -33.2bp.

- Limited data today: The final December S&P Global Manufacturing PMI was unchanged from the flash reading of 51.8, confirming a 5-month low for the index (52.2 Nov). In turn, the details of the report confirmed the flash data in portraying a broad-based softening amid overall growth in manufacturing.

- Focus on the first two full weeks of the year see nonfarm payrolls (next Friday) and CPI reports (Jan 13) for December with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7.

- No scheduled Fed speakers today - while Philadelphia Fed President Anna Paulson answers questions at a AEA conference tomorrow at 1015ET, MN Fed Kashkari speaks to the same conference on Sunday at 1250.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.87% (+0.16), volume: $3.485T

- Broad General Collateral Rate (BGCR): 3.82% (+0.13), volume: $1.299T

- Tri-Party General Collateral Rate (TCR): 3.82% (+0.13), volume: $1.255T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $74B

- Daily Overnight Bank Funding Rate: 3.65% (+0.01), volume: $123B

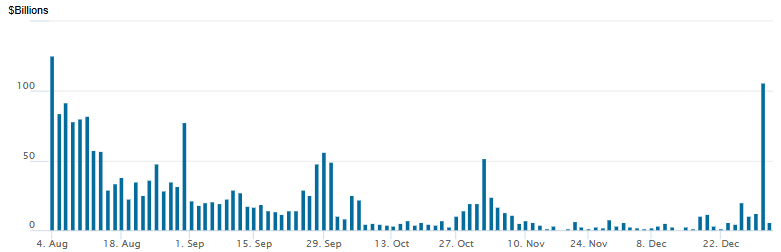

FED Reverse Repo Operation

RRP usage retreats back to $5.667B with 7 counterparties this afternoon after surging to $105.933B last Thursday's end of 2025. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options trade remained mixed/two-way Friday - the first full session of the New Year. Underlying futures held near late session lows, curves bear steepened as projected rate cut pricing steady to mildly firmer vs. early morning levels (*): Jan'26 steady at -3.7bp, Mar'26 at -13.7bp (-12.8bp), Apr'26 at -19.2bp (-18.7bp), Jun'26 steady at -33.2bp.

SOFR Options:

-4,000 SFRH6 96.50 straddles 12.25 over 99.62 calls ref 96.48

Block, 5,000 SFRH6 96.50 puts 5.75 over the 96.50/96.62 call spread ref 96.485

+4,000 0QH6 97.00/97.50 call spds vs. 96.75 puts, 0.0 net

3,000 0QF6 96.75/96.81 4x3 put spds vs. 97.06 calls, 2 net

-6,00 0QF6 97.25 calls, 0.5 ref 96.90/0.05%

Block/screen, 6,000 SFRG6 96.43/96.56/96.62/96.75 call condors, 3.75 ref 96.475

1,000 SFRG6 96.37/96.43/96.50 put flys

2,500 SFRF6 96.56 calls, 1.5 last

1,250 SFRU6 97.00/97.25 2x3 call spds

Treasury Options:

2,000 TUG6 104.37 straddles, ref 104-11.75

+5,000 FVG6 108.75/109.25/109.75 iron flys, 24 ref 109-06.25

10,000 TYG6 113 calls, 12, total volume just over 20,400, ref 112-08

5,000 TYH6 113 calls, 28 ref 112-07.5

5,850 wk3 FV 108.5/108.75 put spds vs. 109.75 calls x2

2,000 USH6 117/120/121 broken call flys ref 115-02

2,000 USG6 109/112 put spds, 4

2,500 wk2 TY 111.75/112.25 3x2 put spds ref 112-08.5 (exp 1/9)

2,000 TYH6 110/110.5/112 broken put trees ref 112-13.5

6,500 TUH6 104/104.25/104.37/104.5 broken put condors ref 104-12.5

over 5,600 TYH6 111.5 puts, 23 last

5,000 TYH6 113.5/114.5/116 broken call flys ref 112-13 to -14

5,000 wk2 TY 112 puts, 11 ref 112-07 (exp 1/9)

1,000 FVH6 108.0/109.0/109.5/110.25 broken put condors

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Close At/Near Highs In Soft Start To 2026

Bund and Gilt yields rose to start the 2026 trading year, with periphery EGBs underperforming overall.

- Yields gapped higher in the return from the New Year's cash trading holiday, with the move in Gilts appearing more pronounced by their slight descent in December 31st's abbreviated session (in which EGBs did not trade).

- Yields would fall to session lows in late morning London time on a day light in impactful data and macro headlines, but round-tripped higher as the day progressed. Gilt yields closed above their opening highs, with the 10Y closing at the highest intraday levels since Dec 22.

- While 10Y Bund yields finished off their opening levels, the 2.900% close was the highest since October 2023.

- Data was uneventful from a market perspective: UK and Eurozone PMIs were revised downward in December's final reports, while Eurozone household and NFC lending growth ticked up to the fastest since May 2023 in November.

- The UK and German curves bear steepened on the day, with BTPs leading periphery EGB underperformance.

- No major sovereign credit rating reviews scheduled for after hours on Friday.

- Next week's schedule is highlighted by flash December inflation readings: France and Germany release data on Tuesday, with the Netherlands, Italy and the Eurozone due on Wednesday. MNI's preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.7bps at 2.139%, 5-Yr is up 2.8bps at 2.476%, 10-Yr is up 4.5bps at 2.9%, and 30-Yr is up 6.4bps at 3.541%.

- UK: The 2-Yr yield is up 2.8bp at 3.720%, 5-Yr is up 3.3bps at 3.961%, 10-Yr is up 5.8bps at 4.537%, and 30-Yr is up 6.5bps at 5.273%.

- Italian BTP spread up 1.7bps at 71.3bps / French OAT spread up 0.5bps at 71bps

MNI OPTIONS: Eurex Returns From Holiday With Call Structure Buying Resuming

Friday's Europe rates/bond options flow included:

- DUG6 106.8/106.9/107 call fly paper paid 1.75/2.0 on 4.5K

- RXG6 128.5/129.5 call spread paper paid 12 on 2K

- SFIH6 96.40/96.35/96.30 put ladder bought for 1.5 in 5k

MNI FOREX: Equity Volatility & Fix Related Flows Help Contain FX Ranges

- Early strength for broad dollar indices on Friday was short-lived, with volatility in equity markets and potential fix-related flows helping to stall any topside momentum for the greenback and contain G10 FX ranges. Furthermore, limited appetite following the holiday period and ahead of the weekend close sees the USD index tracking close to unchanged levels to start the year.

- The most notable early mover was the Australian dollar, benefitting from the initial risk on tone for equities. This translated into AUDUSD rising over half a percent to regain the 0.6700 handle, keeping bullish conditions firmly intact for the pair. Despite the subsequent reversal lower for major US benchmarks, AUD remains at the top of the G10 leaderboard, bolstering the likelihood of another test of the recent cycle highs at 0.6728.

- Conversely, the Euro is a relative underperformer, printing as low as 1.1713 following downward revisions in the Eurozone December Manufacturing PMI. Attempts above the 1.1800 handle across December have proved short-lived, and today’s breach of the 20-day EMA at 1.1724 will be closely monitored. A clear break would signal scope for a deeper retracement, allowing an overbought condition to unwind.

- GBPUSD had the most notable bounce leading into the WMR fix, rising from session lows of 1.3434 to briefly print above 1.35. Note that GBPUSD moving average studies have recently crossed and are in a bull-mode position, highlighting a dominant uptrend.

- In EM, both MXN and ZAR have remained resilient through the equity turnaround, both rising ~0.65% on the session. For USDMXN, a move below 17.88 has placed spot at the lowest level since July 2024.

- Fed's Paulson and Kashkari are scheduled to speak over the weekend, both under elevated scrutiny as they newly come into rotation of FOMC voters this year. Lots of attention remains on the upcoming announcement of the new Fed Chair, while Monday’s data focus turns to US ISM manufacturing.

MNI US STOCKS: Late Equities Roundup: Off Lows, DJIA Outperforming

- The DJIA continues to climb higher Friday, SPX eminis and Nasdaq inching off second half lows to modestly higher in late trade. Currently, the DJIA trades up 333.4 points (0.69%) at 48401.01, S&P E-Mini Futures up 12 points (0.17%) at 6906, Nasdaq up 9.2 points (0%) at 23253.1.

- Tech-heavy Nasdaq and SPX indexes remain off early - to opening session highs amid increased competition for US chip and software companies. Asia equities traded strong overnight Hong Kong’s tech index jumped 3.6% after DeepSeek launched a paper on cheaper AI development, reigniting optimism over Chinese tech sector.

- Meanwhile, Shanghai Biren Technology Co surged 119%, after a successful IPO for the company. Baidu is also up strongly, after it submitted a proposal to spin-off its AI chip unit called Kunlunxin via a Hong Kong IPO, in which it currently holds around 60% (via BBG).

- In the US, however. a mix of Technology, Software and Services related stocks continued to lead declines in late trade: AppLovin Corp -7.73%, Palantir Technologies -5.56%, Intuit -4.75%, Gartner -4.55%, Workday -4.54%, Tyler Technologies -3.89%, Adobe -3.77%, Salesforce -3.62%, ServiceNow -3.45% and Crowdstrike Holdings -3.40%.

- Additional laggers included Progressive Corp -6.78%, Carvana -5.07% and Tesla -2.24% - the latter down after reporting the second consecutive year of lower than expected sales.

- On the positive side, Industrials and Energy sector shares continued to lead advances: Comfort Systems USA +6.73%, Caterpillar +4.19%, United Rentals +3.97%, Hubbell +3.86%, Quanta Services +3.84% and Boeing +3.52% buoyed the former while oil and gas shares supported the latter: Halliburton +5.10%, SLB Ltd +4.79%, Devon Energy +3.63%, Occidental Petroleum +3.55%, APA Corp +3.45% and ConocoPhillips +3.22%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Short-Term Weakness Appears Corrective

- RES 4: 7080.92 0.764 proj Nov 21 - Dec 11 - 18 price swing

- RES 3: 7021.79 0.618 proj Nov 21 - Dec 11 - 18 price swing

- RES 2: 7014.00 High Oct 30 and the bull trigger

- RES 1: 6994.00 High Dec 26

- PRICE: 6903.00@ 1455 ET Jan 2

- SUP 1: 6858.92 50-day EMA values

- SUP 2: 6771.50 Low Dec 18 and a key support

- SUP 3: 6684.50 Low Nov 24

- SUP 4: 6583.00 Low Nov 21 and a reversal trigger

Short-term weakness in S&P E-Minis appears corrective. A key short-term support has been defined at 6771.50, the Dec 18 low. A break of this level is required to signal scope for a deeper retracement and would highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the primary uptrend.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 05/01/2026 | 0700/0200 | * | Turkey CPI | |

| 05/01/2026 | 0730/0830 | ** | Retail Sales | |

| 05/01/2026 | 0930/0930 | ** | BOE M4 | |

| 05/01/2026 | 0930/0930 | ** | BOE Lending to Individuals | |

| 05/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/01/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/01/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 06/01/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 06/01/2026 | 0001/0001 | * | BRC Monthly Shop Price Index |