FOREX: Equity Volatility & Fix Related Flows Help Contain FX Ranges

Jan-02 17:43

- Early strength for broad dollar indices on Friday was short-lived, with volatility in equity markets and potential fix-related flows helping to stall any topside momentum for the greenback and contain G10 FX ranges. Furthermore, limited appetite following the holiday period and ahead of the weekend close sees the USD index tracking close to unchanged levels to start the year.

- The most notable early mover was the Australian dollar, benefitting from the initial risk on tone for equities. This translated into AUDUSD rising over half a percent to regain the 0.6700 handle, keeping bullish conditions firmly intact for the pair. Despite the subsequent reversal lower for major US benchmarks, AUD remains at the top of the G10 leaderboard, bolstering the likelihood of another test of the recent cycle highs at 0.6728.

- Conversely, the Euro is a relative underperformer, printing as low as 1.1713 following downward revisions in the Eurozone December Manufacturing PMI. Attempts above the 1.1800 handle across December have proved short-lived, and today’s breach of the 20-day EMA at 1.1724 will be closely monitored. A clear break would signal scope for a deeper retracement, allowing an overbought condition to unwind.

- GBPUSD had the most notable bounce leading into the WMR fix, rising from session lows of 1.3434 to briefly print above 1.35. Note that GBPUSD moving average studies have recently crossed and are in a bull-mode position, highlighting a dominant uptrend.

- In EM, both MXN and ZAR have remained resilient through the equity turnaround, both rising ~0.65% on the session. For USDMXN, a move below 17.88 has placed spot at the lowest level since July 2024.

- Fed's Paulson and Kashkari are scheduled to speak over the weekend, both under elevated scrutiny as they newly come into rotation of FOMC voters this year. Lots of attention remains on the upcoming announcement of the new Fed Chair, while Monday’s data focus turns to US ISM manufacturing.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: UPDATE: Thursday Data Calendar Adds Revelio & Regional Fed Data

Dec-03 17:42

- US Data/Speaker Calendar (prior, estimate). All times ET

- 12/04 0730 Challenger Job Cuts YoY (175.3%, --)

- 12/04 0830 Initial Jobless Claims (216k, 220k); Continuing Claims (1.960M, 1.963M)

- 12/04 0830 Revelio Labor Statistics

- 12/04 0830 Chicago Fed Labor indicators

- 12/04 1130 Dallas Fed Weekly Economic Index

- 12/04 1130 US Tsy $90B 4W, $80B 8W bill auctions

- 12/04 1230 Fed VC Bowman on bank supervision (text, moderated Q&A)

- Source: Bloomberg Finance L.P. / MNI

LOOK AHEAD: Thursday Data Calendar: Challenger Job Cuts, Weekly Claims

Dec-03 17:34

- US Data/Speaker Calendar (prior, estimate). All times ET

- 12/04 0730 Challenger Job Cuts YoY (175.3%, --)

- 12/04 0830 Initial Jobless Claims (216k, 220k); Continuing Claims (1.960M, 1.963M)

- 12/04 1130 US Tsy $90B 4W, $80B 8W bill auctions

- 12/04 1230 Fed VC Bowman on bank supervision (text, moderated Q&A)

- Source: Bloomberg Finance L.P. / MNI

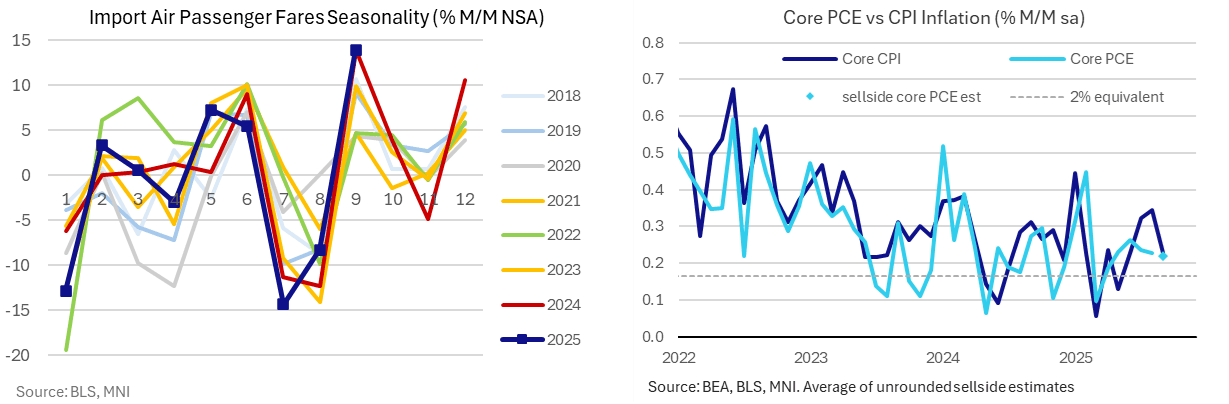

US DATA: Core PCE Estimates Still Likely Near 0.22% M/M For Friday’s Sept Report

Dec-03 17:27

- Within the import price data, air passenger fares increased a non-seasonally adjusted 14.0% M/M in September.

- That repeats the 13.9% in Sep 2024 but is strong compared to the 6.4% M/M averaged in the prior three years, leaving a reasonable seasonally adjusted increase.

- On its own, we estimate it could be worth 1-2bp for core PCE but its impact on tracking will clearly depend on what analysts had already pencilled in.

- For instance, Morgan Stanley have lowered their core PCE inflation estimate 1bp to 0.22% M/M as they estimate airfares increased 2.6% M/M after their own seasonal adjustment vs an estimated 3.2% M/M.

- We don’t imagine today’s release will have materially changed analyst estimates for Friday’s core PCE release, seen at a median 0.22% M/M after last week’s PPI report. MS had been at the higher end of a narrow range of 0.20-0.23% we’d seen after PPI.

- This follows 0.23% M/M in Aug and 0.24% M/M with MS previously seeing scope for a +1bp revision to Aug and +1.5bp for Jul.