MNI ASIA MARKETS ANALYSIS: Trump Says Speaking to Iran

HIGHLIGHTS

- Treasuries look to finish near highs Friday - holding a narrow second half range. Pres Trump been speaking with Iran, will make deal with India, Pakistan.

- Early risk-on tone followed unscheduled comments from Fed Governor Waller on the possibility of a rate cut in July and headlines that Iran was ready to discuss limitations on uranium enrichment plans.

- Stocks reversed early gains in the second half while short end rates priced in an optimistic 50bp in rate cuts by year end.

US TSYS

MNI US TSYS: Tsys Narrow/Higher Range, Trump Been "Speaking to Iran"

- Treasuries look to finish higher Friday, top half of narrow range. Early risk-on tone followed unscheduled comments from Fed Governor Waller on the possibility of a rate cut in July and headlines that Iran was ready to discuss limitations on uranium enrichment plans.

- No market reaction to late Pres Trump comments to reporters & social media posts: "WILL MAKE TRADE DEAL WITH INDIA, PAKISTAN," "BEEN SPEAKING TO IRAN," "IRAN WANTS TO SPEAK TO US, NOT EUROPE" - Bbg posts. Trump adds Europe is not going to help with Iran, nor will China; Trump "might" support Israel/Iran ceasefire

- The price details of the Philly Fed manufacturing survey for June showed a pullback from elevated rates for both prices paid and prices received in the current period. Six-month ahead expectations for prices paid pushed higher again though, and at 68.9 is getting closer to the high of 77.8 from Jan 2022, although prices received isn’t quite as relatively elevated.

- Tsy Sep'25 10Y futures trades +5 at 110-30.5 vs. 111-03 high, remains below key resistance and its recent high of 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish and highlight a stronger reversal. This would open 111-30, a Fibonacci retracement.

- Curves steeper, 2s10s +2.611 at 47.137, 5s30s +3.530 at 93.143. 10Y yield at 4.3791% vs. 4.3593% low. Projected rate cut pricing back to 50bp by December.

- Cross asset: Stocks mixed (DJIA +29.34 at 42,202.0, SPX eminis -20.75 at 6013.5), Gold mildly lower at 3365.05, Bbg US$ index little firmer at 1210.80 +1.10.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (-0.03), volume: $2.639T

- Broad General Collateral Rate (BGCR): 4.27% (-0.02), volume: $1.088T

- Tri-Party General Collateral Rate (TCR): 4.27% (-0.02), volume: $1.062T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $109B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $290B

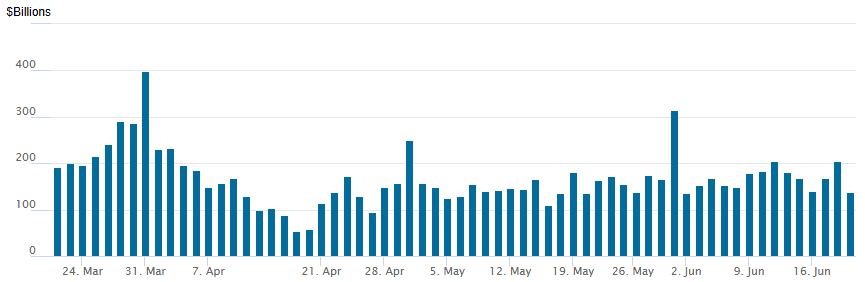

FED Reverse Repo Operation

RRP usage resumes following Thursday's holiday, retreats $138.283B this afternoon from $205.050B Wednesday, total number of counterparties at 40. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

While early Treasury call interest faded in the the second half, a surge in SOFR put options were reported despite underlying futures clinging near session highs after the bell. Note large Dec'25 SOFR ratio put spread - a cheap hedge for no rate cut by year end even as projected cuts pricing gained. Underlying futures gained after Fed Gov Waller comments of potential for July rate cut this morning. Projected rate cut pricing gains vs. this morning's levels (*) as follows: Jul'25 at -3.6bp (-2.6bp), Sep'25 at -20bp (-17.1bp), Oct'25 at -33.6bp (-30.1bp), Dec'25 at -51bp (-46.4bp).

SOFR Options:

+50,000 SFRZ5 95.50/95.68 2x1 put spd 0.25 (Fed on hold through Yr end hedge)

-5,000 SFRU5 95.87/96.00/96.12 1x3x2 call flys, .25 ref 95.895

-2,500 2QU5 96.62 straddles, 42.0 ref 96.645

-20,000 SFRV5 96.00 puts, 10.5 to 10.0 ref 96.135

-20,000 SFRQ5 95.62/95.75 put spds, 2.0 ref 95.88

+4,000 SFRN5 95.62/95.68/95.75 put fly, 0.5 vs. 95.87/0.05%

-5,000 0QU5 96.43 puts, 11.0 vs. 96.66/0.33%

+10,000 SFRU5 96.18/96.31 call spds, 1.125 ref 95.875

+10,000 SFRH6 98.00/99.00 2x3 call spds 3.0 over 95.50 puts ref 96.385 to -.36

13,200 SFRZ5 95.75 puts ref 96.13

+10,000 2QX5/2QZ5 96.00/96.25/96.50 put fly strip, 7.5 total db

13,400 SFRZ5 95.87 puts, ref 96.105

4,000 0QU5 97.00 calls ref 96.66

3,500 SFRN5 95.81 puts ref 95.86

2,200 SFRN5 95.75 puts ref 95.86

4,500 SFRH6 96.37 calls ref 96.325

Treasury Options:

2,500 TUU5 103.75 puts, 103-22.38

2,200 FVQ5 109.5 calls ref 108-06.5

2,500 TYQ5 116.5/117 call spds ref 110-27

over 10,000 TYU5 107/108 put spds, 8 ref 110-25.5

-10,000 TYU5 115 calls, 12.0

2,000 TYU5 107/108 put spds 8 ref 110-22

-8,500 TYQ5 110.5 straddles, 141-140 (implieds 5.98-5.92%)

over +50,000 TYQ5 112 calls, 24 ref 110-20 to -20.5 appr implied vol 6.49%

-15,000 TYQ5 109/110/111/112 iron condors, 38

5,000 TYQ5 111 calls vs. 109/110 put spds ref 110-20.5

5,000 wk4 TY 110.5/110.75 strangles

3,000 TYQ5 109/110 2x1 put spds, 6 ref 110-21

5,400 TYQ5 112 calls, 27 ref 110-26.5

+25,000 TYQ5 112.5 calls, 20 vs. 110-27.5/0.20%, appr implied vol 6.57%

6,600 FVN5 107.75 puts ref 108-05.5

12,900 TYN5 111 calls ref 110-28

2,100 USN5 112.5 puts, 2 ref 113-18

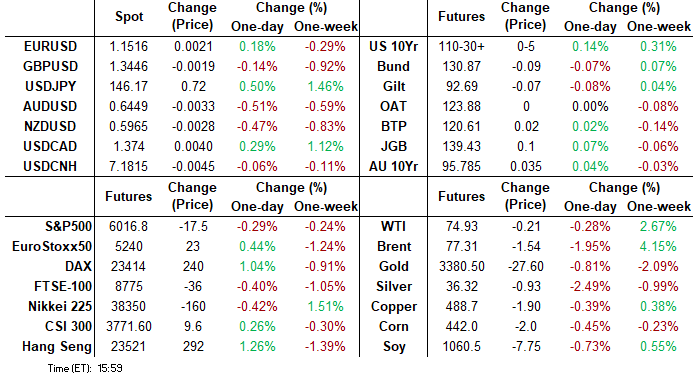

MNI FOREX: EURJPY Extends Rally, Reaches Near 11-Month High

- The week has been characterised by a fragile risk backdrop associated with the middle east conflict, furtively boosting the greenback’s appeal. The USD Index has showed above the downtrendline that has helped define the dollar weakness across Trump's term so far, with the geopolitical uncertainty prompting a covering phase that triggered a close above resistance yesterday. This level remains relevant and a corrective phase higher could build a base on a convincing break.

- There has been mixed price action across G10 on Friday, with the most notable laggards, the AUD and NZD, while the Japanese yen has also been under pressure. As such, USDJPY has risen as high as 145.96, narrowing the gap to an important resistance at 146.28, the May 29 high.

- However, EURUSD is higher Friday and sits just 25 pips lower on the week, a very positive sign for market participants looking for further single currency appreciation in H2. Moving average studies continue to display a dominant uptrend, with corrective dips remaining well supported. Scope is seen for a climb towards 1.1696, a Fibonacci projection.

- The Euro’s resilience has seen EURJPY (+0.63%) extend its recent rally, and notably climbing above 168.00 to trade at near 11-month highs for the cross, and signalling scope for a move towards 170.00.

- USDCAD stands 0.22% higher on the day following a weaker-than-expected set of Canadian April retail sales and a notably weak flash print for May.

- Global flash PMI data highlights Monday’s calendar, with French and German readings kicking things off.

MNI OPTIONS: Expiries for Jun23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1460-70(E917mln), $1.1490(E863mln), $1.1500(E524mln), $1.1550(E891mln)

- AUD/USD: $0.6500-10(A$597mln)

MNI US STOCKS: Late Equities Roundup: Reversing Gains Into Weekend

- Stocks continued to scale off early Friday gains to mildly weaker as accounts squared up ahead of the weekend. Stocks were buoyed in the first half after unscheduled comments from Fed Governor Waller on the possibility of a rate cut in July and headlines that Iran was ready to discuss limitations on uranium enrichment plans.

- Support evaporated in the second half as wires reported Pres Trump was considering more military deployments in the US let alone abroad.

- Currently, the DJIA trades down 30.24 points (-0.07%) at 42140.74, S&P E-Minis down 22.5 points (-0.37%) at 6011.5, Nasdaq down 122.7 points (-0.6%) at 19423.76.

- Health Care, Communication Services and Materials sector shares underperformed in late trade while leading sectors included Consumer Staples and Financial Services.

- Laggers included IT services stocks: Accenture PLC -7.03%, Arista Networks -3.80% and Cognizant Technology Solutions -3.08% and pharmaceuticals: Eli Lilly & Co -2.23%, Vertex Pharmaceuticals -1.69% and Dexcom -1.16%. Other laggers included Steel Dynamics -3.5% and Albemarle -3.48%.

- Consumer Staples leading gainers included Kroger +8.86%, Mondelez International +3.42% and The Hershey Co +2.21%. Additional leaders late Friday included Builders FirstSource +5.88%, CarMax +5.86%, Coinbase Global +3.21% and PayPal Holdings+2.28%

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11 and the bull trigger

- PRICE: 6012.25 @ 1513 ET Jun 20

- SUP 1: 5969.50/5902.27 Intraday low / 50-day EMA

- SUP 2: 5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis remains bullish. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6006.73, the 20-day EMA. A clear breach of this average would suggest potential for a deeper retracement and expose the 50-day EMA, at 5902.27. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

COMMODITIES

MNI AMERICAS OIL: US Daily Oil Summary: WTI up 10% on Week

CRUDE: WTI has pulled back today, although has pared losses after falling to an intraday low of $74.30/b. Fears of imminent involvement in the Israel-Iran conflict appeared to ease after Trump said he would give himself up to two weeks to decide on taking military action. Nevertheless, ongoing political risks have driven WTI up nearly 10% on the week.

- WTI JUL 25 down 0.3% at 74.91$/bbl

- President Trump signalled a decision for the US to strike Iran within two weeks which leaves the door open for diplomacy and negotiations.

- US President Trump said on Wednesday that he has approved a plan but is still hoping that Tehran will agree to abandon its nuclear programme.

- A senior Iranian official said that Iran is ready to discuss limitations on its uranium enrichment but that ‘zero enrichment will undoubtedly be rejected.’

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/06/2025 | 0700/0300 | Fed Governor Christopher Waller | ||

| 23/06/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/06/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/06/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/06/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/06/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/06/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/06/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/06/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/06/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/06/2025 | 1300/1500 | ECB Lagarde At ECON Hearing | ||

| 23/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/06/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/06/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/06/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 23/06/2025 | 1720/1320 | Chicago Fed's Austan Goolsbee | ||

| 23/06/2025 | 1830/1430 | Fed Governor Adriana Kugler |