MNI ASIA MARKETS ANALYSIS: Trade Uncertainty Saps Sentiment

HIGHLIGHTS

- Treasuries moderated near session lows following comments by Fed Gov Miran (voter) at a Nomura Research Forum stated that US-China trade tensions tied to rare-earth curbs "pose significant downside risks".

- "BESSENT SUGGESTS POSSIBILITY OF LONGER CHINA TARIFF TRUCE, TARIFF-TRUCE COMMENT TIED TO CHINA RARE-EARTH DELAY" Bbg

- The USD Index started the session weaker and generally maintained those losses through the London close. Powell's relative easing bias late on Tuesday provided the initial trigger.

- Look ahead: Thursday's Retail Sales, PPI and Business Inventories suspended due to the Gov shutdown. On the other hand, Weekly Jobless Claims on a state level likely to be gradually parsed out.

US TSYS

MNI US TSYS: Tsys Whipsaw Lower, Risk Sentiment Tested on Policy & Trade

- Treasuries ratcheted lower Wednesday, buffeted by several rounds of selling and a reversal in overall sentiment that triggered selling in equities.

- Treasuries retreated through early overnight levels, coinciding with EU headlines that the EU is discussing "preferential treatment to give domestic firms bidding for public contracts worth about €2.5 trillion ($2.9 trillion) a year," Bbg. Note, however, 10Y Bund also declined and is rebounding.

- Treasuries moderated near session lows following comments by Fed Gov Miran (voter) at a Nomura Research Forum stated that US-China trade tensions tied to rare-earth curbs "pose significant downside risks". Ironically, this comes after after Treasury Sec Bessent suggested the possibility of a "longer tariff truce with China tied to rare-earth imports" helped risk sentiment earlier.

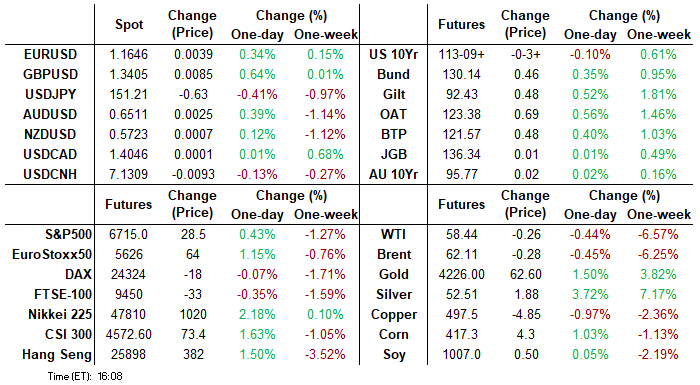

- Currently, Tsy Dec'25 10Y contract trades 113-09 (-4) vs. 113-06.5 low, yld tapped 4.0455% high; curves flatter/off lows: 2s10s -1.490 at 53.445 (51.608 low), 5s30s -1.561 at 100.734 (98.827 low). Initial technical support at 112-26 (20-day EMA) followed by the 50-day EMA at 112-16. A clear break of the average would expose 111-13+, the Aug 18 low and a key support.

- Cross asset: Bbg US$ index off lows, -3.35 at 1211.09 (1210.10 low), stocks off early highs: DJIA down down 72.67 points (-0.16%) at 46,200.11, S&P E-Minis up 12.5 points (0.19%) at 6,699.25, Nasdaq up 91.7 points (0.4%) at 22,611.45.

- Look ahead: Thursday's Retail Sales, PPI and Business Inventories suspended due to the Gov shutdown. On the other hand, Weekly Jobless Claims on a state level likely to be gradually parsed out.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.19% (+0.04), volume: $2.932T

- Broad General Collateral Rate (BGCR): 4.16% (+0.04), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.16% (+0.04), volume: $1.113T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.10% (+0.00), volume: $80B

- Daily Overnight Bank Funding Rate: 4.10% (+0.00), volume: $168B

FED Reverse Repo Operation

RRP usage bounces to $5.484B with 20 counterparties from $3,516B Tuesday (lowest level since early April 2021). Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option flow leaned towards calls on two-way trade on net after underlying futures retreated. Projected rate cut pricing largely steady vs. late Tuesday levels (*): Oct'25 at -24.5bp (-24.5bp), Dec'25 at -48.4bp (-48.4bp), Jan'26 at -61.5bp (-61.2bp), Mar'26 at -74.4bp (-74.1bp).

SOFR Options:

5,000 3QX5 96.75 calls vs. 3QF6 96.75/97.75 call spds, 4.5 net cr conditional curve steepener

+15,000 SFRZ5 96.00 puts cab

+6,000 SFRZ5 96.00 puts, .25 ref 96.375

-10,000 SFRH6 96.50/96.68/96.87/97.06 call condors, 4.75 ref 96.605

+2,500 0QZ5 97.50/98.00/98.50 call flys, 2.0

+2,500 SFRM6 97.00/98.00/99.00 call flys, 11.25

-5,000 0QZ5 96.50/96.75 2x1 put spds, 1.5

3,300 SFRM6 98.00/98.12 call spds, 0.5 ref 96.84

4,500 SFRX5 97.00 calls, cab ref 96.365 ref 96.365 to -.37

+2,000 SFRF6 97.00/97.50 2x1 put spds, 0.5

+8,000 SFRZ5 96.25/96.43 2x1 put spds, 5.5 ref 96.37

+1,250 SFRX5 96.18/96.37/96.56 iron flys, 6.5 ref 96.375

Treasury Options:

5,750 TYG6 111 puts, 26 ref 113-04

Block, 5,000 TYZ5 115/TYG6 116 call spds on 2:3 ratio, 44 net vs. 113-08

10,000 TYZ5 114.5 calls, 22 ref 113-15, total volume over 23,500

over 9,000 TYX5 114.5 calls, 4 ref 104-14 to -14.5, total volume over 12,600

5,000 TYX5 113/113.5/114 2x1x1 call trees, 45 ref 113-14

-40,000 TYZ5 113.5/115 call spreads, 30 vs. 113-16/0.29%

3,000 USZ5 120/122 call spds

+5,500 TYZ5 111/112 put spds vs. 116 calls, even net

+3,000 TYX5 115/116 1x2 call spds, 0.0

+2,000 TYZ5 114.5/115.5 call spds, 13 ref 113-15

+2,000 TYZ5 114.5/115 call spds, 8 ref 113-15.5

+2,000 TYX5 111.5/112/112.5/113 put condors, 6.0

over 8,000 TYX5 114 calls, 10

2,000 FVZ5 108.5 puts, 5 ref 109-24.75 to -25

2,000 USZ5 110/114 2x1 put spds, 10 vs. 118-07/0.06%

+4,000 TYZ5 111/112 put spds, 9

MNI BONDS: EGBs-GILTS CASH CLOSE: OATs' Continued Gains Buoys Broader Space

European curves continued to bull flatten Wednesday, with French outperformance continuing.

- Longer-end yields gapped lower on the open and continued lower for most of the session, buoyed by comments after Tuesday's cash close by Fed Chair Powell pointing to a possible end to QT in coming months, as well as a perception of easing French political risks.

- In a light session for data (including some final national-level Eurozone September inflation readings), Euro area industrial production shrank less than expected in August but all four of the largest countries saw declines.

- On the day, Gilts twist flattened with Bunds bull flattening. UK 2s10s had their flattest close since early July; for Germany, March.

- Periphery/semi-core EGB spreads closed tighter, led by Italy and France.

- Thursday's scheduled highlight is UK monthly activity data, while we get multiple central bank speakers including BOE's Mann and Greene, and ECB''s Wunsch, Kocher, Lane, and Lagarde. On the French political front we also get no-confidence motions on the government.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 1.3bps at 1.922%, 5-Yr is down 3.6bps at 2.166%, 10-Yr is down 3.9bps at 2.571%, and 30-Yr is down 4.6bps at 3.146%.

- UK: The 2-Yr yield is up 0.1bps at 3.902%, 5-Yr is down 3.7bps at 4.001%, 10-Yr is down 4.7bps at 4.543%, and 30-Yr is down 5.1bps at 5.343%.

- Italian BTP spread up 2.6bps at 80.9bps / French OAT down 2.3bps at 77.5bps

MNI OPTIONS: Large Trading In And Out Of Euribor Call, Mixed Trade In Sonia

Wednesday's Europe rates/bond options flow included:

- ERZ5 98.25c, sold at 0.5 in 10k. Earlier: ERZ5 98.25c, bought for half in 33k

- SFIZ5 96.30/96.40/96.50c fly, bought for 1 in 4k

- SFIZ5 96.20/96.30cs 1x2, bought for 0.25 in 2.5k.

- SFIH6 96.25/96.05/95.85p fly, bought for 4.75 in 5.5k

MNI FOREX: USD Index Weaker Again, Despite Bessent Optimism

- The USD Index started the session weaker and generally maintained those losses through the London close. Powell's relative easing bias late on Tuesday provided the initial trigger, but the much firmer-than-expected CNY fix from the PBOC also worked against the greenback.

- An appearance at the IMF / World Bank forum helped trigger a brief spell of USD support. Bessent's optimism on growth, laying out the groundwork for US growth akin to the "late 1800's or 1990's" is helping the USD higher at the margins and pressing EURUSD toward flat (thereby erasing the ~40 pip gains at the European open). The better-than-expected Empire Manufacturing print will also be helping.

- US 10y yields finding a base at 4.00% has proved a key catalyst, although markets have looked through the persistent S/T uptrend in equities across Wednesday.

- Focus for the duration of the Thursday session turns to the Australian jobs print for September, expected to show employment change of +20k in the month with an unchanged participation rate. AUD had a quieter Wednesday session, despite Treasury Secretary Bessent talking up the possibility of a longer rare earths trade truce with China. This keeps the near-term picture unchanged after Tuesday's new cycle low. However, Tuesday’s recovery highlights a possible reversal pattern - a hammer candle formation. If correct, it signals the end of the bear leg that started Sep 17.

- UK data are also in focus Thursday - with GDP stats as well as industrial and manufacturing production. Ahead of the Thursday print, a late rally in GBP saw GBP/USD rally back to 1.34 on decent volumes. While there was no specific UK newsflow or headlines to drive the move, it helped EURGBP drift into the London finish, closing the gap with the French pension reform-tied rally from earlier in the week.

MNI FX OPTIONS: Expiries for Oct16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-20(E1.5bln), $1.1580-00(E4.0bln), $1.1650-55(E783mln), $1.1700-05(E1.2bln), $1.1735-40(E837mln)

- USD/JPY: Y150.50($729mln), Y151.00($511mln), Y152.00($728mln)

- AUD/USD: $0.6500-20(A$598mln)

- USD/CAD: C$1.3975($946mln)

MNI US STOCKS: Midday Equities Roundup: Unwinding Early Support

- Stocks had extended session highs earlier after Treasury Sec Bessent suggested the possibility of a "longer tariff truce with China tied to rare-earth imports", but retreated with Treasuries following headlines that the EU is discussing "preferential treatment to give domestic firms bidding for public contracts worth about €2.5 trillion ($2.9 trillion) a year," according to Bloomberg.

- Currently, the DJIA trades down 59.6 points (-0.13%) at 46,210.81, S&P E-Minis down 1.5 points (-0.02%) at 6,685, Nasdaq up 40.2 points (0.2%) at 22,563.41.

- A mix of Utilities, Communication Services and Information Technology sector shares held firmer after midday: Bunge Global +10.70%, Advanced Micro Devices +6.05%, Prologis +5.64%, First Solar +5.41%, Morgan Stanley +5.27%, Moderna Inc +4.76% and Generac Holdings +4.58%.

- Leading decliners included stocks from Industrials, Materials and Health Care Sectors: Axon Enterprise -7.33%, Progressive Corp -7.17%, F5 Inc -5.59%, Allstate Corp -5.24%, Abbott Laboratories -4.49%, L3Harris Technologies -4.32%, GE Vernova -4.03% and Motorola Solutions -4.00%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Trend Needle Points North

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6742.50/6812.25 Intraday high / High Sep 9 and bull trigger

- PRICE: 6710.00 @ 1536 ET Oct 15

- SUP 1: 6605.62 50-day EMA

- SUP 2: 6540.25 Low Oct 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

A sharp sell-off in S&P E-Minis last Friday appears corrective - for now. The contract has found support below the 50-day EMA, currently at 6605.62, and the Oct 10 low of 6540.25 has been defined as a key short-term support. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

MNI COMMODITIES: Gold Extend Gains, Crude Falls Amid US-China Tensions

- Gold registered another all-time high on Wednesday, buoyed by the escalation in US-China trade tensions and Powell's relative easing bias late on Tuesday.

- Spot rose to a peak at $4,218/oz earlier in the session, before paring gains, with price currently up by 1.3% at $4,198.

- This week’s extension in gold reinforces current bullish conditions, with the move up maintaining the price sequence of higher highs and higher lows. After piercing the $4,200 handle today, sights turn to $4,239.7 next, a Fibonacci projection point.

- The trend is in overbought territory, however. A move down would be considered corrective and would allow the overbought set-up to unwind. Support lies at $3,918.7, the 20-day EMA.

- Meanwhile, silver has also rebounded by 2.9% to $52.9/oz today, keeping the precious metal just below this week’s record high ($53.546).

- Bloomberg writes that the silver market has been impacted by a lack of liquidity in London, prompting prices to soar above futures in New York.

- Trend signals in silver remain bullish, and a break above yesterday’s record high would turn attention to $54.00 round number resistance next.

- Elsewhere, crude has extended losses amid demand concerns due to the trade tensions, as well as rising global supplies.

- WTI Nov 25 is down by 0.6% at $58.3/bbl.

- A bearish theme in WTI futures remains intact, with sights on $57.50 next, the May 30 low. On the upside, initial resistance is at $62.31, the 50-day EMA.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/10/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 16/10/2025 | 0600/0700 | ** | Trade Balance | |

| 16/10/2025 | 0600/0700 | ** | Index of Services | |

| 16/10/2025 | 0600/0700 | ** | Index of Production | |

| 16/10/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 16/10/2025 | 0800/1000 | *** | HICP (f) | |

| 16/10/2025 | 0830/0930 | BOE Credit Conditions Survey | ||

| 16/10/2025 | 0900/1100 | * | Trade Balance | |

| 16/10/2025 | 0900/0500 | * | CREA Existing Home Sales | |

| 16/10/2025 | 0900/1100 | Foreign Trade | ||

| 16/10/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 16/10/2025 | 1230/0830 | *** | Retail Sales | |

| 16/10/2025 | 1230/0830 | *** | PPI | |

| 16/10/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 16/10/2025 | 1230/0830 | *** | PPI | |

| 16/10/2025 | 1230/0830 | *** | Retail Sales | |

| 16/10/2025 | 1300/1400 | BOE Mann in Panel on MonPol and Trade Shocks | ||

| 16/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 16/10/2025 | 1300/0900 | Fed Governor Michael Barr | ||

| 16/10/2025 | 1300/0900 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 1400/1000 | * | Business Inventories | |

| 16/10/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/10/2025 | 1400/1000 | * | Business Inventories | |

| 16/10/2025 | 1400/1000 | Fed Governor Michelle Bowman | ||

| 16/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 16/10/2025 | 1445/1545 | BOE Mann in MonPol Panel at IMF/World Bank Meetings | ||

| 16/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 16/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 16/10/2025 | 1545/1745 | ECB Lane in Policy Panel at IIF Annual Meeting | ||

| 16/10/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 16/10/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 16/10/2025 | 1600/1800 | ECB Lagarde in IMF Policy Debate | ||

| 16/10/2025 | 1645/1245 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 1730/1330 | BOC Governor Macklem speaks at Peterson Institute event in Washington. | ||

| 16/10/2025 | 1830/1930 | BOE Greene in Panel on UK/EU Relations | ||

| 16/10/2025 | 2015/1615 | Fed Governor Stephen Miran | ||

| 16/10/2025 | 2030/1630 | Richmond Fed's Tom Barkin | ||

| 16/10/2025 | 2200/1800 | Minneapolis Fed's Neel Kashkari |