US STOCKS: Midday Equities Roundup: Unwinding Early Support

Oct-15 17:38

- Stocks had extended session highs earlier after Treasury Sec Bessent suggested the possibility of a "longer tariff truce with China tied to rare-earth imports", but retreated with Treasuries following headlines that the EU is discussing "preferential treatment to give domestic firms bidding for public contracts worth about €2.5 trillion ($2.9 trillion) a year," according to Bloomberg.

- Currently, the DJIA trades down 59.6 points (-0.13%) at 46,210.81, S&P E-Minis down 1.5 points (-0.02%) at 6,685, Nasdaq up 40.2 points (0.2%) at 22,563.41.

- A mix of Utilities, Communication Services and Information Technology sector shares held firmer after midday: Bunge Global +10.70%, Advanced Micro Devices +6.05%, Prologis +5.64%, First Solar +5.41%, Morgan Stanley +5.27%, Moderna Inc +4.76% and Generac Holdings +4.58%.

- Leading decliners included stocks from Industrials, Materials and Health Care Sectors: Axon Enterprise -7.33%, Progressive Corp -7.17%, F5 Inc -5.59%, Allstate Corp -5.24%, Abbott Laboratories -4.49%, L3Harris Technologies -4.32%, GE Vernova -4.03% and Motorola Solutions -4.00%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

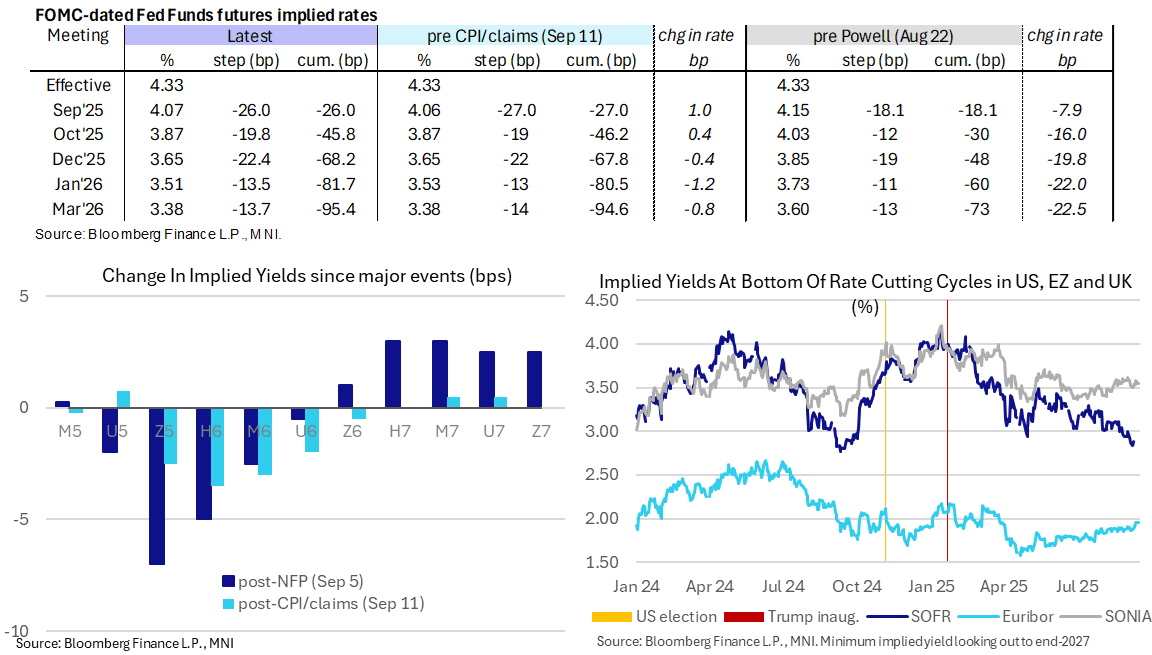

STIR: Dec 2025 Fed Funds Implied Rate Almost Fully Reverses Claims Hit

Sep-15 17:36

- Fed Funds implied rates see the Dec’25 lead today’s increase, currently 2bp higher from Friday’s close to have almost fully reversed Thursday’s drop seen on a surprise uptick in initial jobless claims along with the broader US CPI report.

- It’s likely a positioning play, with the sole data being a surprisingly weak Empire manufacturing report.

- Cumulative cuts from 4.33% effective: 26bp for Wed, 46bp Oct, 68bp Dec, 81.5bp Jan and 95.5bp Mar.

- SOFR futures hold the session’s twist flattening, with U5 and Z5 1 tick lower vs gains of up to 2.5 ticks in U6 and Z6.

- The SOFR implied terminal yield of 2.915% (SFRH7, -1.5bp) meanwhile is unchanged from when US desks filtered in. It remains off last Monday's close of 2.84% (lowest since Sep 2024 and one of the lowest for the cycle) but still points to more than 140bp of cuts ahead.

- Still to come today, Miran’s Senate confirmation vote (expected to pass having already passed the Banking Committee 13-11). The cloture vote is at ~1730ET before the full confirmation voter at ~2000ET.

- We also expect at some point to hear a ruling in the ongoing Trump-Cook case on whether the court will grant a stay on the decision that allowed Cook to remain in her job for now (and thus attend this week’s FOMC meeting starting tomorrow before the decision on Wed).

MNI EXCLUSIVE: MNI Interviews Former Fed Economist Claudia Sahm

Sep-15 17:05

- MNI interviews former Fed economist Claudia Sahm -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

US STOCKS: A Minor Dip Off All-Time Highs, Alphabet The Fourth $3tn Company

Sep-15 17:01

- ESZ5 has softened a little in recent trading but at 6672.00 (+0.4%) still trades close to its earlier fresh all-time high of 6681.25, with gains at the time extended by Trump suggesting a move to semi-annual reporting for corporates.

- Next resistance is seen at 6685.25 (1.00 proj of Aug 1-15-20 price swing) after which lies the round 6700. Support meanwhile isn’t seen until 6546 (20-day EMA).

- Some large idiosyncratic moves at play include Tesla (+5.6%) after Musk bought ~$1bn of shares, Alphabet (+3.3%) having become the fourth extending company with a market cap in excess of $3trn after building on previous gains from a recent antitrust ruling and Oracle (+3.3%) attributed to data center construction expectations along with Seagate Technology up 7.8%. Other notable gains include Amazon (+1.6%) and Apple (+1.0%).

- Nvidia meanwhile is back to flat, gaining intraday with a lack of fresh headlines at the China trade delegation press conference after Bessent-He talks. It had dragged pre-market and earlier in the session after China said it violated antitrust regulations with its acquisition of Mellanox.

- Leaders: Communication services (+2.0%), consumer discretionary (+1.4%) and IT (+0.5%).

- Laggards: Health care (-1.0%), consumer staples (-0.8%) and materials (-0.6%).

- The tech-heavy nature of day’s gains unsurprisingly sees NDQ outperform at +0.65% (20 pts off earlier all-time highs of 24274.80). The Russell 2000 also performs well (+0.4%) whilst the Dow Jones lags (+0.05%).