US STOCKS: Midday Equities Roundup: AI Chip Demand Gains Momentum Again

- Stocks are firmer early Thursday, off early highs after the Nasdaq climbed to the highest level since last Friday when the tech heavy index marked a new record high of 23,119.91. Advances in SPX eminis and the DJIA less ambitious as markets early stages of the latest earnings cycle.

- Currently, the DJIA trades up 63.75 points (0.14%) at 46,315.77, S&P E-Minis up 11.5 points (0.17%) at 6,725.5, Nasdaq up 106.3 points (0.5%) at 22,773.36.

- Unsurprisingly, Information Technology sector shares led gainers, particularly semiconductor makers as AI demand gained momentum. Bloomberg reported earlier that Taiwan Semiconductor Manufacturing Co "hiked its projection for 2025 revenue growth to the mid-30% range, sending a strong signal of confidence in demand for components like Nvidia Corp chips that power AI."

- Leading chip makers included: Micron Technology +7.27%, Western Digital +6.40%, Seagate Technology +4.70% and Super Micro Computer +4.06%.

- Pharmaceuticals followed close behind with: Bio-Techne +4.28%, Hologic +3.99%, Align Technology +3.85%, Charles River Labs +3.50% and Insulet Corp +3.00%.

- Conversely, Financial and Industrial sector shares underperformed, insurance names weighed on the former: Marsh & McLennan -6.36%, Brown & Brown -4.64%, Arthur J Gallagher -4.57%, Chubb -4.19% and Aon -4.12%.

- Verisk Analytics -4.35%, Copart -2.06%, Jacobs Solutions -1.69% and Uber Technologies -1.53% weighed on the Industrials sector.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: EU Officials On Inflation Implications From CO2 Trading Scheme

European officials and parliamentarians look at the implications of ETS2 CO2 trading rules for inflation. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

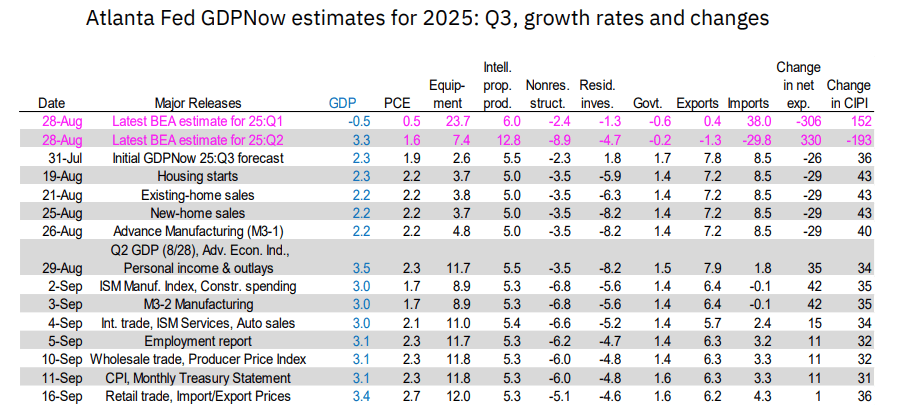

US OUTLOOK/OPINION: GDPNow Suggests Pickup In Private Domestic Demand In Q3

The Atlanta Fed's latest GDPNow estimate for Q3 jumped to 3.41% from 3.09% in the last full update on September 10 (and 3.3% posted in Q2). This was very much a domestic demand-driven upgrade, with real PCE now seen contributing well over half of growth (1.85pp vs 1.54pp in the previous estimate) thanks to better-than-expected advance retail sales.

- The underlying details from the GDPNow estimate imply final sales to private domestic purchasers, closely watched by the Fed, is growing at around 2.4%, a pickup after 1.9% in both Q1 and Q2.

- "After recent releases from the US Census Bureau, US Bureau of Labor Statistics, and Treasury's Bureau of the Fiscal Service, the nowcasts of third-quarter real personal consumption expenditures growth and real gross private domestic investment growth increased from 2.3 percent and 6.2 percent, respectively, to 2.7 percent and 6.9 percent, while the nowcast of the contribution of net exports to third-quarter real GDP growth decreased from 0.23 percentage points to 0.08 percentage points."

- The next release will be Wednesday after housing starts/permits data.

BOC: MNI BoC Preview-Sept 2025: Cuts To Resume On Softening Data

The Bank of Canada is expected to cut its benchmark overnight rate by 25bp to 2.50% on Wednesday September 17. This comes after three consecutive holds, amid a period in which activity and labour market data proved more resilient than expected in the face of the US-Canada trade conflict.

- Data since the July meeting have been almost unambiguous in tilting the balance toward a further easing, culminating with softer core CPI trends in August’s inflation report released on the eve of the decision.

- Almost all Canadian analysts expect a 25bp cut to be announced Wednesday.

- A 25bp reduction would bring rates toward the lower end of the BOC’s estimated neutral range.

- With no Monetary Policy Report released at this meeting and thus no new economic projections, there will be initial attention on the decision statement which is expected to remain non-committal on future cuts but retain the overall easing bias. That’s a tone likely to be echoed at the press conference.

- While Governing Council’s message will probably reiterate they are proceeding “carefully” with a meeting-by-meeting approach, the overall meeting communications will leave the door open to another rate cut in October if data continue to develop in a similar direction over the interim period.

- Views on the BOC terminal rate are split between those analysts who see one further cut beyond this week (2.25% terminal), and those who see two more (2.00%, so slightly below what would largely be considered neutral). That matches markets pricing between 1 and 2 cuts by end-2026 in addition to this week’s.