US TSYS: Tsys Whipsaw Lower, Risk Sentiment Tested on Policy & Trade

Oct-15 19:57

- Treasuries ratcheted lower Wednesday, buffeted by several rounds of selling and a reversal in overall sentiment that triggered selling in equities.

- Treasuries retreated through early overnight levels, coinciding with EU headlines that the EU is discussing "preferential treatment to give domestic firms bidding for public contracts worth about €2.5 trillion ($2.9 trillion) a year," Bbg. Note, however, 10Y Bund also declined and is rebounding.

- Treasuries moderated near session lows following comments by Fed Gov Miran (voter) at a Nomura Research Forum stated that US-China trade tensions tied to rare-earth curbs "pose significant downside risks". Ironically, this comes after after Treasury Sec Bessent suggested the possibility of a "longer tariff truce with China tied to rare-earth imports" helped risk sentiment earlier.

- Currently, Tsy Dec'25 10Y contract trades 113-09 (-4) vs. 113-06.5 low, yld tapped 4.0455% high; curves flatter/off lows: 2s10s -1.490 at 53.445 (51.608 low), 5s30s -1.561 at 100.734 (98.827 low). Initial technical support at 112-26 (20-day EMA) followed by the 50-day EMA at 112-16. A clear break of the average would expose 111-13+, the Aug 18 low and a key support.

- Cross asset: Bbg US$ index off lows, -3.35 at 1211.09 (1210.10 low), stocks off early highs: DJIA down down 72.67 points (-0.16%) at 46,200.11, S&P E-Minis up 12.5 points (0.19%) at 6,699.25, Nasdaq up 91.7 points (0.4%) at 22,611.45.

- Look ahead: Thursday's Retail Sales, PPI and Business Inventories suspended due to the Gov shutdown. On the other hand, Weekly Jobless Claims on a state level likely to be gradually parsed out.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Trading Closer To Its Recent Highs

Sep-15 19:50

- RES 3: 95.995 - 1.618 proj of the Sep 3 - 9 - 10 price swing

- RES 2: 95.865 - 1.000 proj of the Sep 3 - 9 - 10 price swing

- RES 1: 95.780 - High Sep 12

- PRICE: 95.735 @ 20:26 BST Sep 15

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures are trading closer to their recent highs and a short-term bull cycle remains in play. Short-term resistance to watch is last week’s 95.780 high on Sep 12. A break of this level would signal scope for a continuation higher and pave the way for a climb towards 95.865, a Fibonacci projection. Key short-term support has been defined at 95.510, the Sep 3 low.

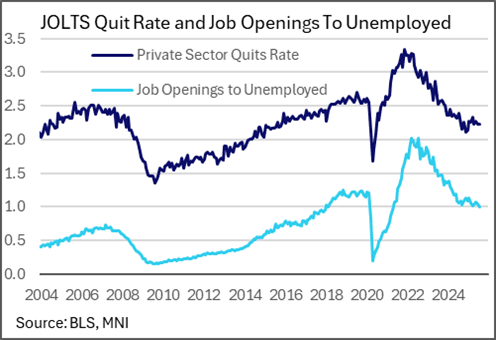

US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Openings Ease Again [5/5]

Sep-15 19:45

- Slower moving indicators also still carry weight as the FOMC assesses broader labor market balance.

- The JOLTS report for July was softer than expected, primarily on the openings front as the ratio of vacancies to unemployed fell to a new recent low.

- Powell at Jackson Hole had pointed to this metric in the category of little changed to only modestly softer over the past year, leaving sensitivity to any subsequent declines here.

- Specifically, the ratio of openings to unemployed fell from 1.05 to 0.99. Whist only marginal at this stage, that’s the first time there have been fewer openings than unemployed since Apr 2021 or, prior to the pandemic, early 2018.

- The quit rate meanwhile was unchanged at 2.01%, continuing to stabilize at low levels having averaged 2.0% since Aug 2024, and actually a little above some 1.9% readings in 2H24 rather than pushing lower still.

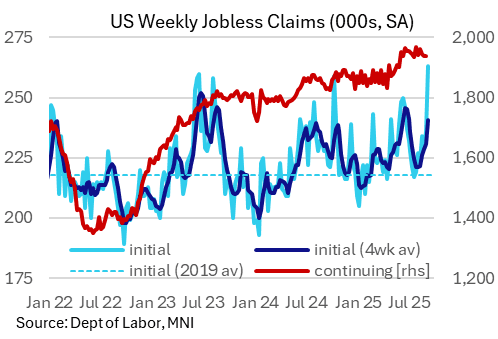

US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Caveated Claims Warning [4/5]

Sep-15 19:40

- As for other timely measures of labor market conditions, weekly jobless claims data have painted a mixed picture.

- The latest initial jobless claims print has fired a warning shot with a surprisingly steep rise to 263k for its highest since 2021, although a large part of this increase was driven by what’s an idiosyncratic-looking increase in Texas. Being the second largest state in the US it shouldn’t be completely looked past, but it does add an asterisk next to the latest spike in what can be noisy data week-to-week.

- Our continued preference is to focus on the four-week average although this too shows an upward trend, now at 241k for a 20k increase since August and its highest since June. We’d start to take a stronger signal of impending labor market weakness if this rate starts to push above 250k in what would break ranges seen over the past two years.

- Continuing claims meanwhile have very roughly plateaued ever since a more concerted push higher back in May and June, a finding that coincidentally tallies with June being the weakest print for payrolls growth as the data currently stand.