MNI ASIA MARKETS ANALYSIS: Tariff Relief Ahead?

HIGHLIGHTS

- Cautious risk-on Tuesday as markets took positive sounding tariff negotiation statements from Trump officials at face value.

- Pres Trump to announce "more tariff relief" at a rally in Michigan this afternoon, "domestic automakers will be happy" WH Deputy Chief of Staff Miller said.

- Projected rate cut pricing rising in the second half of the year compared to this morning's levels (*) as follows: Jul'25 at -39.1bp (-37.6bp), Sep'25 -61.0bp (-57.4bp).

- Treasury quarterly refunding announcement Wednesday Morning

MNI US TSYS: Modest Risk On - Domestic Automakers Hopeful For Tariff Relief

- Treasuries look to finish near near midday highs Tuesday, curves mildly steeper amid decent short end support all day (conditional steepeners via options, Block buying SOFR White packs) as Trump officials reported progress in tariff negotiations without much hard facts.

- Pres Trump to announce "more tariff relief" at a rally in Michigan this afternoon, "domestic automakers will be happy" WH Deputy Chief of Staff Miller said.

- Cautious risk-on support in rates buoyed projected rate cut pricing in the later half of the year (Sep at -61.0bp) while stocks finished near moderate session highs (SPX eminis +35.0 at 5588.0).

- The JOLTS report saw a second month with lower-than-expected job openings, and this time by a greater extent in March. However, layoffs fell to their lowest since June and quit rates surprisingly inched higher.

- US consumer confidence dropped for a 5th consecutive month in April following the November peak per the Conference Board's survey, with the Composite to 86.0 (88.0 expected, 93.9 prior upwardly revised from 92.9) - the lowest since May 2020.

- Focus turns to Wednesday's ADP private jobs data, GDP, Chicago PMI, PCE and Home Sales.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.03), volume: $2.567T

- Broad General Collateral Rate (BGCR): 4.35% (+0.03), volume: $1.047T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.03), volume: $1.011T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $105B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $279B

FED Reverse Repo Operation

RRP usage rises to $157.537B this afternoon from $148.649B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 37.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported better upside call volume on net underlying futures see-saw near midday highs (TYM5 +7.5 at 112-04.5 vs. -07.5 high). Curves mildly steeper (2s10s +.412 at 51.346). Projected rate cut pricing rising in the second half of the year compared to this morning's levels (*) as follows: May'25 at -2.6bp (-2.3bp), Jun'25 at -16.9bp (-16.9bp), Jul'25 at -39.1bp (-37.6bp), Sep'25 -61.0bp (-57.4bp).

SOFR Options:

+20,000 SFRU5 96.00 puts, 10.0 vs. 96.315 to -.32/0.25%

-15,000 SFRN5/0QN5 96.12/96.25 call spd spd, 5.25 midcurve over, steepener

+10,000 SFRZ5 96.75/97.25 call spds, 14.25 ref 96.645

-8,000 0QM5 96.87/97.00/97.25/97.3 call condors, 2.87 ref 96.98

+2,500 0QM5 97.50/98.00/1000 2x3x1 call flys 7.0 vs. 96.365/0.14%

+3,500 0QK5 96.75 puts, 6.5

+5,000 SFRZ5 96.00/96.25/96.50 put trees, 2 ref 96.585

-4,000 0QM5/2QM5 95.87/96.12 put spd strip w/2QM5 96.00/96.25 put spd, 2.5 total

21,000 SFRM5 95.87/96.00/96.25/96.37 call condors

15,400 SFRM5 95.75/95.81 put spds ref 95.895

11,400 SFRM5 95.68 puts, 0.5 last

over 5,900 SFRZ5 95.62 puts, 3.5 last

12,580 SFRZ 95.56/95.68/95.81 put flys ref 96.575

2,500 0QZ5 97.00/97.50 call spds ref 96.935

1,850 SFRK5 95.81/96.18 1x2 call spds ref 95.885

Treasury Options:

+15,000 wk2 TY 112.75 calls, 21

2,500 TYM5 112 straddles,

+5,000 TYM5 109/113 strangles, 35-36

-6,000 TYM5 111.75 straddles, 142 (imp vol 7.22%)

+12,000 TYM5 110/113 strangles, 38-39 vs. 111-25/0.25% (imp vol 7.36%)

20,000 wk1 5Y (exp Fri)/Mon wkly 5Y (exp Mon) 110 call spds ref 108-26.75

6,300 TYM5 113/116 call spds ref 111-27.5

over 4,300 TYM5 114 calls

MNI BONDS: EGBs-GILTS CASH CLOSE: Edges Higher On Soft Data

European FI gained slightly on Tuesday, retracing some of the previous session's weakness.

- Gains were fairly steady through the session, with few major headline/macro catalysts, amid a backdrop of data that was largely on the weaker side of expectations.

- Spanish April preliminary HICP came in firmer than expected, though Spanish GDP came in soft.

- ECB consumer inflation expectations rose for both 1Y and 3Y, though the EC Economic Sentiment survey was weaker than expected.

- Below-consensus US job openings and consumer confidence readings added to the theme.

- ECB's Stournaras sounded cautious on moving rates below 2% (from 2.25% at present); an MNI sources piece debate within the Governing Council ahead of the June rate decision.

- Both the German and UK curves bull flattened, with 10Y Gilts touching 3-week lows. Periphery/semi-core EGB spreads widened modestly, with Portugal underperforming.

- Wednesday's calendar includes French GDP and German retail sales/unemployment, but the highlight will be German, French, and Italian flash April inflation.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 1.736%, 5-Yr is down 1.5bps at 2.044%, 10-Yr is down 2.4bps at 2.497%, and 30-Yr is down 2bps at 2.927%.

- UK: The 2-Yr yield is down 2.3bps at 3.843%, 5-Yr is down 2.8bps at 3.958%, 10-Yr is down 2.9bps at 4.48%, and 30-Yr is down 2.6bps at 5.244%.

- Italian BTP spread up 0.2bps at 111bps / Portuguese up 1.3bps at 55.3bps

MNI EGB OPTIONS: European Rates See Call Buying, Outrights And Spreads

Tuesday's Europe rates/bond options flow included:

- ERU5 98.56c, bought for 3.25 in 6k

- ERU5 98.50/98.625cs vs 97.9375/97.8125ps, bought the cs for 0.75 in 5k

- ERH6 98.5625/98.1875ps 1x2, bought for 5.5 in 5k

- SFIZ5 96.80/97.10cs vs 2NZ5 96.90/97.20cs, bought the front for 0.25 in 9k

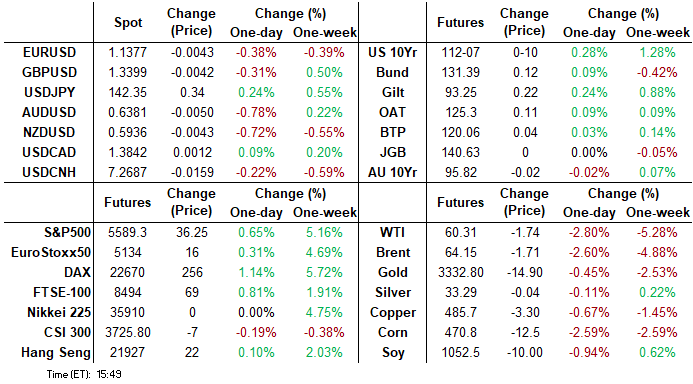

MNI FOREX: G10 Currencies Trade Mixed, Antipodeans Underperform

- Despite sentiment in equity markets not necessarily reflecting it, currencies trade with a moderate risk off tone. This has allowed the likes of AUD and NZD to give up the prior session advance, both falling around 0.65% as we approach the APAC crossover.

- Dented sentiment may be stemming from reports regarding Amazon, who on Tuesday denied a report that it planned to list the costs of President Trump's tariffs next to total prices of products after the White House slammed the mega online retailer earlier in the day. The clash came after PunchBowl News, citing an unnamed source, reported the shopping site will soon display the share of a product's cost that is derived from tariffs rolled out this month.

- For AUDUSD specifically, overnight highs at 0.6450 represented 4-month highs for the pair, which has subsequently drifted steadily lower through the session. Initial key support to monitor is 0.6307, the 50-day EMA, of which a clear break would be a concern for the bullish narrative.

- Elsewhere, lower US yields for a second consecutive session appear to be providing a yen tailwind, with USDJPY pressing towards the 142.00 handle. Technical conditions continue to highlight a dominant downtrend for the pair and below here, 141.49 (Apr 23 low) would provide the first support before the market refocuses its attention on cycle lows at 139.89.

- Economic calendar highlights for Wednesday’s APAC session include Australian CPI and China PMI’s. Later in the session, the focus will be on Eurozone inflation/growth data and US Q1 GDP. Other notable releases include US PCE and ADP, the MNI Chicago PMI and Canada GDP.

MNI FX OPTIONS: Expiries for Apr30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1375-95(E2.7bln), $1.1425(E500mln)

- USD/JPY: Y140.50($1.9bln), Y142.00($1.8bln), Y144.40-50($959mln), Y145.00($1.5bln), Y148.50($716mln)

- AUD/USD: $0.6115(A$1.1bln), $0.6250(A$702mln)

- NZD/USD: $0.5950(N$521mln)

MNI US STOCKS: Late Equities Roundup: Treading Higher

- Stocks are holding moderately higher late Tuesday with Pres Trump trade officials teasing out positive sounding trade negotiation sound bites. Currently, the DJIA trades up 345.02 points (0.86%) at 40575.44, S&P E-Minis up 37 points (0.67%) at 5590, Nasdaq up 115.2 points (0.7%) at 17482.71.

- A mix of IT, Materials, Real Estate and Pharmaceutical sectors led both gainers and losers on the day.

- Tech stocks included Zebra Technologies +7.19%, SBA Communications +6.65%, Honeywell International +5.30%, Cadence Design Systems +5.13%. Elsewhere, Sherwin-Williams +5.66%, American Tower +4.76%, A O Smith +4.40% and Labcorp Holdings +4.36%.

- Conversely, Regeneron Pharmaceuticals led laggers -7.40% on the day, Brown & Brown -6.03%, NXP Semiconductors -5.81%, Alexandria Real Estate -5.17%, Insulet -3.66%, UnitedHealth Group -2.24% and Super Micro Computer -2.07%.

- Latest earnings expected after the close: Booking Holdings, Mondelez International, Caesars Entertainment, Seagate, Starbucks, Frontier Communications, Expand Energy, Fair Isaac, Visa, BXP, PPG, Edison Int, ONEOK, First Solar, CoStar Group and Snap Inc.

MNI EQUITY TECHS: E-MINI S&P: (M5) Resistance To Watch Is At The 50-Day EMA

- RES 4: 5837.25 High Mar 25 and a bull trigger

- RES 3: 5773.25 High Apr 2

- RES 2: 5619.66 50-day EMA and a key resistance

- RES 1: 5597.25 High Apr 29

- PRICE: 5588.50 @ 1452 ET Apr 29

- SUP 1: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 2: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 3: 4832.00 Low Apr 7 and the bear trigger

- SUP 4: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

The corrective bull cycle in S&P E-Minis that started on Apr 7, remains in play. The contract has breached a number of important short-term resistance points. Price has cleared the 20-day EMA and pierced 5528.75, the Apr 10 high. The next key resistance is 5619.66, the 50-day EMA. A clear breach of this EMA would strengthen a bull theme. Initial key support lies at 5127.25, the Apr 21 low. A break would be bearish

MNI COMMODITIES: WTI Slides Amid Trade War Uncertainty, Gold Edges Lower

- Trade war concerns have continued to weigh on energy markets today as China/US tensions drag on. High Kazakh supply and the unwinding of OPEC+ cuts add to the pressure of trade war demand fears.

- WTI Jun 25 is down by 2.8% at $60.3/bbl.

- Some positive news did at least come from reports that China has waived the 125% tariff on US ethane imports imposed earlier this month, Reuters said citing two sources.

- A medium-term bearish theme in WTI futures remains intact, with sights on initial support at $58.29, the April 10 low, followed by $54.67, the April 9 low and the bear trigger.

- Meanwhile, spot gold has also fallen by 0.8% to $3,316/oz, as the yellow metal continues to consolidate after hitting a fresh record high at $3,500 last week.

- Gold remains 6% higher MTD amid ongoing haven demand due to the trade war and associated dollar weakness.

- From a technical perspective, the trend needle for gold still points north, and the latest move down appears corrective. The retracement has allowed an overbought condition to unwind.

- Moving average studies are unchanged and remain in a bull-mode position, highlighting a dominant uptrend. The next objective is $3,547.9, a Fibonacci projection. Initial firm support to watch lies at $3,239.5, the 20-day EMA.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/04/2025 | 0530/0730 | *** | GDP (p) | |

| 30/04/2025 | 0530/0730 | ** | Consumer Spending | |

| 30/04/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/04/2025 | 0600/0800 | ** | Retail Sales | |

| 30/04/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 30/04/2025 | 0645/0845 | *** | HICP (p) | |

| 30/04/2025 | 0645/0845 | ** | PPI | |

| 30/04/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/04/2025 | 0755/0955 | ** | Unemployment | |

| 30/04/2025 | 0800/1000 | *** | GDP (p) | |

| 30/04/2025 | 0800/1000 | *** | GDP (p) | |

| 30/04/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/04/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/04/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/04/2025 | 0900/1100 | *** | HICP (p) | |

| 30/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 30/04/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP Q/Q | |

| 30/04/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP Y/Y | |

| 30/04/2025 | 1000/1200 | ** | PPI | |

| 30/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/04/2025 | 1200/1400 | *** | HICP (p) | |

| 30/04/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/04/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/04/2025 | 1230/0830 | *** | GDP | |

| 30/04/2025 | 1230/0830 | *** | Employment Cost Index | |

| 30/04/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/04/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/04/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/04/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/04/2025 | 1400/1000 | *** | Personal Income and Consumption | |

| 30/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/04/2025 | 1530/1630 | BOE Lombardelli At New Economics Teacher Training Launch | ||

| 30/04/2025 | 1730/1330 | BOC Meeting Minutes | ||

| 01/05/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/05/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/05/2025 | 0130/1130 | ** | Trade price indexes | |

| 01/05/2025 | 0130/1130 | ** | Trade Balance | |

| 01/05/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |