MNI ASIA MARKETS ANALYSIS: Stocks Retreat On Fiscal Concerns

HIGHLIGHTS

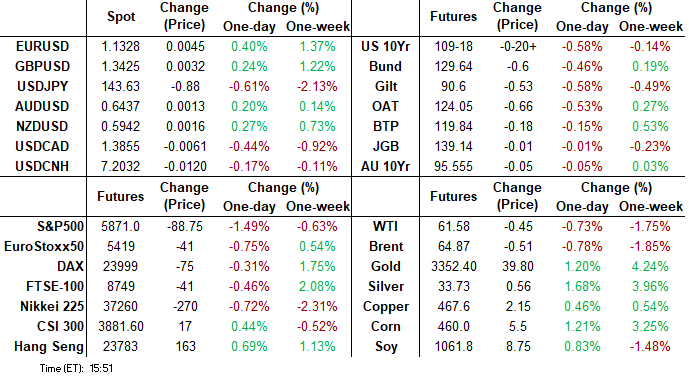

- Treasuries look to finish near late session lows, curves bear steepen as bond yields climb to the highest levels since late October 2023 Wednesday: 5.0955%.

- No economic data, headline or outright flow to site for the move other than trepidation over Pres Trump's tax & spending bill estimated to increase the deficit appr $3.3 trillion over 10 years.

- Lawmakers continued to debate the bill and passage remained uncertain despite Pre Trump personally haranguing GOP holdouts.

US TSYS

MNI US TSYS: Massive Deficit Estimates Tied to Tax/Spending Bill Weighing on Bonds

- Treasuries look to finish near late Wednesday session lows, curves bear steepening: 2s10s +6.792 at 58.019 - highest level since May 1. Heavier volumes tied to Jun/Sep Tsy futures rolls, 5s well over 1M.

- No economic data, headline or outright flow to site for the move other than trepidation over Pres Trump's tax & spending bill estimated to increase the deficit appr $3.3 trillion over 10 years. Lawmakers continued to debate the bill and passage remained uncertain despite Pre Trump personally haranguing GOP holdouts.

- Treasury futures extend session lows after the $16B 20Y Bond auction (912810UL0) tailed, drawing a high yield of 5.047% vs 5.035% When-Issued yield at the cutoff; 2.46x bid-to-cover vs. 2.63x prior. Bonds yield climbed to 5.0955% intraday high - last seen late October 2023. 10Y yield up to 4.5825% (+.0956).

- The Jun'25 10Y futures contract slipped to 109-13.5 low (-25) briefly -- through initial technical support at 109-18.5 (May 15 low) before bouncing to 109-19 - strengthening a bearish theme and exposing key support at 109-08, Apr 24 low and a bear trigger.

- Cross asset update: Gold up 33.4 at 3323.42, stocks weaker with rise in bond yield (SPX emini -95.0 to 5864.75), Crude retreating (WTI -0.62 at 61.41).

- Look ahead to Thursday's data: Weekly Claims at 0830ET, Flash PMIs at 0945ET, Exist Home Sales at 1000ET and KC Fed Mfg Activity at 1100ET.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.27% (-0.02), volume: $2.554T

- Broad General Collateral Rate (BGCR): 4.26% (-0.02), volume: $1.060T

- Tri-Party General Collateral Rate (TCR): 4.26% (-0.02), volume: $1.023T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $294B

FED Reverse Repo Operation

RRP usage rebounds to $162.082B this afternoon from $136.033B yesterday, total number of counterparties at 41. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Aside from a large scale buyer of Jun'25 SOFR calls, flow leaned towards low delta put structures Wednesday as underlying futures weaker, near lows while projected rate cut pricing drifts near early morning levels (*) as follows: Jun'25 at -1.4bp (-0.5bp), Jul'25 at -7bp (-6.7bp), Sep'25 at -20.8bp (-19.6bp), Oct'25 at -33.5bp (-33.7bp), Dec'25 at -50.6bp (-50.7bp).

SOFR Options:

over +100,000 SFRM5 96.50 calls, 0.5

-4,000 SFRZ5 95.87/96.00 put spds, 5.75

+3,000 0QX5 96.00 puts, 10.5 ref 96.62

+20,000 SFRZ5 95.37/95.62 put spds, 1.5 ref 96.17

-6,000 SFRU5 95.81 / SFRZ5 95.68 put spds, 5.0 net/Sep over

-2,500 SFRM5 95.75 puts, 8.25 ref 95.68

+4,000 0QM5 96.25 puts, 2.5 vs. 96.53

-2,000 2QZ5 95.75/97.25 strangles, 20.75 ref 96.43

Block 5,000 SFRU5 96.12/96.37 call spds, 3.5 ref 95.89

1,900 SFRM5 95.68/95.75/95.81 call flys ref 95.68

2,600 SFRM5 95.75/95.87 2x1 put spds ref 95.68

+6,000 SFRM5 95.68 puts, 2.5

2,000 SFRM5 95.75 put vs. 0QN5 96.12 put, 0.5 net flattener

+1,000 SFRM5 95.50/95.68 2x1 put spds cab

+5,000 0QM5 96.12 puts, 1.0 vs. 96.575 to -.58/0.05%

-2,000 2QN5 96.43 puts, 14.5 vs. 96.50/0.44%

Treasury Options:

11,491 TYN5 100/108.5/110 broken put flys ref 109-28

3,800 FVU5 106.25/107.5 2x1 put spds ref 107-18.75

2,000 FVM5 107.5/107.75 call spds 6 ref 107-16.5

+25,000 TYN5 111.5 calls, 18 vs. 109-28/0.20%, appr 6.78% vol (total volume over 58k on day

-3,500 TYN5 110 straddles, 143, appr 6.63% vol

1,250 USM5 112/USN5 109 put spds

20,000 TYM5 110.5/111 call spds, 2 ref 109-29

over 3,300 USN5 109 puts, 50 ref 111-19

+8,000 TYM5 111/112/113 call flys, 1.0

(another 3k TYM5 112 calls, 1 ref 109-30)

+5,000 TYM5 109.5 puts, 6

+3,000 TYU5 107.5 puts, 41-42

+3,000 FVM5 108 calls, 2

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Again Post-UK CPI

Gilt underperformance vs Bunds extended for a second day Wednesday.

- UK CPI data was firmer than expected, particularly services inflation, even when adjusting for Easter effects.

- This drove a sell-off in Gilts which lasted throughout the morning, exacerbated by continued weakness in Treasuries.

- Though UK yields closed off the highs, they (10Y) reached the highest levels since early April.

- While Bunds weakened in sympathy with Gilts, the 10Y UK/Germany spread closed close above 210bp for the first time in a month.

- Periphery / semi-core EGBs traded mixed, with Greece a notable outperformer.

- At an MNI event this morning, ECB's Kazaks said that "If the current baseline holds, we will soon reach the terminal rate".

- Thursday's data highlight is May flash PMIs, while we also get multiple speakers including BOE's Breeden, Pill, and Dhingra, and ECB's Nagel, Holzmann and Guindos (and the accounts of the April ECB meeting).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.9bps at 1.871%, 5-Yr is up 4.2bps at 2.193%, 10-Yr is up 4bps at 2.646%, and 30-Yr is up 4.8bps at 3.136%.

- UK: The 2-Yr yield is up 4bps at 4.083%, 5-Yr is up 4.5bps at 4.241%, 10-Yr is up 5.4bps at 4.757%, and 30-Yr is up 6bps at 5.518%.

- Italian BTP spread unchanged at 99.6bps /Greek down 1.8bps at 74bps

MNI EGB OPTIONS: Busy In Sonia Flows After Above-Expected UK CPI

Wednesday's Europe rates/bond options flow included:

- OEM5 118.00p, bought for 3.5 in 3k.

- ERU5 98.375/98.50/98.625/98.75 call condor 4K given at 1.0

- ERZ5 98.375/98.625 call spread paper paid 5 on 5K

- SFIM5 95.95/95.90/95.85/95.80 put condor 10K given at 2

- SFIU5 96.00/96.20cs 1x2, bought for 2.75 in 10k

- SFIZ5 95.50/96.00/96.50c fly vs 97.00/96.50ps 1x2, sold the fly at -15 in 18.5k

- SFIZ5 96.30/96.55/96.80 call fly, bought for 3.75 in 18k

- SFIZ5 96.15/96.00/95.80 broken put fly paper paid 1.5 on 5K

MNI FOREX: USD Dip Holds Through London Close

- The USD dip persisted into the Wednesday close, with the USD Index slipping to the lowest level since early May. Moves began in earnest at the NY crossover, as a re-steepening of the US curve and run lower in US equity futures triggered another phase of the 'Sell the US' theme in global markets.

- UK CPI data came in well ahead of expectations, with tax changes for transport and the timing of Easter driving price gains well ahead of both market and BoE expectations. GBP/USD rallied in response, with the pair hitting a new multi-year high at 1.3469. These gains were short-lived, however, despite a further contraction of rate cut pricing across UK OIS markets.

- We note that GBP/USD has struggled to maintain gains above the 1.34 handle on several occasions already this year, as well as in 2024, 2019 and 2020. Spot gains today saw a brief print at 1.3469, but markets have already reversed ~60 pips off the high to contain the overall bullish breakout. The keeps focus on the bearish tweezer candle formation printed on April 28/29, which could mark a near-term top. 1.3342 undercuts as first support, ahead of the more meaningful 50-day EMA at 1.3137. A move through here would challenge the near-term bullish trend narrative.

- New daily lows for USD/CAD and EUR/CAD were printed through the London close, shrugging off the slippage in crude oil prices after the surprise in crude oil inventories at the weekly DoE numbers. The price action keeps the trend condition in USDCAD bearish, and confirms recent gains as corrective. Moving average studies are in a bear-mode position, highlighting the dominant downtrend that targets 1.3744, a Fibonacci retracement.

- Thursday trade should be led by prelim PMI data for May, with the core European states seen posting only minor improvements in growth prospects across the month - as firms across both manufacturing and services sectors remain under pressure from the uncertainties surrounding tariffs and global geopolitics. Weekly jobless claims data are the US calendar highlight, while the central bank speaker slate also picks up. Appearances are due from ECB's Holzmann, Vujcic, Elderson, Escriva & de Guindos, Fed's Barkin & Williams, BoE's Breeden, Pill & Dhingra as well as RBA's Hauser.

MNI FX OPTIONS: Expiries for May22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1175(E1.9bln), $1.1300-15(E828mln), $1.1390-00(E510mln)

- GBP/USD: $1.3260-70(Gbp1.5bln), $1.3390-95(Gbp673mln)

- EUR/GBP: Gbp0.8590-00(E790mln)

- USD/JPY: Y143.50($602mln)

- USD/CAD: C$1.3700($659mln), C$1.4050($1.3bln)

MNI US STOCKS: Late Equities Roundup: Pharmaceuticals, Estate Management Lagging

- Stocks retreated again after bouncing off early second half lows Wednesday, taking cues from higher Treasury Bond yield, not to mention a large sell program (1,891 names, largest since April 10). Trading desks had cited this morning's higher bond yields partly triggered by fiscal developments (or lack thereof) as lawmakers continue to discuss Pres Trump's tax/spending bill.

- Investor sentiment flagged amid concerns the "big beautiful" tax & spending deal will increase the deficit an estimated $3.3 trillion over 10 years, weighing on equities as well as the Greenback (Bbg US$ index -5.22 at 1217.49).

- Currently, the DJIA trades down 696.7 points (-1.63%) at 41980.32, S&P E-Minis down 74.75 points (-1.25%) at 5884.5, Nasdaq down 183.1 points (-1%) at 18959.6.

- Health Care and Real Estate sectors underperformed in late trade, pharmaceuticals companies continued to weigh on the former with Moderna -7.29%, Bio-Techne -6.02% and Charles River Laboratories -5.32%. Estate management and investment trust stocks weighed on the former with CBRE Group -4.84%, Alexandria Real Estate -4.38%, Iron Mountain -3.69% and Weyerhaeuser -3.62%.

- Communication Services and Consumer Staples sectors outperformed in late trade, interactive media and entertainment buoyed the Communication Services sector with Alphabet +3.68%, Match Group +0.34% and Netflix +0.32%. Limited gainers in Staples included Philip Morris International +0.34%, Monster Beverage +0.21% and Coca-Cola Co +0.14%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bull Cycle Intact

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5993.50 High May 20

- PRICE: 5886.75 @ 1410 ET May 21

- SUP 1: 5837.25/5703.54 High Mar 25 / 50-day EMA

- SUP 2: 5455.50 Low Apr 30

- SUP 3: 5355.25 Low Apr 24

- SUP 4: 5127.25 Low Apr 21 and a key support

A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective. An important resistance at 5837.25, the Mar 25 high and a bull trigger, has recently been cleared. This has strengthened the current bullish theme, and paves the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5703.54, the 50-day EMA.

MNI COMMODITIES: Precious Metals Extend Gains, Crude Falls

- Spot gold has risen by a further 0.7% today amid concerns about US fiscal policy and ongoing geopolitical tensions in the middle east.

- The move has brought the yellow metal back above the $3,300/oz level, currently trading at $3,314/oz.

- The gains signal the end of the corrective phase for gold between Apr 22 - May 15. Medium-term trend signals remain bullish, with moving average studies in a bull-mode position, highlighting a dominant uptrend.

- A continuation higher would open $3,435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3,121.0, the May 15 low.

- Similarly, silver has also rallied by another 0.9% to $33.4/oz today, bringing the precious metal to its highest level since April 29.

- A bullish theme in silver remains intact, with resistance to watch at $33.686, the Apr 25 high. Clearance of this level would confirm a resumption of the uptrend, opening $34.590, the Mar 28 high.

- Meanwhile, crude reversed earlier gains after an unexpected rise in US crude stocks in EIA data today.

- WTI Jul 25 is down by 0.9% at $61.5/bbl.

- For WTI futures, attention remains on support at $54.33, the Apr 9 low and bear trigger. Key resistance to watch is $62.82, the 50-day EMA, a clear break of which would highlight a stronger reversal, opening $65.82, the Apr 4 high.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 22/05/2025 | 0600/0700 | *** | Public Sector Finances | |

| 22/05/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/05/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 22/05/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 22/05/2025 | 1050/1150 | BOE's Breeden On Climate Panel | ||

| 22/05/2025 | 1100/1200 | BOE's Dhingra On UK Productivity Panel | ||

| 22/05/2025 | 1130/1330 | ECB April Minutes Released | ||

| 22/05/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 22/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 22/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 22/05/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/05/2025 | 1230/1330 | BOE's Pill At MonPol Conference (Text 16:30BST) | ||

| 22/05/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 22/05/2025 | 1400/1000 | *** | NAR existing home sales | |

| 22/05/2025 | 1400/1000 | * | Services Revenues | |

| 22/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 22/05/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 22/05/2025 | 1500/1700 | ECB's Elderson Dinner Speech at Biodiversity Day | ||

| 22/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 22/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 22/05/2025 | 1535/1735 | ECB's de Guindos Speech in Madrid | ||

| 22/05/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 22/05/2025 | 1800/1400 | New York Fed's John Williams | ||

| 22/05/2025 | 1900/1500 | New York Fed's Roberto Perli | ||

| 23/05/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 23/05/2025 | 2330/0830 | *** | CPI |