MNI ASIA MARKETS ANALYSIS: Steady Fed, Policy Patience

HIGHLIGHTS

- FOMC held interest rates steady for a third meeting Wednesday, opting to take a wait-and-see stance as it assesses the effect of gyrating trade policies on the economy’s prospects and the path of inflation.

- Stocks bounced late after Pres Trump rescinds global chips curb "amid AI restrictions debate", scaling back half the move ahead of the close.

- The greenback extends late session highs as the Federal Reserve awaits further clarity.

MNI US TSYS: Near Highs After Fed Held Rates Steady, Remain Patient

- Treasuries finish higher after the Federal Reserve held rates steady at 4.25-4.5%, reiterating the patience as the US economy is still solid. "The labor market is solid. Inflation is low. We can afford to be patient as things unfold. There's no real cost to our waiting at this point.

- Powell added that while there has been some "souring sentiment ... the shock from tariffs hasn’t hit yet. We’re going to be looking at both sentiment and real economic data. It’s not at all clear what the appropriate response for monetary policy is. Unemployment hasn’t gone up, job creation is fine and layoffs aren’t increasing in any kind of impressive way," Powell added.

- Tsy Jun'25 10Y futures are +7 at 111-17 after the bell (111-04 low/111-22 high), still inside technical support and resistance levels. Curves mixed, 2s10s -1.551 at 49.222, 5s30s +.578 at 90.707.

- Cross asset update: Bbg US$ index +6.41 at 1222.75; stocks firmer after Tump rescinds global chip curbs (SPX eminis +26.5 at 5652.50), Gold weaker (-63.20 at 3368.51), Crude lower (WTI -1.13 at 57.96).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (-0.01), volume: $2.620T

- Broad General Collateral Rate (BGCR): 4.31% (+0.00), volume: $1.075T

- Tri-Party General Collateral Rate (TCR): 4.31% (+0.00), volume: $1.035T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $120B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $295B

FED Reverse Repo Operation

RRP usage climbs to $154.859B this afternoon from $129.858B yesterday, total number of counterparties at 46. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported mixed SOFR & Treasury options overnight, leaning towards low delta put structures on modest volumes. Underlying futures weaker in the short end, curves twist flatter in the lead-up to today's FOMC annc. Projected rate cut pricing looks steady to mildly lower vs. late Tuesday levels (*) as follows: May'25 steady at -0.5bp, Jun'25 at -8.2bp (-8.4bp), Jul'25 at -23.8bp (-25.2bp), Sep'25 -43.8bp (-46.2bp).

SOFR Options:

+20,000 SFRU5 95.75.95.87 2x1 put spds, 1.75 ref 96.14

+10,000 SFRU5 95.75 puts, 2.25 ref 96.155

-5,000 0QZ5 97.50/98.00 call spds 9.0 ref 96.90

Block, 6,000 SFRU5 95.81/SFRZ5 95.68 put spds, 1.0 net/Sep over

Update, over -14,000 SFRH6 96.62 straddles sold on day from 80-79 ref 96.655

+20,000 SFRZ5 95.68 puts, 3.5 ref 56.455

+4,000 SFRU5 95.62/95.87 put spds w/ SFRZ5 95.87/96.12 call spd strip, 22.5

+8,000 SFRN5 95.81/95.93/96.06 put vlys vs. 4,000 96.18/96.31 call spds, 1.5 net

-2,000 SFRZ5 96.43 straddles, 62.0 ref 96.455

-2,500 SFRH6 96.62 straddles, 80.0 ref 96.655

+4,000 SFRU5 95.68/95.81/96.00 2x3x1 put flys 1.25 ref 96.15

-2,000 SFRU5 96.00 puts, 12.0 ref 96.15

+3,000 SFRM5 SFRM5 95.75/95.81/95.87 put flys, 0.5 ref 95.785

-5,000 0QU5 95.50/96.00 put spds, 3.0 vs. 96.81/0.08%

+4,000 SFRZ5 96.50/2QZ5 96.75 call spds, 0.25 net

4,000 SFRZ5 97.50 calls, 8.5 ref 96.47/0.10%

5,000 SFRU5 96.12/96.50/96.68 1x3x2 broken call flys ref 96.145

+2,000 SFRN5 95.87/96.12 put spds 7.5 over SFRU5 95.62/95.81 put spds

3,800 SFRK5 95.68 puts, .25 ref 95.78 to -.785

1,250 0QM5 97.00/97.75 call spds vs. 2QM5 96.93/97.68 call spds

+4,000 0QK5 96.50/96.62 put spds, 2.5 ref 96.785

1,500 0QM5 96.31/95.56 put spds ref 96.80

2,000 0QM5 97.12/2QM5 97.00, 0.0 call spds

Treasury Options:

-11,500 TYM5 113 calls, 11 ref 111-16

+3,000 TYM5/TYQ5 111.5 straddle spds 130 net

5,000 wk2 FV 110/110.5/111 put flys

4,200 TYM5 109.25/111 2x1 put spds vs. 111.5/113.25 1x2 call spds

over 3,000 wk2 TY 110.5/111.75 strangles ref 111-07.5 (exp Fri)

6,700 TUN5 103.25/103.5/103.62/103.75 put condors ref 103-30.75

2,000 FVN5 106.5/107.5 put spds vs. 109/110 call spds

appr 10,000 TYM5 109.5 puts, 7 last

+2,000 TYM5 109.25/110.25 put spds, 12

2,500 TYM5 109/110 put spds, ref 111-08

over -3,400 TYM5 111.5 calls, 31 last

MNI BONDS: EGB-GILTS CASH CLOSE: Curves Bull Flatten Ahead Of BOE Tomorrow

The German and UK cash curves bull flattened Wednesday, with Bunds lightly outperforming Gilts.

- There was no obvious headline trigger for the bid that began mid-morning, but strength extended through the session as equities and oil/gas benchmarks moved away from highs.

- 10-year Bund yields ended the session down 6.5bps to 2.47%, with Gilts down 5.4bps to 4.46%.

- The space largely brushed aside a Reuters sources article detailing German defence spending plans, with the piece lacking clarity on whether the touted E60bln of additional spending is for 2025 alone or split across the current parliamentary term.

- Today’s LT OAT and 5-year Gilt auctions saw solid results.

- 10-year EGB spreads to Bunds tightened through the morning, but the moves partially unwound in the afternoon alongside continued equity weakness.

- Eurozone data (strong German factory orders, weak Italian retail sales and in-line Eurozone retail sales) were not market movers.

- Tomorrow’s focus is on the BOE decision. An outcome other than a 25bp cut would be surprising but there will be a number of things to watch: any changes to the guidance and the inflation / growth forecast changes, the vote split and the introduction of new scenarios. (MNI preview here).

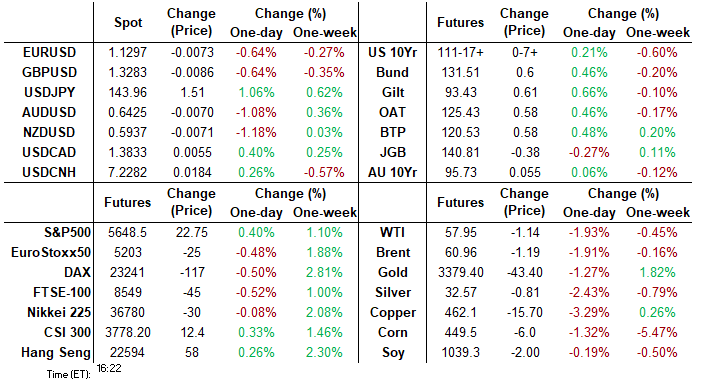

MNI FOREX: Greenback Extends Session Highs as Fed Awaits Further Clarity

- The US dollar is firmer on Wednesday, as the USD Index continues a consolidatory phase between 99.00/100.00. Losses in G10 have been most pronounced for the likes of JPY, AUD and NZD, while the Swiss Franc has reversed yesterday’s weakness and is among the best performers Wednesday.

- USDJPY remained the key focus for FX volatility on Wednesday, where initially a positive reaction to US/China talks progress prompted a firm recovery from the 142.40 lows to around 143.20 overnight in Asia. Following the release of the Fed statement, some dovish caveats and comments from Trump on not rolling back China tariffs saw USDJPY briefly slip back below 143.00. However, this sentiment was short-lived, and Chair Powell’s nod to a patient approach and awaiting further clarity prompted a swift reversal to fresh session highs. The pair is pushing 143.85 as we approach the APAC crossover.

- For AUDUSD, today’s 1.0% decline stalls a prior 3-day winning streak that prompted the pair to print fresh recovery highs at 0.6515. The recent breach of 0.6450, the Apr 29 high, confirms a resumption of the uptrend and maintains the current sequence of higher highs and higher lows.

- Late gains for the dollar helped EURUSD slip to session lows just above the 1.13 handle, whole cable also now trades below 1.33.

- The Swiss Franc notably outperforms on a relative basis. We have noted that recent recovery highs for USDCHF matched perfectly with the prior breakdown point of 0.8333, the 2023 low, likely helping the resumption of weakness in recent sessions. Furthermore, the pair briefly dipped below a couple of daily lows from late April around the 0.8200 mark, keeping bearish conditions firmly intact for now.

- Focus on Thursday turns to other G10 central banks, with decisions from Sweden, Norway and the Bank of England all scheduled. Jobless claims highlight the US calendar.

MNI US STOCKS: Late Equities Roundup: Off Post-FOMC Lows

Stocks rebound off lower levels following headline that Pres Trump rescinds global chips curb "amid AI restrictions debate". Stocks rallied to the following levels: DJIA up 391.52 points (0.96%) at 41226.44; S&P E-Mini Future up 40.25 points (0.72%) at 5668.5; Nasdaq up 104.6 points (0.6%) at 17801.08; but scaled back half the move ahead the close.

- Stocks remain mixed late Wednesday, off initial lows following the FOMC announcement to leave rates steady. The Dow remains higher after trading weaker since Monday - sentiment cautiously buoyed ahead US/China trade talks expected in Geneva over the weekend.

- Currently, the DJIA trades up 133.14 points (0.33%) at 40973.79, S&P E-Minis down 10.25 points (-0.18%) at 5617.5, Nasdaq down 101.2 points (-0.6%) at 17592.12.

- Health Care and Consumer Discretionary sectors outperformed in late trade, leading gainers in the former include Charles River Laboratories that surged 18.80% higher after report better than expected earnings and rising outlook, Cencora +4.82%, IQVIA Holdings +4.62%, Centene +4.36% and West Pharmaceutical +3.92%. Meanwhile, Discretionary stocks included: Deckers Outdoor +3.27%, NIKE +2.51% and Best Buy +2.40%.

- Consumer Services and Information Technology sectors continued to underperform, interactive media and entertainment shares weighing on the former. Notably, Alphabet trades -8.02% on the back of Apple's Cue, who talks up that they're exploring adding an AI search function to their native browser - and may select Perplexity or Anthropic as options for the product.

- Laggers in the IT sector included Arista Networks -5.75%, Super Micro Computer -4.68%, Crowdstrike Holdings -4.48% and Apple -1.57%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bull Cycle Intact

- RES 4: 5864.43 200-dma

- RES 3: 5837.25 High Mar 25 and a bull trigger

- RES 2: 5773.25 High Apr 2

- RES 1: 5724.75 High May 2

- PRICE: 5638.75 @ 14:27 BST May 7

- SUP 1: 5536.59 20-day EMA

- SUP 2: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 3: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 4: 4832.00 Low Apr 7 and the bear trigger

Bullish conditions in S&P E-Minis remain intact. The contract has breached the 50-day EMA, at 5622.98. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5536.59, the 20-day EMA.

MNI COMMODITIES: Crude Falls, Gold, Copper Pull Back

- Oil prices have lost ground in US hours, as Mideast tensions have waned and headlines suggest limited optimism for US-China trade war progress.

- WTI June 25 is down by 1.7% at $58.1/bbl.

- Trump said on Tuesday the bombing of Yemen will stop as a ceasefire with the Houthis is brokered via Oman, in a move he said will stop attacks on ships.

- A medium-term bearish trend in WTI futures remains intact with attention on $54.67, the Apr 9 low and a bear trigger. Key resistance to watch is $63.88, the 50-day EMA.

- Meanwhile, spot gold has fallen by 1.3% to $3,388/oz.

- Analysts at Saxo Bank said that having surged ahead of the Chinese market reopening, a setback was expected. They add that while US-China trade talks may ease demand in the short term, a deal may still be difficult to strike.

- For gold, a continuation higher would refocus attention on key resistance and the bull trigger at $3,500.1, the Apr 22 high. Key short-term support has been defined at $3,202.0, the May 1 low.

- Elsewhere, copper has pulled back by 2.8% to $465/lb.

- Despite the move, Goldman Sachs says that a de-escalation in trade tensions and resilient Chinese copper demand will likely continue to support copper ahead.

- Key short-term resistance for copper has been defined at $498.25, the Apr 23 high. A continuation of weakness would expose $436.00, the Apr 10 low.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 08/05/2025 | 0600/0800 | ** | Trade Balance | |

| 08/05/2025 | 0600/0800 | ** | Industrial Production | |

| 08/05/2025 | 0700/0900 | ** | Industrial Production | |

| 08/05/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 08/05/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data | ||

| 08/05/2025 | 1400/1000 | BOC Financial Stability Report and Financial System Survey | ||

| 08/05/2025 | 1400/1000 | ** | Wholesale Trade | |

| 08/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 08/05/2025 | 1500/1100 | BOC Governor Macklem presser Financial System Review | ||

| 08/05/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/05/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 08/05/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 09/05/2025 | 2330/0830 | ** | average wages (p) | |

| 09/05/2025 | 2330/0830 | ** | Household spending |