MNI ASIA MARKETS ANALYSIS: Shrugging off Tariff Inflation Risk

HIGHLIGHTS

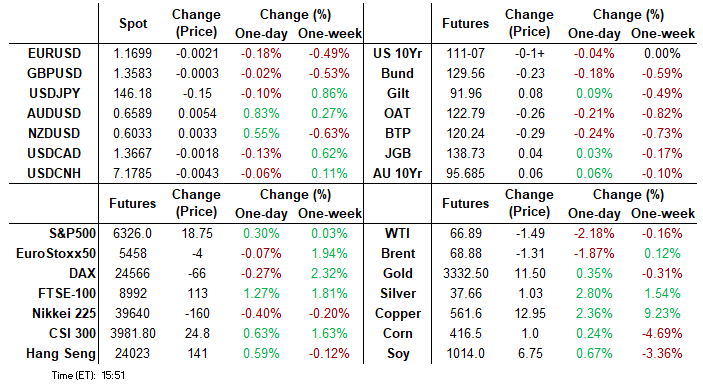

- Treasuries look to finish mixed Thursday, curves twist flatter (2s10s -1.132 at 47.152, 5s30s -3.180 at 92.868) as Bonds led a rebound off midday lows.

- SPX eminis and Nasdaq stocks climbed to new all-time highs as markets shrugged off tariff-related event and pass-through inflation risks to focus on economic data.

- SF Fed President Daly said "the economy's in a good place and policy's in a good place. So I see two cuts as a likely outcome," she told a MNI Livestreamed Connect event.

US TSYS

US TSYS: Bonds Lead Rebound Off Early Lows, S&P/Nasdaq Climb To New Highs

- Treasuries look to finish mixed Thursday, off early session lows, curves twist flatter with Bonds leading the rebound in late trade (USU5 +4 at 114-06): 2s10s -0.913 at 47.371, 5s30s -2.776 at 93.272. Markets traded with a positive tone, shrugging off tariff-related event and pass-through inflation risks to focus on economic data.

- The latest weekly claims showed a further improvement in seasonally-adjusted initial claims, though the continued elevation in continuing claims kept the broader theme of a 'low firing, low hiring' labor market very much intact going into the second half of the year. Initial jobless claims were below expected at 227k (235k consensus, 232k prior rev from 233k) in the Jul 5 week. Continuing claims were exactly in line at 1,965k (1,965k expected, prior rev from 1,964k)

- SF Fed President Daly said "the economy's in a good place and policy's in a good place. So I see two cuts as a likely outcome," she told a MNI Livestreamed Connect event, adding it's possible that a large tariffs-driven increase in inflation does not materialize.

- Earlier, StL Fed Pres Musalem sounded a little dovish on incoming inflation data, emphasizing that on a 3-month basis there have been "very positive inflation trends in core and headline [PCE] in goods and in services, and those are very welcome developments".

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (-0.02), volume: $2.752T

- Broad General Collateral Rate (BGCR): 4.31% (-0.01), volume: $1.133T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.01), volume: $1.101T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $105B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $262B

FED Reverse Repo Operation:

RRP usage retreats to $183.339B this afternoon from $227.273B yesterday, total number of counterparties at 36. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow remained mixed Thursday, leaning towards calls, bull steepeners, vol sales and position unwinds on the day. Underlying futures weaker but off lows, curves twist flatter as Bonds led a rebound in the second half. Projected rate cut pricing held largely steady vs morning (*) levels: Jul'25 at -1.7bp, Sep'25 at -18.8bp (-19.1bp), Oct'25 at -34.2bp, Dec'25 at 52.6bp.

SFOR Options:

-30,000 0QQ5 96.75/97.00 call spds 6.5 over 96.37 puts vs. 96.755 to -.76/0.30%

Block, 5,000 SFRU5 96.12/96.18 call spds 0.75 ref 95.875

1,750 SFRX5 96.00/96.12 3x2 put spds ref 96.16

+4,000 SFRU5 95.68/95.75/95.81 call flys, 0.5 ref 95.88

Block/pit, +10,000 2QU5 97.00/97.50 call spd vs. 3QU5 96.75/97.25 call spds, 0.0 net/steepener

Block/pit, +15,000 0QU5 97.00/97.50 call spds 1.5 over 3QU5 96.75/97.25 call spds

+2,500 SFRZ5 95.37/95.62 put spds, 0.5 ref 96.165

Block/pit/screen, +21,000 SFRU5 95.62/95.75 2x1 put spds 2.75

10,400 SFRH6 97.25/98.25 call spds ref 96.44

5,500 SFRH6 96.75/97.00 call spds ref 96.43

-2,000 SFRZ55 95.68/95.81 put spds vs. 0QZ5 96.25/96.37 put spds, 0.0 net

3,000 0QV5 97.00/97.25 call spds, 3.0 vs. 96.3125

2,000 2QH6 97.00/97.50 call spds ref 96.61

+3,500 SFRQ5 96.00/96.12 call spds, 1.75 ref 95.895

5,000 SFRQ5 95.68/96.06 strangles, 2.5

Treasury Options:

1,350 FVQ5/FVU5 108.5 straddle spd

2,396 TYQ5 111 straddles, 55

3,000 TYQ5 110 puts, 5

-1,000 TYU5 111 straddles, 140

-6,000 wk2 TY 111.5 calls, 3 ref 111-06.5/0.24%

3,000 wk2 TY 110.25/112.25 call over risk reversals, 0.0

2,000 TYQ5 111.75/112.25 call spds, 7 vs. 111-06.5/0.10%

+1,800 wk2 TY 110.5/110.75 put spds, 1 ref 111-07.5

+2,500 wk3 FV 108/108.5 put spds, 13 ref 108-14.25/0.31%

MNI EGB BONDS: EGBs-GILTS CASH CLOSE: German Yields Resume Recent Uptrend

EGB yields resumed their recent uptrend Thursday, with Gilts outperforming Bunds.

- There was once again no overt macro headline or data driver for Bund and broader EGB weakness, with the prevailing theme continuing to be expansionary German fiscal policy.

- Solid US jobless claims data also contributed to global core FI weakness in the afternoon through the cash close.

- Fiscal policy remains a concern in the UK too, but Gilts continued to consolidate from last week's spike.

- European data was second-tier, with Italian industrial production coming in weaker than expected, and German final June inflation confirming the flast estimates.

- The German curve bear steepened on the day, with 10Y yields seeing their highest close since April 2 and 2Y since May 15. The UK curve bull steepened.

- Periphery/semi-core spreads were mostly wider to Bunds, with Spain/Portugal notable outperformers.

- Friday's data highlight is UK monthly activity/GDP, with appearances by ECB's Panetta, Vujcic and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3bps at 1.89%, 5-Yr is up 3.4bps at 2.273%, 10-Yr is up 3.2bps at 2.705%, and 30-Yr is up 4.1bps at 3.203%.

- UK: The 2-Yr yield is down 2.4bps at 3.856%, 5-Yr is down 1.5bps at 4.026%, 10-Yr is down 1.7bps at 4.595%, and 30-Yr is down 1.6bps at 5.406%.

- Italian BTP spread up 0.3bps at 85.4bps / Spanish down 0.8bps at 61.4bps

MNI EGB OPTIONS: Sizeable Ratio Trades And Condor Of Note In Rates

Thursday's Europe rates/bond options flow included:

- RXQ5 129.50/128.50ps, bought for 28.5 in 3.5k (follows Wednesday's RXQ5 128.5/127.5ps, bought for 10.5 up to 11.5 in 5k)

- ERU5 98.0625/97.9375ps 1x2 vs ERZ5 98.0625/97.9375ps 1x2, bought the Dec for -0.75 in 20k

- ERZ5 98.25/98.37/98.50/98.62c condor, bought for 2.75 in 25k total

- SFIH6 96.50/97.00/97.50 call fly vs 96.15 put, bought for 3.5 in 6.5k

- SFIH6 96.60/97.00 1x2 call spread vs 96.00 put pays 1 for the call spread in 4k (vs 19)

MNI FOREX: DXY Set to Advance Again, AUD Strength Standing Out

- Although off its best levels, the USD index looks set to post its highest recovery close on Thursday, having risen around 1.4% from last week’s cycle lows. Price action has been assisted by a better-than-expected set of US jobless claims data, underpinning the latest strength for the greenback.

- However, intra-day sentiment across the G10 complex has been mixed, with the EUR and GBP underperforming while the likes of AUD and NZD have thrived. Fresh weekly highs for e-mini S&P 500 futures have assisted the higher beta currencies , providing a particularly supportive tone for the Australian dollar, which has been notably outperforming in the crosses. This dynamic has allowed the likes of EURAUD and GBPAUD to extend losses to 0.88% and 0.72% respectively as we approach the APAC crossover

- EURAUD has now reached a near three-week low back below 1.7800, exacerbated by a clean break below 20-day EMA support, which intersected at 1.7865. For GBPAUD, price action extends the 3-day slide to 1.5%, and the cross is now breaching short-term trendline support, located around 2.0660.

- In similar vein, continued outperformance against the Kiwi has seen AUDNZD also extend its most recent rally, with the cross testing the May highs at 1.0922. A sustained break would signal scope for a move back to the early April highs just above the 1.10 mark.

- Although showcasing another 100+ pip range (145.76 – 146.79), USDJPY holds close to unchanged on the session and might struggle for momentum in either direction owing to the lack of US data on Friday. The global calendar will be highlighted by UK GDP figures and Canadian employment data.

MNI FX OPTIONS: Expiries for Jul11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E2.1bln), $1.1550(E581mln), $1.1700(E1.4bln), $1.1770(E2.4bln), $1.1825-40(E1.8bln)

- USD/JPY: Y146.30($649mln), Y146.75-90($667mln)

- AUD/USD: $0.6550-60(A$580mln)

- USD/CAD: C$1.3625-45($ C$1.3700-15($1.1bln)

MNI US STOCKS: Late Equities Roundup: SPX Eminis, Nasdaq Mark New Highs

- Stocks continued to rise in late Thursday trade - focus on upcoming earnings and economic data while pushing tariff headline risk to the backburner for the moment. SPX eminis and Nasdaq indexes making new all-time highs while the DJIA still has a ways to go to breach December 4 high of 45073.63.

- Currently, the DJIA trades up 260.62 points (0.59%) at 44717.31, S&P E-Minis up 22.75 points (0.36%) at 6329.75, Nasdaq up 31.7 points (0.2%) at 20642.3.

- Consumer Discretionary and Health Care sectors led gainers in the second half, a mix of travel, auto and broadline retailers buoyed the former: Norwegian Cruise Line Holdings +5.33%, Expedia Group +4.85%, Tesla +3.13%, Best Buy Co +2.65% and Tapestry +2.53%. Pharmaceutical shares supported the Health Care sector: Bio-Techne +5.17%, Moderna +4.09%, Charles River Laboratories +3.54%, Agilent Technologies +3.18% and IQVIA Holdings +2.89%

- On the flipside, Information Technology and Communication Services continued to underperform in late trade, software and services stocks weighing on the IT sector: Autodesk -7.08%, PTC -5.91%, Fortinet -5.44%, Palo Alto Networks -5.09% and Crowdstrike Holdings -3.69%. Interactive media and telecom shares weighed on the latter: Netflix -2.51%, Take-Two Interactive Software -2.18%, AT&T -1.46%, T-Mobile US -1.32% and Verizon Communications -1.28%.

- The latest corporate earning cycle kicks off next week Tuesday with banks and financial stocks reporting: Blackrock, JPMorgan Chase & Co, Wells Fargo & Co, Bank of New York Mellon, State Street Corp and Citigroup.

MNI EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6335.50 Intraday High

- PRICE: 6329.00 @ 1455 ET Jul 10

- SUP 1: 6246.25 Low Jul 7

- SUP 2: 6176.77/6032.93 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis remains bullish and the contract is trading closer to its recent highs. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6032.93.

MNI COMMODITIES: Crude Slides Amid Production Hike Plans, Copper Rallies

- WTI has fallen today after reports suggested that OPEC+ is discussing another large hike in September. Signs of rising trade tensions due to tariffs also added to bearish pressure.

- WTI Aug 25 is down by 2.3% at $66.8/bbl.

- Saudi Arabia and its partners already have a tentative plan to complete the revival of a 2.2m b/d supply revival in September, with another monthly trance of 550k b/d, Bloomberg reports.

- OPEC is discussing a pause in further production increases after its next monthly hike, delegates told Bloomberg.

- WTI futures maintain a bearish tone following the reversal from the June 23 high. Support to watch is the 50-day EMA, at $65.27.

- Meanwhile, spot gold is up by just 0.2% at $3,320/oz as the yellow metal continues to struggle for direction.

- Support to watch is the bear trigger at $3,248.7, the June 30 low. On the upside, a resumption of gains would refocus attention on $3,451.3, the June 16 high.

- Copper has rebounded by 2.3% today to $561/lb, leaving the red metal up by more than 11.5% since Trump’s 50% copper tariff announcement on Tuesday. He has said that the tariff will take effect from Aug 1.

- Sights are on a retest of this week’s $589.55 high, clearance of which would open the $600.00 handle.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/07/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 11/07/2025 | 0600/0700 | ** | Trade Balance | |

| 11/07/2025 | 0600/0700 | ** | Index of Services | |

| 11/07/2025 | 0600/0700 | ** | Index of Production | |

| 11/07/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/07/2025 | 0645/0845 | *** | HICP (f) | |

| 11/07/2025 | 1130/1330 | ECB Cipollone At Ukraine Recovery Conference | ||

| 11/07/2025 | - | *** | Money Supply | |

| 11/07/2025 | - | *** | New Loans | |

| 11/07/2025 | - | *** | Social Financing | |

| 11/07/2025 | 1230/0830 | *** | Labour Force Survey | |

| 11/07/2025 | 1230/0830 | * | Building Permits | |

| 11/07/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/07/2025 | 1800/1400 | ** | Treasury Budget |