COMMODITIES: Crude Slides Amid Production Hike Plans, Copper Rallies

Jul-10 18:53

- WTI has fallen today after reports suggested that OPEC+ is discussing another large hike in September. Signs of rising trade tensions due to tariffs also added to bearish pressure.

- WTI Aug 25 is down by 2.3% at $66.8/bbl.

- Saudi Arabia and its partners already have a tentative plan to complete the revival of a 2.2m b/d supply revival in September, with another monthly trance of 550k b/d, Bloomberg reports.

- OPEC is discussing a pause in further production increases after its next monthly hike, delegates told Bloomberg.

- WTI futures maintain a bearish tone following the reversal from the June 23 high. Support to watch is the 50-day EMA, at $65.27.

- Meanwhile, spot gold is up by just 0.2% at $3,320/oz as the yellow metal continues to struggle for direction.

- Support to watch is the bear trigger at $3,248.7, the June 30 low. On the upside, a resumption of gains would refocus attention on $3,451.3, the June 16 high.

- Copper has rebounded by 2.3% today to $561/lb, leaving the red metal up by more than 11.5% since Trump’s 50% copper tariff announcement on Tuesday. He has said that the tariff will take effect from Aug 1.

- Sights are on a retest of this week’s $589.55 high, clearance of which would open the $600.00 handle.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Crude, Gold Edge Lower As US-China Talk Developments Awaited

Jun-10 18:48

- Crude markets have erased earlier gains to lose ground on the day, as the market awaits developments from a second day of US-China trade talks in London.

- WTI Jul 25 is down by 0.9% at $64.7/bbl.

- US Commerce Secretary Lutnick described negotiations yesterday as “fruitful” and have continued throughout today.

- Elsewhere, the Iranian Foreign Ministry has reported that a sixth round of indirect talks between Iran and the US will take place in the Omani capital, Muscat, on Sunday, 15 June.

- WTI futures remain above the 50-day EMA, signalling scope for an extension towards $65.82 next, the Apr 4 high.

- It is still possible that the recovery since early May is a correction, however, and support to watch lies at $59.74, the May 30 low.

- Meanwhile, spot gold has struggled for direction as the outcome of the US-China talks remain key for near-term sentiment. The yellow metal has edged down by 0.1% to $3,323/oz.

- The latest pullback in gold appears corrective in nature, and medium-term trend signals remaining bullish.

- Initial support to monitor in the event of a positive tariff outcome is the 50-day EMA at $3,242.4, which shields key support at $3,121.0, the May 15 low.

- Should these support levels hold, or if talks do not bring a de-escalatory outcome, it may provide a platform to build back towards the June 5 high at $3,403.5 and the May 7 high of $3,435.6.

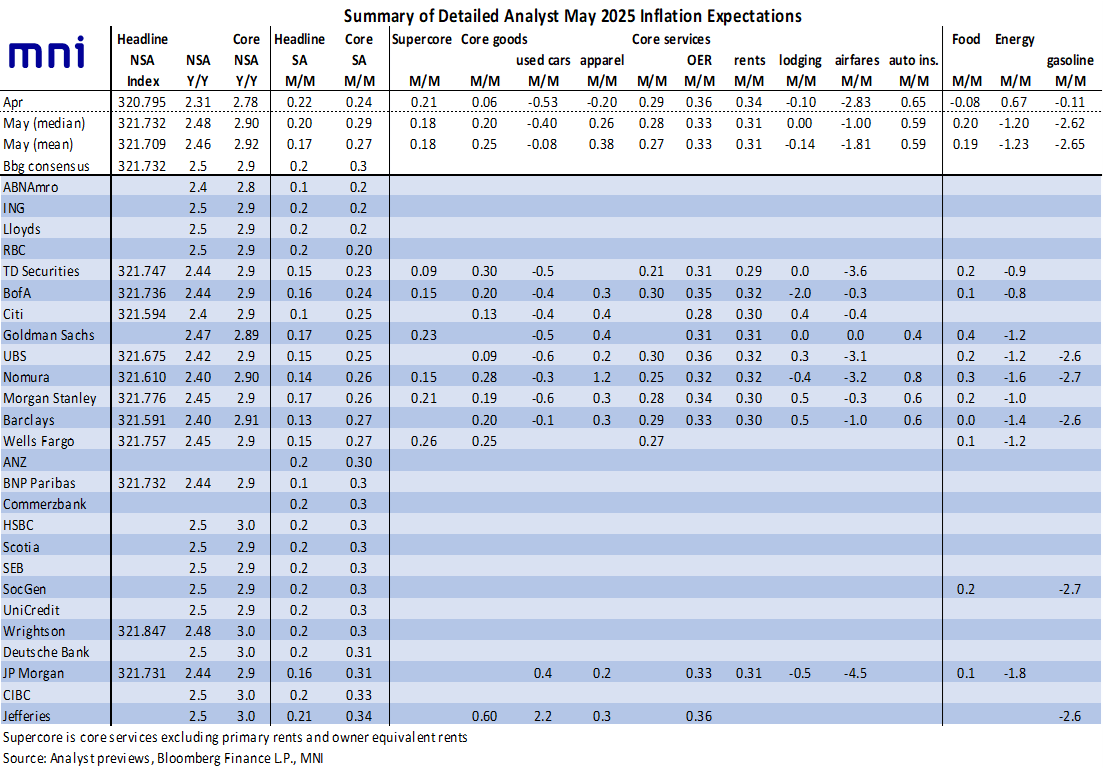

US OUTLOOK/OPINION: Detailed Analyst CPI Expectations For Tomorrow's Release

Jun-10 18:47

The below table summarizes a range of analyst expectations for tomorrow's May US CPI release, taken from the MNI US CPI Preview found here.

- It finds a median expectation for core CPI inflation of 0.29% M/M, close to the rounded 0.3% M/M in the Bloomberg survey although it's 0.27% M/M when just looking at unrounded estimates.

- As for sequential drivers, quite a few of the categories that we tend to focus on are expected to see some acceleration relative to April's M/M findings. There are however some wide ranges to estimates for some of the noisier categories whilst the heavily weighted rent components are expected to moderate a touch back a little closer to pre-pandemic trends.

BONDS: EGBs-GILTS CASH CLOSE: Rally Extends On Softening UK Jobs Data

Jun-10 18:44

European yields fell for the second day this week Tuesday, with Gilts outperforming Bunds.

- Gains were basically steady throughout the session, as some of last week's ECB-related selloff continued to reverse.

- Data out early in the session confirmed that the UK labour market is softening at an increasing pace, with AWE wage data on track to come in even lower in Q2 than the BOE’s Q1 forecast miss, and HMRC payrolls data pointing to growing slack. Our analysis of the release is here (PDF).

- The data saw BOE cut pricing rise to nearly 50bp for the year, up from 41bp prior.

- The UK curve leaned bull steeper, with the belly outperforming. Germany's bull flattened.

- Periphery / semi-core EGB spreads were mixed, with BTPs once again outperforming and 10Y now targeting the 90bp level vs Bunds.

- Wednesday is light for European data, with the main highlight expected to be the ECB Wage tracker. Most attention will be on US CPI. We also hear from ECB's Lane, Makhlouf, and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 1.847%, 5-Yr is down 3.3bps at 2.123%, 10-Yr is down 4.4bps at 2.523%, and 30-Yr is down 4.2bps at 2.97%.

- UK: The 2-Yr yield is down 8.4bps at 3.919%, 5-Yr is down 9bps at 4.048%, 10-Yr is down 9bps at 4.542%, and 30-Yr is down 7.4bps at 5.254%.

- Italian BTP spread down 0.7bps at 91.3bps / French OAT unchanged at 67.2bps