MNI ASIA MARKETS ANALYSIS: Risk-Off Sentiment Retreats

HIGHLIGHTS

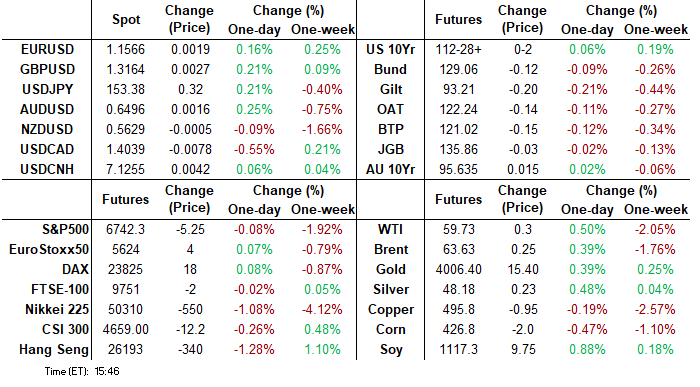

- Treasuries scaled off midday highs late Friday, curves holding mildly steeper with 2s-10s advancing, broader dollar rally that had been playing out following the FOMC showed signs of fatigue this week.

- Rates supported by a combination of weaker equities (chip makers underperforming) and a sharp decline in UofM consumer sentiment & current conditions slid to their lowest on record.

- Republicans reject Senate Democrats off on ACA subsidy as the US Govt shutdown looks to enter it's sixth week next week.

US TSYS

MNI US TSYS: Risk-Off Sentiment Recedes Late, US Gov Shutdown To Enter Week 6

- Treasuries look to finish mixed Friday - well off midday highs as early risk-off tone moderated. Republicans reject Senate Democrats off on ACA subsidy as the US Govt shutdown looks to enter it's sixth week next week.

- Currently, the Dec'25 10Y contract trades +1.5 at 112-28 after testing resistance above at 113-02, clearance of this level would highlight a potential bullish reversal.

- A short-term bearish threat in Treasuries remains intact. Sights are on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-07. Clearance of these price points would expose a trendline support at 112-00 - the trendline is drawn from the May 22 low.

- The preliminary University of Michigan consumer survey for November saw a sharp decline in consumer sentiment as the perception of current conditions slid to their lowest on record: Consumer sentiment: 50.3 (Bloomberg consensus 53.0) after 53.6 – lowest since Apr 2022; Current conditions: 52.3 (cons 59.0) after 58.6 – lowest on record; Expectations: 49.0 (cons 49.0) after 50.3.

- Fed Vice Chair Jefferson (voter) on wanting to proceed slowly being closer to a neutral level rather than talking on Powell’s “fog”. He does though note a meeting-by-meeting stance being especially prudent with a lack of official data.

- Stocks well off midday lows, Materials, Consumer Staples and Energy sector shares continued to advance in the second half. Late-cycle earnings expected next Monday: Blackstone Secured Lending, Terawulf Inc, Occidental Petroleum, Paramount Skydance, Getty Images Holdings, Rocket Lab Corp and CoreWeave Inc.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.92% (+0.01), volume: $3.156T

- Broad General Collateral Rate (BGCR): 3.89% (+0.01), volume: $1.219T

- Tri-Party General Collateral Rate (TCR): 3.89% (+0.01), volume: $1.189T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.87% (+0.00), volume: $87B

- Daily Overnight Bank Funding Rate: 3.87% (+0.00), volume: $160B

FED Reverse Repo Operation

RRP usage slips to $4.903B with 9 counterparties this afternoon - from $10.754B Thursday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options look mixed by the bell, decent downside Treasury puts with some SOFR call skew buying late. Underlying mixed after the bell - scaling back risk-off support late. Projected rate cut pricing steady to mixed vs late Thursday levels (*): Dec'25 at -16.5bp (-17.5bp), Jan'26 at -27.1bp (-27.1bp), Mar'26 at -37.6bp (-36.3bp), Apr'26 at -43.6bp (-42.1bp).

SOFR Options:

+20,000 SFRH6 96.25/96.75 call over risk reversals, 3.0 ref 96.43

+5,000 SFRH6 97.25/97.75 calls, 1.75 ref 96.47

+15,000 0QX596.37 puts, 5.0 vs. 96.93/0.52%

+23,000 SFRZ5 96.06/96.12/96.18/96.25 put condors, 1.25 ref 96.25

12,000 SFRZ5 96.06/96.12 put spds

+7,500 SFRZ5 96.37 calls, 2.0 vs. 96.255/0.24%

Block, 3,000 0QZ5 96.68 puts, 3.0 ref 96.905

2,500 SFRZ5 96.25/96.37/96.44 broken call flys vs. 96.06/96.12 put spds ref 96.26

over 15,000 SFRZ6 98.00/99.00 call spds, 6.0 ref 96.915 to -.92

Block/screen 8,500 SFRH6 96.31/96.37 put spds ref 96.435

2,000 0QZ5 96.25/96.87/97.00/97.12 put condors ref 96.895

+5,000 SFRX5 96.31/96.37/96.43 call flys, .5 ref 96.255 to -.25

Treasury Options:

10,000 FVF6 108.75/109/109.5 put trees ref 109-15.75

15,000 TYZ5 111.5 puts, 2 ref 113-00

3,000 TYZ5 115 calls, 2 ref 113-00, t

over +20,000 111/112 put spds 2 over 114.5 calls ref 112-26

+10,000 TYZ5 111.5 puts, 3

2,000 TYF6 115/116 call spds ref 112-21

+5,000 wk1 TY 113 calls, 1

-2,000 TYF5 112.5/113 strangles, 126 ref 112-21

over 9,800 TYZ5 113 calls, 20-24 last

MNI BONDS: EGBs-GILTS CASH CLOSE: Bear Steepening Confirmed For The Week

European yields rose again Friday, capping a bear-steepening move for the week as a whole.

- Core bonds gained strongly in morning trade as global equities hit the weakest levels of the month so far.

- Despite a lack of a US nonfarm payrolls report due to government shutdown, bonds would reverse lower in the middle of the European afternoon session.

- This reversal was not really triggered by any particular macro / headline trigger, but rather order-related selling flows that saw curves bear steepen.

- For the week, both the German (2Y yield +2.2bp, 10Y +3.3bp) and UK (2Y +2.7bp, 10Y +5.7bp) bear steepened, with Gilts underperforming despite what had been perceived as a dovish-vs-expectations BOE meeting.

- Periphery/semi-core EGB spreads widened slightly, mirroring the continued pullback in equities.

- Next week's calendar highlight is UK labour market data, with various other data including German ZEW.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.3bps at 1.99%, 5-Yr is up 0.9bps at 2.256%, 10-Yr is up 1.6bps at 2.666%, and 30-Yr is up 2.8bps at 3.266%.

- UK: The 2-Yr yield is up 1.2bps at 3.798%, 5-Yr is up 3.1bps at 3.928%, 10-Yr is up 3.3bps at 4.466%, and 30-Yr is up 3.2bps at 5.25%.

- Italian BTP spread up 0.5bps at 76.7bps / French OAT up 0.3bps at 79.7bps

MNI OPTIONS: Euribor Upside Continues, Alongside Some Mixed Bobl

Friday's Europe rates/bond options flow included:

- OEZ5 118p, bought for 16.5 and 17 in ~6.5k

- OEZ5 118.00/117.75/117.00p fly sold at 2.5 in 2k

- ERH6 98.06/98.12cs vs 97.87p with ERH6 98.06/98.12cs vs 97.93p, bought the call spreads for flat in 4k

- ERM6 98.75/98.87cs, bought for 0.25 in 20k.

- ERM6 98.12/98.18cs vs 97.81p, bought the cs for -0.25 in 10k

- SFIF6 96.55/96.50/96.35/96.25p condor, bought for 1.25 in 2k

MNI FOREX: Equity Selloff Has Limited FX Impact, CAD Boosted on Jobs Data

- Further volatility and bearish sentiment for the major equity benchmarks on Friday had a relatively limited impact in the currency space. Underperformance of the US indices and another 1.6% move in the Nasdaq weighed on the dollar index, with the likes of EUR and GBP outperforming on the session.

- In general, the broader dollar rally that had been playing out following the FOMC showed signs of fatigue this week. The DXY reaching its initial objective at the August highs (~100.25) may have also contributed to the reversal lower across Thursday and Friday trade. Amid this dynamic, EURUSD is now roughly 100 pips above the recent pullback lows, trading around 1.1580 as we approach the weekend close.

- Additionally, and following the dovish hold by the Bank of England on Thursday, sterling has traded in a resilient manner with cable rising back above the prior breakdown level of 1.3140 to trade around 1.3175 at typing. Positioning dynamics has likely been assisting the bounce, while the move higher is allowing an oversold trend condition to unwind.

- CAD has been one of the best performers across the G10, following a stellar employment report released today. USDCAD sits 0.45% lower on the session, notably falling back below the prior breakout level at 1.4080. Furthermore, the latest price action sees USDCAD edge further away from previously touted resistance, the top of a bull channel, drawn from the July 23 low. Having highlighted this area as a key obstacle to further USDCAD strength, price has subsequently respected the line twice, bolstering the potential of a short-term bearish signal.

- China PPI/CPI data crosses over the weekend, before the focus turns to UK labour market data on Tuesday.

MNI OPTIONS: Expiries for Nov10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1475(E1.9bln), $1.1500(E1.1bln), $1.1550(E723mln), $1.1600(E784mln), $1.1750(E1.1bln), $1.1770(E1.2bln)

- GBP/USD: $1.3100(Gbp712mln)

- EUR/GBP: Gbp0.8825(E609mln)

- AUD/USD: $0.6610-20(A$1.3bln)

- USD/CNY: Cny7.1000($651mln)

MNI US STOCKS: Late Equities Roundup: Sentiment Improves Materials, Staples & Energy

- Major US equity indexes are mixed late Friday - well off midday lows with the DJIA outperforming at the moment. Despite the weekend - risk sentiment improving as Treasuries pare support at the bell. Currently, the DJIA trades up up 30.54 points (0.07%) at 46939.77, S&P E-Minis down 6.25 points (-0.09%) at 6740.5, Nasdaq down 99.1 points (-0.4%) at 22952.4.

- Materials, Consumer Staples and Energy sector shares continued to advance in the second half:

- Albemarle +6.28%, Solstice Advanced Materials +4.98%, International Paper +4.13%, Freeport-McMoRan +3.26%, Mosaic +2.41% and Sherwin-Williams +2.25%.

- Monster Beverage +6.02%, Molson Coors Beverage +4.81%, Dollar Tree +3.18%, Dollar General +3.10% and Tyson Foods +2.73%.

- Devon Energy +3.73%, Williams Cos +2.66%, Exxon Mobil +2.45%, EQT Corp +2.35%, Diamondback Energy +2.02% and Occidental Petroleum +1.86%.

- Conversely, Information Technology sector shares continued to underperform amid ongoing concerns over stock valuations tied to all things AI related: Microchip Technology -7.43%, Corning -3.37%, Skyworks Solutions -3.20%, ON Semiconductor -3.05%, Analog Devices -2.83% and Teradyne -2.77%.

- Communication Services followed: Take-Two Interactive Software -7.06%, Trade Desk Inc -5.99% and Alphabet -2.13%.

- Late-cycle earnings expected next Monday: Blackstone Secured Lending, Terawulf Inc, Occidental Petroleum, Paramount Skydance, Getty Images Holdings, Rocket Lab Corp and CoreWeave Inc.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Has Pierced The 50-day EMA

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6857.75/6953.75 High Nov 5 / High Oct 30 and the bull trigger

- PRICE: 6701.25 @ 14:43 GMT Nov 7

- SUP 1: 6690.75 Low Oct 22

- SUP 2: 6571.25 Low Oct 17

- SUP 3: 6540.25 Low Oct 10 and a key support

- SUP 4: 6476.62 23.6% retracement of the Apr 7 - Oct 30 bull cycle

The trend condition in S&P E-Minis is unchanged, it remains bullish and the pullback since the Oct 30 high appears corrective. Today’s move down has resulted in a test of support around the 50-day EMA, at 6708.51. A clear break of this level average would strengthen a short-term bear theme and signal scope for a deeper retracement, towards 6540.25 initially, the Oct 10 low. The bull trigger has been defined at 6953.75, the Oct 30 high.

COMMODITIES

MNI AMERICAS OIL: Oil Summary at US Close: WTI Falls on Week

WTI is on higher on the day but remains on track for a net decline on the week with market focus still on downside risk from signs of a surplus.

- WTI DEC 25 up 0.6% at 59.79$/bbl

- OPEC oil output rose 50kb/d to 29.07mb/d in October, Bloomberg said.

- OPEC+’s decision to pause production hikes in Q1 26 is a precautionary move at a time when the market, according to Kpler’s Amena Bakr, cited by Dow Jones.

- Gunvor has withdrawn its offer for Lukoil’s international assets after the US Treasury Department said the oil and gas trader would never get a license.

- China's headline Oct trade figures were weaker than forecasts, with export growth falling to -1.1%y/y, the weakest result since Feb this year.

- China total imports also moderated to 1.0%y/y from 7.4% in Sep although oil imports rose to 48.36m mt, from 47.25m mt in Sep and 8.2% higher on the year: Customs data.

- Oil in floating storage in Asia has surged in recent, Reuters said.

- In Q4, oil markets are expected to feel the impact of increased global production reaching the water, according to International Seaways executives.

- Mexico’s Pemex is currently in the process of assigning hydrocarbon development projects to private sector partners, Energy Minister Luz Elena Gonzalez told Congress Nov. 7.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/11/2025 | 0700/0800 | *** | CPI Norway | |

| 10/11/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/11/2025 | 0910/0910 | BOE Lombardelli at BOE/Ghana Central Bank Conference | ||

| 10/11/2025 | - | *** | Money Supply | |

| 10/11/2025 | - | *** | New Loans | |

| 10/11/2025 | - | *** | Social Financing | |

| 10/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 10/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 10/11/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/11/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/11/2025 | 2350/0850 | Balance of Payments | ||

| 11/11/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 11/11/2025 | 0500/1400 | Economy Watcher's Survey |