OPTIONS: Expiries for Nov10 NY cut 1000ET (Source DTCC)

Nov-07 16:56

- EUR/USD: $1.1475(E1.9bln), $1.1500(E1.1bln), $1.1550(E723mln), $1.1600(E784mln), $1.1750(E1.1bln), $1.1770(E1.2bln)

- GBP/USD: $1.3100(Gbp712mln)

- EUR/GBP: Gbp0.8825(E609mln)

- AUD/USD: $0.6610-20(A$1.3bln)

- USD/CNY: Cny7.1000($651mln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Sizeable Upside Continues Alongside Vol Selling In Euribor Wednesday

Oct-08 16:52

Wednesday's Europe rates/bond options flow included:

- ERZ5 98.00^ sold at 7.5 in 1.5k (had been sold at 7 / 7.25 Tuesday)

- ERF6 98.1875/98.3125cs vs ERM6 98.37/98.50cs, bought the June for half in 5k

- ERH6 98.25/98.37cs, bought for 1 in 20k

- ERH6 98.06/98.18cs, bought for 3 in 5k

- ERH6 98.00/98.06/98.12/98.18c condor, bought for 0.25 in 4k

- ERM6 98.31/98.43cs, bought for 1.75 in 10k

- ERM6 98.75c, bought for 1 in 23.3k

- ERM6 98.50/98.625/98.75/98.875c condor, bought for half in 7.5k (around 50k done this week)

- ERU6 97.93/97.81ps v ERM6 97.87p, bought the ps for half in 3k

- 0RM6 98.25 calls paper paid 5.25-5.5 on 9K (ref. 97.91)

- SFIM6 96.50/96.75cs, bought for 5.25 in 6k

US TSYS/SUPPLY: WI 10Y Re-Open

Oct-08 16:50

WI 10Y stable at 4.117% ahead of the $39B 10Y note auction re-open (91282CNT4) cut-off at 1300ET, compares to last month's stop: drawing 4.033% high yield vs. 4.047% WI.

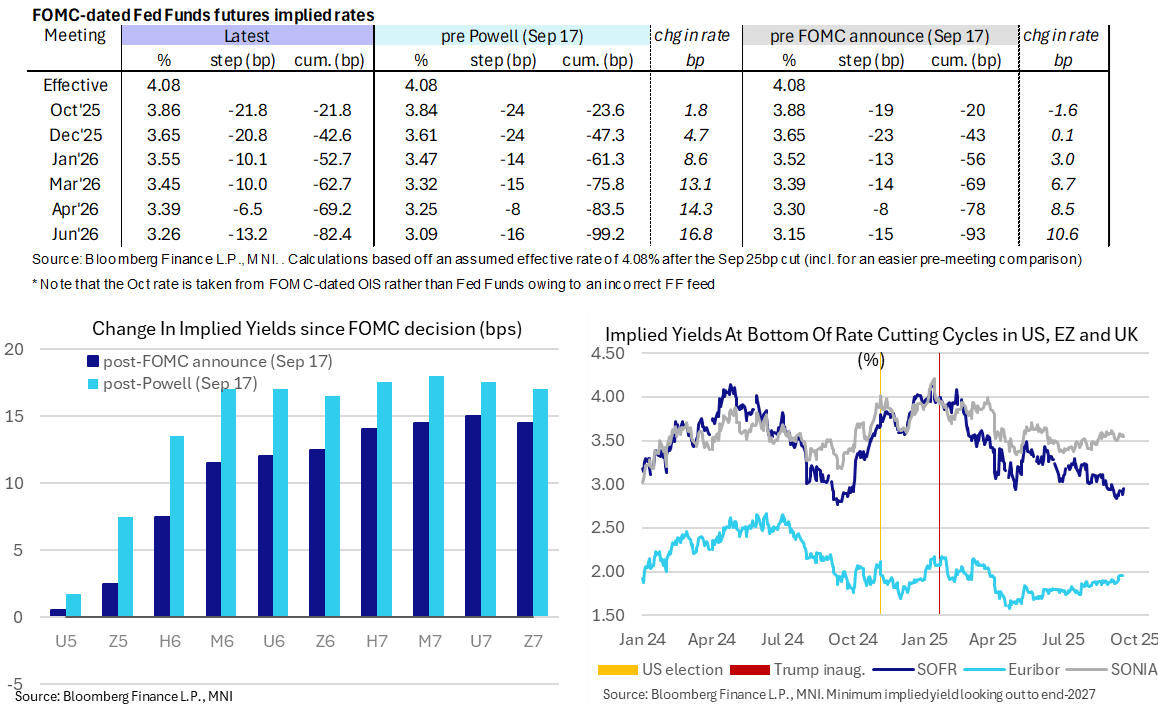

STIR: Near-Term Rate Path Back Close To Pre-ADP Levels, FOMC Minutes To Come

Oct-08 16:47

- Fed Funds implied rates are towards their most hawkish of the day, with the Dec implied rate for example back close to levels prior to last week’s soft ADP release.

- Further gains for crude oil futures (WTI 1st +1.3%) and S&P 500 e-minis back at record highs are likely in the driving seat.

- Moves are still relatively modest on the day, with 1.5bp increases for Dec and Jan meetings and 2.5bp higher through Mar-Jun meetings.

- Cumulative cuts from 4.08% effective: 22bp Oct, 42.5bp Dec, 52.5bp Jan, 62.5bp Mar, 69bp Apr and 82.5bp June.

- SOFR futures also see modest losses, sitting 2 ticks lower through H6-H7 contracts.

- The SOFR implied terminal yield of 3.07% is back in the SFRH7 after technically tilting into the Z6 on Monday for the first time since mid-July. It roughly points to 100bp of cuts ahead.

- Fedspeak has indeed been a non-event today although we are still to get the FOMC minutes at 1400ET - see the above posts starting 1121ET for a more detailed take on what to look for. That's barring any spillover to front rates at the upcoming 10Y auction at 1300ET.