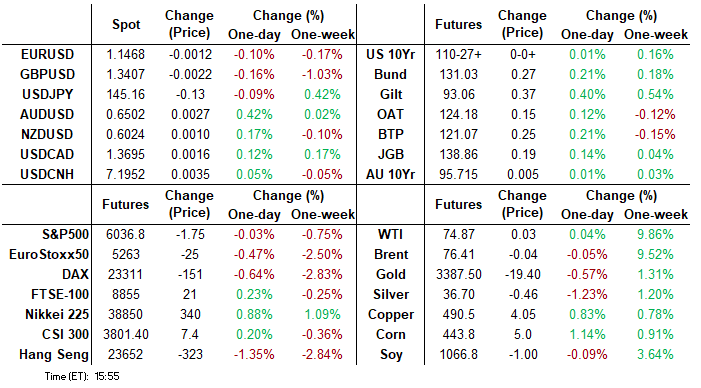

MNI ASIA MARKETS ANALYSIS: Powell's Patient Policy

HIGHLIGHTS

- Treasuries drifted higher heading into the FOMC, muted react to broad drop in Housing Starts and Building Permits for May.

- Rates gapped higher immediately after the Fed left rates steady, remain patient despite ongoing uncertainty tied to tariffs and inflation.

- Chairman Powell said the Fed will "make smarter and better decision if we wait to get a sense of the pass-through of inflation and the effects on spending, and hiring, and all those things."

- Chairman Powell reiterated the amount of uncertainty in and from the Dot Plot, "no one holds these rate paths with a lot of conviction," Powell said.

US TSYS

MNI US TSYS: Chairman Powell Presser Ongoing, Rates & Stocks Extend Lower

- Treasury futures and stocks are extending lows as Chairman Powell's press conference continues.

- Tsy Sep'25 10Y futures currently -3 at 110-24 vs. 110-22.5 overnight low.

- Initial support to watch lies at 109-28, the Jun 6 / 11 low. A breach of this level would be bearish and open the bear trigger at 109-12+, the May 22 low.

- Curves steeper, 2s10s +1.414 at 44.697, 5s30s +0.263 at 90.075.

- Cross asset: Stocks trading lower now (SPX eminis -7 at 6035.25), Gold slipping lower at 3376.30, Bbg US$ index rebounds: 1210.77 +1.70.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.31% (-0.01), volume: $2.692T

- Broad General Collateral Rate (BGCR): 4.29% (-0.01), volume: $1.087T

- Tri-Party General Collateral Rate (TCR): 4.29% (-0.01), volume: $1.063T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $285B

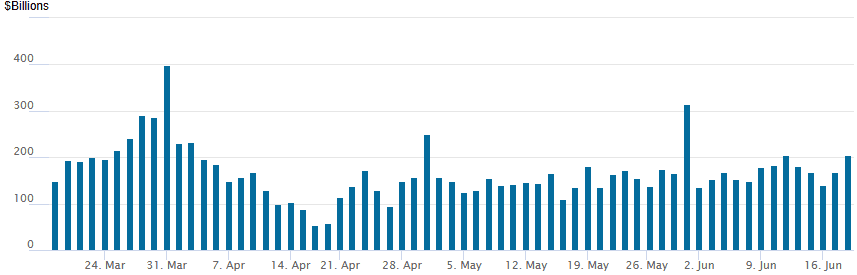

FED Reverse Repo Operation

RRP usage climbs to $205.050B this afternoon from $168.939B yesterday, total number of counterparties at 40. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Mixed SOFR & Treasury option flow on net, underlying futures well off initial gap bid post FOMC, curves mildly steeper while projected rate cut pricing gains slightly on longer dates vs. this morning's levels (*) as follows: Jul'25 at -2.6bp (-3.6bp), Sep'25 at -18.7bp (-17.7bp), Oct'25 at -31.6bp (-29.1bp), Dec'25 at -48.2bp (-45.1bp).

SOFR Options:

+3,000 SFRH6 95.50 puts, 3.0 vs. 96.325/0.10%

+2,500 SFRZ5 96.25/96.37/96.62/96.75 call condors, 1.75

-1,000 SFRZ5 96.12 straddles, 42.5

+4,000 SFRU5 95.68/95.81/96.00/96.12 put condors, 4.5

+2,000 SFRZ5 95.75 puts, 3.75

-5,000 SFRN5 95.68/95.81 put spds, 1.75 ref 95.89

Pit/screen over +55,000 SFRU5 95.50/95.62 put spds, .25 ref 95.86, bid for more

3,700 SFRZ5 96.25/96.50 call spds vs. 95.68 puts ref 96.115

-3,000 0QN5 97.25/97.31 call strip vs. SFRN5 96.50/96.56 call strip, cab net 0QN over

+4,000 SFRQ5 95.68/95.75 put spds, 2.5 ref 95.855

+5,000 0QH6 97.25/98.00 call spds, 13.0 vs. 96.745/0.18%

2,000 SFRV5 96.18/96.43 call spds ref 96.09

2,800 SFRU5 95.93/96.00/96.06 call flys

+3,000 SFRU5 95.56/95.62/95.68 put flys, 1.25 ref 95.86

+12,800 SFRH6 96.50/97.00/98.00 broken call flys, 2.5 ref 96.32 to -.33

1,600 3QZ5 96.25/96.62/97.00 call flys, 8.0

Treasury Options: (July serial options expire Friday)

5,000 FVU5 111 calls, 10.5 ref 108-07.75 to -08

2,500 TUN5 103.25/103.37/103.5/103.62 put condors, ref 103-22

1,250 FVN5 108.25/108.5/109/110 broken call condors ref 108-09.75

1,800 FVN5 107.25/107.75/108.25 put flys ref 108-09.5

2,000 USU5 114/116/118 call flys ref 114-06

+5,000 TYQ5 110.5/111.5/112 1x3x2 call flys 4 over TYQ5 112/113/113.5 1x3x2 call flys

+2,000 TYQ5 114.5 calls, 8

-3,000 TYN5 110.75 calls, 16 vs 110-22.5/0.50%

+3,000 TYN5 111.5 calls, 6

+1,500 Wed wkly TY 110.75/111/111.25 call flys, 3.0

+6,500 Wed wkly FV 107.5/107.75 put spds, 1 (exp today)

+2,000 TYN5 110.5/111/111.5 call flys, 8

MNI BONDS: EGBs-GILTS CASH CLOSE: UK Curve Bull Flattens Ahead Of BOE

Curves bull flattened Wednesday, with Gilts modestly outperforming Bunds ahead of Thursday's BOE decision announcement.

- Early trade saw some bull steepening led by Gilts after UK CPI data looked in line with expectations.

- There was a broad rally across core FI for almost the entire remainder of the session however, with the long end leading gains.

- The main triggers were weak-leaning US data (jobless claims and residential construction), with lower oil prices as US President Trump seemingly views a near-term resolution on the Iran-Israel conflict.

- The German and UK curves both bull steepened on the day. Periphery/semi-core EGB spreads were little changed.

- Overnight focus will be on the US Federal Reserve, but the BOE takes centre-stage Thursday - MNI's preview is here.

- It would be a surprise to markets if the outcome is anything other than an on hold decision with unchanged official guidance. Expectations are relatively strongly pointing towards a 7-2 vote split for a hold/cut respectively.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.6bps at 1.842%, 5-Yr is down 3.8bps at 2.103%, 10-Yr is down 3.8bps at 2.497%, and 30-Yr is down 4.1bps at 2.944%.

- UK: The 2-Yr yield is down 3.5bps at 3.888%, 5-Yr is down 4.7bps at 4.006%, 10-Yr is down 5.5bps at 4.495%, and 30-Yr is down 5.4bps at 5.229%.

- Italian BTP spread down 0.2bps at 95bps / French OAT unchanged at 71.5bps

MNI EGB OPTIONS: More Upside In Rates, Including An ECB Cutting Play

Wednesday's Europe rates/bond options flow included:

- RXN5 131c vs RXQ5 132c spread, sold the Aug at 32 in 3.1k

- RXQ5 130/128.5ps, bought for 44 in 3.1k

- ERX5 98.5625/98.625cs, bought for half in 34.8k

- ERH6 98.5625/98.1875ps 1x2 sold at 10.75 down to 10.5 in 20k

- ERH6 98.0625/98.1875/98.50/98.625c condor vs 97.875p, bought the condor for half in 2.5k

MNI FOREX: Greenback Reverses Higher as Powell Downplays Economic Concerns

- The US dollar spent much of the pre-Fed session trading with a moderate downward bias as President Trump hinted at potential talks with Iran, which fleetingly boosted risk sentiment. On the FOMC release, this greenback weakness extended as the Fed confirmed the median dot for 2025 year-end rates as steady in predicting two further cuts this year.

- USDJPY traded down to a low of 144.34 on the release, while EURUSD tried to consolidate gains back above 1.15.

- However, higher median Fed dots for 2026 and 2027 and a relatively optimistic view of economic activity and the labour market prompted a sharp dollar reversal higher through Chair Powell’s press conference, with the USD index rallying to fresh session highs.

- Once again, USDJPY was in focus here as the pair rose back above 145.00, narrowing the gap to the overnight highs and initial resistance around 145.45. Further out, key short-term resistance is 146.28, the May 29 high.

- Both the EUR and GBP were laggards amid the dollar reversal, both notable underperformers across G10. For GBPUSD, we have printed fresh pullback lows as the move extends below 1.3415, placing greater attention on the next important support, which lies at 1.3350, the 50-day EMA.

- Thursday remains busy on the central bank front, with the SNB kicking off the calendar. This will be followed by decisions from the Norges Bank and the BOE. In terms of data, New Zealand GDP and Australian employment figures are scheduled.

MNI OPTIONS: Expiries for Jun19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1415-25(E2.4bln), $1.1475-00(E2.5bln), $1.1510-20(E629mln), $1.1545-50(E1.2bln), $1.1585-00(E3.2bln)

- GBP/USD: $1.3500(Gbp511mln)

- EUR/GBP: Gbp0.8600(E519mln)

- EUR/JPY: Y161.90-00(E981mln)

- AUD/USD: $0.6460(A$741mln), $0.6550(A$683mln), $0.6600(A$1.1bln)

EQUITIES

MNI US STOCKS: Late Equities Roundup: Back to Geopol Risk Watching, Eqs Pare Gains

- Stocks reversed moderate session support after the Federal Reserve held rates steady, continuing to express patience in changing rates amid ongoing tariff related pass-through inflation.

- "We'll make smarter and better decision if we wait to get a sense of the pass-through of inflation and the effects on spending, and hiring, and all those things," Chairman Powell said. Back to watching geopolitical headlines regarding Iran/Israel war.

- Currently, the DJIA trades down 17.77 points (-0.04%) at 42197.95, S&P E-Minis up 5 points (0.08%) at 6043.75, Nasdaq up 56 points (0.3%) at 19576.7.

- Gainers led by Coinbase Global climbing 15.74% after a Stablecoin bill cleared the Senate. Other leaders included TKO Group Holdings +5.41%, Caesars Entertainment +4.31%, Jabil +4.27%, Nucor +4.17% and Super Micro Computer +3.41%.

- Conversely, financial services led laggers in the second half: Mastercard -5.29%, Visa -4.48%, Paycom Software -3.63%, PayPal Holdings -3.47% and Corpay -3.06%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Structure Remains Bullish

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11 and the bull trigger

- PRICE: 6047.75 @ 14:27 BST Jun 18

- SUP 1: 5979.00/5896.83 Low Jun 13 / 50-day EMA

- SUP 2:5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6003.83, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5896.83. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

MNI COMMODITIES: Crude Rangebound, Gold Steady After Fed Rate Hold

- Crude prices have struggled for clear direction today after Trump’s comments seemed to suggest that Iran wanted to negotiate, while also somewhat distancing the US from direct involvement.

- WTI Jul 25 is up by 0.1% at $74.9/bbl.

- Global oil markets remain well supplied according to the IEA as long as Middle East escalations do not lead to disruptions. Slowing global demand and increased OPEC+ production are providing a buffer.

- The sharp rally in WTI futures in recent sessions marked an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is in an extreme overbought position.

- A continuation higher would expose the $80.00 handle, while a firm support is noted at $68.49, the Jun 13 low.

- Meanwhile, spot gold is broadly unchanged on the session around $3,390/oz, as it also consolidates recent gains, which saw the yellow metal trade as high as $3,451 at the start of this week.

- A bullish theme in gold remains intact and recent gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend.

- Resistance at $3,435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3,500.1, the Apr 22 all-time high.

- Initial key support to monitor is $3,276.3, the 50-day EMA.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 19/06/2025 | 0730/0930 | *** | SNB PolicyRate | |

| 19/06/2025 | 0730/0930 | *** | SNB Interest Rate Decision | |

| 19/06/2025 | 0730/0930 | ECB's Lagarde On Economic and Financial Integration | ||

| 19/06/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 19/06/2025 | 0900/1100 | ** | Construction Production | |

| 19/06/2025 | 0945/1145 | ECB de Guindos On Eurozone Economic Outlook | ||

| 19/06/2025 | 1030/1230 | ECB Lagarde Keynote Speech At Economic Integration Conference | ||

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | - | ECB Cipollone At Eurogroup Meeting | ||

| 19/06/2025 | 1600/1800 | ECB Lagarde At Financi'Elles event | ||

| 20/06/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 20/06/2025 | 2330/0830 | *** | CPI |