MNI ASIA MARKETS ANALYSIS: Headline Risk Eases

HIGHLIGHTS

- Treasuries look to finish mildly lower - back near opening levels after whipsawing lower after weekly claims & retail sales data - inexplicably rebounding to post session highs soon after.

- Treasuries spent the rest of the day gradually unwinding support to mildly lower after the bell, curves unwinding a small portion of Wednesday's steepening (2s10s -1.724 at 54.217).

- The US dollar traded with a constructive tone on Thursday as markets stabilised following late volatility induced by the Trump-Powell headlines yesterday.

- Stocks climbed to new highs, Information Technology, Industrial and Consumer Staples sector shares outperforming.

US TSYS

MNI US TSYS: Near Midrange After Early Post-Data Volatility

- Treasuries look to finish near opening levels after whipsawing lower/higher following this morning's data. Less headline driven volatility on the day as threats of Pres Trump threats to fire Fed Chair Powell ahead of his May 2026 term end cooled.

- Treasury futures extend lows after lower than expected weekly and continuing jobless claims, retail sales higher than expected (modest up-revisions to prior), import prices lower/export higher than expected. little react to latest in-line Business Inventories & Housing Markets index data.

- Trading desks at a loss to explain the rebound off this morning's lows, no particular headline or flow drivers as Tsys climb past yesterdays highs - back to early Tuesday levels.

- The latest weekly jobless claims report was better than expected for both initial and continuing claims, extending improvements in initial claims (and this time for a payrolls reference period) whilst continuing claims stabilize rather than extend what had been a sharp rise back in June.

- Retail sales were more solid than expected in June. It was expected that the GDP-input Control Group category would come in stronger than the other main aggregates, due in large part to anticipated weakness in auto sales, but this did not play out: Control was actually one of the weaker parts of this report relatively speaking, rising 0.5% M/M - above expectations of 0.3%, but this was offset by a 0.2pp downward rev to 0.2% in May.

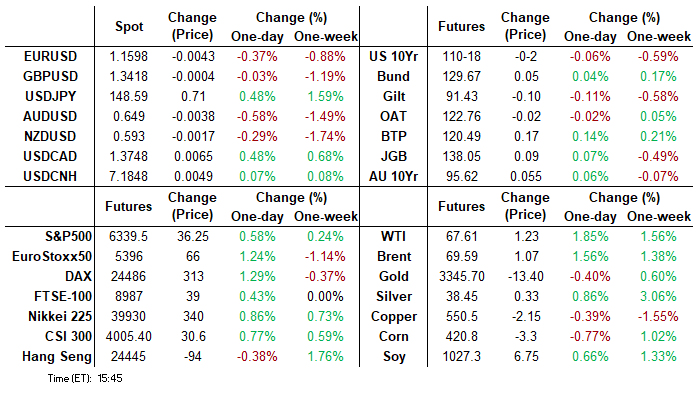

- Currently, Sep'25 10Y futures -2.5 at 110-17.5 vs. 110-25 high, 10Y yld +.0020 at 4.4573%, curves remain flatter after basis hit highest levels since October 2021 late Wednesday: 2s10s currently -2.219 at 53.722, 5s30s -1.098 at 100.548.

- Cross asset: stocks firmer/new highs (SPX eminis +39.5 at 6342.75); Bbg US$ index firmer/off highs (BBDXY +3.45 at 1207.56); Gold weaker/off lows (-6.73 at 3340.40); crude firmer (WTI +1.19 at 67.57).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.03), volume: $2.771T

- Broad General Collateral Rate (BGCR): 4.33% (-0.03), volume: $1.141T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.03), volume: $1.108T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

FED Reverse Repo Operation:

RRP usage slips to $193.660B this afternoon from $197.086B yesterday, total number of counterparties at 35. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option flow revolved low delta puts with underlying futures back near opening levels after whipsawing lower/higher in early trade, have been scaling steadily off highs since consolidating. Curves flatter (2s10s -1.524 at 54.417) while projected rate cut pricing cools slightly from early morning/pre-data (*) levels: Jul'25 at -0.6bp, Sep'25 at -14.2bp (-14.2bp), Oct'25 at -26.1bp (-26.6bp), Dec'25 at -42.7bp (-43.8bp).

SOFR Options:

2,500 SFRV5/SFRU5 95.68 put spds

+4,000 SFRU5 95.68/95.75/95.87 2x3x1 put flys, 2.0 ref 95.82

+10,000 SFRU5 95.68/95.75/95.81 2x1x1 put trees, 0.5

1,000 SFRZ5 95.75/95.87/96.25/96.37 put condors ref 96.09

1,200 0QU5 96.62/96.87 put spds ref 96.72

+2,000 SFRU5 95.68/95.81 put spds

2,400 SFRZ 96.43/96.87 strangles, 47

+2,500 SFRZ5 96.12/96.25/96.37/96.50 call condors, 2.0 ref 96.125/0.05%

Treasury Options:

+6,630 TYU5 110 puts, 29

Block/screen 15,000 USU5 110 puts, 50 ref 112-14/0.28%

2,668 TYU5 110.5/111.5 1x3 call spds

3,000 USQ5 113/114 1x2 call spds, 6 net ref 112-13

+5,000 TYQ5 110.5 straddles, 41

-10,000 TYU5 112.5 calls, 13

2,600 TYU5 110.5/111.5/112 1x3x2 broken call flys ref 110-22.5

1,500 TUU5 103.25/103.5/103.62/103.75 broken put condors ref 103-19.5

over 10,000 TYQ5 110 puts, 11

over -5,100 TYU5 108/109 put spds, 10 ref 110-13.5

2,500 USU5 108 puts, 39 ref 112-01

8,330 TYQ5 110.5/111.5 2x1 put spds ref 110-13.5

+15,000 wk3 TY 110.5 puts, 11

2,100 TYV5 110/111/112 call flys ref 110-10.5

5,000 TYV5 112 calls ref 110-14.5

1,500 FVQ5 107.25/107.5 put spds ref 108-00.75

-1,000 FVQ5 107.5 straddles, 41

+2,000 TYU5 111.5/112/113 broken call flys, 1 vs. 110-19/0.05%

-1,500 FVU5 108.25 straddles, 103.5

-3,000 TYQ5 109.75 puts, 6

+5,000 USU5 109 puts, 55

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform On Data...Again

Gilts underperformed Bunds for a second day Thursday, with UK data again coming in firmer than expected.

- For the second consecutive session, Gilt yields gapped higher at the open, with UK labour market data a little firmer than expected on net, including an upward revision to May payrolls and solid private regular AWE but a slightly above-expected LFS unemployment rate.

- This reducing the implied probability of remaining 2025 cuts, in turn seeing the UK short-end underperform on the day.

- Spanish and French supply helped weigh on EGBs early as well.

- However, Gilts and Bunds regained ground over the course of the session, boosted in mid-afternoon trade by a spillover rally in US Treasuries as import price data came in on the soft side. With the long-end leading the rally, curves extended a flattening move going into the cash close.

- On the day, the German curve twist flattened, with the UK's bear flattening.

- Periphery / semi-core EGB spreads closed modestly wider.

- Friday's calendar is on the lighter side, with German producer prices and Eurozone current account / construction data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.2bps at 1.862%, 5-Yr is down 0.1bps at 2.229%, 10-Yr is down 1.2bps at 2.675%, and 30-Yr is down 1.6bps at 3.198%.

- UK: The 2-Yr yield is up 5bps at 3.905%, 5-Yr is up 4.6bps at 4.088%, 10-Yr is up 1.6bps at 4.655%, and 30-Yr is up 1.3bps at 5.482%.

- Italian BTP spread up 0.3bps at 85.9bps / Spanish up 0.7bps at 61.6bps

MNI OPTIONS: Slew Of Sonia Call Structure Buying After CPI, Labour Reports

Thursday's Europe rates/bond options flow included:

- ERZ5 98.125/98.25/98.375 call fly paper paid 3.5 on 8K and 3K

- SFIQ5 95.95/95.90 put spread 12.5K given at 0.25

- SFIZ5 96.25/96.50/96.75 1x3x2 call fly, bought for 3.25 in 5k, now bought for 15k all day

- SFIZ5 96.30/96.55/96.80 1x3x2 call fly paid 3.0 on 11K

- SFIZ5 96.40/96.60 call spread vs. 5.6k SFIZ5 96.30 puts net paid -0.125 for the call spread - package 11.2K

- SFIH6 96.60/97.00 1x1.25 call spread paper paid 4.5 on 7.5K

- SFIH6 96.55/96.65 call spread vs. SFIH6 96.20/96.10 put spread paper paid 1.5 for the package on 10K, buying the call spread

MNI FOREX: DXY Consolidates Advance After Dipping From Fresh Recovery Highs

- The US dollar traded with a constructive tone on Thursday as markets stabilised following late volatility induced by the Trump-Powell headlines yesterday. The USD index spiked higher following the stronger set of US retail sales data, lower initial jobless claims and a much firmer-than-expected Philly Fed business outlook, allowing the DXY to reach fresh recovery highs. However, lower-than-expected import prices did immediately offset this sentiment and prompted a quick reversal of the post-data greenback advance.

- After this, currencies traded with a subdued tone - reflective of the markets taking a breather following the Trump-induced volatility – which allowed the markets to digest the last scheduled appearances for FOMC speakers before the media blackout starts this weekend. There is also a lack of meaningful data on Friday’s calendar.

- AUD (-0.65%) remains an underperformer following the weaker-than-expected jobs report overnight and the notable uptick in the unemployment rate, which have bolstered RBA easing expectations. For AUDUSD, today’s move below the 50-day EMA (intersects at 0.6490) appears meaningful, and a daily close below this average would be the first in over three months, highlighting a stronger reversal. The initial target for the move would be 0.6435 (Fib retracement) before 0.6373, the Jun 23 low and technical bear trigger.

- Greenback strength has notably weighed on the Japanese yen Thursday, with USDJPY bouncing over 200 pips from yesterday’s low to briefly trade back above 149.00. Yesterday’s highs at 149.18 capped gains and will be the short-term reference point above as markets eagerly await trade discussions between US/Japan officials and this weekend’s upper house election. Above here, attention will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high.

- GBP has moderately outperformed on Thursday, following this morning’s UK labour market data which was a little firmer-than-expected. This has allowed EURGBP to further unwind a small portion of the punchy move higher across June and July, trading back below 0.8650. It is worth noting that moving average studies are in a bull-mode position, highlighting a dominant uptrend, and initial support to watch lies at 0.8606, the 20-day EMA.

- Japan National Core CPI will print overnight before US housing starts and UMich sentiment and inflation expectations highlight the US calendar.

MNI FX OPTIONS: Expiries for Jul18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1566-70(E899mln), $1.1600(E2.2bln), $1.1650(E1.0bln), $1.1700(E1.3bln), $1.1850(E1.2bln)

- USD/JPY: Y148.00($597mln), Y148.25($844mln), Y148.50($521mln)

- GBP/USD: $1.3395-10(Gbp1.3bln)

- AUD/USD: $0.6455-60(A$695mln), $0.6480-00(A$1.2bln)

- NZD/USD: $0.5932-50(N$498mln)

- USD/CAD: C$1.3715-30($1.3bln)

MNI US STOCKS: Late Equities Roundup: IT, Industrials, Staples Outperforming

- Stocks hold near midday highs late Thursday, SPX eminis near early Tuesday's all-time highs (6342.00) after this morning's better than expected Retail Sales and lower jobless claims data, Information Technology, Industrial and Consumer Staples sector shares outperforming.

- Currently, the DJIA trades up 271.49 points (0.61%) at 44527.38, S&P E-Minis up 36 points (0.57%) at 6339.25, Nasdaq up 163.1 points (0.8%) at 20894.09.

- Leading gainers in late trade included: Albemarle Corp +8.66%, Snap-on +7.52%, PepsiCo +6.83%, Allegion +4.63%, Eaton Corp +4.31%, Hubbell +3.84%, Palantir Technologies +2.75% and Oracle +2.36%.

- On the flipside, Health Care sector shares weighed on indexes, partially tied to lagging earnings, funding cuts and tariff-related passthrough drag: Elevance Health -11.45%, Abbott Laboratories -8.1%, Molina Healthcare -4.67%, Centene -3.63%, Eli Lilly -3.58% and Baxter International -2.47%.

- On earnings, Interactive Brokers Group and Netflix report after today's close. Reporting early Friday: Charles Schwab, Truist Financial Corp, 3M Co, Comerica, Southern Copper Corp, Huntington Bancshares, Schlumberger, American Express and Ally Financial.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bullish Trend Conditions

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6343.00 High Jul 15

- PRICE: 6339.25 @ 14:34 BST Jul 18

- SUP 1: 6241.00 Low Jul 16

- SUP 2: 6226.62/6082.03 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

S&P E-Minis are still trading in a range, closer to their recent highs. The trend condition remains bullish. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7. This was followed by a break of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6082.03.

MNI COMMODITIES: Crude Rises, Gold Edges Lower

- Crude is higher today but remains within the trading range seen since Tuesday with focus on US trade talks, potential secondary tariffs on Russia, and near-term market tightness.

- President Trump’s White House Press Secretary said that secondary sanctions would apply to Russian oil buyers.

- WTI Aug 25 is up by 1.8% at $67.6/bbl.

- A bearish tone in WTI futures remains intact. The sharp reversal from the June 23 high continues to highlight scope for an extension lower and this suggests that recent gains have been corrective.

- Support to watch is the 50-day EMA, at $65.61. Initial resistance to monitor is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Meanwhile, spot gold has edged down by 0.3% to $3,338/oz as the US dollar traded with a more constructive tone following yesterday’s late volatility.

- A bull cycle in gold that started June 30 remains intact and the yellow metal is holding on to the bulk of its recent gains.

- Note that medium-term trend conditions are bullish, with moving average studies in a bull-mode position, highlighting a dominant uptrend.

- An extension would expose $3,395.1, the June 23 high, and $3,451.3, the June 16 high.

- On the downside, first support to watch is $3,282.8, the July 9 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/07/2025 | 0600/0800 | ** | PPI | |

| 18/07/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/07/2025 | 0900/1100 | ** | Construction Production | |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 18/07/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |