MNI ASIA MARKETS ANALYSIS: Hassett Odds as Fed Chair Ebb/Flow

HIGHLIGHTS

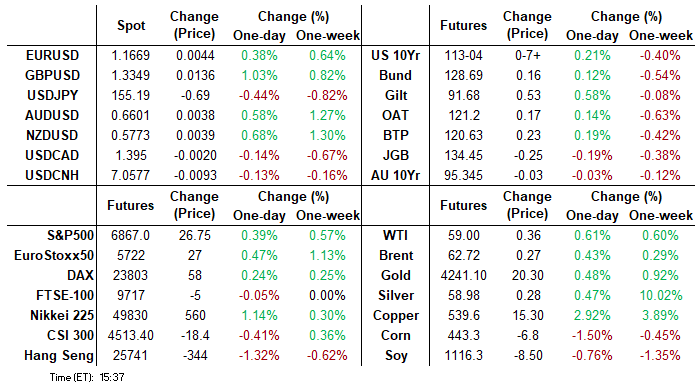

- Treasuries look to finish moderately higher Wednesday - off early session highs after a flurry of mixed data and market discussions over Kevin Hassett's chances of becoming the next Fed Chair in May 2026.

- Stocks climbed to the best levels since mid-November after Microsoft denied a write-up from "The Information" they had lowered "AI software sales quotas".

- Broad dollar weakness has been notably extended Wednesday, prompting the DXY to print fresh pullback lows below 99.00, reaching a five-week low at 98.83.

- Thursday Data Calendar: Challenger Job Cuts, Weekly Claims, Revelio & Regional Fed Data

US TSYS

MNI US TSYS: Tsys Grind Off Midmorning Lows, Mixed Data Ahead Thursday Weekly Claims

- Treasuries look to finish moderately firmer Wednesday - off early morning highs following a flurry of economic data.

- TYH6 currently +7.5 at 113-04 vs. 113-07 high, initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25.

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February. The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- The S&P Global US services PMI was revised lower in the final November release 54.1 (flash & cons 55.0) in Nov final after 54.8 in Oct, dipping to its lowest since June rather than confirming what had been its highest since July.

- Stocks continue to plow higher Wednesday, recovering from early session lows after Microsoft denied a write-up from "The Information" they had lowered "AI software sales quotas". Pretty specific, nevertheless, while market concerns over stretched AI-tied valuations are on full display.

- Charles Gasparino at Fox Business reports on X that there is a 'last-ditch' effort by Wall Street and corporate America insiders to caution President Donald Trump against nominating National Economic Council Director Kevin Hassett as Federal Reserve Chair.

- Look Ahead Thursday Data Calendar: Challenger Job Cuts, Weekly Claims, Revelio & Regional Fed Data.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.01% (-0.11), volume: $3.407T

- Broad General Collateral Rate (BGCR): 3.96% (-0.11), volume: $1.310T

- Tri-Party General Collateral Rate (TCR): 3.96% (-0.11), volume: $1.276T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $91B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $160B

FED Reverse Repo Operation

RRP usage retreats to $2.514B while counterparties surge to 40 this afternoon from $5.620B Tuesday. Compares to last Tuesday November 18: $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options remained mixed after better downside put interest early overnight. Underlying futures well off midmorning lows - still off early morning highs. Projected rate cut pricing mixed vs. early morning levels (*): Dec'25 at -23.6bp (-24.6bp), Jan'26 at -31.4bp (-31.8bp), Mar'26 at -40.4bp (-39.8bp), Apr'26 at -47.9bp (-46.3bp).

SOFR Options:

+6,000 SFRZ5 96.12 puts, .25 vs. 96.2825

+15,000 SFRF6 96.50/96.75 call spds 2.0-2.75 over 96.37 puts ref 96.465

+4,000 SFRH6 96.75 calls, 4.0 vs. 96.475/0.20%

2,089 SFRZ5 96.12/96.18/96.25 call flys

2,000 0QZ5 96.81/96.87/97.00/97.06 call condors ref 96.95

3,500 SFRZ5 96.31/96.37 call spds ref 96.275

5,000 SFRZ5 96.25/96.31 call spds ref 96.2725

over 9,600 SFRZ5 96.31 calls ref 96.2725

3,000 SFRH6 96.00 puts ref 96.445

+6,000 SFRZ5 96.25/96.37 put spds, 9.0

+5,000 SFRZ5 96.18/96.25 put spds, 0.75

+7,500 SFRH6 96.18/96.25/96.31 put trees, 0.0 vs. 96.405/0.02%

+6,000 SFRH6 96.18/96.31/96.37 broken put flys, 2.0

over -4,100 SFRM6 98.00 calls, 2.0 ref 96.715/0.04%

+1,850 SFRF6 96.56/96.75 call spds, 2.75 vs 96.46/0.18%

Treasury Options:

-5,000 TYF6 112.5/113.5 strangles, 39

+84,361 wk2 Fri 30Y 106 puts, cab-7**

3,000 Wed wkly 113.5 calls ref 113-03.5 (exp today)

2,000 USG6 108 puts ref 116-21

-2,500 TYF6 114/114.75 call spds, 9 vs. 113-08/0.12%

+2,000 USG6 108/112 3x1 put spds, 6 ref 116-14

2,000 USF6 125.5 calls ref 116-16

+1,750 FVF6 111 calls, 3 vs. 109-20.5/0.08%

+7,600 Wed wkly 113 calls ref 112-28 to 30 (exp today)

tyf6 114/114.75 cs vs 113-08 12% seller 9s 2500x 648am

**File under patently absurd low-delta 30Y put trade:

84,361 wk2 30Y 106 puts trade on screen at cab-7

The 10 handle out-of-the-money option expires next week Friday - after the final FOMC of 2025. while markets are widely anticipating a 25bp rate cut on December 10.

Most likely a hedge vs some short term balance sheet risk that corresponds to a rise in 30Y yield to (rough) appr 5.48% from current yield of 4.73%. (Two caveats: bond cheapest to deliver will change to a higher duration bond most likely; the duration on US 30y cash and USH prob ably won't shift in parallel.)

There has been a rise in low delta option trades - Treasury & SOFR - on both sides of the curve over the last few sessions. SOFR has seen rise of par (100 strike) and above call options in midcurves targeting early 2026.

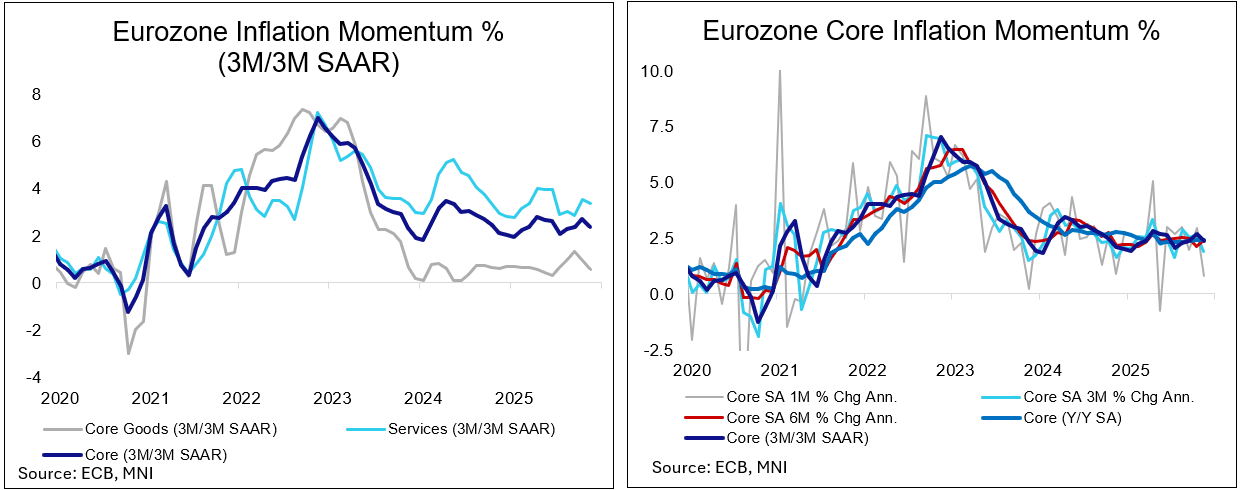

MNI EUROPEAN INFLATION: MNI Eurozone Inflation Insight – Nov 2025

MNI Eurozone Inflation Insight, offering MNI analysis across a range of Eurozone-wide and country-level inflation metrics for the flash November release. You can find the full report here.

- HICP inflation was as originally expected but marginally above where consensus likely stood following most country-level data in the flash November release. Core HICP was in line with expectations.

- Energy was the main mover and surprise, coming in 0.3pp above expectations.

- The full November release on Dec 17 will provide a more useful update on exact drivers. That especially applies to services inflation, where it is not yet clear to what extent firm October airfares may have unwound.

- By country, Germany and Spain were stronger than expected, while France, Italy and the Netherlands saw downside misses.

- The ECB is still seen as being highly unlikely to cut at its Dec 18 meeting (<1bp priced), where new projections will be watched to judge whether a very mild easing bias (6bp of cuts by mid-2026) is warranted.

MNI FOREX: Dollar Index Breaks to 5-Week Lows, GBPUSD Surges Over 1%

- Broad dollar weakness has been notably extended Wednesday, prompting the DXY to print fresh pullback lows below 99.00, reaching a five-week low at 98.83. This extends the two-week selloff to around 1.55%, with the index previously stalling at touted 100.48 resistance in November.

- Greenback weakness continues to be a reflection of a more dovish profile for the Fed under potential Kevin Hassett leadership and an associated more optimistic risk backdrop. Weaker-than-expected ADP jobs data from the US and a softer headline ISM services PMI work in favour of the short-term narrative playing out.

- The USD index looks set to post a significant technical close, with the first daily close below the 50-day exponential moving average since early October. This impulse is generating several bullish signals across the rest of the G10 basket, and continues to bolster the optimistic sentiment for EM FX.

- GBP is a notable outperformer, assisted by a set of stronger PMI data this morning. The 1.05% rally for cable today may have been assisted by positioning dynamics as pre-budget positioning is squeezed further. Spot has narrowed the gap substantially to 1.3368, a Fibonacci retracement. Above here, 1.3416 is the next notable resistance, the Oct 21 high.

- The significance of the break below the 50-day EMA in EURGBP at 0.8755 also stands out. The cross is now on course for a close below the late November lows and the lowest level since October 28th.

- Elsewhere, AUDUSD has now printed eight consecutive sessions of higher highs, keeping a bullish theme firmly intact, while it is worth reiterating that a primary driver of AUD strength is the continued pullback in front-end vols. Price action narrows the gap to the Oct 29 high at 0.6618, which is a key near-term resistance. In similar vein, NZD continues its post-RBNZ recovery, with today’s 0.7% gains edging spot closer to the medium-term pivot at 0.5800.

- Both EUR, JPY and CHF are slightly underperforming G10 peers and the adjustment of the DXY, however, EURUSD looks set to close above a key resistance of 1.1656, a strong reversal signal.

MNI FX OPTIONS: Expiries for Dec04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E4.1bln), $1.1600(E2.2bln), $1.1650(E2.3bln), $1.1675(E1.6bln), $1.1700(E708mln)

- USD/JPY: Y153.00($1.2bln), Y154.00($900mln), Y155.50-70($1.6bln)

- GBP/USD: $1.3030-50(Gbp2.1bln)

- AUD/NZD: N$1.1365(A$600mln)

MNI US STOCKS: Late Equities Roundup: Best Levels Since Mid-November

- Stocks continue to plow higher Wednesday, recovering from early session lows after Microsoft denied a write-up from "The Information" they had lowered "AI software sales quotas". Pretty specific, nevertheless, while market concerns over stretched AI-tied valuations are on full display.

- The Information wrote: "Executives at Microsoft and other enterprise software firms heralded 2025 as the year artificial intelligence would be capable of automating tasks that involve multiple steps, such as generating dashboards based on company sales data. But as the year comes to a close, Microsoft has lowered expectations for how quickly it can get customers to spend money on these newer products, known as agents. Multiple Microsoft divisions, for instance, have lowered how much salespeople are supposed to grow".

- Currently, the DJIA trades up 450.77 points (0.95%) at 47925.84, S&P E-Mini Futures up 27 points (0.39%) at 6867.25, Nasdaq up 57.8 points (0.2%) at 23471.29.

- Information Technology and Utilities sector shares led declines in late trade:

- While chip makers traded strong ahead midday (Microchip Technology +9.75%, ON Semiconductor +8.65%, NXP Semiconductors +5.34% and Cadence Design Systems +4.22%), there was a greater breadth of software laggers: Sandisk Corp -8.28%, Seagate Technology -4.97%, Western Digital -3.25%, Micron Technology -2.89% and Microsoft -1.70%..

- Meanwhile, Southern Co -1.64%, Exelon Corp -1.39%, PPL Corp -1.38%, PG&E -1.01% and Duke Energy -1.00% continued to weigh on the Utilities sector.

- On the positive side, Energy and Financial Services sector shares led advances in the first half:

- APA Corp +4.79%, EQT Corp +4.30%, Expand Energy +3.83% and Targa Resources +3.01%

- Robinhood Markets +5.40%, Fiserv Inc +4.38%, Coinbase Global +4.16%, Blackrock +3.43% and Citigroup +3.17%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Holding On To Its Recent Gains

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6852.56 76.4% retracement of the Oct 30 - Nov 21 bear leg

- RES 1: 6871.75 High Dec 3

- PRICE: 6870.00 @ 1455 ET Dec 3

- SUP 1: 6674.50/6525.00 Low Nov 25 / 21

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

S&P E-Minis are holding on to their recent gains following the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

MNI COMMODITIES: Crude Rises, Copper Extends Gains Amid Supply Concerns

- WTI crude prices have risen today after limited signs of a breakthrough in Ukraine peace plan discussions, while Caspian Pipeline Consortium disruption continues to be monitored.

- Weekly EIA data showed a modest rise in crude stocks while product builds were more substantial.

- WTI Jan 26 is up by 0.4% at $58.9/bbl.

- US Secretary of State Rubio said that talks are currently at the point of trying to work out what Ukraine can accept and to bridge the divide between it and Russia.

- For WTI futures, moving average studies are in a bear-mode position, highlighting a dominant downtrend. Key support and the bear trigger remains at $55.99, the Oct 20 low, while key short-term resistance is $61.84, the Oct 24 high.

- Meanwhile, spot gold has unwound earlier gains, which saw it trade as high as $4,241.5/oz, with price currently broadly unchanged at $4,209/oz.

- 20- and 50-day exponential moving averages continue to provide the notable supports, intersecting at $4,133 and $4,017 respectively.

- On the upside, sights are on key resistance and the bull trigger at $4,381.5, the Oct 20 high.

- Elsewhere, copper has outperformed on Wednesday, amid concerns of a US tariff-related squeeze on global supplies. Price is up by 2.9% at $539/lb, taking total gains since the Nov 21 lows to around 8%.

- Next resistance is at $550, the Jul 9 and 28 lows, a clearance of which would open $588.70, the Jul 30 high.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0800/0900 | ** | Unemployment | |

| 04/12/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/12/2025 | 0930/0930 | BOE Decision Maker Panel Data | ||

| 04/12/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/12/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference | ||

| 04/12/2025 | 1300/1400 | ECB Cipollone Chairs Panel on Fiscal Policy | ||

| 04/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 04/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 04/12/2025 | 1500/1000 | * | Ivey PMI | |

| 04/12/2025 | 1500/1600 | ECB Lane at Fiscal Policy Conference | ||

| 04/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 04/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/12/2025 | 1700/1200 | Fed Vice Chair Michelle Bowman | ||

| 04/12/2025 | 1800/1900 | ECB de Guindos Speech at Business Innovation Awards | ||

| 05/12/2025 | 2330/0830 | ** | Household spending |