US TSYS: Tsys Grind Off Midmorning Lows, Mixed Data Ahead Thursday Weekly Claims

Dec-03 20:28

- Treasuries look to finish moderately firmer Wednesday - off early morning highs following a flurry of economic data.

- TYH6 currently +7.5 at 113-04 vs. 113-07 high, initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25.

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February. The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- The S&P Global US services PMI was revised lower in the final November release 54.1 (flash & cons 55.0) in Nov final after 54.8 in Oct, dipping to its lowest since June rather than confirming what had been its highest since July.

- Stocks continue to plow higher Wednesday, recovering from early session lows after Microsoft denied a write-up from "The Information" they had lowered "AI software sales quotas". Pretty specific, nevertheless, while market concerns over stretched AI-tied valuations are on full display.

- Charles Gasparino at Fox Business reports on X that there is a 'last-ditch' effort by Wall Street and corporate America insiders to caution President Donald Trump against nominating National Economic Council Director Kevin Hassett as Federal Reserve Chair.

- Look Ahead Thursday Data Calendar: Challenger Job Cuts, Weekly Claims, Revelio & Regional Fed Data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

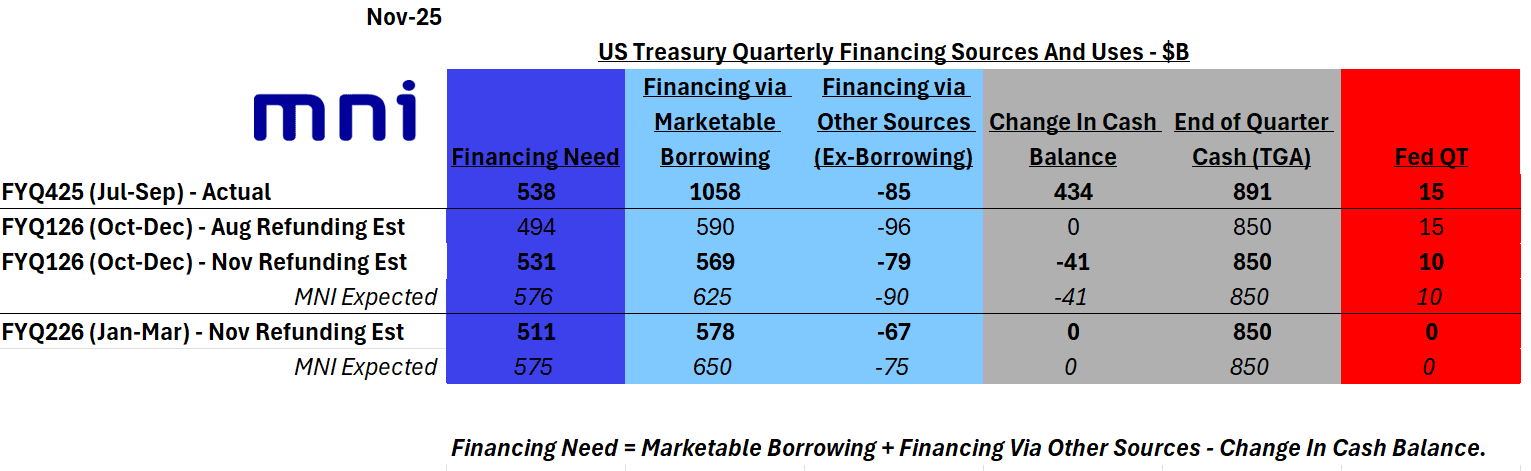

US TSYS/SUPPLY: Treasury Borrowing Requirements Come In On Low Side Of Expected

Nov-03 20:17

Treasury's borrowing / financing estimates (link) for the current and next quarters are in the table below. Main takeaways:

- The current quarter's borrowing requirements were lowered to $569B from August's $590B estimate. For the initial estimate of Jan-Mar requirements, a slight further uptick to $578B is seen.

- These borrowing estimates are below MNI's expectations and are at the lower end of most estimates we'd seen.

- Oct-Dec borrowing estimates ranged from $525B to a high end of $710B (when adjusting for analysts' TGA assumptions).

- For Jan-Mar estimates ranged from $387B to as high as $795B.

- End-quarter cash targets are unchanged at $850B. Some risk had been seen of an upward revision to $900B or higher, which would have upped the borrowing requirements.

PIPELINE: Corporate Bond Roundup: Over $40B to Price Monday

Nov-03 20:05

November kicks off with $40.25B corporate debt to price Monday, $17.5B Alphabet 8pt leading:

- Date $MM Issuer (Priced *, Launch #)

- 11/03 $17.5B #Alphabet: $1B 3Y +30, $500M 3Y SOFR+52, $2.5B +5Y +40, $1.25B 7Y +50, $3.5B 10Y +62, $2B 20Y +72, $4B 30Y +82, $2.75B 50Y +107 (massive debt issuance includes $6.5B over 6 tranches: 3Y, 6Y, 7Y, 13Y, 19Y and 39Y).

- 11/03 $6B #Novartis Capital: $700M 3Y +30, $800M 3Y SOFR+52, $1.75B 5Y +45, $925M 7Y +50, $925M 10Y +55, $350M 20Y +55, $550M 30Y +65

- 11/03 $4B #Qatar $1B 3Y +15, $3B 10Y Sukuk +20

- 11/03 $3.25B #UBS $2B 8NC7 +95, $1.25B 21.5NC20.5 +87.5

- 11/03 $2.35B #Shell $1B 5Y +50, $350M 5Y SOFR+78, $1B +10Y +67

- 11/03 $2B Tenet 7NC3 5.5%, 8NC3 6.0%

- 11/03 $1B #EBAY $600M 3Y +65, $400M 10Y +103

- 11/03 $1B #Nisource 30.7NC5.5 5.75%

- 11/03 $1B Neptune Bidco 5.5NC2

- 11/03 $600M #WEC Energy 30.5NC5.25 5.625%

- 11/03 $550M *EPR Properties 5Y +130

- 11/03 $500M *Lincoln National 10Y +125

- 11/03 $500M #Howmet Aerospace WNG 7Y +65

US TSYS: Late SOFR/Treasury Option Roundup

Nov-03 20:03

SOFR/Treasury option flow remained mixed Monday, modest week-opener volumes with no Gov-tied data on day 34 of the shutdown. Underlying futures weaker out the curve, short end mildly higher. Projected rate cut pricing gains slightly vs. late Friday levels (*): Dec'25 at -16.4bp (-15.6bp), Jan'26 at -24.6bp (-23.5bp), Mar'26 at -32.9bp (-32.1bp), Apr'26 at -39.1bp (-38.5bp).

- SOFR Options:

- 3,500 SFRZ5 96.06/96.12 put spds 1.75 ref 96.24

- +7,500 0QF6 97.12/97.37/97.43/97.68 call condors, 3.0 vs. 96.905/0.10%

- 4,000 SFRZ5 96.18/96.31/96.43/96.56 call condors ref 96.245

- 7,000 SFRX5 96.37/96.50 call spds, 0.37 ref 96.235

- 2,000 SFRM6 96.62 straddles, 39.5

- +7,000 0QF6 97.56 calls, 2.0 vs. 96.915/0.08%

- +2,000 SFRF6 96.37 put 1.25 over 0QF6 96.75 puts

- 1,750 0QZ5 96.68/96.75/96.87 put trees ref 96.895

- 1,000 SFRZ5 96.18/96.37/96.56 2x3x1 put flys ref 96.245

- 1,250 SFRZ5 96.18/96.31 put spds ref 96.24

- +2,500 SFRZ5 96.25/96.3125/96.4375/96.50 call condor, 3.25 vs. 96.27/0.05%

- 2,000 SFRZ5 96.12/96.18/96.25/96.31 call condors, 0.5

- Block, 4,000 SFRZ5 96.12/96.18 2x1 put spds, 0.5 ref 96.245

- Treasury Options:

- 5,000 TUG6 104.25 puts ref 104-10

- +10,000 TYZ5 112.25/Mon wkly 112.5 put diagonal spd, 6

- +1,000 FVF6 108.5/110.25 strangles 23 over FVZ5 108.25/110.5 strangles covered

- +5,000 TYZ5 111/112 put spds, 8

- -1,000 USF6 102/133 strangles, 2

- 5,000 wk2 TY 113 calls ref 112-26