MNI ASIA MARKETS ANALYSIS: Focus on Chair Powell, Jackson Hole

HIGHLIGHTS

- Treasuries look to finish weaker Thursday, off midday lows as markets set sites on Friday morning's speech by Fed Chairman Powell on the economy from the annual Jackson Hole economic symposium.

- Treasury yields climbed after mixed data, initially retreating after higher than expected weekly & continuing jobless claims, then rebounding after stronger than expected S&P Global flash PMI data.

- Hawkish comments from Cleveland Fed Hammack - that a rate cut at the next FOMC on September 17 is unlikely given current data.

US TSYS

MNI US TSYS: Treasury Yields Rise Ahead Jackson Hole Symposium

- Treasuries are holding weaker levels, off lows after the bell - inside session ranges followed mixed data with hawkish Fed comments setting the tone in the first half. Heavy overall volumes (TYU5 over 2.4M) due to quarterly futures roll and option hedging ahead Sep'25 expiry tomorrow, rather than active position taking.

- Many participants plied the sidelines ahead tomorrow's Jackson Hole economic symposium with Fed Chairman Powell speaking at 1000ET. The full Jackson Hole schedule will be released this evening (Thursday) at 2000ET (0100UK time early Friday morning), which will include the various academic paper presentations. The full Symposium website is here (which will include links to papers, livestreams, and schedule): https://www.kansascityfed.org/research/jackson-hole-economic-symposium/

- Treasuries gained following this morning's higher than expected weekly jobless and cointinuing claims: Initial claims increased to 235k (sa, cons 225k) in the week to Aug 16 – a payrolls reference period – after an unrevised 224k. Continuing claims meanwhile also surprised higher with 1972k (sa, cons 1960k) in the week to Aug 9 after a downward revised 1942k (initial 1953k).

- Cleveland Fed President Hammack (non-2025 FOMC voter but votes in 2026; hawk) echoes earlier commentary today from the sidelines of Jackson Hole from KC's Schmid (a fellow hawk) in casting doubt on the necessity of a September rate cut. "with the data I have right now, and with the information I have, if the meeting was tomorrow, I would not see a case for reducing interest rates."

- Weaker rates saw projected rate cuts continue to cool vs. early morning (*) levels: Sep'25 at -18bp (-19.6bp), Oct'25 at -30.1bp (-32.1bp), Dec'25 at -48bp (-51.4bp), Jan'26 at -58.6bp (-62.6bp).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.31% (-0.02), volume: $2.704T

- Broad General Collateral Rate (BGCR): 4.30% (-0.01), volume: $1.140T

- Tri-Party General Collateral Rate (TCR): 4.30% (-0.01), volume: $1.114T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $115B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $269B

FED Reverse Repo Operation

RRP usage slips to $25.358B this afternoon from $34.999B yesterday -- compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021. Total number of counterparties at 17. This week's retreat compares this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

While paired, SOFR & Treasury options still leaned toward upside call structures Thursday, looking to take advantage of more rate cuts than currently priced in for year end into March 2026. That said, hawkish comments from Cleveland Fed Hammack - that a rate cut at the next FOMC on September 17 is unlikely given current data saw projected rate cuts continue to cool vs. early morning (*) levels: Sep'25 at -18bp (-19.6bp), Oct'25 at -30.1bp (-32.1bp), Dec'25 at -48bp (-51.4bp), Jan'26 at -58.6bp (-62.6bp).

SOFR Options:

+15,000 SFRZ5 95.93/96.06/96.25/96.37 call condor w/ SFRZ5 95.93/96.06/96.18/96.31 call condor, 7.0-7.5

-10,000 0QZ5 96.75/97.00/97.50/97.75 call condors, 8.25 ref 96.87

+3,000 SFRZ5 96.12/96.25/96.62 4x4x3 broken call trees from 4.25-4.5

+10,000 SFRZ5 96.25 calls, 11.5 vs. 96.135/0.40%

Block, 8,000 SFRZ5 95.75 puts, 1.75 ref 96.16

+5,000 SFRZ5 96.37/96.50 call spds 2.75 ref 96.175

+15,000 0QH6/0QM6 97.50/98.00 call spd strip covered, 14.0 total

+15,000 SFRH6 97.25 calls, 6.0 (+60k yesterday)

-4,000 0QZ5 97.00/97.12 call spds, 4.0 vs. 96.875/0.08%

Block, 6,000 SFRU5 95.68/95.75/95.81 put flys, 0.75 net

3,600 SFRU5 95.81/95.87/96.00/96.06 call condors ref 95.8775

5,000 SFRZ5 96.25/96.50/97.00 broken call flys ref 96.18

2,000 SFRU5 95.87 straddles

14,000 SFRU5 96.00/96.12/96.25 call spds ref 95.88

1,500 SFRU5 95.68/95.75 3x1 put spds ref 95.88

2,000 SFRU5 95.81/95.87 put spds, 3.75 ref 95.8775

+3,000 SFRZ5 96.50/96.75 call spds, 2.75 ref 96.195

2,500 0QH6 97.62/98.12 call spds ref 96.91

Treasury Options: Reminder Sep'25 options expire tomorrow

Update -10,000 TYV5 111.5 straddles, 128-129

3,200 FVU5 108.5 puts, 4.5 ref 108-20

+15,000 FVU5 108.5/108.75 call over risk reversals, 0.5 vs. 108-20.25/0.5%

+7,000 USU5 116 calls, 2

3,000 TYV5 112/113/114 call flys ref 111-24

over 10,100 TYU5 111.5 puts, 5 last

2,000 TYU5 112.25/112.5/112.75 call flys ref 111-24

2,000 TYV5 112/113/114 call flys ref 111-26

2,100 TYV5 113 calls, 23 ref 111-27.5

1,000 TUV5 103.25/103.75 put spds ref 104-02.88

MNI BONDS: EGBs-GILTS CASH CLOSE: PMIs See Yields Rise

Strong global purchasing managers' indices released Thursday saw European yields reverse much of the prior session's fall.

- Rates sold off on stronger-than-expected Eurozone and UK August flash composite PMIs (though EZ Manufacturing beat with Services missing, whereas in the UK it was vice-versa). Latest UK monthly public finance data looked a little better than expected but was marred by revisions to the Apr-Jun data.

- Combined with very strong US PMIs combined with hawkish Fed-speak, there was plenty to keep the pressure on both ends of the yield curve through the cash close.

- The German curve leaned bear flatter, with underperformance in the belly, while Gilts underperformed overall in a bear-steepening move with 10Y the weakest segment.

- Periphery / semi-core EGB spreads widened steadily throughout the session as equities remained under pressure from the higher yield environment - 10Y BTP/Bund closed at its widest level in 13 sessions (Aug 4).

- The regional calendar includes Q2 Eurozone negotiated wage data, German final GDP, and French manufacturing confidence, with global attention on Federal Reserve Chair Powell's Jackson Hole speech on Friday (1500 UK time).

Closing Yields / 10-Yr EGB Spreads To Germany

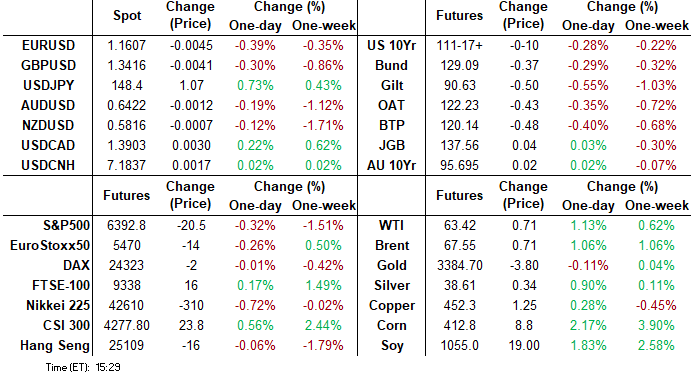

- Germany: The 2-Yr yield is up 3.9bps at 1.972%, 5-Yr is up 4.2bps at 2.315%, 10-Yr is up 4bps at 2.757%, and 30-Yr is up 3.3bps at 3.327%.

- UK: The 2-Yr yield is up 4.8bps at 3.97%, 5-Yr is up 4.8bps at 4.124%, 10-Yr is up 5.7bps at 4.729%, and 30-Yr is up 4.7bps at 5.578%.

- Italian BTP spread up 1.6bps at 82.4bps / French OAT up 1.2bps at 70.7bps

MNI OPTIONS: Mixed Schatz Structures, Bund And Sonia Put Flies Feature Thursday

Thursday's Europe rates/bond options flow included:

- DUX5 107.10/107.00/106.90/106.70p condor, bought for half in 8.5k

- DUX5 107.30/107.50cs vs 106.80p, bought the cs for half in 1k

- RXX5 126.5/125/123.5p fly, bought for 17 in 1.5k.

- SFIZ5 95.90/95.70/95.50p fly sold at 0.25 in ~5k

MNI FOREX: USD Index Extends Bounce as Chair Powell Awaited Friday

- Higher US yields in the aftermath of the stronger-than-expected US PMI data have helped propel USDJPY (+0.70%) comfortably back above the 148.00 handle on Thursday, taking the pair to a fresh weekly high.

- Above here, firm resistance to watch is at 148.52, the Aug 12 high, of which a breach would be viewed as a short-term bullish signal. The August 01 high at 150.92 remains key resistance. In terms of support, the August 14 low at 146.21 is the first notable level.

- A more stable session for equities has helped AUD and NZD to relatively outperform on Thursday, placing greater pressure on the likes of EUR and GBP, which have slipped in line with the USD index adjustment.

- For EURUSD, this has translated into weekly printed lows at 1.16, and further pressure being placed on 50-day EMA support. The average now intersects at 1.1591, and a clear break would threaten the underlying bullish trend structure, signalling scope for a deeper retracement towards key support at 1.1392, the Aug 1 low.

- In similar vein, GBPUSD looks set to extend its losing streak to four consecutive sessions, narrowing the gap to the August 11 low at 1.3400. Today’s price action looks set to confirm a break of the 50-day EMA, confirming the likely potential for a technical reversal.

- Downside in EURNOK (-0.86%) has persisted through the afternoon, which sees the cross down 0.8% today and testing key support at the 50-day EMA of 11.8298. Clearance of this level would expose the July 30 low at 11.7460

- Japan National CPI data is scheduled Friday before the global focus turns to Fed Chair Powell’s speech at Jackson Hole. UK and Canada retail sales data are also scheduled.

MNI FX OPTIONS: Expiries for Aug22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E700mln), $1.1660-75(E1.4bln)

- USD/JPY: Y147.90-00($1.9bln)

- USD/CAD: C$1.3685($646mln)

MNI US STOCKS: Late Equities Roundup: Tariffs Impacting Consumer Stock Earnings

- Stocks remain weaker late Thursday, SPX eminis retreating for the fifth consecutive session as investor focus turned to Friday morning's speech on the economy by Fed Chairman Powell at the annual economic symposium in Jackson Hole, WY.

- Currently, the DJIA trades down 146.38 points (-0.33%) at 44791.25, S&P E-Minis down 22.75 points (-0.35%) at 6390.5, Nasdaq down 84.5 points (-0.4%) at 21086.54.

- Consumer Staples and Discretionary sector stocks continued to lead the decline in the second half: weaker earnings tied to tariffs saw Walmart fall -4.88%, Costco Wholesale -2.48%, Target -2.12%, Dollar General -1.78% and Sysco -1.40%.

- Underperforming discretionary stocks included: Norwegian Cruise Line -1.97%, Royal Caribbean Cruises -1.86%, Williams-Sonoma -1.60% and DR Horton -1.38%.

- On the positive side, Energy and Health Care sector shares continued to lead gainers, oil and gas stocks buoyed as crude prices added to mid-week gains (WTI +.88 at 63.59): Baker Hughes +2.03%, Schlumberger +1.77%, APA +1.72%, EQT +1.60% and Chevron +1.59%.

- Meanwhile, pharmaceuticals supported the Health Care sector: Merck & Co +2.54%, Humana +2.14%, Pfizer +1.91% and UnitedHealth Group +1.76%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6600.00 Round number resistance

- RES 3: 6554.98 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6508.75 High Aug 15 and all-time High

- PRICE: 6384.25 @ 14:45 BST Aug 21

- SUP 1: 6362.75 Low Aug 20

- SUP 2: 6313.25 Low Aug 6

- SUP 3: 6287.15 50-day EMA

- SUP 4: 6239.50 Low Aug 1

The dominant uptrend in S&P E-Minis remains intact and the latest shallow retracement appears to be a correction. Moving average studies remain in a bull-mode position, highlighting a clear uptrend and positive market sentiment. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6403.75, the 20-day EMA (pierced), and 6287.15, the 50-day EMA.

MNI COMMODITIES: Crude Extends Gains, Gold Edges Lower Ahead Of Chair Powell

- Crude is trading higher again today, extending Wednesday’s rally, as ongoing uncertainty around progress towards a peace deal in Ukraine is weighed against market oversupply risks.

- WTI Oct 25 is up by 1.3% at $63.5/bbl.

- President Trump seemingly hinted at increased military support for Ukraine in a Truth Social post amid an ebb in optimism that the White House will deliver substantial progress towards a Ukraine peace agreement.

- Despite today’s gains, a bear cycle in WTI futures remains intact and the contract continues to trade closer to its recent lows. A key support at $61.29, the Jun 30 low, has been breached, and a continuation lower would open $57.71, the May 30 low.

- Initial resistance to watch is $63.85, the 50-day EMA, with key short-term resistance at $69.36, the Jul 30 high.

- Meanwhile, spot gold has edged down by 0.3% to $3,339/oz, as the USD index bounce extended after stronger-than-expected US PMI data and the market awaits Fed Chair Powell’s speech at Jackson Hole on Friday.

- Powell is unlikely to clearly signal a September cut, given the split in the Committee on the need to cut rates. Instead, he will likely leave the door open to a September cut, but not as overtly as some may think.

- Despite the latest pullback, a bull cycle in gold remains intact. A resumption of gains would open $3,439.0, the Aug 23 high. On the downside, first support to watch lies at $3,268.2, the Jul 30 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 22/08/2025 | 0600/0800 | ** | Unemployment | |

| 22/08/2025 | 0600/0800 | *** | GDP (f) | |

| 22/08/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/08/2025 | 0900/1100 | Q2 Negotiated Wage Growth | ||

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1400/1000 | Fed Chair Jerome Powell | ||

| 22/08/2025 | 1400/1000 | *** | US Fed Chair Speech | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 22/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |